Cut old people's benefits, they'll die soon anyway

Discussion

crankedup said:

Our experiences at that time mirrors this ^^^^^^^^^^

We saved every penny toward a house deposit, during which time the first house price boom took off. Unfortunately we were still saving up at that point. First home furniture was all second hand except for the sofa which was chuck outs from the local shoe shop, two club chairs used by hundreds of new shoe shoppers Nigh on went bust in the mid eighties and more hard work long hours managed to come back. Happy days

Nigh on went bust in the mid eighties and more hard work long hours managed to come back. Happy days

With the way house prices have moved against earnings there are broad masses of people in the generations below you that cannot afford a house in a nice area near where they need to be for work no matter what sacrifices they make. Admittedly you sound a little unlucky, my parents bought in 1977 during a housing slump. We saved every penny toward a house deposit, during which time the first house price boom took off. Unfortunately we were still saving up at that point. First home furniture was all second hand except for the sofa which was chuck outs from the local shoe shop, two club chairs used by hundreds of new shoe shoppers

Nigh on went bust in the mid eighties and more hard work long hours managed to come back. Happy days You mention inheritance it is not something I am looking for at least 30 years hopefully (and given increased life expectancy hopefully that will be the case), so if and when it does come, the balance of the estate (after probable care home fees) will be split three ways and give me some extra savings in retirement. It is not going to change the fact that over the course of their lives the generations after the baby boomers will pay more to live in worse housing.

anonymous said:

[redacted]

Have you considered selling your mobile phone, you X-box, your Sky box, even your TV? The car can go as well, not to mention booze, nights out and parties. Holidays? Nah, no need for them. Because that's what I did in essence. But for the current generation, such things are seen as essentials. In my first ten 13 years of employment, I paid into a pension scheme that was embezzled. No compensation by the way. In the next 30 years I had 12% gross removed from my pay on the promise of a pension. For the first 17 years the scheme made a tremendous profit for the government.

There is money around otherwise the current government would not have been able to cut higher tax rates and the other benefits for high earners.

The cause of the housing crisis is the lack of housing. This is the only reason. If there were more houses, there would be lower prices. However, it has been governments, mainly voted in by the middle classes oddly enough despite your moan, failing to provide for the population that has given rise to the current problems.

I had nothing to do with the cutting back of house building. Nor did your parents I bet. But you are suffering. So why not get over yourself and do something about it? Join a political party. Dump your mobile phone contract.

I get a fuzzy feeling from the knowledge that my kids have it better than I did. Much better in many ways. I hope that their kids will to, but it will require a change of direction from politicians for that to happen.

Moan away. That will change things you know. If you moan enough perhaps there will be a lot more houses on the market. Or perhaps not.

Derek Smith said:

Have you considered selling your mobile phone, you X-box, your Sky box, even your TV? The car can go as well, not to mention booze, nights out and parties. Holidays? Nah, no need for them. Because that's what I did in essence. But for the current generation, such things are seen as essentials.

In my first ten 13 years of employment, I paid into a pension scheme that was embezzled. No compensation by the way. In the next 30 years I had 12% gross removed from my pay on the promise of a pension. For the first 17 years the scheme made a tremendous profit for the government.

Highly unlikely at the time and even less likely in restrospect. The cost of a pension scheme cannot be determined from comparing contributions in to benefits out in any particular year. Further, the assumptions made at the time to determine contorbutions have been proven to have been wildly unrealistic, particular in the case of future longevity improvements.In my first ten 13 years of employment, I paid into a pension scheme that was embezzled. No compensation by the way. In the next 30 years I had 12% gross removed from my pay on the promise of a pension. For the first 17 years the scheme made a tremendous profit for the government.

The scheme that you paid 12% for will end up costing at least twice as much, and for new entrants the costs is 3-4 times that amount.

Derek Smith said:

There is money around otherwise the current government would not have been able to cut higher tax rates and the other benefits for high earners.

