How far will house prices fall [volume 4]

Discussion

p1stonhead said:

Isnt £50k, 40 years ago, still really really expensive? Average price was what £5-10k?

£50k in 1976 would be worth £324,633.99 in 2015 according to http://www.bankofengland.co.uk/education/Pages/res...I guess it is widening the rich/poor gap, large inheritances when people die, gets passed down and gives a cash injection for the recipients to purchase, if your parents and grandparents dont own property or have a low value property then you dont get that potential for a lump sum.

Always been the cash but it seems to be getting worse, plus the middle classes are much better at avoiding IHT with trusts and passing stuff on.

Always been the cash but it seems to be getting worse, plus the middle classes are much better at avoiding IHT with trusts and passing stuff on.

J4CKO said:

I guess it is widening the rich/poor gap, large inheritances when people die, gets passed down and gives a cash injection for the recipients to purchase, if your parents and grandparents dont own property or have a low value property then you dont get that potential for a lump sum.

Always been the cash but it seems to be getting worse, plus the middle classes are much better at avoiding IHT with trusts and passing stuff on.

That's pretty much it as far as I can see. A wodge from the sale of a previous property that was bought for peanuts plus some more at incredibly low interest rates. Completely cuts out young people from less wealthy backgrounds though and is the worst thing about the UK (and lots of other countries) at present. And I speak as someone who hasn't done that badly at all from it. Always been the cash but it seems to be getting worse, plus the middle classes are much better at avoiding IHT with trusts and passing stuff on.

Randy Winkman said:

J4CKO said:

I guess it is widening the rich/poor gap, large inheritances when people die, gets passed down and gives a cash injection for the recipients to purchase, if your parents and grandparents dont own property or have a low value property then you dont get that potential for a lump sum.

Always been the cash but it seems to be getting worse, plus the middle classes are much better at avoiding IHT with trusts and passing stuff on.

That's pretty much it as far as I can see. A wodge from the sale of a previous property that was bought for peanuts plus some more at incredibly low interest rates. Completely cuts out young people from less wealthy backgrounds though and is the worst thing about the UK (and lots of other countries) at present. And I speak as someone who hasn't done that badly at all from it. Always been the cash but it seems to be getting worse, plus the middle classes are much better at avoiding IHT with trusts and passing stuff on.

Timmy40 said:

Hitch said:

sooperscoop said:

Friends in Shanghai have been going to "Buy in Manchester!' presentations for at least 3 years. The Chinese always flock to where the Chinese already are.

If the centre of Manchester can keep hold of it's prices, then the outskirts are very attractive, there's plenty of nice areas with 200k semis within 20 mins commute of the centre.

But these seminars are usually centred on some big infrastructure development which is claimed to be the catalyst for business investment and residential growth. What are they claiming is happening in Manchester?! If the centre of Manchester can keep hold of it's prices, then the outskirts are very attractive, there's plenty of nice areas with 200k semis within 20 mins commute of the centre.

I assume a wealthy Chinese family would be quite likely to decide to buy a flat their kid could use whilst at Uni then rent it out afterwards as an investment and handy way of having some money out of China ( just incase ).

ukbabz said:

p1stonhead said:

Isnt £50k, 40 years ago, still really really expensive? Average price was what £5-10k?

£50k in 1976 would be worth £324,633.99 in 2015 according to http://www.bankofengland.co.uk/education/Pages/res...battered said:

Inflation is only half the tale. Borrowing 50k in 1976 would have cost a fortune because of heavy interest rates. You would have needed a hefty income to service that. My parents, both teachers, borrowed 14k in 79 and had 2 salaries. One full salary went on the mortgage.

I guess the £50K for a 3 bed house in 1976 is a London thing, but even so that would have been a pretty immense purchase.Our first house in the NW in 1980 was a new 3 bed detached at £20K and people thought we were insane. Your typical 3 bed semi was £15K.

I didn't think there was such a difference between the regions back then?

battered said:

ukbabz said:

p1stonhead said:

Isnt £50k, 40 years ago, still really really expensive? Average price was what £5-10k?

£50k in 1976 would be worth £324,633.99 in 2015 according to http://www.bankofengland.co.uk/education/Pages/res...However, the mortgage costs I was paying at the time would be similar to the cost of a mortgage at current interest rates at current house price.

