How far will house prices fall [volume 4]

Discussion

spikeyhead said:

turbobloke said:

Inheritance, depending on how thinly it's shared out i.e. how many kids and the level of their ambition.

I'll either be in my 60s or 70s before I inherit, by which time it would be a little late to start climbing the ladder.crankedup said:

Few years back much talk regarding 'life time' mortgages' was being seen as a way forward allowing those aspiring to own a home could consider this type of loan. Talk suggesting that this mortgage could be passed down the family line, is that still an option?

That worked REALLY well in Japan...AstonZagato said:

crankedup said:

Few years back much talk regarding 'life time' mortgages' was being seen as a way forward allowing those aspiring to own a home could consider this type of loan. Talk suggesting that this mortgage could be passed down the family line, is that still an option?

That worked REALLY well in Japan...(FORTUNE Magazine)

By Susan Moffat

21 May 1990

The Japanese, famous for saving, are now loading their future generations with debt. Nippon Mortgage and Japan Housing Loan, two big home lenders, are offering 99- and 100-year multigeneration loans with interest rates from 8.9% to 9.9%. Borrowers put up their homes as collateral. Such deals represent sound fiscal planning for some families, especially the very wealthy living in Tokyo who, perversely, can almost not afford to inherit a house: Japan's graduated inheritance tax can take up to 70% of a family's assets, including its home. Under the 100-year loan plan, a second generation can move into a deceased parent's home and pay inheritance taxes on only a fraction of the house's value. Most Japanese, of course, don't have such problems. Their challenge is to find a house they can afford, especially if they want to live in Tokyo. The housing crunch there inspired Robinsons on the Sand, a 1989 hit movie that's now No. 8 on Japan's VCR rental list. It tells the story of a salaryman and his family, who are willing to do anything to escape the misery of their tiny rented apartment. The ''anything'' turns out to be living on constant display as a ''model family'' in a spacious model home while potential buyers tramp through. Jealous neighbors bully the children and make obscene phone calls. Before long, one of the two sons turns delinquent, the daughter is killing kittens, and the father ends up homeless in the street. Mom and the kids finally return to their old apartment, where they watch TV in the closet in blessed privacy. So much for that particular family's Japanese dream.

turbobloke said:

Pork said:

crankedup said:

Few years back much talk regarding 'life time' mortgages' was being seen as a way forward allowing those aspiring to own a home could consider this type of loan. Talk suggesting that this mortgage could be passed down the family line, is that still an option?

Isn't that the norm in Germany, for those that want to buy?Link said:

Intergenerational mortgages – a sign of the times?

by Ian Giles | Jul 18, 2014

Various new mortgage products linked to high property prices are either coming to market or available now iirc.by Ian Giles | Jul 18, 2014

AstonZagato said:

crankedup said:

Few years back much talk regarding 'life time' mortgages' was being seen as a way forward allowing those aspiring to own a home could consider this type of loan. Talk suggesting that this mortgage could be passed down the family line, is that still an option?

That worked REALLY well in Japan...anonymous said:

[redacted]

Well yes, but it needs to be a managed withdrawal otherwise you would end up bankrupting the very property developers you want to be able to expand and build the housing required.Personally, as with most regulation, I would like a change in the presumption. Instead of no development being allowed unless expressly allowed, all development should be permitted unless expressly forbidden.

The government should designate areas where development is not permitted, not crude "green belts" but areas of great natural beauty and the best farmland. Anywhere else you can build as long as you compensate those who will be affected directly. I.E. if a developer wants to put in a thousand homes that will increase traffic congestion they also have to upgrade the main road to town. If houses have their view impacted compensate those households directly.

turbobloke said:

AstonZagato said:

crankedup said:

Few years back much talk regarding 'life time' mortgages' was being seen as a way forward allowing those aspiring to own a home could consider this type of loan. Talk suggesting that this mortgage could be passed down the family line, is that still an option?

