Morgage 1st Timer

Discussion

Hi looking for advice for my daughter who is 22 and looking for her first flat

Flat prices around £120k

Salary £18k would expect to rise fairly quickly but rather be safe than sorry and still have a social life

No debt and savings of around £10k

How sensible is shared ownership?

what sort of term would be available, is 25 years the maximum?

Are their any other goverment schemes that would help

New mortgage ISA, when will they start?

Assuming at this stage we are not adding any help although we probably will, could we secure against our house, around £300k of equity in it with around £20k left to pay

Flat prices around £120k

Salary £18k would expect to rise fairly quickly but rather be safe than sorry and still have a social life

No debt and savings of around £10k

How sensible is shared ownership?

what sort of term would be available, is 25 years the maximum?

Are their any other goverment schemes that would help

New mortgage ISA, when will they start?

Assuming at this stage we are not adding any help although we probably will, could we secure against our house, around £300k of equity in it with around £20k left to pay

Sogra said:

Hi looking for advice for my daughter who is 22 and looking for her first flat

Flat prices around £120k

Salary £18k would expect to rise fairly quickly but rather be safe than sorry and still have a social life

No debt and savings of around £10k

How sensible is shared ownership?

what sort of term would be available, is 25 years the maximum?

Are their any other goverment schemes that would help

New mortgage ISA, when will they start?

Assuming at this stage we are not adding any help although we probably will, could we secure against our house, around £300k of equity in it with around £20k left to pay

Your daughter will be limited to circa 4.5x her £18k = £81kFlat prices around £120k

Salary £18k would expect to rise fairly quickly but rather be safe than sorry and still have a social life

No debt and savings of around £10k

How sensible is shared ownership?

what sort of term would be available, is 25 years the maximum?

Are their any other goverment schemes that would help

New mortgage ISA, when will they start?

Assuming at this stage we are not adding any help although we probably will, could we secure against our house, around £300k of equity in it with around £20k left to pay

She will need a minimum 10% deposit, more if it's a new build flat.

Shared ownership sounds like it would be the way forward, unless you can bridge the deposit gap for your daughter? To do that you could release some of the equity in your property via a remortgage.

Thanks Sarnie,

we could find £10k or so with out too much trauma to help with deposit.

With shared ownership who decides on the split and how much is the rent element?

Could we do a buy to let mortgage using our equity and my daughter pay us the rent (additional mortgage), both houses would be hers anyway at some stage.

Trying Hard to retire at 55 so also need not to help too much

we could find £10k or so with out too much trauma to help with deposit.

With shared ownership who decides on the split and how much is the rent element?

Could we do a buy to let mortgage using our equity and my daughter pay us the rent (additional mortgage), both houses would be hers anyway at some stage.

Trying Hard to retire at 55 so also need not to help too much

Sogra said:

Thanks Sarnie,

we could find £10k or so with out too much trauma to help with deposit.

With shared ownership who decides on the split and how much is the rent element?

Could we do a buy to let mortgage using our equity and my daughter pay us the rent (additional mortgage), both houses would be hers anyway at some stage.

Trying Hard to retire at 55 so also need not to help too much

The Developer/Housing Association decide on what split they want to offer, you would need to google some local developments and go have a chat with them.we could find £10k or so with out too much trauma to help with deposit.

With shared ownership who decides on the split and how much is the rent element?

Could we do a buy to let mortgage using our equity and my daughter pay us the rent (additional mortgage), both houses would be hers anyway at some stage.

Trying Hard to retire at 55 so also need not to help too much

You can't take out a BTL mortgage and rent it to your daughter, you are not allowed to rent a BTL to immediate family members.

If you trust the daughter just give her the deposit and explain that you'd like her to bear in mind her moral obligation to return the gesture if/when you are in need yourself.

Why? Because after 7 years it will take the outright gift out of your Estate for Inheritance Tax purposes - assuming your total assets are likely to exceed £325k, which catches many people when the parents house is eventually sold.

Why? Because after 7 years it will take the outright gift out of your Estate for Inheritance Tax purposes - assuming your total assets are likely to exceed £325k, which catches many people when the parents house is eventually sold.

Sarnie said:

The Developer/Housing Association decide on what split they want to offer, you would need to google some local developments and go have a chat with them.

You can't take out a BTL mortgage and rent it to your daughter, you are not allowed to rent a BTL to immediate family members.

Without wishing to be a pedant.You can't take out a BTL mortgage and rent it to your daughter, you are not allowed to rent a BTL to immediate family members.

The Shared Ownership range is usually influenced by the borrower (the OP's daughter) though in order for the Housing Assoc to access government funding the minimum is typically set at 25%. At this level rent would be charged on the remaining 75%.

Mortgage lenders may also specify a minimum ownership level but again this is usually 25%.