The key to understanding house prices is how affordable people find the mortgage.

EddieSteadyGo said:

battered said:

ukbabz said:

p1stonhead said:

Isnt £50k, 40 years ago, still really really expensive? Average price was what £5-10k?

£50k in 1976 would be worth £324,633.99 in 2015 according to http://www.bankofengland.co.uk/education/Pages/res...However, the mortgage costs I was paying at the time would be similar to the cost of a mortgage at current interest rates at current house price.

The key to understanding house prices is how affordable people find the mortgage.

Derek Chevalier said:

The key to understanding it is how interest rates and wage inflation are linked. In times of high inflation and high wage growth, the pain was in the early years, but wage growth soon reduced the pain of the monthly payments. We do not have that luxury today.

Would be interested to see the analysis which draws you to the conclusion that the relationship between inflation and wages (often called 'real wages') is the main factor. You can borrow £300,000 at a cost of around £675 / month (excluding repayments for a moment to make it easier to compare like with like).

My first mortgage had an interest rate of around 6.5%. If you borrowed £100,000 at the time it made the interest only repayment circa £540 / month.

Adjusting for 20 years of wage inflation, current mortgages affordability is similar.

Most people buying a house look at what they can afford on a monthly basis. Dividend that number by the mortgage rate and multiple by 12 gives you a good indication of the price of the house they are buying. It has always been pretty such the same.

This one is old - needs updating.

The point is absolutely valid - the low rates certainly do make housing "affordable".

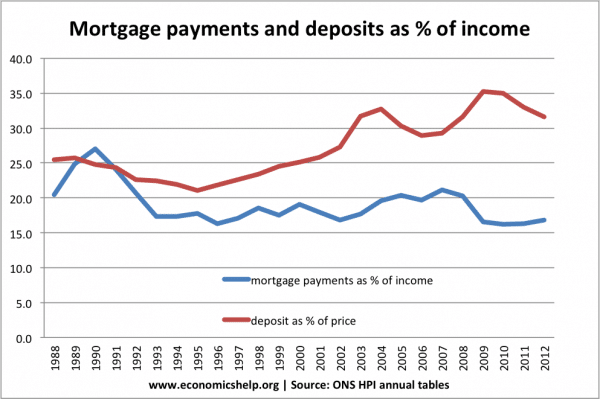

The problem is more for deposits, particularly for FTBs.

I believe for most FTBs if they switched to a mortgage it would be cheaper than rent - it's just coming up with 25% deposit is nearly impossible.

The point is absolutely valid - the low rates certainly do make housing "affordable".

The problem is more for deposits, particularly for FTBs.

I believe for most FTBs if they switched to a mortgage it would be cheaper than rent - it's just coming up with 25% deposit is nearly impossible.

This is a fundamental shift. I remember when I bought my first house in 1995 I had a 10% deposit (£4k) and this was regarded as pretty good. It actually got me a lower rate. In addition I went from paying £360pcm rent for a 2 bed flat to about £230 on a whole house. My net income at the time was £900pcm ish, living in the flat was tight. The difference is that the part that actually paid very little to reduce the capital, it was an endowment (remember them?) of about £60pcm.

Fast forward to the present day. That house is now about £125k. Anyone sane is now on a repayment scheme, you need to pay back 5k a year plus interest. That's 600pcm plus maybe 4k interest, so £930ish total, for a 100% loan. A 90% loan like I had would be say £800. You can see that the actual capital payback amount is now 2/3 of the total, whereas it was only 25%.

Rental price on that house will be about £500pcm. Maybe 550 tops. That's a long way off the £800 pcm you'll need even if you can come up with the £12.5k 10% deposit. This is a 2 bed starter home in a decent but by no means posh bit of Leeds. I wish I still bloody had it. I could have boarded it up and paid the mortgage and made money.

Fast forward to the present day. That house is now about £125k. Anyone sane is now on a repayment scheme, you need to pay back 5k a year plus interest. That's 600pcm plus maybe 4k interest, so £930ish total, for a 100% loan. A 90% loan like I had would be say £800. You can see that the actual capital payback amount is now 2/3 of the total, whereas it was only 25%.