That worked REALLY well in Japan...(FORTUNE Magazine)

By Susan Moffat

21 May 1990

The Japanese, famous for saving, are now loading their future generations with debt. Nippon Mortgage and Japan Housing Loan, two big home lenders, are offering 99- and 100-year multigeneration loans with interest rates from 8.9% to 9.9%. Borrowers put up their homes as collateral. Such deals represent sound fiscal planning for some families, especially the very wealthy living in Tokyo who, perversely, can almost not afford to inherit a house: Japan's graduated inheritance tax can take up to 70% of a family's assets, including its home. Under the 100-year loan plan, a second generation can move into a deceased parent's home and pay inheritance taxes on only a fraction of the house's value. Most Japanese, of course, don't have such problems. Their challenge is to find a house they can afford, especially if they want to live in Tokyo. The housing crunch there inspired Robinsons on the Sand, a 1989 hit movie that's now No. 8 on Japan's VCR rental list. It tells the story of a salaryman and his family, who are willing to do anything to escape the misery of their tiny rented apartment. The ''anything'' turns out to be living on constant display as a ''model family'' in a spacious model home while potential buyers tramp through. Jealous neighbors bully the children and make obscene phone calls. Before long, one of the two sons turns delinquent, the daughter is killing kittens, and the father ends up homeless in the street. Mom and the kids finally return to their old apartment, where they watch TV in the closet in blessed privacy. So much for that particular family's Japanese dream.

It's the only way their insatiable appetite for more and more finance churning and skimming can grow and thus survive.

While houses get mixed up in that the market is never gonna be anything but a mess.

Help to Buy is really "Help the banks to get more young people on the life-long pyramid scheme that funds banks and their investors for doing feck all"

JagLover said:

Well yes, but it needs to be a managed withdrawal otherwise you would end up bankrupting the very property developers you want to be able to expand and build the housing required.

Personally, as with most regulation, I would like a change in the presumption. Instead of no development being allowed unless expressly allowed, all development should be permitted unless expressly forbidden.

The government should designate areas where development is not permitted, not crude "green belts" but areas of great natural beauty and the best farmland. Anywhere else you can build as long as you compensate those who will be affected directly. I.E. if a developer wants to put in a thousand homes that will increase traffic congestion they also have to upgrade the main road to town. If houses have their view impacted compensate those households directly.

I'm sure there would be someone waiting in the wings to pick up where the incumbent leaves off.Personally, as with most regulation, I would like a change in the presumption. Instead of no development being allowed unless expressly allowed, all development should be permitted unless expressly forbidden.

The government should designate areas where development is not permitted, not crude "green belts" but areas of great natural beauty and the best farmland. Anywhere else you can build as long as you compensate those who will be affected directly. I.E. if a developer wants to put in a thousand homes that will increase traffic congestion they also have to upgrade the main road to town. If houses have their view impacted compensate those households directly.

turbobloke said:

jonny70 said:

Derek Chevalier said:

They've ridden the biggest bubble of all time, so have plenty of equity, and in my experience those that are buying the £1m homes are on a fair bit more than 100k

That maybe the case but it begs the question how todays young or the next generation will buy these houses ? If the people who live in these houses today cant really afford to buy them now, its only because they have ridden the huge bubble and built up huge equity. Then how the hell will their kids afford them ?

RYH64E said:

I'm now in my fifties and my parents are in their 70s, so I'll probably be due to inherit when I'm about the same age as you. My children in their late teens now, so I've asked my parents to leave whatever I'm due directly to them, the money may not help me with whatever property ladder aspirations I have left by then but I'm sure it will help my children at a time when they most need help. Most of us fifty something year olds have done well out of property anyway and don't need help getting on the ladder, skipping a generation makes sense.

Hopefully your children are sensible and would make good use of an inheritance but sadly I think too many live for today and would use it for travelling to 'find themselves' or piss it on various gee-gaws.I'm in the opposite position with no children and relatively asset-rich and trying to work out a way of spending my last pound as I take my last breath.

turbobloke said:

jonny70 said:

Derek Chevalier said:

They've ridden the biggest bubble of all time, so have plenty of equity, and in my experience those that are buying the £1m homes are on a fair bit more than 100k

That maybe the case but it begs the question how todays young or the next generation will buy these houses ? If the people who live in these houses today cant really afford to buy them now, its only because they have ridden the huge bubble and built up huge equity. Then how the hell will their kids afford them ?

jonny70 said:

turbobloke said:

jonny70 said:

Derek Chevalier said:

They've ridden the biggest bubble of all time, so have plenty of equity, and in my experience those that are buying the £1m homes are on a fair bit more than 100k

That maybe the case but it begs the question how todays young or the next generation will buy these houses ? If the people who live in these houses today cant really afford to buy them now, its only because they have ridden the huge bubble and built up huge equity. Then how the hell will their kids afford them ?

rovermorris999 said:

RYH64E said:

I'm now in my fifties and my parents are in their 70s, so I'll probably be due to inherit when I'm about the same age as you. My children in their late teens now, so I've asked my parents to leave whatever I'm due directly to them, the money may not help me with whatever property ladder aspirations I have left by then but I'm sure it will help my children at a time when they most need help. Most of us fifty something year olds have done well out of property anyway and don't need help getting on the ladder, skipping a generation makes sense.