Higher taxes were simply reduced to the level that they were for the vast majority of the previous government, before they decided to play political games in the run up to the election. Evidence suggests that higher earners have lost more in £ terms than other parts of the income distribution.Plus of course the 50% tax didn't actually raise meaningful amounts of money.

We are spending £90bn more than we can afford, each and every year (and government spending continues to increase year on year) so not sure where you think this money is?

Derek Smith said:

The cause of the housing crisis is the lack of housing. This is the only reason. If there were more houses, there would be lower prices. However, it has been governments, mainly voted in by the middle classes oddly enough despite your moan, failing to provide for the population that has given rise to the current problems.

I'm afraid that it is the massive increase in population that has driven the shortage and you can only blame one government for that!Derek Smith said:

I had nothing to do with the cutting back of house building. Nor did your parents I bet. But you are suffering. So why not get over yourself and do something about it? Join a political party. Dump your mobile phone contract.

I get a fuzzy feeling from the knowledge that my kids have it better than I did. Much better in many ways. I hope that their kids will to, but it will require a change of direction from politicians for that to happen.

Moan away. That will change things you know. If you moan enough perhaps there will be a lot more houses on the market. Or perhaps not.

Whether you are to blame or not does not change the fact that you'll be taking out from the system more than you put in.I get a fuzzy feeling from the knowledge that my kids have it better than I did. Much better in many ways. I hope that their kids will to, but it will require a change of direction from politicians for that to happen.

Moan away. That will change things you know. If you moan enough perhaps there will be a lot more houses on the market. Or perhaps not.

Edited by sidicks on Tuesday 6th October 09:52

SPS said:

Well - really bored with the predictable and small minded hypocrites who espouse the "you never had it so good" mantra when they don't actually know what it was like.

Can't wait till you get to 80 and get you meager State Pension and see how you react. Some idiot will be saying - "you never had it so good". But then I expect you will say it was not us - it was the older generations like your mother and father.

That's exactly the point. I'm 48 and spending a considerable amount on the welfare of current pensioners. When I am able to retire at, I anticipate, 75 or so, I fully expect that there will be no such largesse aimed at me - if there is such a thing as a State Pension by then it will be means-tested out of existence for anyone who has a private or company pension.Can't wait till you get to 80 and get you meager State Pension and see how you react. Some idiot will be saying - "you never had it so good". But then I expect you will say it was not us - it was the older generations like your mother and father.

On that basis I would rather put my current NI contributions into a pensions provision from which I might expect to one day see some benefit...

Derek Smith said:

Munter said:

SPS said:

My children are working full time as are their partners but we still have to run the "Bank of Mum & Dad" just to help them make ends meet each month. In addition we are unpaid baby sitters too (allowing both parents to work) - which by the way is a secret delight!!

Without us and thousands of pensioners like us many young families would not be able to afford their rent or mortgages so would basically have no place to live (oh I forgot - move back into the parents home).

Which generation was it that created this situation?Without us and thousands of pensioners like us many young families would not be able to afford their rent or mortgages so would basically have no place to live (oh I forgot - move back into the parents home).

So it is hardly a generation issue.

The comments being reported from TPA are insensitive but there are valid points in the reality that some pensioners may not use certain free benefits and could (some even would) give them up voluntarily rather than have then taken.

Derek Smith said:

1968, the year of my engagement.

I was in full time employment, in a job that paid over the average industrial wage. My wife was a PA to a publisher, greater take home pay than me.

We were engaged for around 20-22 months. In that time my fiancee's pay went into a fund for a deposit on a house. We went nowhere where we weren't subsidised or it was free. If we couldn't afford it, we didn't have it. A lovely 14-year-old Standard Pennant took me to work and occasionally us out for a Sunday - I worked most Saturdays - but not often. We didn't live together but with out separate parents. No electronic devices, no toys as such. My brother had gone through the same process a couple of years before.

