Car PCP and deposits on them

Discussion

pigeonskirt said:

sidicks said:

pigeonskirt said:

Sidicks, are you in the motor trade?

No, is that relevant?Edited by sidicks on Saturday 28th February 19:13

I've worked at a main franchise (in sales) for 8 years. Most of our finance is now PCP. Let me tell you, if you put a large deposit in, it can be extremely difficult to re deal at the end of your plan. Generally speaking, people use a large deposit to give artificially low payments. They then get used to this, come back to re deal in 3 years, and wonder why their payment goes from £165 to £245 a month. There are cases where putting in a large deposit on PCP is beneficial..perhaps they are just planning on paying off the balloon at the end. Perhaps they are cash customers taking PCP to get an FDA (that's a deposit allowance from the finance company) which they will then settle off early. They may even want to use a large deposit to lower the GFV and at the same time the amount borrowed to lower interest (which is where I think you're coming from) but again, in the real world this doesn't really happen...mainly because the monthly payment then becomes unaffordable.

Most people you're dealing with are maxing out their credit. If they want a new car the only way to do it is on a PCP so they can't make choices. There's no way they're going to put more into the deposit - they simply don't have any free cash - but they probably could stretch to another £50/mth. However give them that £50 back and would they save it towards the deposit on their next car? Hell no, they'd spend it on something.

So it makes perfect sense to keep them on a monthly which is likely to repeatable for future deals.

oop north said:

Mastiff said:

Unless I'm misreading that, I think you may have missed the point. The analogy is meant to reflect the merits/downsides of wholly owning or renting an asset that is definately going to depreciate. I could have used the word "Reindeer" instead of "Flat" but then you probably would only have had a go at me about fluctuations in the Caribou market?

Missed what point? In my opinion, the whole argument about owning or leasing a depreciating asset (you must "always" hire it) is a nonsense. I maintain that property is a lousy example (it is in a class of its own, really) - it just pushes the person looking at the example to give a conclusion that suits the person putting their argument forward. It seems to me that the nub is this:

- it might well be reasonable to say that you should not rent an appreciating asset (because that way you lose the benefit of appreciation)

but

- it does not follow that you should not rent a depreciating asset - because in general you cannot avoid the depreciation

With a PCP you might be able to limit the depreciation to a maximum amount, but you are still going to have to pay for it (unless the manufacturer is promoting one particular type of purchase over others - e.g., Golf R lease). You don't magically get rid of depreciation by leasing something (if you did, you wouldn't need GAP insurance would you?) - someone's going to have to pay for it

Mastiff said:

As to whether or not it's the "right" way to buy a car, surely that's down to the individual?

Yes - and most of the argument here is between traders who tell customers they should keep the deposit down because it's better for them, without pointing out that it will cost them a lot more in the long run. I and others are pointing out the folly of just believing what the people in the trade say - ie, that following their advice will cost more moneyI totally agree with your second point and believe it or not, there are new FCA regulations that are trying to cover how these are sold - as a dealer you SHOULD always advise the customer on the cheapest way to purchase, whichever way that client wishes to purchase, if you follow me.

I do have the advantage of speaking from a position that the manufacturer I work for sets GFV very low, ensuring that I have not had a vehicle in negative equity in the 5 years that I have been here - in fact changing the vehicle is often possible with no additional deposit. I have also known monthly payments GO DOWN because there is enough equity in the current car. The downside of all of that is that the monthly payments are higher than our competitors but as you say, it's just maths and the money has to come from somewhere.

The popularity of PCP finance seems to have come about from drivers coming out of company cars and using their monthly allowance to finance a new vehicle. Replacing the vehicle every 3 years keeps it up to date and gives many of the benefits and peace of mind that an employer provided vehicle would. It is probably very popular with manufacturers and dealers because it encourages customers to return every 2-3 years, buying a new vehicle and providing a nice 2-3 year old car for the used forecourt.

If you can put down a larger deposit I think it makes sense to reduce the balloon payment, giving a larger deposit towards your next car or making it easier to pay the balance and keep the one you have.

