Discussion

Prizam said:

Its not for business reasons, or greed. Its so I will have a pension. I don't hold out much hope for current pension schemes to ever really pay out properly.

Then again, I have been brought up to provide for my self, I could sell everything and get some nice cars then expect the "System" to fully support me in my old age.

The next thing, once I have scrimped and saved through my life to buy two property's that are too look after me in my old age. Is that I will be expected to sell them to pay for my own care once i can no longer look after my self. Whilst others get it given to them.

TAX, life and death is simply not fair. EVERYONE should pay the same flat rate tax. No matter how rich or poor. THAT is a levil playing field!

Sorry, I'm not getting at you, sorry if it seems that way - I'm not knocking your choice of investment, just trying to explain why taxes have changed toward BTL and the reasons for them changing.Then again, I have been brought up to provide for my self, I could sell everything and get some nice cars then expect the "System" to fully support me in my old age.

The next thing, once I have scrimped and saved through my life to buy two property's that are too look after me in my old age. Is that I will be expected to sell them to pay for my own care once i can no longer look after my self. Whilst others get it given to them.

TAX, life and death is simply not fair. EVERYONE should pay the same flat rate tax. No matter how rich or poor. THAT is a levil playing field!

Just want to pick you up on the statement "Its not for business reasons" Well, I'm afraid making money is what business is all about. If you intend to make money then its a business. You really need to nail down you motivations and view on all this because your "customer" will be a tenant who values it as his home. Please treat it as business and as a commitment to providing a quality service. Its something that alot of so-called amateur Landlords forget. You need to know the rules, what you are getting in to and your responsibilities.

Oh, We all have under performing pensions.

People have picked up on houses because its an investment they can understand - its just that its been demonstarted as a collision course with home buyers that just want to live in one house.

There are other investments if you look around, arguably ones that are more productive personally and for society in the long run.

So there! :-)

Edited by BL Fanboy on Thursday 4th February 13:03

BL Fanboy said:

As above, most people dont really need two houses - hence the 3 %.

In a similar vein, the mortgage interest offsetting advantages to BTL are being reduced too. Its all intended to level the playing field between those folks that see property as a home and those that want to use property as an investment vehicle.

It does seem unfair, but its an area of business where "business men/women" (which is what you become when you take on an addition property for profit etc) become in effective competition for houses the with "man in the street joe blogs" who wants somewhere to live.

It seems unfair that a legitimate business expense cant be as fully offset against tax as before and indeed as in other businesses, but when it collides with an ordinary person that needs a house and cant do as such - eg prices are bid up by the sums working better for a business, they've decided to start evening it up. - Wouldnt it be great if I could offset my mortgage interest against my income tax?

Two people grappling for a common commodity - one already has a home and wants to snaffle another for business purposes vs someone who just want to live in one house as a basic human need.

Seems fair to me. Could get even fairer to be honest.

I have a few BTL's and realise why the changes have been made, but if it is to deter "business" from competing with Joe Public why do holdings of more than 15 properties get exemption? These really are the people operating as a business, rather than people like myself who are supplimenting income/pension.In a similar vein, the mortgage interest offsetting advantages to BTL are being reduced too. Its all intended to level the playing field between those folks that see property as a home and those that want to use property as an investment vehicle.

It does seem unfair, but its an area of business where "business men/women" (which is what you become when you take on an addition property for profit etc) become in effective competition for houses the with "man in the street joe blogs" who wants somewhere to live.

It seems unfair that a legitimate business expense cant be as fully offset against tax as before and indeed as in other businesses, but when it collides with an ordinary person that needs a house and cant do as such - eg prices are bid up by the sums working better for a business, they've decided to start evening it up. - Wouldnt it be great if I could offset my mortgage interest against my income tax?

Two people grappling for a common commodity - one already has a home and wants to snaffle another for business purposes vs someone who just want to live in one house as a basic human need.

Seems fair to me. Could get even fairer to be honest.

Edited by BL Fanboy on Thursday 4th February 12:23

oldnbold said:

I have a few BTL's and realise why the changes have been made, but if it is to deter "business" from competing with Joe Public why do holdings of more than 15 properties get exemption? These really are the people operating as a business, rather than people like myself who are supplimenting income/pension.

Yeah, good point. The tories are quite "big business".It could be that larger institutionalised investors are being encouraged to stay in or join. The advantages would be that tenants could be assured of much much longer tenanacies with larger landlords thus more security, rather than the small time landlord that sells off in the short term for personal cash flow reasons.

