These fifty grand loans

Discussion

jammy-git said:

gizlaroc said:

I wish they had done it for £100k.

I would have restructured my borrowings.

Not sure if it is worth me borrowing another £50k. Problem is it disappears and you are left with £1000 a month going out.

50k just "disappears"? Me and you lead very different lives!I would have restructured my borrowings.

Not sure if it is worth me borrowing another £50k. Problem is it disappears and you are left with £1000 a month going out.

Now of course, I would hope to do some business when we open, but my concern is taking on more debt and still not surviving.

If that happens who will come first come payout? The bank or Funding circle who I am guaranteeing with my home? Or this loan?

It is very easy for £50k to just be eaten up, I could in theory pay that out on day one to suppliers and still be left with £40k of invoices due and payment holiday payments to be cleared.

Sure it would make the next 3 months (clothing game so work in seasons) easier, but then we are into a new season, we would get to the end of that and need to start paying that £50K back.

The loan is 5 years, at 4% apr that means you get 12 month holiday and then 48 x £1150 a month roughly.

Not sure business will have picked up enough by then for that not to put pressure on us.

I guess the answer is, take the loan, and just consider that for the next 5 years I will take £14k a year less or I think what I may do is take the £50k, pay off my Funding Circle loan of £64k and then apply again for a smaller loan from them, around £30k over 60 months, which will be around £550. So roughly what we are paying now.

We borrowed £90k from them over 60 months at roughly £1730 a month, so that would keep the monthlies similar with a small cash injection of £16000 and it would take away the guarantees from ourselves, which would be nice.

I got this today from my accountant's firm:

In a welcome boost, small businesses owners can get from £2,000 to £50,000 “within days” from the Government’s brand new Bounce Back Loans scheme.

On 27 April 2020, Chancellor Rishi Sunak announced the new scheme, adding to the existing support for small businesses affected by coronavirus.

The Government is giving accredited lenders a 100% guarantee for the loans, and aiming to deliver loans through this scheme as quickly as possible.

What’s available?

You can borrow between £2,000 and £50,000, with a cap of 25% of your annual turnover.

The Chancellor stated you can get the cash “within days” but the scheme won’t open until Monday 4 May 2020.

Are you eligible?

You can apply for a loan if your business:

- is based in the UK

- has been negatively affected by coronavirus

- was not an ‘undertaking in difficulty’ on 31 December 2019

PSC contractors will be eligible, as will most one-man limited companies. We know you’ve been left behind by the Government’s COVID-19 support measures so far, and this is your opportunity to access some much needed funds to ensure your business survival beyond the lockdown.

Are the loans interest-free?

No, but for the first 12 months, you won’t pay any interest and you won’t have to make any repayments.

You won’t pay an arrangement fee or early repayment charges – the Government will cover any fees as well as your interest for the first 12 months.

The Government is negotiating with lenders to make sure that for the rest of the term of the loans, borrowers pay a low standardised rate of interest.

How do you apply for a Bounce Back Loan?

The scheme will open for applications on Monday 4 May 2020. To apply, you’ll fill in a short online form.

Where can you get a Bounce Back Loan?

The scheme will be available through a network of accredited lenders and, as with CBILS, we are recommending the first port of call should perhaps be your existing business bank.

What can you use the loan for?

As far as we can see, so far there is no restriction on the use of the loan, and we see it as being sensible to use this as a contingency fund. Remember that there are no charges, interest or repayments required in the first year.

If your business is in financial difficulties at the moment, then having access to the funds may be the lifeline you need until the crisis is over and your business is back earning.

Alternatively, if your business is not yet feeling the effects of lockdown, is not yet in financial distress, but it could be in the next few months, then having up to 25% of your turnover sitting in the bank could provide you with the buffer you need to keep going. If you don’t need it, don’t use it, and pay it back before the interest charging period starts.

In a welcome boost, small businesses owners can get from £2,000 to £50,000 “within days” from the Government’s brand new Bounce Back Loans scheme.

On 27 April 2020, Chancellor Rishi Sunak announced the new scheme, adding to the existing support for small businesses affected by coronavirus.

The Government is giving accredited lenders a 100% guarantee for the loans, and aiming to deliver loans through this scheme as quickly as possible.

What’s available?

You can borrow between £2,000 and £50,000, with a cap of 25% of your annual turnover.

The Chancellor stated you can get the cash “within days” but the scheme won’t open until Monday 4 May 2020.

Are you eligible?

You can apply for a loan if your business:

- is based in the UK

- has been negatively affected by coronavirus

- was not an ‘undertaking in difficulty’ on 31 December 2019

PSC contractors will be eligible, as will most one-man limited companies. We know you’ve been left behind by the Government’s COVID-19 support measures so far, and this is your opportunity to access some much needed funds to ensure your business survival beyond the lockdown.

Are the loans interest-free?

No, but for the first 12 months, you won’t pay any interest and you won’t have to make any repayments.

You won’t pay an arrangement fee or early repayment charges – the Government will cover any fees as well as your interest for the first 12 months.