I can see PCP making a lot of sense if you are at the stage in life where you have a good income but large mortgage and little capital. It is also possibly better to finance your car with easy payments and keep investing in ISAs and pensions, rather than losing a year or more allowance.

If you can put down a larger deposit I think it makes sense to reduce the balloon payment, giving a larger deposit towards your next car or making it easier to pay the balance and keep the one you have.

I can see PCP making a lot of sense if you are at the stage in life where you have a good income but large mortgage and little capital. It is also possibly better to finance your car with easy payments and keep investing in ISAs and pensions, rather than losing a year or more allowance.

Dr Jekyll said:

I was responding to your argument that "(people don't buy with cash because) they can do other things with that money".

I understood what you were replying to, I just didn't want people to think that I meant...Dr Jekyll said:

Do you really believe that the bulk of PCP buyers put their capital into something that gives a higher after tax return than the interest they are paying?

...because I didn't! I may be in the Motor Trade but I'm not a fool.

sidicks said:

The fact remains, a larger deposit remains the cheaper way to finance a car, due to the (often) significant amount of interest saved, yet apparently car finance salesman don't appear to understand this...

Disputing this demonstrates a major lack of understanding.

In the short term, yes. The major lack of understand of how PCP agreements work and how interest is calculated on them though, is yours. Disputing this demonstrates a major lack of understanding.

Edited by sidicks on Saturday 28th February 19:54

Let's work backwards. The MGFV isnt just a figure plucked out of thin air. They are calculated by looking at historical trade values, depreciation from new etc. very simply put, if you purchase a car for £30k, whatever the MGFV you expect to have an equity return of around 10-15% should you p/ex the car. If you put in more than that, it's money that won't be coming back. In effect, you have paid more deposit for a short term reduction in payments.

But then you'll tell us 'you save on interest if you put more deposit in'

In a normal HP agreement, yes but once again, a fundemental lack of understanding of how interest is calculated on a PCP. You are paying a much higher rate on that amount than the bit you are paying back. You really wont save much by putting in a bigger deposit as there is no way of reducing that chunk of interest.

Like it or not, the best and lowest cost way overall with a PCP is low deposit. Frankly, if the OP is intending ownership its the wrong finance in the firstplace.

TVR1 said:

In the short term, yes. The major lack of understand of how PCP agreements work and how interest is calculated on them though, is yours.

Let's work backwards. The MGFV isnt just a figure plucked out of thin air. They are calculated by looking at historical trade values, depreciation from new etc. very simply put, if you purchase a car for £30k, whatever the MGFV you expect to have an equity return of around 10-15% should you p/ex the car. If you put in more than that, it's money that won't be coming back. In effect, you have paid more deposit for a short term reduction in payments.

But then you'll tell us 'you save on interest if you put more deposit in'

In a normal HP agreement, yes but once again, a fundemental lack of understanding of how interest is calculated on a PCP. You are paying a much higher rate on that amount than the bit you are paying back. You really wont save much by putting in a bigger deposit as there is no way of reducing that chunk of interest.

Like it or not, the best and lowest cost way overall with a PCP is low deposit. Frankly, if the OP is intending ownership its the wrong finance in the firstplace.

This is all kinds of wrongLet's work backwards. The MGFV isnt just a figure plucked out of thin air. They are calculated by looking at historical trade values, depreciation from new etc. very simply put, if you purchase a car for £30k, whatever the MGFV you expect to have an equity return of around 10-15% should you p/ex the car. If you put in more than that, it's money that won't be coming back. In effect, you have paid more deposit for a short term reduction in payments.

But then you'll tell us 'you save on interest if you put more deposit in'

In a normal HP agreement, yes but once again, a fundemental lack of understanding of how interest is calculated on a PCP. You are paying a much higher rate on that amount than the bit you are paying back. You really wont save much by putting in a bigger deposit as there is no way of reducing that chunk of interest.