The deposit did not cover the house we wanted and I had to borrow £75 from my parents. We bought a little bungalow in Hextable, trying to balance fares and housing costs. I could not afford a house in London in those days. Nor now come to that.

Yeah, we benefited all right.

If couples today didn't cohabit and pay rent and instead put one of their wages away each month for 18-20 months, did not pay for mobiles, pads, TV packages, games consoles and so much more, I have that sneaking feeling that they too could afford to buy a bottom of the range house. But they won't of course.

Those of us who walked into the bonus of all but free housing, if the myths are to be believed, had to save up for the deposit. If anyone moaning about how good I had it wants to know what 'saving up' means, feel free to ask.

On top of that, the interest rate meant that for the first couple of years we were poorer than when we were saving. £36 18s 6p pcm. It meant that my wife's wages were all we lived on. My father said that he'd pay my mortgage if ever I was unemployed. That was a massive relief. My parents used to bring food parcels each week.

If I have it that good again, I'll probably kill myself.

If you stop moaning about how much better it was in the old days and start bloody saving, I'll stop telling you the realities of the 1970s and you can go back to your ignorance.

I remember an uncle of mine saying, after I moaned to him about the sacrifices (explanation of that word available as well) we were making, 'You don't know you'r alive.'

Now I know what he meant and how frustrated he must have felt at my complaints.

Oh please go and reread my post and dismount from your horse. I'm not talking about my personal circumstance. I graduated in '95 and have had a bumpy old road, but I'm generally comfortable about my lot. The reality was that it took 15 years of career for me to have a salary, and savings that allowed me to contemplate buying a house. I was in full time employment, in a job that paid over the average industrial wage. My wife was a PA to a publisher, greater take home pay than me.

We were engaged for around 20-22 months. In that time my fiancee's pay went into a fund for a deposit on a house. We went nowhere where we weren't subsidised or it was free. If we couldn't afford it, we didn't have it. A lovely 14-year-old Standard Pennant took me to work and occasionally us out for a Sunday - I worked most Saturdays - but not often. We didn't live together but with out separate parents. No electronic devices, no toys as such. My brother had gone through the same process a couple of years before.

The deposit did not cover the house we wanted and I had to borrow £75 from my parents. We bought a little bungalow in Hextable, trying to balance fares and housing costs. I could not afford a house in London in those days. Nor now come to that.

Yeah, we benefited all right.

If couples today didn't cohabit and pay rent and instead put one of their wages away each month for 18-20 months, did not pay for mobiles, pads, TV packages, games consoles and so much more, I have that sneaking feeling that they too could afford to buy a bottom of the range house. But they won't of course.

Those of us who walked into the bonus of all but free housing, if the myths are to be believed, had to save up for the deposit. If anyone moaning about how good I had it wants to know what 'saving up' means, feel free to ask.

On top of that, the interest rate meant that for the first couple of years we were poorer than when we were saving. £36 18s 6p pcm. It meant that my wife's wages were all we lived on. My father said that he'd pay my mortgage if ever I was unemployed. That was a massive relief. My parents used to bring food parcels each week.

If I have it that good again, I'll probably kill myself.

If you stop moaning about how much better it was in the old days and start bloody saving, I'll stop telling you the realities of the 1970s and you can go back to your ignorance.

I remember an uncle of mine saying, after I moaned to him about the sacrifices (explanation of that word available as well) we were making, 'You don't know you'r alive.'

Now I know what he meant and how frustrated he must have felt at my complaints.

I'm commenting on those who are starting out now, and to be clear that is not me. At least I can find it in my capability to be mildly empathetic to their situation.

The current situation is materially different to what has gone before.

