GT4 fast road brake pads - PFC's and which compound

Discussion

TDT said:

Ref STs.., as you know… Primary Porsche audience is PCCB replacement… so why not produce at the same size as OEM

The development costs are then amortised further by being able to resolve for Steel upgrade also, with just adding calliper spacer rather than having to calculate if 380mm CCST would work…

Also they probably don’t see calliper down spacing as their problem… so fine they make a smaller spacer for Steel rotors… for say a 400mm rotor for the front… probably not worth it in their eyes… seeing as they seemingly wont even help at all with spare bells for people to convert from ‘Turbo hub’ to ‘GT3 Hub’ which might be a larger use case and actually would cost them nothing, apart from advice, and would be some additional revenue/product line.

Just boils down to business.

The main issue with 9x1 and prior steel rotors is the cracking due to full cross-drilling. So you ‘might’ end up needing to change them frequently, in a heavy track usage scenario.

The 9x2 rotors such as on 992 GT3/RS and 4RS are only dimpled… so cracking risk is heavily reduced and the rotor much more durable.

Brakes (pads/rotors) are a consumable, so just depends on how/when you want to spend.

Just seen this ....The development costs are then amortised further by being able to resolve for Steel upgrade also, with just adding calliper spacer rather than having to calculate if 380mm CCST would work…

Also they probably don’t see calliper down spacing as their problem… so fine they make a smaller spacer for Steel rotors… for say a 400mm rotor for the front… probably not worth it in their eyes… seeing as they seemingly wont even help at all with spare bells for people to convert from ‘Turbo hub’ to ‘GT3 Hub’ which might be a larger use case and actually would cost them nothing, apart from advice, and would be some additional revenue/product line.

Just boils down to business.

The main issue with 9x1 and prior steel rotors is the cracking due to full cross-drilling. So you ‘might’ end up needing to change them frequently, in a heavy track usage scenario.

The 9x2 rotors such as on 992 GT3/RS and 4RS are only dimpled… so cracking risk is heavily reduced and the rotor much more durable.

Brakes (pads/rotors) are a consumable, so just depends on how/when you want to spend.

Edited by TDT on Sunday 28th April 10:03

Maybe this is why Surface Transform are trying to sell what they can sell as complete kits ?