Like it or not, the best and lowest cost way overall with a PCP is low deposit. Frankly, if the OP is intending ownership its the wrong finance in the firstplace.

TVR1 said:

Let's work backwards. The MGFV isnt just a figure plucked out of thin air. They are calculated by looking at historical trade values, depreciation from new etc. very simply put, if you purchase a car for £30k, whatever the MGFV you expect to have an equity return of around 10-15% should you p/ex the car. If you put in more than that, it's money that won't be coming back. In effect, you have paid more deposit for a short term reduction in payments.

I don't understand what you're saying here? Every PCP quote has a "Total Amount Payable". (deposit + fees + monthly payments + GFV ). The GFV doesn't depend on the deposit, but on the parameters you've said.

As you increase the deposit, the total amount payable will go DOWN not up.

Also GFV's can be "plucked out of thin air" if required. I have an 18 month PCP quote for a 46K car in front of me. The deposit is 50% and the GFV is just over £2K. This minimizes the "total amount payable" given that I plan to pay off the finance and owning the car outright after 6 months.

silentbrown said:

TVR1 said:

Let's work backwards. The MGFV isnt just a figure plucked out of thin air. They are calculated by looking at historical trade values, depreciation from new etc. very simply put, if you purchase a car for £30k, whatever the MGFV you expect to have an equity return of around 10-15% should you p/ex the car. If you put in more than that, it's money that won't be coming back. In effect, you have paid more deposit for a short term reduction in payments.

I don't understand what you're saying here? Every PCP quote has a "Total Amount Payable". (deposit + fees + monthly payments + GFV ). The GFV doesn't depend on the deposit, but on the parameters you've said.

As you increase the deposit, the total amount payable will go DOWN not up.

Also GFV's can be "plucked out of thin air" if required. I have an 18 month PCP quote for a 46K car in front of me. The deposit is 50% and the GFV is just over £2K. This minimizes the "total amount payable" given that I plan to pay off the finance and owning the car outright after 6 months.

If you increase the deposit then, sure, it reduces the interest, but only by a relatively small amount as the interest on the payments is declining anyway throughout the term.

Especially with low interest rates, it's not the significant saving that sidicks suggested earlier - in the great scheme of things, it's small beer. For the industry, it's a bad thing for repeat business as it gets the customer used to low payments.

Sheepshanks said:

He's saying the GFV is fixed. Therefore the interest on it is a fixed amount.

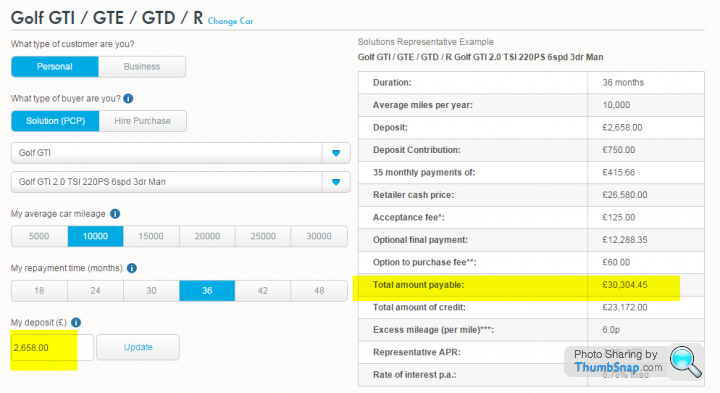

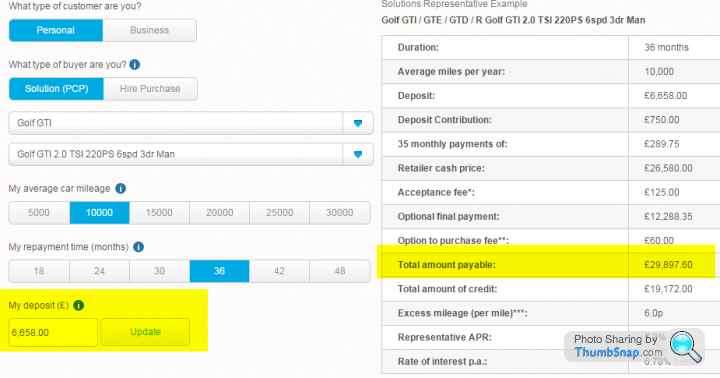

That's true. but the GFV (depending on term) is usually well under half of the amount borrowed. Here's some real examples. Golf R with 2,658 (minimum deposit)

... versus £6658 deposit. (the max that VW allows is around £7500. They don't allow more because that would reduce their profit too much!)