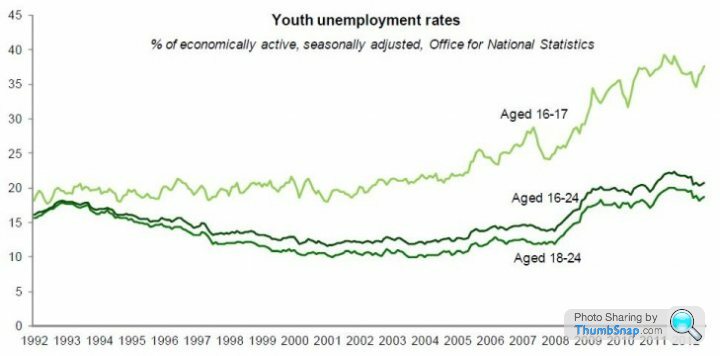

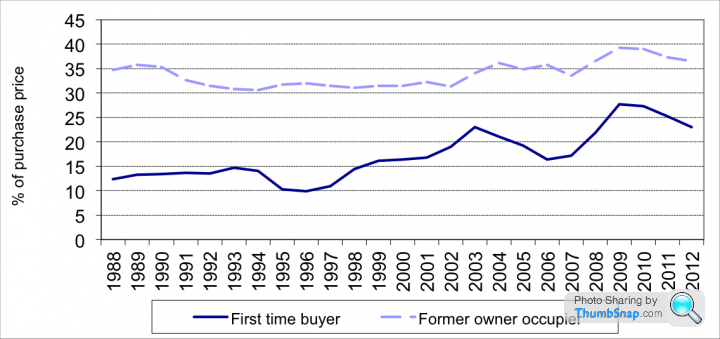

It is forecast by 2020 that the number of 25-34 yr olds buying their own house will drop from 60% (1995) to 20%. That is catastrophic, and not because they want to spend their money on mobile phones and consoles.

http://www.theguardian.com/business/2015/may/22/ho...

Similarly unemployment.

I get your generation had it hard. The 70s were not a picnic.

My generation had it tricky but not that bad, provided you surfed the boom, but getting stuck in a low paid job was a perpetual risk. The reality is however that my salary has moved the grand total of 10% in the last 10 years, but that's ok. It's hefty enough to be able to just about deal with the £1300 a month mortgage.

It is an utterly different order of challenge if you are under 30 today, and opportunities that were there back in 1970 *just do not exist* with an extremely hostile environment. Take deposit ratios for example.

That's crippling. Any money you are putting to that will be at the expense of pensions. It will almost certainly be at the expense of having a family.

Not impressed by overly defensive responses. I certainly am not blaming the older generations for the current situation. I am however pretty unimpressed generally, and certainly on this thread, by the lack of awareness of that older generation to the scale of the challenge, and that things are very different to how things were back when I was starting out, nevermind back in 68.

sidicks said:

Whether you are to blame or not does not change the fact that you'll be taking out from the system more than you put in.

You have a balanced view in the main but................Edited by sidicks on Tuesday 6th October 09:52

I have paid in to the NI/tax system 100's of thousands of pounds over my 45 years of employment, and yes for the last 20 years I was a higher tax rate payer.

From the state I will get less than half of the weekly equivalent of the minimum wage (£6.70 per hr) as my State Pension.

So if I am lucky enough to live another 15 years I will have contributed to the taxation system many times more than I will take out.

Luckily I managed to run two private/company pensions which by the way took a chunk out of my salary each month.

I am also still contributing to the system as I am taxed on my private pensions too.

I also would like to point out that there are many thousands of pensioners who are living on less than the minimum wage and really do struggle to just survive and in many cases are just left to face what is left of their life scared and alone. Maybe that would be a better debate to have rather than this.

We need to remember that we - the public - are the ones who have to take the crap from the political class and the "wealth providers" and they must just love the fact that we appear to be having a go at each other instead of focusing on the main causes of our various distressed states.

