Pension gain in the last 2 years

Discussion

I have a company pension and use one of the big pension companies to manage it. I have split the funds into a mixed portfolio of a Jupiter fund and a Blackrock fund. In the two years I have had the pension including the amount I transferred in, it is around the 40k mark. I have seen in the 2 years, "just" £2k growth, which equates to around 4.5%. I guess I was expecting more, even in these lean economic times. Should I just be grateful or when the stock markets gets back to pre-2008 levels, could/should I expect to see see a bigger rise?

type-r said:

Actually just 2.25% growth per year.

If it makes you feel any better, I asked about the rate for cash deposit part of my pension, this is a fund holding holding millions, 0.02% I was told, when I asked who agreed such a low rate, when at the time I had been able to get 4% over 3 years in a savings account, they were not happy when I said I hope somebody got a good backhander out of the deal.

Doesn't it depend on the funds? I would have thought last few years would have seen a good return, I've had people saying "you should put your pension with xyz who I have it with, they've made y% in the last few years" without thinking that the stock market has made y% in the last few years (or more). Are you in very cautious, low risk funds? They should have looked at your risk appetite when putting you into them. A prospective adviser asked me if I was aware that I'd lost 22% of my funds value in recent years, across the period that stock markets had tanked. I wasn't particularly, but then of course this gave him the opportunity to say he could put me in much less risky situation, of course he could but then the returns wouldn't have been so good.

Thpe R

Firstly, the important stuff. Nice buyers guide in this week's Autocar. Made em almost want one..

Anyway, whichever route you go down with your Jupiter and Black Rock, your thinking right now and your behaviour is critical to your success, just as important as the types of funds you selected with them (passive, active or somewhere in between). It's important right now because your emotions are running high and the markets, as we have seen these past few weeks, are running low. Still, ebola, the Neverendum, European Central Bank prevarication, dubious economic data from Germany and the Ukraine.. well, it was always going to end in tears wasn't it?

One of the biggest difficulties that I, as an adviser, face is getting people to stay the course when results are temporarily disappointing. Let's face it, we all know that markets go up and they go down. When they go down, there’s a tendency for people to eject and when they are going well, there is a tendency for people to buy in. Fear and greed, that short termism governs and taints so many people's perspectives.

2.5% may sound appalling, but is it ok given the sectors you're investing in right now? And are you having your ankles chopped away by having someone charge you too much for the privilege of looking after your money? Don't obsess about the funds and the superficial stuff, get back to basics, see if your original objectives and your original 'big picture' is still as valid today as you thought it was then.

Jupiter and Black Rock are not dummies. But scratching at that 2.5% return right now is the worse thing you could do, (simply because it is bugging you that is!). Take a deep breath, retrace your steps and go back to basics. Don't rush things, take your time. If you need any help, just put the questions down here and I'm sure there'll be a wealth of experience and insight that you can tap into.

Firstly, the important stuff. Nice buyers guide in this week's Autocar. Made em almost want one..

Anyway, whichever route you go down with your Jupiter and Black Rock, your thinking right now and your behaviour is critical to your success, just as important as the types of funds you selected with them (passive, active or somewhere in between). It's important right now because your emotions are running high and the markets, as we have seen these past few weeks, are running low. Still, ebola, the Neverendum, European Central Bank prevarication, dubious economic data from Germany and the Ukraine.. well, it was always going to end in tears wasn't it?

One of the biggest difficulties that I, as an adviser, face is getting people to stay the course when results are temporarily disappointing. Let's face it, we all know that markets go up and they go down. When they go down, there’s a tendency for people to eject and when they are going well, there is a tendency for people to buy in. Fear and greed, that short termism governs and taints so many people's perspectives.

2.5% may sound appalling, but is it ok given the sectors you're investing in right now? And are you having your ankles chopped away by having someone charge you too much for the privilege of looking after your money? Don't obsess about the funds and the superficial stuff, get back to basics, see if your original objectives and your original 'big picture' is still as valid today as you thought it was then.

Jupiter and Black Rock are not dummies. But scratching at that 2.5% return right now is the worse thing you could do, (simply because it is bugging you that is!). Take a deep breath, retrace your steps and go back to basics. Don't rush things, take your time. If you need any help, just put the questions down here and I'm sure there'll be a wealth of experience and insight that you can tap into.