Rental price on that house will be about £500pcm. Maybe 550 tops. That's a long way off the £800 pcm you'll need even if you can come up with the £12.5k 10% deposit. This is a 2 bed starter home in a decent but by no means posh bit of Leeds. I wish I still bloody had it. I could have boarded it up and paid the mortgage and made money.

battered said:

This is a fundamental shift. I remember when I bought my first house in 1995 I had a 10% deposit (£4k) and this was regarded as pretty good. It actually got me a lower rate. In addition I went from paying £360pcm rent for a 2 bed flat to about £230 on a whole house. My net income at the time was £900pcm ish, living in the flat was tight. The difference is that the part that actually paid very little to reduce the capital, it was an endowment (remember them?) of about £60pcm.

Fast forward to the present day. That house is now about £125k. Anyone sane is now on a repayment scheme, you need to pay back 5k a year plus interest. That's 600pcm plus maybe 4k interest, so £930ish total, for a 100% loan. A 90% loan like I had would be say £800. You can see that the actual capital payback amount is now 2/3 of the total, whereas it was only 25%.

Rental price on that house will be about £500pcm. Maybe 550 tops. That's a long way off the £800 pcm you'll need even if you can come up with the £12.5k 10% deposit. This is a 2 bed starter home in a decent but by no means posh bit of Leeds. I wish I still bloody had it. I could have boarded it up and paid the mortgage and made money.

Your math is off. It's £600 worst case on such a mortgage (standard table mtge).Fast forward to the present day. That house is now about £125k. Anyone sane is now on a repayment scheme, you need to pay back 5k a year plus interest. That's 600pcm plus maybe 4k interest, so £930ish total, for a 100% loan. A 90% loan like I had would be say £800. You can see that the actual capital payback amount is now 2/3 of the total, whereas it was only 25%.

Rental price on that house will be about £500pcm. Maybe 550 tops. That's a long way off the £800 pcm you'll need even if you can come up with the £12.5k 10% deposit. This is a 2 bed starter home in a decent but by no means posh bit of Leeds. I wish I still bloody had it. I could have boarded it up and paid the mortgage and made money.

I think wage stagnation, if that is a saying has been the biggest hold on the economy, precession days Friday nights and Saturday nights were equally busy here in Essex, Friday nights became pretty quiet and even Saturday's are not as lively as they use to be, I think this is generally down to people having less money to splash out. I earn 20k a year more than I did in 2008 and I don't think much better off and I have no debt other than my mortgage.

In which case money is even cheaper to borrow than I thought. 125k across 25 years is 5k a year just to give back the money without any interest. £600 a month is £7200 a year so you are only paying £2200 interest on 125k. Less than 2%. No wonder housing is going mad.

The rest of my point still stands even if the numbers are different. The capital payment used to be trivial compared to the interest, now it's all about the capital payback. It's also interesting that rental is now cheaper than buying, so maybe prices will stabilise.

The rest of my point still stands even if the numbers are different. The capital payment used to be trivial compared to the interest, now it's all about the capital payback. It's also interesting that rental is now cheaper than buying, so maybe prices will stabilise.

And yet Houses selling in record time despite worries over EU vote

http://www.thetimes.co.uk/article/221e0844-365f-11...

http://www.thetimes.co.uk/article/221e0844-365f-11...

J4CKO said:

Sheepshanks said:

J4CKO said:

I think things have officially gone mad, one went up over the road at 100/125 grand more than I would have expected, had several buyers in a week and they resorted to sealed bids above the asking price, so probably 150 grand more than I would have thought it was worth.

All very well, this middle class self congratulatory house price stuff but I have three kids that will need to get something in the next five or so years, a 3 bed family house shouldnt be that expensive.

I see your profile says you're in Cheshire - I'm in a village in west Cheshire and anything that looks even slightly OTT price-wise is just sitting there.All very well, this middle class self congratulatory house price stuff but I have three kids that will need to get something in the next five or so years, a 3 bed family house shouldnt be that expensive.

Someone mentioned proximity to good schools earlier - an issue all over West Cheshire and into Chester is the good schools are rammed so young families won't move into the area as they can't get places for their kids.

I know someone in one of the houses paid £260K in 2006 - seems incredible compared to some areas that they're still not back to their peak prices.

Edited by Sheepshanks on Monday 20th June 13:56

Gassing Station | News, Politics & Economics | Top of Page | What's New | My Stuff