JagLover said:

crankedup said:

Our experiences at that time mirrors this ^^^^^^^^^^

We saved every penny toward a house deposit, during which time the first house price boom took off. Unfortunately we were still saving up at that point. First home furniture was all second hand except for the sofa which was chuck outs from the local shoe shop, two club chairs used by hundreds of new shoe shoppers Nigh on went bust in the mid eighties and more hard work long hours managed to come back. Happy days

With the way house prices have moved against earnings there are broad masses of people in the generations below you that cannot afford a house in a nice area near where they need to be for work no matter what sacrifices they make. Admittedly you sound a little unlucky, my parents bought in 1977 during a housing slump. We saved every penny toward a house deposit, during which time the first house price boom took off. Unfortunately we were still saving up at that point. First home furniture was all second hand except for the sofa which was chuck outs from the local shoe shop, two club chairs used by hundreds of new shoe shoppers

Nigh on went bust in the mid eighties and more hard work long hours managed to come back. Happy days You mention inheritance it is not something I am looking for at least 30 years hopefully (and given increased life expectancy hopefully that will be the case), so if and when it does come, the balance of the estate (after probable care home fees) will be split three ways and give me some extra savings in retirement. It is not going to change the fact that over the course of their lives the generations after the baby boomers will pay more to live in worse housing.

The inheritance issues will be down to individuals and how they want to financially assist their own families. For example, baby boomers can always down size and offer a lump sum from the equity to the kids, I would write in for use as house deposit only perhaps. The Government could help by adjustment of current gifting legislation. Won't help everybody but its one way forward perhaps, it could free up some rental property as more younger people can then get onto the housing ladder?

SPS said:

sidicks said:

Whether you are to blame or not does not change the fact that you'll be taking out from the system more than you put in

You have a balanced view in the main but................I have paid in to the NI/tax system 100's of thousands of pounds over my 45 years of employment, and yes for the last 20 years I was a higher tax rate payer.

From the state I will get less than half of the weekly equivalent of the minimum wage (£6.70 per hr) as my State Pension.

So if I am lucky enough to live another 15 years I will have contributed to the taxation system many times more than I will take out.

Luckily I managed to run two private/company pensions which by the way took a chunk out of my salary each month.

I am also still contributing to the system as I am taxed on my private pensions too.

I also would like to point out that there are many thousands of pensioners who are living on less than the minimum wage and really do struggle to just survive and in many cases are just left to face what is left of their life scared and alone. Maybe that would be a better debate to have rather than this.

We need to remember that we - the public - are the ones who have to take the crap from the political class and the "wealth providers" and they must just love the fact that we appear to be having a go at each other instead of focusing on the main causes of our various distressed states.

Fact is that the minority (circa 30% from memory) subsidise the remainder - the fact that people have paid NIC for X years does not mean that their state benefits are not being massively subsidised. Again it may be right to do so, but it does not change the facts!

Eric Mc said:

Not all pensioners' benefits are essential to life. There are plenty of pensioners who wouldn't notice such cuts e.g. - free bus travel, free TV licences etc.

I was about to try and make this point but you did it better Eric.Pensioner benefits should be means-tested - those who don't need them shouldn't sponge off the State when that money could be used beneficially elsewhere. A report from 2013 stated:

"On average, wealth is highest amongst the 45-64 year old age group; remains relatively high amongst the 65+ age group but is lower for households in which children or young adults (25-44) live."

That age group are the wealthiest in the country; to NOT means-test would be a dereliction of financial duty.

In the same way I don't receive any state benefits because of what I earn, the same should apply to pensioners who have significant wealth - I would have no objection to even redirecting recouped benefits payments to bolster those of the poorest pensioners.

They've taken positive steps with the TV Licence; previously this was chargeable and paid for out of Government funds for pensioners! Osborne has finally righted this wrong and said that they will be issued free of charge - a saving of hundreds of millions to the rest of us taxpayers. http://www.bbc.co.uk/news/entertainment-arts-33400...

