Discussion

Just having a play with FIRECalc.

Obviously it's geared up for the US but has anyone used it (or similar) to do any broad assumptions/sanity checks about when they might be able to stop working (with the option of always doing something later if they wanted to) without s tting bricks about running out of money?

tting bricks about running out of money?

Obviously it's geared up for the US but has anyone used it (or similar) to do any broad assumptions/sanity checks about when they might be able to stop working (with the option of always doing something later if they wanted to) without s

tting bricks about running out of money?Great website. Thanks for sharing!

I put some simple numbers in to begin with and was very happy to see that I got 100% success and a lot of surplus. Then I realised that some of the numbers I‘d put in didn‘t really reflect the nuances of our plan and at one point got a scare when it said only 69% success. And then I realised there are a lot of parameters that you can play with to reflect your personal situation and have got it to 98.9% success when retiring in 10 years (at 50) and living for 50 years…

I think I need to spend a bit more time with it though, as it‘s looking like the dog‘s home is going to get quite the endowment.

ETA and now I‘ve spotted another parameter to play with we‘re potentially back at 85% success. Hmmm….

I put some simple numbers in to begin with and was very happy to see that I got 100% success and a lot of surplus. Then I realised that some of the numbers I‘d put in didn‘t really reflect the nuances of our plan and at one point got a scare when it said only 69% success. And then I realised there are a lot of parameters that you can play with to reflect your personal situation and have got it to 98.9% success when retiring in 10 years (at 50) and living for 50 years…

I think I need to spend a bit more time with it though, as it‘s looking like the dog‘s home is going to get quite the endowment.

ETA and now I‘ve spotted another parameter to play with we‘re potentially back at 85% success. Hmmm….

Edited by eyebeebe on Saturday 1st May 20:20

Edited by eyebeebe on Saturday 1st May 20:21

I've played with https://engaging-data.com/will-money-last-retire-e... a fair bit.

I prefer it as it reminds me that while working longer reduces the risk of running out of money, it brings the nasty grey area closer.

I prefer it as it reminds me that while working longer reduces the risk of running out of money, it brings the nasty grey area closer.

Thanks, and yes the parameters are the interesting things for obvious reasons

I've not yet found a way of being able to guess how much a DC pension might be worth in X years time if you stop contributions though.

Do people just make an assumption around compound interest and see what that throws out then assume 4% SWR or something?

This isn't "serious" planning this is just a bit of what if.

I've not yet found a way of being able to guess how much a DC pension might be worth in X years time if you stop contributions though.

Do people just make an assumption around compound interest and see what that throws out then assume 4% SWR or something?

This isn't "serious" planning this is just a bit of what if.

I found this one which is probably less configurable than the Firecalc one & again uses American data:

https://engaging-data.com/will-money-last-retire-e...

I particularly like the Wedge of Death; for me it forcasts that at 80 I have 0% chance of being broke but 50% chance of being dead.

He has a few other calculators lower down on the page.

https://engaging-data.com/early-retirement-calcula...

Another free one - seems very configurable & updated recently:

https://cfiresim.com/

https://www.tidewaywealth.co.uk/s/26/calculators

As far as I can see any equivalents that use British data are pay only & meant to be used by IFAs & the like:

https://www.timelineapp.co/

https://www.planwithvoyant.co.uk/content/en_GB/ind...

https://engaging-data.com/will-money-last-retire-e...

I particularly like the Wedge of Death; for me it forcasts that at 80 I have 0% chance of being broke but 50% chance of being dead.

He has a few other calculators lower down on the page.

https://engaging-data.com/early-retirement-calcula...

Another free one - seems very configurable & updated recently:

https://cfiresim.com/

https://www.tidewaywealth.co.uk/s/26/calculators

As far as I can see any equivalents that use British data are pay only & meant to be used by IFAs & the like:

https://www.timelineapp.co/

https://www.planwithvoyant.co.uk/content/en_GB/ind...