If you think about it, asking someone to leave because you are retiring and selling up or fancy a villa in Spain is an upheaval a lot of tenants could do without.

Plus I suppose institutions look more at yeald rather than capital growth which traditionally is that of the small time "private" investor.

oldnbold said:

I have a few BTL's and realise why the changes have been made, but if it is to deter "business" from competing with Joe Public why do holdings of more than 15 properties get exemption? These really are the people operating as a business, rather than people like myself who are supplimenting income/pension.

This is what I meant by running it as a "business".I understand why TAX has changed on BTL, just don't think it is fair. What other investments are there that will give me a reasonable return and be "safe as houses".

BL Fanboy said:

Plus I suppose institutions look more at yeald rather than capital growth which traditionally is that of the small time "private" investor.

I would disagree with that, my BTL's are there to provide income or "yield" as are many other people's in simular situations. Any capital growth is nice but only my children will benefit from that if they chose to sell up when I finally fall off my perch.And I would suggest that there a lot of individuals who own in excess of 15 properties either as a sole trader or wraped up in Ltd Company. I have several friends who have between 1 - 10 BTL's like me, all have them as income generators, one is infact a multi millionaire who very recently withdrew/sold most of his other investments and extended his portfolio to provide more monthly income.

BL Fanboy said:

There are other investments if you look around, arguably ones that are more productive personally and for society in the long run.

So there! :-)

Perhaps you could point me in the direction of these other fantastic low risk investments. Preferably something that will provide a net return of at least 10% on the cash invested. Oh and obviously some capital growth as well.So there! :-)

Edited by BL Fanboy on Thursday 4th February 13:03

No denying that a BTL or two can be a "good" financial investment.

Obviously there are pro's, cons with any investment.

Some investment types make more or less than others and are riskier/safer than others- all obviously.

I was never saying that x is better than y.

My point, originally was that things are being made harder for BTL because of its increasingly negative "social" impact.

If it becomes untenable for the small guy, then you know to get out.

Obviously there are pro's, cons with any investment.

Some investment types make more or less than others and are riskier/safer than others- all obviously.

I was never saying that x is better than y.

My point, originally was that things are being made harder for BTL because of its increasingly negative "social" impact.

If it becomes untenable for the small guy, then you know to get out.

Sheepshanks said:

Timmy40 said:

..what if it takes more than 6m to rennovate?

A couple of people have suggested 6mths - it's actually 18mths.In terms of BTL....what's to stop anyone who wants to do it from setting up a Ltd Co ( which is a person in law ), funding it with a 40% deposit then the Ltd Co buying a rental property with a BTL mortgage and not paying the 3% surcharge. Ltd Co are cheap to setup so you could do one for each property.

Timmy40 said:

Ah OK that's not so bad then.

In terms of BTL....what's to stop anyone who wants to do it from setting up a Ltd Co ( which is a person in law ), funding it with a 40% deposit then the Ltd Co buying a rental property with a BTL mortgage and not paying the 3% surcharge. Ltd Co are cheap to setup so you could do one for each property.

I believe that that solution is indeed doable, many of the BTL mortgage lenders are now happier to lend to a small Ltd Co. Of course you will then also inherit the other costs of running a Ltd Co, certified accounts, corp tax etc. In terms of BTL....what's to stop anyone who wants to do it from setting up a Ltd Co ( which is a person in law ), funding it with a 40% deposit then the Ltd Co buying a rental property with a BTL mortgage and not paying the 3% surcharge. Ltd Co are cheap to setup so you could do one for each property.

oldnbold said:

Timmy40 said:

Ah OK that's not so bad then.

In terms of BTL....what's to stop anyone who wants to do it from setting up a Ltd Co ( which is a person in law ), funding it with a 40% deposit then the Ltd Co buying a rental property with a BTL mortgage and not paying the 3% surcharge. Ltd Co are cheap to setup so you could do one for each property.

I believe that that solution is indeed doable, many of the BTL mortgage lenders are now happier to lend to a small Ltd Co. Of course you will then also inherit the other costs of running a Ltd Co, certified accounts, corp tax etc. In terms of BTL....what's to stop anyone who wants to do it from setting up a Ltd Co ( which is a person in law ), funding it with a 40% deposit then the Ltd Co buying a rental property with a BTL mortgage and not paying the 3% surcharge. Ltd Co are cheap to setup so you could do one for each property.

oldnbold said:

Timmy40 said:

Ah OK that's not so bad then.