We're moving in the right direction - cut where it can be done but we shouldn't lose sight of the fact that many pensioners rely on many of the benefits and we shouldn't do anything to jeopardize their well-being.

Funk said:

I was about to try and make this point but you did it better Eric.

Pensioner benefits should be means-tested - those who don't need them shouldn't sponge off the State when that money could be used beneficially elsewhere. A report from 2013 stated:

"On average, wealth is highest amongst the 45-64 year old age group; remains relatively high amongst the 65+ age group but is lower for households in which children or young adults (25-44) live."

That age group are the wealthiest in the country; to NOT means-test would be a dereliction of financial duty.

In the same way I don't receive any state benefits because of what I earn, the same should apply to pensioners who have significant wealth - I would have no objection to even redirecting recouped benefits payments to bolster those of the poorest pensioners.

They've taken positive steps with the TV Licence; previously this was chargeable and paid for out of Government funds for pensioners! Osborne has finally righted this wrong and said that they will be issued free of charge - a saving of hundreds of millions to the rest of us taxpayers. http://www.bbc.co.uk/news/entertainment-arts-33400...

We're moving in the right direction - cut where it can be done but we shouldn't lose sight of the fact that many pensioners rely on many of the benefits and we shouldn't do anything to jeopardize their well-being.

Unless of course the cost of doing so would outweigh the savings, something that is all too common with government beurocracy!Pensioner benefits should be means-tested - those who don't need them shouldn't sponge off the State when that money could be used beneficially elsewhere. A report from 2013 stated:

"On average, wealth is highest amongst the 45-64 year old age group; remains relatively high amongst the 65+ age group but is lower for households in which children or young adults (25-44) live."

That age group are the wealthiest in the country; to NOT means-test would be a dereliction of financial duty.

In the same way I don't receive any state benefits because of what I earn, the same should apply to pensioners who have significant wealth - I would have no objection to even redirecting recouped benefits payments to bolster those of the poorest pensioners.

They've taken positive steps with the TV Licence; previously this was chargeable and paid for out of Government funds for pensioners! Osborne has finally righted this wrong and said that they will be issued free of charge - a saving of hundreds of millions to the rest of us taxpayers. http://www.bbc.co.uk/news/entertainment-arts-33400...

We're moving in the right direction - cut where it can be done but we shouldn't lose sight of the fact that many pensioners rely on many of the benefits and we shouldn't do anything to jeopardize their well-being.

sidicks said:

Derek Smith said:

Quoted me, post above.

I'm not sure if you understand how the police 'pension scheme' worked.Edited by sidicks on Tuesday 6th October 09:52

A cut was taken from the pay of serving officers in theory to pay for the retired officers' pensions. It is a simple calculation that showed that more was taken out than paid out, and by a considerable percentage. From memory, it was the late 90s before the pension even drew even.

On top of that, there was an independent review of police pay and they came up with a figure, and then reduced it, using the pension scheme as the reason. So the >12% in real terms was considerably more. Not that the government honoured the independent review of course. Perish the thought.

You state that the cost will be twice what I paid in. Let's ignore the reduction in pay: many pension schemes include the employer paying an equal or greater amount in. Further, the calculations do not include interest.

The current pension arrangements are entirely different.

Re: the tax cus. Whatever the worth of those who are paid lots of money, if the money's not there, the reduction has to be paid for by the poor.

Re: the population rise. I didn't bring in silly party politics as if that was the answer, so will not do this time. However, some governments have blocked building homes and made councils sell homes at a massive loss for political advantage, which would have been bad enough, but then they were blocked from building any more.

But, and it is a big but, the government is there to plan for the future. They – of all colours – have failed. The blame is theirs. It is not as if the population increase occurred overnight. I knew the problem was coming some years ago, as did the authors of the articles I read. It was a dreadful bit of politicking. They should be ashamed of themselves. I'm ashamed of them.