The Government is negotiating with lenders to make sure that for the rest of the term of the loans, borrowers pay a low standardised rate of interest.

How do you apply for a Bounce Back Loan?

The scheme will open for applications on Monday 4 May 2020. To apply, you’ll fill in a short online form.

Where can you get a Bounce Back Loan?

The scheme will be available through a network of accredited lenders and, as with CBILS, we are recommending the first port of call should perhaps be your existing business bank.

What can you use the loan for?

As far as we can see, so far there is no restriction on the use of the loan, and we see it as being sensible to use this as a contingency fund. Remember that there are no charges, interest or repayments required in the first year.

If your business is in financial difficulties at the moment, then having access to the funds may be the lifeline you need until the crisis is over and your business is back earning.

Alternatively, if your business is not yet feeling the effects of lockdown, is not yet in financial distress, but it could be in the next few months, then having up to 25% of your turnover sitting in the bank could provide you with the buffer you need to keep going. If you don’t need it, don’t use it, and pay it back before the interest charging period starts.

JPJPJP said:

I'm wondering how well funding circle comes through this. It seemed to be in reasonable shape pre covid 19.

It is a weird one, all the lenders are individual investors, they are told that there is no guarantee on their investment, they are given everyones accounts and told the interest rate based on risk, so it is a gamble that they know they can lose on. So I guess they won't get hit? Other than many of the investors may get burnt and not invest going forward, if too many chose that route it is collapse.

"We know you’ve been left behind by the Government’s COVID-19 support measures so far"

The grants, furlough freebies and self-employed £2.5k a month handout whilst you can still conduct your day job?

Ah, a loan, to kick the can down the road. Ta muchly. I think I would rather just close up now. Whole thing is a f king mismanaged joke.

king mismanaged joke.

The grants, furlough freebies and self-employed £2.5k a month handout whilst you can still conduct your day job?

Ah, a loan, to kick the can down the road. Ta muchly. I think I would rather just close up now. Whole thing is a f

king mismanaged joke. Shnozz said:

"We know you’ve been left behind by the Government’s COVID-19 support measures so far"

The grants, furlough freebies and self-employed £2.5k a month handout whilst you can still conduct your day job?

Ah, a loan, to kick the can down the road. Ta muchly. I think I would rather just close up now. Whole thing is a fking mismanaged joke.

Not really. The grants, furlough freebies and self-employed £2.5k a month handout whilst you can still conduct your day job?

Ah, a loan, to kick the can down the road. Ta muchly. I think I would rather just close up now. Whole thing is a f

king mismanaged joke. Many businesses owe suppliers, who will not supply further until current invoices are settled.

This gives you a chance to get those invoices settled and carry on trading, paying back those invoices over 60 (or maybe it is 72 months?) with a 12 month break while business picks up again.

I guess it depends what it is you do, but for many this will be a life saver.

Think of it this way, if the suppliers said "Don't worry about the invoices due now, we can spread that over the next 60 months, and just start again as normal, will that help?" I bet 99% of companies would say "yeah.".

Depends on your POV, but for many small businesses, they've not qualified for the grants, they need people working so can't furlough and not self-employed. So far, they've had no help from the government. So whilst everyone else is getting free hand-outs, small and micro businesses are getting debt.

I don't see what you're getting at there in relation to what I posted?

I'm a micro business on every level btw.

We did get some grant, but we are building up debt like 80% of UK business is.

Surely, if you can still trade and don't need to furlough staff then you still have an income?

It is crap for everyone, unless you are in the food game.

I'm a micro business on every level btw.

We did get some grant, but we are building up debt like 80% of UK business is.

Surely, if you can still trade and don't need to furlough staff then you still have an income?

It is crap for everyone, unless you are in the food game.

mondeoman said:

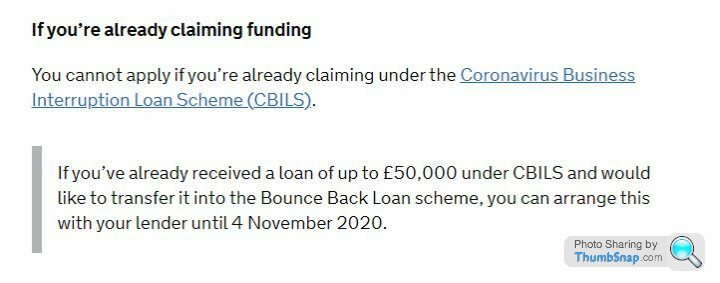

Just wondering if you can have a CBILs loan AND one of these?

https://www.gov.uk/guidance/apply-for-a-coronaviru...

I don’t suppose anyone knows how the the 25% of turnover is assessed, do they work off your last set of filed accounts, in our case 2018/2019 as many won’t have done 2019/2020 yet? Will they take an average of passed years?

Out year end is 31st Dec so I have until September to do 2019 accounts, hope they don’t want them.

Out year end is 31st Dec so I have until September to do 2019 accounts, hope they don’t want them.