So an additional £4,000 deposit is cheaper by over £400 over the 3 years. Depends on your view of small beer.

FWIW I picked up my car today, my baloon is tiny, £3200 to be precise, in 3 years I am guaranteed a minimum of around 5.5k hopefully more which means I will have 2.5 to 3k deposit on the next car. ( The person I am dealing with is a friend of 10 years, so I know this to be accurate ).

I put down £1k deposit, which has removed some negative equity on my trade in plus given me a deposit of 750 ish. All in all for a new car I think this is pretty good, under 180 a month, free servicing for 3 years, no tax, tank of fuel plus fully fitted mats and styling kit all chucked in.

I will think carefully about PCP deposit amounts in the future though!

I put down £1k deposit, which has removed some negative equity on my trade in plus given me a deposit of 750 ish. All in all for a new car I think this is pretty good, under 180 a month, free servicing for 3 years, no tax, tank of fuel plus fully fitted mats and styling kit all chucked in.

I will think carefully about PCP deposit amounts in the future though!

TheHound said:

TVR1 said:

In the short term, yes. The major lack of understand of how PCP agreements work and how interest is calculated on them though, is yours.

Let's work backwards. The MGFV isnt just a figure plucked out of thin air. They are calculated by looking at historical trade values, depreciation from new etc. very simply put, if you purchase a car for £30k, whatever the MGFV you expect to have an equity return of around 10-15% should you p/ex the car. If you put in more than that, it's money that won't be coming back. In effect, you have paid more deposit for a short term reduction in payments.

But then you'll tell us 'you save on interest if you put more deposit in'

In a normal HP agreement, yes but once again, a fundemental lack of understanding of how interest is calculated on a PCP. You are paying a much higher rate on that amount than the bit you are paying back. You really wont save much by putting in a bigger deposit as there is no way of reducing that chunk of interest.

Like it or not, the best and lowest cost way overall with a PCP is low deposit. Frankly, if the OP is intending ownership its the wrong finance in the firstplace.

This is all kinds of wrongLet's work backwards. The MGFV isnt just a figure plucked out of thin air. They are calculated by looking at historical trade values, depreciation from new etc. very simply put, if you purchase a car for £30k, whatever the MGFV you expect to have an equity return of around 10-15% should you p/ex the car. If you put in more than that, it's money that won't be coming back. In effect, you have paid more deposit for a short term reduction in payments.

But then you'll tell us 'you save on interest if you put more deposit in'

In a normal HP agreement, yes but once again, a fundemental lack of understanding of how interest is calculated on a PCP. You are paying a much higher rate on that amount than the bit you are paying back. You really wont save much by putting in a bigger deposit as there is no way of reducing that chunk of interest.

Like it or not, the best and lowest cost way overall with a PCP is low deposit. Frankly, if the OP is intending ownership its the wrong finance in the firstplace.

Like i said, if you really have ownership intentions, PCP is not the correct way. It WILL cost you more. If however you wish to take the end risk out and move from car to car regularly, why not. You only amortise the final higher cost if you either stop driving or pay off the MGFV. Myself? I'd be going down the Personal Contract hire route, if my intention was a regular change. Lower deposits, lower monthlies but no flexibility (well tgere is, but you will pay for it)

On a typical 42 month PCP for every £1000 more or less, your payments change by approximately £29. Can you see why it's a bad idea to put in thousands more to reduce your payments by such a small amount-especially if that deposit is greater than 10-15% as thats money you can kiss goodbye.