You suggest I will be taking out of the system more than I put in. I'm not sure that is correct. I've paid taxes all my life, however they are called. I pay tax now. I also work now. It is the rich who get away without paying taxes. The rich can put untaxed money into their pension and then withdraw it later, again with tax concession. If anyone is getting more, it certainly ain't me.

I was head-hunted by private industry and the pension entitlement and other offers were greater than I received when a police officer. The person who accepted the post has a better pension than me, and has shares and such, and had other benefits of the company he was working for. And for shorter hours and better working conditions.

Derek Smith said:

I'm not sure if you understand how the police 'pension scheme' worked.

A cut was taken from the pay of serving officers in theory to pay for the retired officers' pensions. It is a simple calculation that showed that more was taken out than paid out, and by a considerable percentage. From memory, it was the late 90s before the pension even drew even.

How the cashflows work doesn't change the true cost - the true cost of the pension that you receive is entirely unrelated to the pension paid to some bloke who retired two decades ago.A cut was taken from the pay of serving officers in theory to pay for the retired officers' pensions. It is a simple calculation that showed that more was taken out than paid out, and by a considerable percentage. From memory, it was the late 90s before the pension even drew even.

Derek Smith said:

On top of that, there was an independent review of police pay and they came up with a figure, and then reduced it, using the pension scheme as the reason. So the >12% in real terms was considerably more. Not that the government honoured the independent review of course. Perish the thought.

The cost was based on a number of future assumptions which have proved to be wrong (in some cases very wrong) in practice.Derek Smith said:

You state that the cost will be twice what I paid in. Let's ignore the reduction in pay: many pension schemes include the employer paying an equal or greater amount in. Further, the calculations do not include interest.

Pension scheme funding does not ignore future interest - that's just a lack of understanding as to how such scheme funding is calculated.If the employer is paying it (in this case the taxpayer) then you are not paying it, hence the subsidy!!

Derek Smith said:

You suggest I will be taking out of the system more than I put in. I'm not sure that is correct. I've paid taxes all my life, however they are called. I pay tax now. I also work now.

The top 30% subsidise the remaining 70% in terms of goods and services receive compared to taxes paid. If you have a public sector pension then that skews the percentages even more.Derek Smith said:

It is the rich who get away without paying taxes. The rich can put untaxed money into their pension and then withdraw it later, again with tax concession. If anyone is getting more, it certainly ain't me.

Nice try but the data exists as to who pays the most tax and who subsidises who, and it's not what you are suggesting!Derek Smith said:

I was head-hunted by private industry and the pension entitlement and other offers were greater than I received when a police officer. The person who accepted the post has a better pension than me, and has shares and such, and had other benefits of the company he was working for. And for shorter hours and better working conditions.

You do realise that the vast majority of the private sector ceased offering final salary schemes 10+ years ago?Ridgemont said:

It is forecast by 2020 that the number of 25-34 yr olds buying their own house will drop from 60% (1995) to 20%. That is catastrophic, and not because they want to spend their money on mobile phones and consoles.

http://www.theguardian.com/business/2015/may/22/ho...

Catastrophic is the word.http://www.theguardian.com/business/2015/may/22/ho...

Not only are they unable to get on the ladder, they're bled dry for rent whilst the ownership goalposts move ever further away on a rolling basis. They've not even started a mortgage by the point their parents were halfway through paying theirs off. As a country, the rental situation means we're storing up huge issues for future generations (unless you're a landlord!) because at the point where you should have paid off a house and have no mortgage overhead, people will now have to continue to find ever-increasing rental costs until they die.

My mother is in such a position. She lived with her partner in a property which would have been their retirement home. He developed Parkinsons with dementia in his mid-50s and now, not even a decade later, doesn't recognise her. She still works and couldn't care for him full time so he's in the hands of specialist care and the property was sold to fund it as his pensions weren't enough - it wasn't in his game plan to have to fall back on pensions so early. She's now renting and I'm making plans for how I can begin to support her when she reaches the point where she can no longer work as she won't be able to survive on her pension with the way rents are going. I'm not wealthy and am trying to build my own life (mid-30s, lucky to get on the ladder a decade ago but not been able to move up yet) but unlike many of my friends I have no inheritance coming from anywhere so it's all on me - there's no financial booster to give me a leg-up.