In terms of BTL....what's to stop anyone who wants to do it from setting up a Ltd Co ( which is a person in law ), funding it with a 40% deposit then the Ltd Co buying a rental property with a BTL mortgage and not paying the 3% surcharge. Ltd Co are cheap to setup so you could do one for each property.

I believe that that solution is indeed doable, many of the BTL mortgage lenders are now happier to lend to a small Ltd Co. Of course you will then also inherit the other costs of running a Ltd Co, certified accounts, corp tax etc. In terms of BTL....what's to stop anyone who wants to do it from setting up a Ltd Co ( which is a person in law ), funding it with a 40% deposit then the Ltd Co buying a rental property with a BTL mortgage and not paying the 3% surcharge. Ltd Co are cheap to setup so you could do one for each property.

they are also changing the dividend tax rates in april so you pay more on dividends or additional tax to pay yourself any profit from the business.

then if your limited company sells the property, you are liable to pay 20% corporation tax on any profit, before your try and remove any of the money from the limited company.

so any changes to business tax rates, dividends tax, capital gains etc.... and the limited company route def doesnt look as positive!

I would def be speaking to a decent accountant before embarking on that route.

oldnbold said:

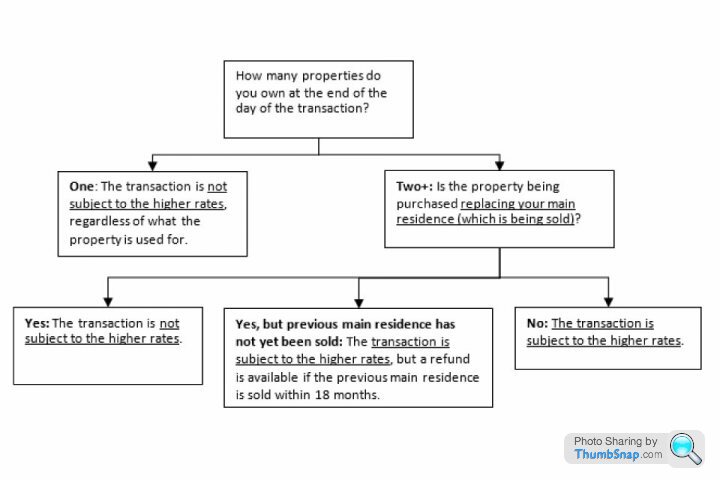

Yes it is thought that primary residences will be exempt the extra 3% and will be treated seperatly from your BTL portfolio. How the OP would get around not selling his primary residence and buying another property I'm not sure. This may help.

http://www.thisismoney.co.uk/money/buytolet/articl...

I have a small BTL portfolio and I am in the process of selling my home to by another and I was obviously concerned about the change. Even my solicitor seems unsure exactly what will happen at the moment as HMRC have yet to issue definate details.

Sadly i certainly don't read it that way. We're in the middle of buying another house and keeping/letting out our old one. We have moved out of the old house and it is now tenanted. However even with a btl mortgage on it, as far as HMRC is concerned, we still own it. Therefore even when we move out of rented and into the new house, we will gain an extra house in our ownership, therefore we will need to pay the extra 3%.http://www.thisismoney.co.uk/money/buytolet/articl...

I have a small BTL portfolio and I am in the process of selling my home to by another and I was obviously concerned about the change. Even my solicitor seems unsure exactly what will happen at the moment as HMRC have yet to issue definate details.

Whilst we are replacing our main residence, it is not being sold, so looking at the plan above, we will need to pay it.

It's causing us a massive headache at the moment as we don't have the extra £17k just lying around, so is threatening our purchase (along with lots of other issues).

The crazy issue I see is that you pay the extra 3% on whichever is the new house, so in the OPs case, even though he's depriving the market of a £400k house, he'll pay the 3% on the £800k of the new house. It'll be cheaper to sell the old one, and then buy it straight back again, although that leads to CGT issues.

MrChips said:

oldnbold said:

Yes it is thought that primary residences will be exempt the extra 3% and will be treated seperatly from your BTL portfolio. How the OP would get around not selling his primary residence and buying another property I'm not sure. This may help.

http://www.thisismoney.co.uk/money/buytolet/articl...

I have a small BTL portfolio and I am in the process of selling my home to by another and I was obviously concerned about the change. Even my solicitor seems unsure exactly what will happen at the moment as HMRC have yet to issue definate details.