Hopefully your children are sensible and would make good use of an inheritance but sadly I think too many live for today and would use it for travelling to 'find themselves' or piss it on various gee-gaws.I'm in the opposite position with no children and relatively asset-rich and trying to work out a way of spending my last pound as I take my last breath.

I personally earn comfortably more than the average salary (high 30k's) and my gf earns a respectable wage (30k ish). I have had to move from Kent to the east midlands and face a 1 hr 15 minute each way commute to work. She has moved back home with her mum and I rent a modest room in a house share. I will more than likely move in to my gf's Mum's house in order to save a bit more money for a deposit. I have just bought a £600 diesel Fabia to save money too.

We are going on holiday this year, and we go out with eachother once a month and do something "fun", and may pop to the pub for an hour or 2 on a friday; something that many seems to begrudge on here. Weirdly my parents seemed to go on holiday and go out with each other when they were a similar age; more than we do, and by my age they had bought their first decent 3 bed, despite both of them earning far more modest wages than I am now relative to their peers. We both spent less than £50 on eachother at Christmas. etc etc. I could go on... Personally my gf and I both realize we couldn't afford to buy on our own, so it makes sense that we do something to maintain some normality in a relationship between a young couple rather than getting fed up with eachother. I guess we could just stay in everyday and **** but I would imagine her Mum would get bored of listening to that...

It's easy for some to say that people my age do nothing to help themselves. Or that we should buy something tiny in a crap part of town "like they did in 1983 to get on the ladder". I guess we could... Difference is they were 21 and single when they were buying their first property, chances are we will be 27 and 28 respectively when we buy ours. I have a feeling that the future Mrs Jimbob (that'll cost me a fortune too lol) will probably want a 3rd and 4th addition to the household not too many years beyond that (biology unfortunately puts a limit to how long). All of a sudden it seems an awful lot of time and expense to buy a ****hole just to move 2 years later.

Complaining isn't going to help. But I feel I have already made and am already making enough sacrifices, and I'm not alone among my peers. At least those of us who don't stand to inherit any time soon! I literally do not know what more I could do to get on the ladder (waiting for someone to suggest sitting in every night eating Aldi beans from a tin).

Edited by jimbobsimmonds on Monday 15th February 16:30

I think it does slightly grate the 'millenials' when they are tarnished with the brush of lazy or not willing to make sacrifices.