The current situation with property shouldn't have been allowed to develop and the worst of it is yet to manifest.

Funk said:

Ridgemont said:

It is forecast by 2020 that the number of 25-34 yr olds buying their own house will drop from 60% (1995) to 20%. That is catastrophic, and not because they want to spend their money on mobile phones and consoles.

http://www.theguardian.com/business/2015/may/22/ho...

Catastrophic is the word.http://www.theguardian.com/business/2015/may/22/ho...

Not only are they unable to get on the ladder, they're bled dry for rent whilst the ownership goalposts move ever further away on a rolling basis. They've not even started a mortgage by the point their parents were halfway through paying theirs off. As a country, the rental situation means we're storing up huge issues for future generations (unless you're a landlord!) because at the point where you should have paid off a house and have no mortgage overhead, people will now have to continue to find ever-increasing rental costs until they die.

IroningMan said:

That's exactly the point. I'm 48 and spending a considerable amount on the welfare of current pensioners. When I am able to retire at, I anticipate, 75 or so, I fully expect that there will be no such largesse aimed at me - if there is such a thing as a State Pension by then it will be means-tested out of existence for anyone who has a private or company pension.

Everyone seems to be assuming that there will either be no state pension or it will be heavily means tested in a generations time, but certainly any Tory government would have to be certifiable to even think about such a change and I am not so sure Labour will be so keen either, particularly as the people with the most income in retirement will tend to be state workers (their core support) on final salary pension schemes.Certainly changes like this would cause REAL anger not just irritating a few crusties with nose rings as Boris described the recent protestors.

crankedup said:

I certainly agree that many young people are unable to fund their own home, but I have acknowledged that earlier.

The inheritance issues will be down to individuals and how they want to financially assist their own families. For example, baby boomers can always down size and offer a lump sum from the equity to the kids, I would write in for use as house deposit only perhaps. The Government could help by adjustment of current gifting legislation. Won't help everybody but its one way forward perhaps, it could free up some rental property as more younger people can then get onto the housing ladder?

I think most being able to buy their own home are already relying on the bank of mum and dad. The inheritance issues will be down to individuals and how they want to financially assist their own families. For example, baby boomers can always down size and offer a lump sum from the equity to the kids, I would write in for use as house deposit only perhaps. The Government could help by adjustment of current gifting legislation. Won't help everybody but its one way forward perhaps, it could free up some rental property as more younger people can then get onto the housing ladder?

Downsizing might be possible but often depends on being able to get somewhere close to children and grand children.

Simple answer

1.Move the winter fuel allowance into state pension

2. Have a separate income tax threshold for 75yo or whatever age the winter fuel allowance comes in and say anyone earning over £20k drop the allowance enough to strip out the winter fuel allowance. This move totally eliminates the means tested and the cost the the testing.

Also what is the actual cost currently of

1. Free TV licence

2. free bus service

3. Winter fuel allowance

It could be that these are so small in total govt budget terms it's really pointless wasting time trying to fix it.

1.Move the winter fuel allowance into state pension

2. Have a separate income tax threshold for 75yo or whatever age the winter fuel allowance comes in and say anyone earning over £20k drop the allowance enough to strip out the winter fuel allowance. This move totally eliminates the means tested and the cost the the testing.

Also what is the actual cost currently of

1. Free TV licence

2. free bus service

3. Winter fuel allowance

It could be that these are so small in total govt budget terms it's really pointless wasting time trying to fix it.

Gassing Station | News, Politics & Economics | Top of Page | What's New | My Stuff