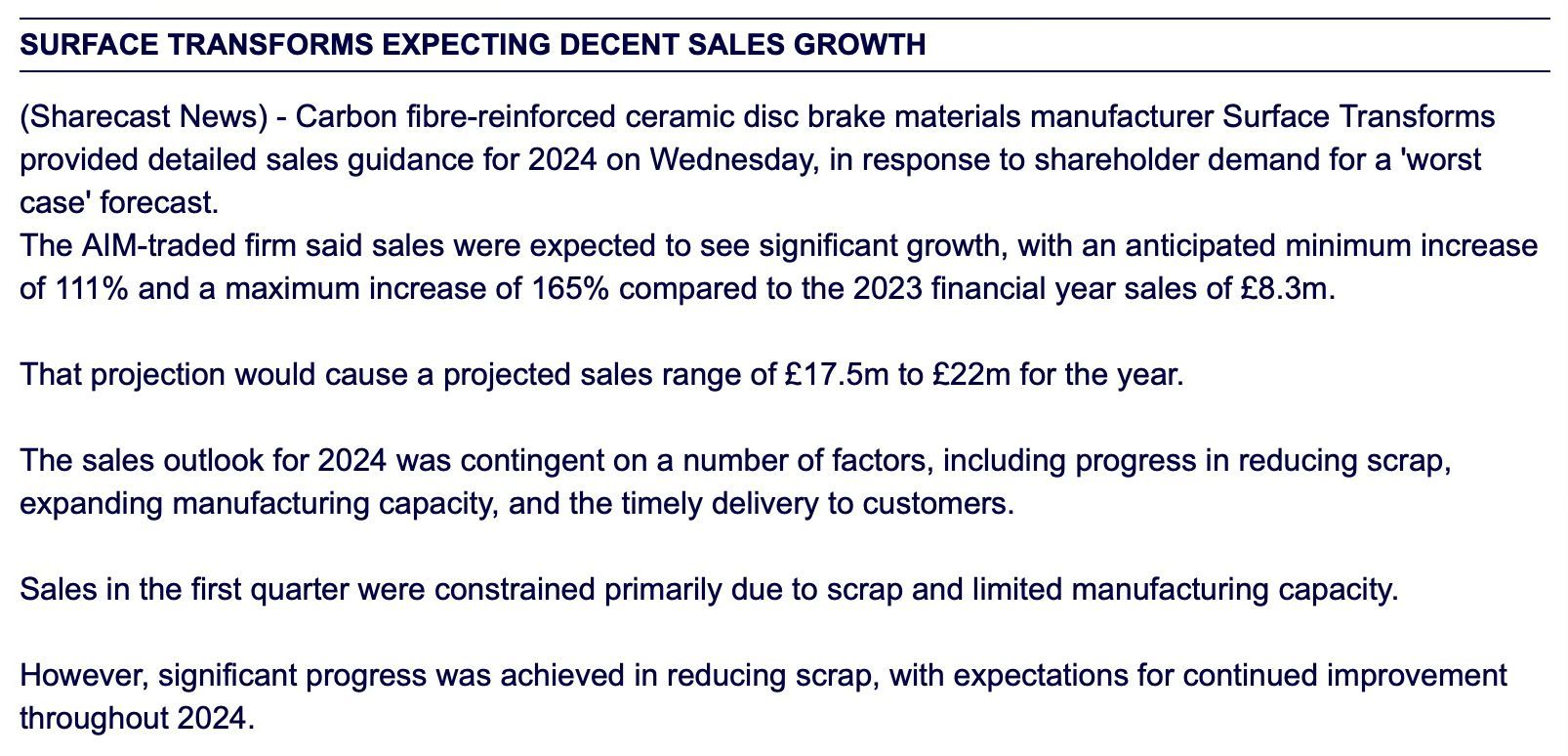

There is more reading in the recent update if you care to look ....

Definitely the major part of the picture - drive sales volume as much as possible.

As per any other business.

Share price has taken a massive hit.. but that isn't a reflection on the product... more just the ST board ability to met shareholder targets that they set - with a technically challenge product with a lot of seeming headwind. Every report I've seen from them says the same thing.

Quarter after quarter... manage scrap, scale capacity.

As per any other business.

Share price has taken a massive hit.. but that isn't a reflection on the product... more just the ST board ability to met shareholder targets that they set - with a technically challenge product with a lot of seeming headwind. Every report I've seen from them says the same thing.

Quarter after quarter... manage scrap, scale capacity.

Edited by TDT on Monday 29th April 16:37

There is no doubt that the product is superb ... and I guess they know why they need "process" for apparently ordinary things, but it doesn't come-over currently as being very customer focussed. Maybe their hands are so tied.

It's also now a concern if the arithmetic makes sense with refurbishments that may not be available ... at the moment I would suggest to anybody that a refurbishment would be a bonus and to base a purchasing decision on single life use ... 50 fast trackways and five sets of pads versus the alternative ?

To be fair, PCCB's potentially finished at 30? fast trackdays and eight or nine sets of pads would offer a reasonable comparison.

Less determined drivers will obviously get more on both ... but this may no longer be the "no-brainer" that it was.

It's also now a concern if the arithmetic makes sense with refurbishments that may not be available ... at the moment I would suggest to anybody that a refurbishment would be a bonus and to base a purchasing decision on single life use ... 50 fast trackways and five sets of pads versus the alternative ?

To be fair, PCCB's potentially finished at 30? fast trackdays and eight or nine sets of pads would offer a reasonable comparison.