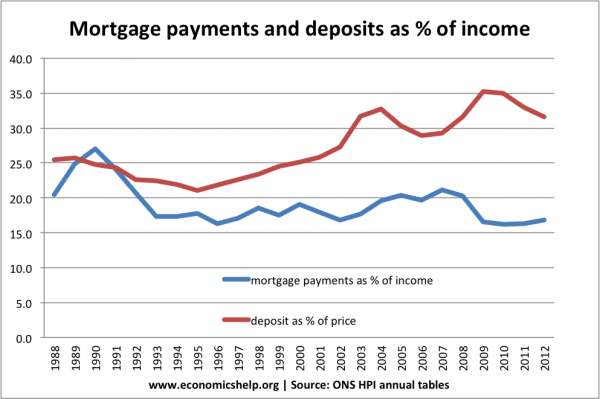

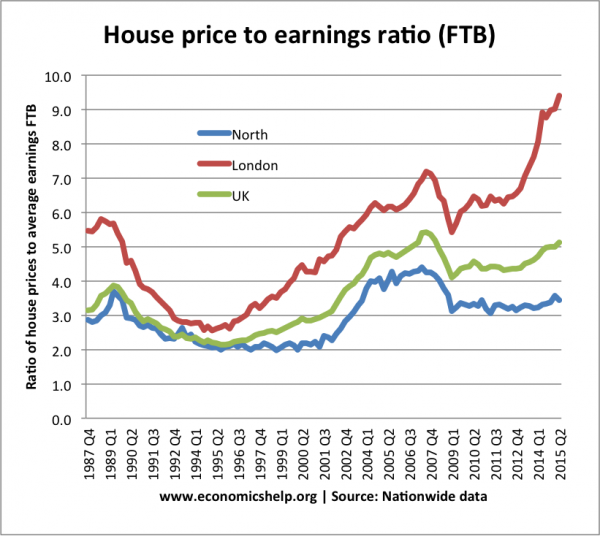

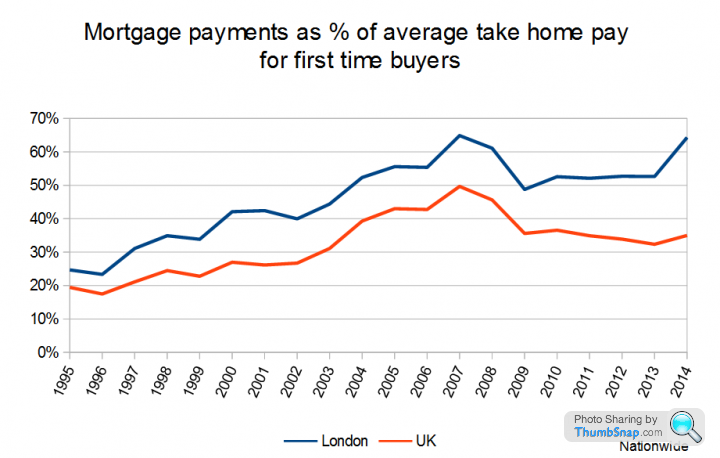

The point is often made around high historic mortgage rates, so a quick google shows some graphs reflecting mortgage spend vs salary, to be clear this isn't mortgage spend vs salary (Minus lots of benders/holidays).

The first time buyers graph is telling, particularly when you compare to the 80/90's e.g. 65% of a person's salary going to mortgage payments in 2014 vs 25% in 1995. Let alone what 2016 would be, and then also considering the deposit.

No wonder people are jumping on the 40% HTB, it is their only chance in today's market. Not that I think the government are doing HTB to help first time buyers, as it certainly fails to address the root cause but simply helps sustain the current prices.

However the situation is what it is and there is nothing you or I can do it about it.

There are lots of things happening right now, such as Chinese pulling out, BTL'ers threatening to pull out.

Who know's what will happen, but it is quite clear that the sub 30 and 40's FTB'er is paying a high price for it.

The point is often made around high historic mortgage rates, so a quick google shows some graphs reflecting mortgage spend vs salary, to be clear this isn't mortgage spend vs salary (Minus lots of benders/holidays).

The first time buyers graph is telling, particularly when you compare to the 80/90's e.g. 65% of a person's salary going to mortgage payments in 2014 vs 25% in 1995. Let alone what 2016 would be, and then also considering the deposit.

No wonder people are jumping on the 40% HTB, it is their only chance in today's market. Not that I think the government are doing HTB to help first time buyers, as it certainly fails to address the root cause but simply helps sustain the current prices.

However the situation is what it is and there is nothing you or I can do it about it.

There are lots of things happening right now, such as Chinese pulling out, BTL'ers threatening to pull out.

Who know's what will happen, but it is quite clear that the sub 30 and 40's FTB'er is paying a high price for it.

Edited by V6Alfisti on Monday 15th February 16:08

Edited by V6Alfisti on Monday 15th February 16:21

V6Alfisti said:

But like I said, I'm happy whatever happens. Go up 10x or drop 10x I'm winning... sadly lots of others are not which is ultimately worse as we all live together on this little island

Mr Whippy said:

Ouch, this sums it up quite nicely when you consider the payment you make stays at that level all else staying the same.

But like I said, I'm happy whatever happens. Go up 10x or drop 10x I'm winning... sadly lots of others are not which is ultimately worse as we all live together on this little island

Thinking about it, things are even worse. All this in recent years has been at record low interest rate. So guess what happens to that percentage of salary going to mortgage when rates eventually rise. That will unfortunately be carnage for many FTB'ers as they will be borrowing £300-400k for a typical London flat. A friend of mine has just done exactly this, about £40-50k down on a £370k flat. That's £320k of debt.But like I said, I'm happy whatever happens. Go up 10x or drop 10x I'm winning... sadly lots of others are not which is ultimately worse as we all live together on this little island

k all in the grand scheme of things for two people earning a half decent London wage.

k all in the grand scheme of things for two people earning a half decent London wage.V6Alfisti said:

It is just him, I know what his salary is and it isn't enough to take any big hits on interest.

Ah ok, then yes, could be in for a rocky ride.That all said, with only modest deposit, he won't have got a rock bottom rate anyway, so might not be too bad if things go up and at renewal time its only a touch more expensive etc. I think most FTB probably do not end up with a rate anywhere near base owing to average deposit size, so rises to base are maybe not such an issue just yet.

Gassing Station | News, Politics & Economics | Top of Page | What's New | My Stuff