I wish there was UK based FIRE calc, which better aligns with typical UK profile, more in property, state pensions and benefits.

US has lots of resources but not always that relevant. For instance, property taxes are very different.

Also it feels odd moving the 'stock return' slider just a little bit left or right and seeing my life plan morph so dramatically in front of my eyes .

US has lots of resources but not always that relevant. For instance, property taxes are very different.

Also it feels odd moving the 'stock return' slider just a little bit left or right and seeing my life plan morph so dramatically in front of my eyes .

Those links are going to keep me busy ^^

I've also used : https://www.retireeasy.co.uk/ which allows a lot of inputs and graphically does a good job of explaining the results but it assumes constant growth every year which we know never happens in reality.

I tried writing my own simplified spreadsheet just to get my head around the standard deviation of every year (simply based on Vanguard's forecast), running it 50x to show the spread. With the usual inputs to play with to see how if effects things. Actually found it useful to get my head around a few things so I'd recommend having a go at doing the same thing.

https://i.imgur.com/JEaaPBH.jpg

I've got about 18 months to go before I intend to jump and in that time I doubt I'll ever convince myself that I've fully understood the full risk but, then again, I can't see how anyone can....

I've also used : https://www.retireeasy.co.uk/ which allows a lot of inputs and graphically does a good job of explaining the results but it assumes constant growth every year which we know never happens in reality.

I tried writing my own simplified spreadsheet just to get my head around the standard deviation of every year (simply based on Vanguard's forecast), running it 50x to show the spread. With the usual inputs to play with to see how if effects things. Actually found it useful to get my head around a few things so I'd recommend having a go at doing the same thing.

https://i.imgur.com/JEaaPBH.jpg

I've got about 18 months to go before I intend to jump and in that time I doubt I'll ever convince myself that I've fully understood the full risk but, then again, I can't see how anyone can....

mids said:

Those links are going to keep me busy ^^

I've also used : https://www.retireeasy.co.uk/ which allows a lot of inputs and graphically does a good job of explaining the results but it assumes constant growth every year which we know never happens in reality.

I tried writing my own simplified spreadsheet just to get my head around the standard deviation of every year (simply based on Vanguard's forecast), running it 50x to show the spread. With the usual inputs to play with to see how if effects things. Actually found it useful to get my head around a few things so I'd recommend having a go at doing the same thing.

https://i.imgur.com/JEaaPBH.jpg

I've got about 18 months to go before I intend to jump and in that time I doubt I'll ever convince myself that I've fully understood the full risk but, then again, I can't see how anyone can....

I'm presuming you're looking to bridge the gap to a pension? Have you you've looked at https://monevator.com/should-you-use-cash-to-bridg... ?I've also used : https://www.retireeasy.co.uk/ which allows a lot of inputs and graphically does a good job of explaining the results but it assumes constant growth every year which we know never happens in reality.

I tried writing my own simplified spreadsheet just to get my head around the standard deviation of every year (simply based on Vanguard's forecast), running it 50x to show the spread. With the usual inputs to play with to see how if effects things. Actually found it useful to get my head around a few things so I'd recommend having a go at doing the same thing.

https://i.imgur.com/JEaaPBH.jpg

I've got about 18 months to go before I intend to jump and in that time I doubt I'll ever convince myself that I've fully understood the full risk but, then again, I can't see how anyone can....

bhstewie said:

hstewie said: I've not yet found a way of being able to guess how much a DC pension might be worth in X years time if you stop contributions though.

.

Isn't that going to depend entirely on what assets are in it? If it's an equity/bond mix (without the "joy" some have of commercial property), I'd be tempted to see which LifeStrategy fund it most closely resembles and look at their return figures, subtracting whatever the management fees are..

Problem with any kind of projection at present is it seems likely that the economic stats are going to bounce all over the place post covid, so there may well be some good and some utterly terrible years ahead, even more so than usual with equities.

xeny said:

I'm presuming you're looking to bridge the gap to a pension? Have you you've looked at https://monevator.com/should-you-use-cash-to-bridg... ?