Less determined drivers will obviously get more on both ... but this may no longer be the "no-brainer" that it was.

TDT said:

Definitely the major part of the picture - drive sales volume as much as possible.

As per any other business.

Share price has taken a massive hit.. but that isn't a reflection on the product... more just the ST board ability to met shareholder targets that they set - with a technically challenge product with a lot of seeming headwind. Every report I've seen from them says the same thing.

Quarter after quarter... manage scrap, scale capacity.

The share price was around 20 times higher in 2021! They must have been some very big promises/targets...As per any other business.

Share price has taken a massive hit.. but that isn't a reflection on the product... more just the ST board ability to met shareholder targets that they set - with a technically challenge product with a lot of seeming headwind. Every report I've seen from them says the same thing.

Quarter after quarter... manage scrap, scale capacity.

ChrisW. said:

Surface Transforms share price now below 1p ...

I looked at Alcon but no Porsche equivalents ... GiroDisc with their caliper mod to avoid the claimed risk of stripping the mounting thread on the "expensive" upright ?

They've just announced a significant fundraising at 1p per share...I looked at Alcon but no Porsche equivalents ... GiroDisc with their caliper mod to avoid the claimed risk of stripping the mounting thread on the "expensive" upright ?

https://polaris.brighterir.com/public/surface_tran...

Well I hope they make it ... I have been delighted with the quality of the product ... I've just been bound up in their obvious struggles this year ...

From the prospectus my concern would be the origin of the contacts in place that they are depending upon ... Aston Martin ? McLaren ? ... life is a mystery !

From the prospectus my concern would be the origin of the contacts in place that they are depending upon ... Aston Martin ? McLaren ? ... life is a mystery !

ChrisW. said:

Well I hope they make it ... I have been delighted with the quality of the product ... I've just been bound up in their obvious struggles this year ...

From the prospectus my concern would be the origin of the contacts in place that they are depending upon ... Aston Martin ? McLaren ? ... life is a mystery !

They talk about nearly £400m of contracts, so surely that implies they have contracts with all the super car manufacturers?From the prospectus my concern would be the origin of the contacts in place that they are depending upon ... Aston Martin ? McLaren ? ... life is a mystery !

They also talk about breaking into the EV market.

I'd be amazed if they fail within 18 months - that would mean their advisors, directors and investors didn't do their due diligence on this fundraise and could face further consequences.

BandOfBrothers said:

They've just announced a significant fundraising at 1p per share...

https://polaris.brighterir.com/public/surface_tran...

This is a second fund raising round in the last 24 months, first also involved shareholder dilution, which is partially why the share price is in the toilet. https://polaris.brighterir.com/public/surface_tran...

Losses in 22, bigger losses in 23, 24 is apparently the point they’ll turn it around with healthy profits in ‘25. However for shareholders ST have been a perpetual jam tomorrow situation for many years.

ST are in the process of scaling volumes due to demand. The first funding round in ‘22 was supposed to provide all the capital needed for the scaling project.

Some of losses come from this scaling and production not being up to scratch quality wise. The second round appears to be intended to provide working capital.

Historically they’ve been very conservative when it comes to investment and growth, reinvesting profits rather than taking on debits. This hasn’t been great for investors seeking returns mind.

I wouldn’t worry about them going pop, if they got near to that point a larger manufacturer will snap them up for the technology.

Anyway back to PFC have they changed something recently? Either I’m a hand fisted clown or the wear sensor cutout is now too small for the OE sensors. I’ve managed to snap my entire bag of spare sensors trying a simple allround pad change. Not a good day TBH.

Don’t get me wrong the sensor cut out in the backing plate used to be tight but with a little force I could get the sensors in… 11 compound pad if that matters, not suited to fast road but excellent on track when you can actually find stock. PFC really do need to sort out their supply chain / stock management issues.

Gassing Station | Boxster/Cayman | Top of Page | What's New | My Stuff