Edited by Ginge R on Monday 27th October 23:38

Thanks for the replies guys. Indeed I am trying to look at the long term and understand short term returns can fluctuate greatly but over the course of time, should come good (hopefully!).

I have diversified into following 3 funds for my personal pension (including one run by the pension company):

SL BlackRock UK Equity Tracker Pension Fund (~50%)

SL Jupiter Merlin Growth Portfolio Pension Fund (~25%)

Standard Life Deposit and Treasury Pension Fund (~25%)

I picked the above funds, without seeking advice from an IFA. I did some basic research, weighed up the risks and selected those.

I have diversified into following 3 funds for my personal pension (including one run by the pension company):

SL BlackRock UK Equity Tracker Pension Fund (~50%)

SL Jupiter Merlin Growth Portfolio Pension Fund (~25%)

Standard Life Deposit and Treasury Pension Fund (~25%)

I picked the above funds, without seeking advice from an IFA. I did some basic research, weighed up the risks and selected those.

I think you have done the math wrong.

If you are in those funds for the last two years you can't possibly have returned just 2.5%.

I suspect you may have had only a much smaller amount in the Nov-12 to Nov-13 period (which had good gains) and more in the period since which is flat to down.

You have to take into account the proportions.

That Blackrock one looks like a terrible tracker though. Although I am no fund pro - Ginge R can give proper advice.

If you are in those funds for the last two years you can't possibly have returned just 2.5%.

I suspect you may have had only a much smaller amount in the Nov-12 to Nov-13 period (which had good gains) and more in the period since which is flat to down.

You have to take into account the proportions.

That Blackrock one looks like a terrible tracker though. Although I am no fund pro - Ginge R can give proper advice.

I did transfer in at some point towards the end of last year from another private pension scheme, so I guess the overall figure of 2.25% is skewed because of that.

ETA: Just double checked online and I actually moved out of the Jupiter fund last year (which was 100%) and have split the share as follows:

SL BlackRock Aquila HP UK Equity Pension Fund 70.0%

Standard Life Managed Cash Pension Fund 30.0%

For some reason, it is showing the a summary of a 50/25/25 split across 3 which is what I stated above.

ETA: Just double checked online and I actually moved out of the Jupiter fund last year (which was 100%) and have split the share as follows:

SL BlackRock Aquila HP UK Equity Pension Fund 70.0%

Standard Life Managed Cash Pension Fund 30.0%

For some reason, it is showing the a summary of a 50/25/25 split across 3 which is what I stated above.

I'm confused about what you transferred in and out of and when - if the 40k wasn't in those funds for the last 2-3 years it is difficult to assess their performance over that time horizon ? Are you saying that 100% was in the Jupiter for most of it? 100% of 40k or you did a transfer in from elsewhere?

silverous said:

I'm confused about what you transferred in and out of and when - if the 40k wasn't in those funds for the last 2-3 years it is difficult to assess their performance over that time horizon ? Are you saying that 100% was in the Jupiter for most of it? 100% of 40k or you did a transfer in from elsewhere?

Ok - I understand it is slightly confusing without having all the info. In summary for the last 2 years:In Feb 2013, I transferred in 17.5k. I have contributed in the last 2 years, 21k. Total 38.5k. Balance currently stands at 40.5k

I can't remember when I made the change but let's say at the start of this year, I went from 100% Jupiter to 70/30 split mentioned in my previous post.

Bottom line, in two years I have increased my personal pension from say around 20k to 40k from my own personal/company contributions but have only realised a 2k return in that time.

type-r said:

silverous said:

I'm confused about what you transferred in and out of and when - if the 40k wasn't in those funds for the last 2-3 years it is difficult to assess their performance over that time horizon ? Are you saying that 100% was in the Jupiter for most of it? 100% of 40k or you did a transfer in from elsewhere?

Ok - I understand it is slightly confusing without having all the info. In summary for the last 2 years:In Feb 2013, I transferred in 17.5k. I have contributed in the last 2 years, 21k. Total 38.5k. Balance currently stands at 40.5k

I can't remember when I made the change but let's say at the start of this year, I went from 100% Jupiter to 70/30 split mentioned in my previous post.

Bottom line, in two years I have increased my personal pension from say around 20k to 40k from my own personal/company contributions but have only realised a 2k return in that time.