HTH

silentbrown said:

TVR1 said:

Let's work backwards. The MGFV isnt just a figure plucked out of thin air. They are calculated by looking at historical trade values, depreciation from new etc. very simply put, if you purchase a car for £30k, whatever the MGFV you expect to have an equity return of around 10-15% should you p/ex the car. If you put in more than that, it's money that won't be coming back. In effect, you have paid more deposit for a short term reduction in payments.

I don't understand what you're saying here? Every PCP quote has a "Total Amount Payable". (deposit + fees + monthly payments + GFV ). The GFV doesn't depend on the deposit, but on the parameters you've said.

As you increase the deposit, the total amount payable will go DOWN not up.

Also GFV's can be "plucked out of thin air" if required. I have an 18 month PCP quote for a 46K car in front of me. The deposit is 50% and the GFV is just over £2K. This minimizes the "total amount payable" given that I plan to pay off the finance and owning the car outright after 6 months.

). You're a smart buyer who probably has a bit more financial nouse than some, simply on the basis of the amount that is available to you. And youve worked out how things work with PCP, manufacturers contributions etc. but yours is not a common case. You've worked out how to meet your required end (ownership) in a smart way.

). You're a smart buyer who probably has a bit more financial nouse than some, simply on the basis of the amount that is available to you. And youve worked out how things work with PCP, manufacturers contributions etc. but yours is not a common case. You've worked out how to meet your required end (ownership) in a smart way. Notwithstanding that and in the OP's case, unless he does what you are doing, he will be having a bum steer if he takes a PCP to achieve ownership at the end of the agreement.

silentbrown said:

Sheepshanks said:

He's saying the GFV is fixed. Therefore the interest on it is a fixed amount.

That's true. but the GFV (depending on term) is usually well under half of the amount borrowed. Here's some real examples. Golf R with 2,658 (minimum deposit)

... versus £6658 deposit. (the max that VW allows is around £7500. They don't allow more because that would reduce their profit too much!)

So an additional £4,000 deposit is cheaper by over £400 over the 3 years. Depends on your view of small beer.

I'd imagine a basic petrol Golf R would be the runt and worth 'feck all at the end. They've set the maximum contribution at 26'ish percent 'cos they don't want to deal with the FCA complaints that come in at the end

TVR1 said:

onthlies but no flexibility (well tgere is, but you will pay for it)

On a typical 42 month PCP for every £1000 more or less, your payments change by approximately £29. Can you see why it's a bad idea to put in thousands more to reduce your payments by such a small amount-especially if that deposit is greater than 10-15% as thats money you can kiss goodbye.

HTH

This sums up the conversation I had today when I picked up the car, I chatted about with my friend / the sales manager, and he agreed that it was around a £30 difference for every 1k, roughly speaking. In my case, putting down 1k on a 4.9 % deal over 3 years has lowered my payments by £30, and if you work out the difference in what I would have saved per month over 3 years not putting that down vs what I have put down, there is around a cup of tea or so difference, at this price point. Knowing that my balloon is smaller than I realised, knowing what they are likely to give me in general terms as a trade in and also knowing that my friend will always treat me with honesty and give me the best deal he can in the future all serves to reassure me that actually this was the right move. On a typical 42 month PCP for every £1000 more or less, your payments change by approximately £29. Can you see why it's a bad idea to put in thousands more to reduce your payments by such a small amount-especially if that deposit is greater than 10-15% as thats money you can kiss goodbye.

HTH

I am glad I bought this up though, for a higher value car it seems to me it is like throwing money down the drain if you do not intend to keep it post deal.

TVR1 said:

TheHound said:

TVR1 said:

In the short term, yes. The major lack of understand of how PCP agreements work and how interest is calculated on them though, is yours.

Let's work backwards. The MGFV isnt just a figure plucked out of thin air. They are calculated by looking at historical trade values, depreciation from new etc. very simply put, if you purchase a car for £30k, whatever the MGFV you expect to have an equity return of around 10-15% should you p/ex the car. If you put in more than that, it's money that won't be coming back. In effect, you have paid more deposit for a short term reduction in payments.