Yes, I see that as the biggest unknown/challenge so have spent most of my time trying to get my head around that stage of the plan. Thanks for the link.aparna said:

Also it feels odd moving the 'stock return' slider just a little bit left or right and seeing my life plan morph so dramatically in front of my eyes .

This is why driving down fees is often emphasised heavily. There's little you can do to increase stock return, but reducing fees has much the same effect.mids said:

Yes, I see that as the biggest unknown/challenge so have spent most of my time trying to get my head around that stage of the plan. Thanks for the link.

I'd guess use cash to get to 55, and then a SIPP between there and your "main" pension? Interesting question is the asset allocation for the SIPP?Edited by xeny on Sunday 2nd May 15:04

Yep, that's the plan.

The thing about retiring early is that there's still (probably) plenty of time to recover from market wobbles so I don't feel it's the right thing to be as 'safe' with the savings as you would be when retiring at 65. My SIPP (to take me from 55 to 65) is with Vanguard and mainly still in global equities rather than piling into bonds/retirement funds.

The thing about retiring early is that there's still (probably) plenty of time to recover from market wobbles so I don't feel it's the right thing to be as 'safe' with the savings as you would be when retiring at 65. My SIPP (to take me from 55 to 65) is with Vanguard and mainly still in global equities rather than piling into bonds/retirement funds.

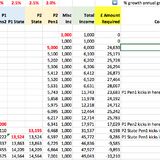

I've got my own spreadsheet to figure things out - pm me if you would like a 'sanitised' version. Essentially looks something like this:

I also ran FIREcalc and cfiresim as well for a little comfort.

I quite like the one at https://whatapalaver.co.uk/retirement-planning-cou... to help figure things out too.

I'm always very conscious that this is a combination of science and guesswork, in proportions that we also cannot predict

How many people predicted Covid, & the impact on lifestyles (& markets)? How many accurately predict their own 'death date' !!

I'm now moving into the 'decummulation phase', so might have more real-world knowledge in a year or two....until then, feel free to ignore anything I wrote above

I also ran FIREcalc and cfiresim as well for a little comfort.

I quite like the one at https://whatapalaver.co.uk/retirement-planning-cou... to help figure things out too.

I'm always very conscious that this is a combination of science and guesswork, in proportions that we also cannot predict

How many people predicted Covid, & the impact on lifestyles (& markets)? How many accurately predict their own 'death date' !!

I'm now moving into the 'decummulation phase', so might have more real-world knowledge in a year or two....until then, feel free to ignore anything I wrote above

mids said:

FIRE is about retiring early, often well before your pension is available.

AKA sacrificing your enjoyment now to buy time later, at which point you won't have enough money to really enjoy yourself then either! Alright if you like walking or gardening I guess, but surely preferably to find a job you enjoy and retire at a normal age?

Condi said:

AKA sacrificing your enjoyment now to buy time later, at which point you won't have enough money to really enjoy yourself then either!

Alright if you like walking or gardening I guess, but surely preferably to find a job you enjoy and retire at a normal age?

What's a normal age, and why is that age the normal age?Alright if you like walking or gardening I guess, but surely preferably to find a job you enjoy and retire at a normal age?

Condi said:

AKA sacrificing your enjoyment now to buy time later, at which point you won't have enough money to really enjoy yourself then either!

Alright if you like walking or gardening I guess, but surely preferably to find a job you enjoy and retire at a normal age?

Why retire at a normal age why not retire older younger or at the age that would be normal or say take a decade “off” retiring then go back to work and work later. Alright if you like walking or gardening I guess, but surely preferably to find a job you enjoy and retire at a normal age?

Freedom is there the only constraints are you need to find your existence. The rest is frankly for the birds.

Surely people have no judgement on what other individuals choose to do/when they retire or don’t.

Gassing Station | Finance | Top of Page | What's New | My Stuff