9% instant access savings accounts

Discussion

MarshPhantom said:

At the risk of repeating myself.

Average UK savings - £10k.

Average UK mortgage - £85k.

Not everyone has a mortgage, believe it or not, not everyone has savings.

I'm off.

As was pointed out above

Number of mortgages - 9.2m

Number of households - 27m

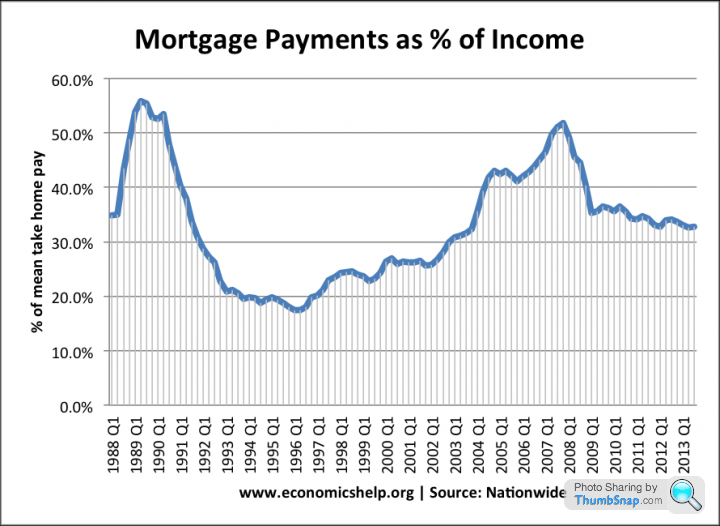

Furthermore when low interest persist for a decade or more you cannot simply look at mortgage rates in isolation and say that makes everyone better off. 3% on a £200K mortgage is the same as 6% on a £100K one and in many parts of the country that is probably the level of increase in mortgage debt needed since 2008.

In the main ultra-low interest rates have reduced outgoings for the already affluent and made life harder for the rest.

JagLover said:

MarshPhantom said:

At the risk of repeating myself.

Average UK savings - £10k.

Average UK mortgage - £85k.

Not everyone has a mortgage, believe it or not, not everyone has savings.

I'm off.

As was pointed out above

Number of mortgages - 9.2m

Number of households - 27m

Furthermore when low interest persist for a decade or more you cannot simply look at mortgage rates in isolation and say that makes everyone better off. 3% on a £200K mortgage is the same as 6% on a £100K one and in many parts of the country that is probably the level of increase in mortgage debt needed since 2008.

In the main ultra-low interest rates have reduced outgoings for the already affluent and made life harder for the rest.

Cotty said:

Dr Doofenshmirtz said:

I wish we could go back to those rates!!

I wish but as someone mentioned the mortgage rates were killer. Mind you as im about to pay mine off im not that worried.House prices are driven largely by what people can afford - they're constantly at the edge of affordability. Drop interest rates to the point where mortgages halve and house buyers don't end up paying half as much every month, house prices increase until those people are back at the edge of their monthly payments.

Yes, lower interest rates now, but lower payments on a house/affordability basis?

Ari said:

No they weren't, because houses were far cheaper so the repayments balanced out.

I see what you are saying but 8.6% was a killer for me when I took my mortgage out. Im not sure I could get a mortgage on my that property now, let alone pay it even at todays rates. The capital payment would cripple me without taking the interest into account.Cotty said:

Ari said:

No they weren't, because houses were far cheaper so the repayments balanced out.

I see what you are saying but 8.6% was a killer for me when I took my mortgage out. Im not sure I could get a mortgage on my that property now, let alone pay it even at todays rates. The capital payment would cripple me without taking the interest into account.Mortgages are killers for most people initially, whatever the reason. That's what I mean about being on the limit of affordability, most people with their first mortgage are on that limit. Lower the interest rate and the prices rise till they're back on the limit - hence the situation we're now in.

Ari said:

Mortgages are killers for most people initially, whatever the reason. That's what I mean about being on the limit of affordability, most people with their first mortgage are on that limit. Lower the interest rate and the prices rise till they're back on the limit - hence the situation we're now in.

Indeed they are. So what you need is a healthy dose of inflation to erode your debt. But now with low inflation for years, people continue to be strapped for years.During my parents time, interest rates where consistently above 10%. My parents struggled, scrimped and saved for years to be able to buy their first house. Their mortgage was their biggest monthly outgoing\burden.

During my time interest rates have been consistently below 5%. I struggled, scrimped and saved for years to be able to buy my first house and my mortgage is my biggest monthly outgoing\burden.

I don't see that much has changed to be honest.

During my time interest rates have been consistently below 5%. I struggled, scrimped and saved for years to be able to buy my first house and my mortgage is my biggest monthly outgoing\burden.

I don't see that much has changed to be honest.

Guvernator said:

During my parents time, interest rates where consistently above 10%. My parents struggled, scrimped and saved for years to be able to buy their first house. Their mortgage was their biggest monthly outgoing\burden.

During my time interest rates have been consistently below 5%. I struggled, scrimped and saved for years to be able to buy my first house and my mortgage is my biggest monthly outgoing\burden.

I don't see that much has changed to be honest.

Precisely my point above. It's not about interest rates, it's about repayments. Lower the interest rates and property rises back to the limit of affordability. During my time interest rates have been consistently below 5%. I struggled, scrimped and saved for years to be able to buy my first house and my mortgage is my biggest monthly outgoing\burden.

I don't see that much has changed to be honest.

Ari said:

Precisely my point above. It's not about interest rates, it's about repayments. Lower the interest rates and property rises back to the limit of affordability.

I think it has risen above the limit of affordability. Some people are resigned to the fact they will never be able to buy a house.

The bank we use, Halifax, has just announced that it is to reduce its interest rates on current accounts to 0.05%. My other half had already drawn out savings from there and elsewhere in favour of premium bonds. Good move as the first eligible draw for the new bonds produced a win. Sadly we will not be vying for a mooring with P. Green's boat this time, it was a miniscule £25.Still better than the 0.05% though

Gassing Station | News, Politics & Economics | Top of Page | What's New | My Stuff