The loan offered will probably be a maximum of 25% of your turnover, or 2 x PAYE salaries of the company (whichever is the lower) up to a max of £50k.

It'll be based on your last set of filed accounts I would have thought

The max loans offered seems to be a condition of the CBILS and I can see it being mirrored onto this scheme.

We'll have to see what next week brings. On paper it could plug a huge hole that the CBILS leaves.....

It'll be based on your last set of filed accounts I would have thought

The max loans offered seems to be a condition of the CBILS and I can see it being mirrored onto this scheme.

We'll have to see what next week brings. On paper it could plug a huge hole that the CBILS leaves.....

JPJPJP said:

I applied for a CBILS through Santander and they emailed me earlier in the week to fill in another security/compliance form but I've deleted the email as went in spam. I am not wanting the CBILS and would rather the new one out on Monday. I can't get hold of anyone on the phone at Santander so am just going to apply for the bounce back loan. Hopefully they'll just disregard my old application as it wasn't completed fully and process the bounce back. Out of interest if you apply for one of these loans does it have to be through your own bank or can you use another?

I was just about to make a start on returning to co op bank before all this kicked off. My current bank will probably turn what should be any easy process into a lot of hassle and hoop jumping.

I was just about to make a start on returning to co op bank before all this kicked off. My current bank will probably turn what should be any easy process into a lot of hassle and hoop jumping.

Treasury has done as much as it can: 2.4% spread to the banks, 100% guarantee, not really included in risk weighting

It is over to the commercial banks now. Unless they really do just quickly push this money out of the door to pretty much every business that applies, they aren't going with the spirit of the Chancellor's intentions imo

It is over to the commercial banks now. Unless they really do just quickly push this money out of the door to pretty much every business that applies, they aren't going with the spirit of the Chancellor's intentions imo

If that is correct and it's going to work out at 2.5% Max then I'm seriously tempted. I'd rather not take on any debt if avoidable but I'd only be wanting around £15k and at those interest rates it's something of a bargain.

I just have to weigh up the risk of taking on 15 grands worth of debt against the the chance I might still have to fold the business in a few months time anyway and end up in a worse place overall.

So far seems to be no mention of personal guarantees, which is good and they shouldn't be required on a 100% backed loan anyway.

It's quite a scary balancing act right now. I could really do with some additional working capital to keep the lights on but I'm also conscious that, as a director, I have to act in the most financially responsible manner possible in order to avoid any comeback if I have to wind the business up further down the road.

I just have to weigh up the risk of taking on 15 grands worth of debt against the the chance I might still have to fold the business in a few months time anyway and end up in a worse place overall.

So far seems to be no mention of personal guarantees, which is good and they shouldn't be required on a 100% backed loan anyway.

It's quite a scary balancing act right now. I could really do with some additional working capital to keep the lights on but I'm also conscious that, as a director, I have to act in the most financially responsible manner possible in order to avoid any comeback if I have to wind the business up further down the road.

Fubar1977 said:

If that is correct and it's going to work out at 2.5% Max then I'm seriously tempted. I'd rather not take on any debt if avoidable but I'd only be wanting around £15k and at those interest rates it's something of a bargain.

I just have to weigh up the risk of taking on 15 grands worth of debt against the the chance I might still have to fold the business in a few months time anyway and end up in a worse place overall.

So far seems to be no mention of personal guarantees, which is good and they shouldn't be required on a 100% backed loan anyway.

It's quite a scary balancing act right now. I could really do with some additional working capital to keep the lights on but I'm also conscious that, as a director, I have to act in the most financially responsible manner possible in order to avoid any comeback if I have to wind the business up further down the road.

You sound exactly who this loan is aimed at. You should take as much as you can get. There is nothing at all to pay for 12 months, so this time next year, pay off what you haven't used and work at the rest over the next few years. It's by far the cheapest form of borrowing. I just have to weigh up the risk of taking on 15 grands worth of debt against the the chance I might still have to fold the business in a few months time anyway and end up in a worse place overall.

So far seems to be no mention of personal guarantees, which is good and they shouldn't be required on a 100% backed loan anyway.

It's quite a scary balancing act right now. I could really do with some additional working capital to keep the lights on but I'm also conscious that, as a director, I have to act in the most financially responsible manner possible in order to avoid any comeback if I have to wind the business up further down the road.

I intend to clear my overdraft (10% over base) and sit on the rest as back up.

fridaypassion said:

Out of interest if you apply for one of these loans does it have to be through your own bank or can you use another?

I was just about to make a start on returning to co op bank before all this kicked off. My current bank will probably turn what should be any easy process into a lot of hassle and hoop jumping.

I was trying to find this out too. I was just about to make a start on returning to co op bank before all this kicked off. My current bank will probably turn what should be any easy process into a lot of hassle and hoop jumping.

Lloyd’s say you have to be an account holder and Barclays you have to apply through online banking so worried you can only apply with your main bank, and if that’s the case I get the feeling it’s not going to be as easy as the government are stating...

Gassing Station | Business | Top of Page | What's New | My Stuff