The question I would be asking in your position is how well have the funds I chose performed relative to their benchmark?

THEN ask whether you have put your money into funds focusing on the RIGHT BENCHMARK.

If they performed relatively in-line - then any "underperformance" is purely to do with the timing of your investments or your allocation to the funds. (e.g. the fund beat the benchmark but the benchmark did poorly so you should have chosen a different fund aiming to beat a different benchmark.)

So if for example I was invested in a FTSE tracker that matched the FTSE perfectly but the FTSE was down 10% while the S&P (US based) was UP 10% then it is my fault for choosing a UK focused fund not a US focused one.

These types of fund are set up to focus all their efforts on beating their benchmark. That's their job.

The key is really down to benchmark selection. And that is your job (for this style of investing).

Put it and leave it, choose a conservative fund, but one where the manager is no too handcuffed.

Your performance is quite poor.

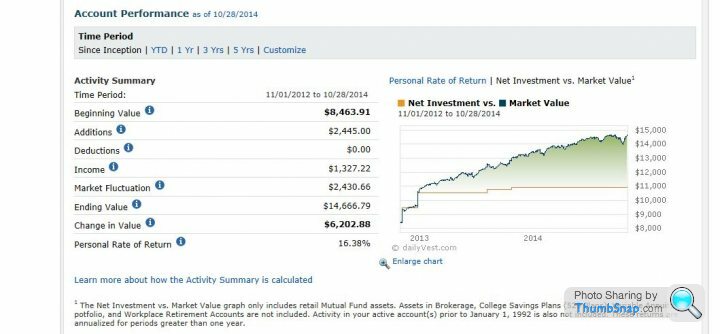

I've just grabbed a screen shot of one of my wife's funds because it was initiated almost 2 years ago to the day. So good for comparison.

This is not a high flyer, the manager holds Bonds as well as shares.

This is a plod along safe fund. Chosen for her because I don't like to be yelled at

Annulised return of 16%

Gross rtn 34%

PRWCX T.R.PRICE Cap Appreciation

Faltering a bit recently but still satisfactory.

Your performance is quite poor.

I've just grabbed a screen shot of one of my wife's funds because it was initiated almost 2 years ago to the day. So good for comparison.

This is not a high flyer, the manager holds Bonds as well as shares.

This is a plod along safe fund. Chosen for her because I don't like to be yelled at

Annulised return of 16%

Gross rtn 34%

PRWCX T.R.PRICE Cap Appreciation

Faltering a bit recently but still satisfactory.

type-r said:

I did transfer in at some point towards the end of last year from another private pension scheme, so I guess the overall figure of 2.25% is skewed because of that.

ETA: Just double checked online and I actually moved out of the Jupiter fund last year (which was 100%) and have split the share as follows:

SL BlackRock Aquila HP UK Equity Pension Fund 70.0%

Standard Life Managed Cash Pension Fund 30.0%

For some reason, it is showing the a summary of a 50/25/25 split across 3 which is what I stated above.

Is this your Standard Life managed cash fund?ETA: Just double checked online and I actually moved out of the Jupiter fund last year (which was 100%) and have split the share as follows:

SL BlackRock Aquila HP UK Equity Pension Fund 70.0%

Standard Life Managed Cash Pension Fund 30.0%

For some reason, it is showing the a summary of a 50/25/25 split across 3 which is what I stated above.

http://www.trustnet.com/Factsheets/Factsheet.aspx?...

As you can see, the performance is hardly going to quicken anyone's pulse. The objective of something like that is to dampen things out, to park cash before cashing out etc, and not to grow wealth. If 70% of your fund is trying to sprint ahead but 30% is saying 'whoa' then you're going to end up with a bit of a mish-mash outcome. It's like a sprinter competing with one miner's boot on one foot and a sprint shoe on the other.

When you left your personal pension, were there any charges or costs associated with transferring at all? There shouldn't have been. Bear in mind too, that although equity performance is generally appalling at the moment it represents the sector and not your specific fund. That doesn't make the malaise any more palatable right now but it might explain it and put it into context.

Fund performance is important, but remember that provider and adviser costs will also impact on returns. Trustnet offers a free service.

http://www.trustnet.com.

http://www.trustnet.com.

Gassing Station | Finance | Top of Page | What's New | My Stuff