But then you'll tell us 'you save on interest if you put more deposit in'

In a normal HP agreement, yes but once again, a fundemental lack of understanding of how interest is calculated on a PCP. You are paying a much higher rate on that amount than the bit you are paying back. You really wont save much by putting in a bigger deposit as there is no way of reducing that chunk of interest.

Like it or not, the best and lowest cost way overall with a PCP is low deposit. Frankly, if the OP is intending ownership its the wrong finance in the firstplace.

This is all kinds of wrongLet's work backwards. The MGFV isnt just a figure plucked out of thin air. They are calculated by looking at historical trade values, depreciation from new etc. very simply put, if you purchase a car for £30k, whatever the MGFV you expect to have an equity return of around 10-15% should you p/ex the car. If you put in more than that, it's money that won't be coming back. In effect, you have paid more deposit for a short term reduction in payments.

But then you'll tell us 'you save on interest if you put more deposit in'

In a normal HP agreement, yes but once again, a fundemental lack of understanding of how interest is calculated on a PCP. You are paying a much higher rate on that amount than the bit you are paying back. You really wont save much by putting in a bigger deposit as there is no way of reducing that chunk of interest.

Like it or not, the best and lowest cost way overall with a PCP is low deposit. Frankly, if the OP is intending ownership its the wrong finance in the firstplace.

TVR1 said:

On a typical 42 month PCP for every £1000 more or less, your payments change by approximately £29. Can you see why it's a bad idea to put in thousands more to reduce your payments by such a small amount-especially if that deposit is greater than 10-15% as thats money you can kiss goodbye.

So if I "kiss goodbye" to £1000 to you, and in return you'd give me the "small amount" of £29 every month for 41 months? Where do I sign???I'm not saying goodbye to my £1000 - just "au revoir", because over the course of the 42 months I'll get it all back together with 189 of it's little friends.

Please, explain to me how this is bad. I'm not saying a PCP deposit is the best or wisest thing you can do with your £££, just that increasing the deposit saves you money over the course of the PCP. Regardless of ownership ambitions, or the GFV. If you disagree, give a worked example. I'm not aware of *any* scenario where my deposit is "lost".

TVR1 said:

In the short term, yes. The major lack of understand of how PCP agreements work and how interest is calculated on them though, is yours.

As they say in the US - you do the Math....TVR1 said:

Let's work backwards. The MGFV isnt just a figure plucked out of thin air. They are calculated by looking at historical trade values, depreciation from new etc. very simply put, if you purchase a car for £30k, whatever the MGFV you expect to have an equity return of around 10-15% should you p/ex the car. If you put in more than that, it's money that won't be coming back. In effect, you have paid more deposit for a short term reduction in payments.

But then you'll tell us 'you save on interest if you put more deposit in'

In a normal HP agreement, yes but once again, a fundemental lack of understanding of how interest is calculated on a PCP. You are paying a much higher rate on that amount than the bit you are paying back. You really wont save much by putting in a bigger deposit as there is no way of reducing that chunk of interest.

The APR is the interest rate charges on the amount borrowed, which includes the GMFV and the gap between car value, deposit and GMFV.But then you'll tell us 'you save on interest if you put more deposit in'

In a normal HP agreement, yes but once again, a fundemental lack of understanding of how interest is calculated on a PCP. You are paying a much higher rate on that amount than the bit you are paying back. You really wont save much by putting in a bigger deposit as there is no way of reducing that chunk of interest.

TVR1 said:

Like it or not, the best and lowest cost way overall with a PCP is low deposit. Frankly, if the OP is intending ownership its the wrong finance in the firstplace.

Priceless! All kinds of wrong.

Please see my example above which has real numbers and confirms my previous comments (supported by others who do clearly have done basic mathematical knowledge)...!!

Edited by sidicks on Tuesday 3rd March 21:22

Gassing Station | Finance | Top of Page | What's New | My Stuff