Sadly i certainly don't read it that way. We're in the middle of buying another house and keeping/letting out our old one. We have moved out of the old house and it is now tenanted. However even with a btl mortgage on it, as far as HMRC is concerned, we still own it. Therefore even when we move out of rented and into the new house, we will gain an extra house in our ownership, therefore we will need to pay the extra 3%.http://www.thisismoney.co.uk/money/buytolet/articl...

I have a small BTL portfolio and I am in the process of selling my home to by another and I was obviously concerned about the change. Even my solicitor seems unsure exactly what will happen at the moment as HMRC have yet to issue definate details.

Whilst we are replacing our main residence, it is not being sold, so looking at the plan above, we will need to pay it.

It's causing us a massive headache at the moment as we don't have the extra £17k just lying around, so is threatening our purchase (along with lots of other issues).

The crazy issue I see is that you pay the extra 3% on whichever is the new house, so in the OPs case, even though he's depriving the market of a £400k house, he'll pay the 3% on the £800k of the new house. It'll be cheaper to sell the old one, and then buy it straight back again, although that leads to CGT issues.

I agree that in your and the OP's situation you will be subject to the extra 3%.

Edited by oldnbold on Thursday 4th February 21:29

Ah yep sorry i misread your post

Ignoring the right/wrongs of the motive of this tax change, the 2 things which stand out as being crazy are the fact it's applied to the new property, not the one you're renting out, and also that it's still payable upfront even if you sell your house within 18 months. I look forward to HMRC dealing with my claim for my money back being dealt with swiftly and efficiently..

Ignoring the right/wrongs of the motive of this tax change, the 2 things which stand out as being crazy are the fact it's applied to the new property, not the one you're renting out, and also that it's still payable upfront even if you sell your house within 18 months. I look forward to HMRC dealing with my claim for my money back being dealt with swiftly and efficiently..

Haha. Like most new taxation rules it's not been thought through very well. In fact one of the problems I can see is that of the small time developer who buys a few old run down properties a year to flip. Sure it's a business and he's making money but also putting poor and unwanted stock back in the market place to help with this shortage HMG are going on about. No sure these guy's are going to have the extra funding for the SD.

oldnbold said:

Any capital growth is nice but only my children will benefit from that if they chose to sell up when I finally fall off my perch.

And on that premise most smaller scale landlords that have been in the business for over 10 years are hanging on to their properties as the capital gains tax of 40% feels like just too much of a hit (especially on interest only properties that still need a chunky mortgage capital repayment). If Osbourne really wants to hurt and discourage such business then reducing this tax may be in his interest. I believe HMRC's CGT property tax take has never been lower as we are all sitting on them. At a 25% rate then maybe more properties would be freed up (which is what he wants)?oldnbold said:

Haha. Like most new taxation rules it's not been thought through very well. In fact one of the problems I can see is that of the small time developer who buys a few old run down properties a year to flip. Sure it's a business and he's making money but also putting poor and unwanted stock back in the market place to help with this shortage HMG are going on about. No sure these guy's are going to have the extra funding for the SD.

True mate. Have a few mates who buy filthy stinking properties, work hard on them and sell them a few months later. Have the tories killed such a business model and entrepreneurialism - let alone their hands on hard graft? Guess they cant offer him a non exec seat on the board in a few years time and some share options... The Tories of all people too!

The Tories of all people too!So i guess then, the best option is for me to move from one house to another. Prehaps liberating some cash from my first property and then once the dust has settled. Buy another smaller property that wont hurt so much on the stamp duty?

Or will i also get f ked over with capital gains if i take any money out of the old house?

ked over with capital gains if i take any money out of the old house?

Or will i also get f

ked over with capital gains if i take any money out of the old house?I don't think established buy to let land lords or investors have any grounds to feel hard done by with current increases in tax applied to the industry.

Remember it was the UK government that bailed out ME who lent so heavily within the industry... If banking system had collapsed even short term house prices really would be low for decades.

8 odd years of low interest rates, I was paying £4700 a month on buy to let portfolio interest only mortgages and thanks to low interest rates at one point it went to £1800 - would have been even less but one was fixed not a tracker.

Home counties seen 1/3 growth since recession hit and far more in London.

Remember it was the UK government that bailed out ME who lent so heavily within the industry... If banking system had collapsed even short term house prices really would be low for decades.

8 odd years of low interest rates, I was paying £4700 a month on buy to let portfolio interest only mortgages and thanks to low interest rates at one point it went to £1800 - would have been even less but one was fixed not a tracker.

Home counties seen 1/3 growth since recession hit and far more in London.

Gassing Station | Homes, Gardens and DIY | Top of Page | What's New | My Stuff