Bizarrely some schemes do not allow 100% ownership so check this out if the intention is to gradually staircase up to 100%. Additionally, if the staircasing is being done in conjunction with a mortgage you'll find that lenders only allow it once or in sizeable 'chunks'.

As for the BTL option, you can rent a property you own with a mortgage to your daughter but you may struggle to find a mortgage lender who offers a suitable product. This is because when letting to an immediate family member the regulations are different.

Sogra said:

Hi looking for advice for my daughter who is 22 and looking for her first flat

Flat prices around £120k

Salary £18k would expect to rise fairly quickly but rather be safe than sorry and still have a social life

No debt and savings of around £10k

Even if she could get a mortgage (lets say with a bigger deposit etc) 18k salary minus tax,NI ,pension contributions then mortgage payment , council tax (at least 1k) ,service charge (probably around 1k) ,electricity & gas, telephone/broadband ,food etc and then the cost of kitting out the flat will leave her with very little disposable income if any at all (does she have any car monthly payments etc?Flat prices around £120k

Salary £18k would expect to rise fairly quickly but rather be safe than sorry and still have a social life

No debt and savings of around £10k

It seems her budget may be very tight , she's probably better off staying put and saving more and waiting for her salary to increase.

Burgmeister said:

She needs more than a 10% deposit as the affordability doesn't stack up at 90% LTV, let alone 95%.

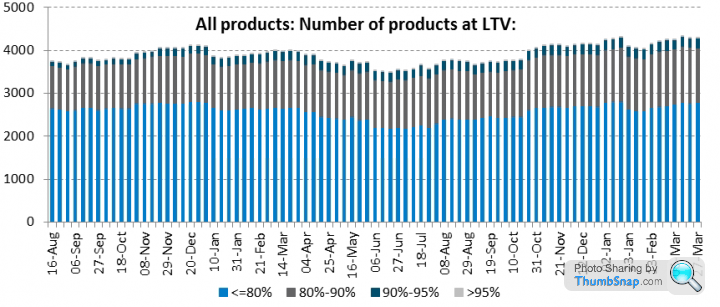

As of today, here is the number of mortgage products available by LTV:

Ah ok. Didn't consider the actual affordability of the repayment. As of today, here is the number of mortgage products available by LTV:

You had me worried there as we are shortly looking to buy our first house with only 5% !

Sarnie said:

Sogra said:

Thanks Sarnie,

we could find £10k or so with out too much trauma to help with deposit.

With shared ownership who decides on the split and how much is the rent element?

Could we do a buy to let mortgage using our equity and my daughter pay us the rent (additional mortgage), both houses would be hers anyway at some stage.

Trying Hard to retire at 55 so also need not to help too much

The Developer/Housing Association decide on what split they want to offer, you would need to google some local developments and go have a chat with them.we could find £10k or so with out too much trauma to help with deposit.

With shared ownership who decides on the split and how much is the rent element?

Could we do a buy to let mortgage using our equity and my daughter pay us the rent (additional mortgage), both houses would be hers anyway at some stage.

Trying Hard to retire at 55 so also need not to help too much

You can't take out a BTL mortgage and rent it to your daughter, you are not allowed to rent a BTL to immediate family members.

I have heard of a few horror stories of when people try to sell a shared ownership house/flat where the offer is always refused by the company who the owner is renting off, I can't recall the details on this but it was something like they always had the final say on the sale

The help to buy loan is much more straight forward and you own 100% of the home from the beginning, you can borrow up to 20% but it must be a new build. A huge deposit of 25-30% is the ideal situation but not everyone can save that kind of money

The help to buy loan is much more straight forward and you own 100% of the home from the beginning, you can borrow up to 20% but it must be a new build. A huge deposit of 25-30% is the ideal situation but not everyone can save that kind of money

Do.not.do.shared.ownership.

I could not imagine anything worse, they are literally a nightmare to sell on.... If you can at all. It is not the way forward, nowhere near. She needs to just sit tight and carry on living at home until her salary rises and she can put away more savings. She will not be able to afford the monthly repayment and the council tax plus bills etc without it dramatically effecting her life, id even go as far to say shed have zero disposable income after all bills. On a new build flat the ground rent and service charge alone would more than likely be £1k a year minimum. Just wait it out imho. Iv got 2 flats now, i lived at home and just watched the money roll in even though i was only on £19k at the time (i paid rent to my parents). £18k and £120k flat does not stack up im afraid.

I could not imagine anything worse, they are literally a nightmare to sell on.... If you can at all. It is not the way forward, nowhere near. She needs to just sit tight and carry on living at home until her salary rises and she can put away more savings. She will not be able to afford the monthly repayment and the council tax plus bills etc without it dramatically effecting her life, id even go as far to say shed have zero disposable income after all bills. On a new build flat the ground rent and service charge alone would more than likely be £1k a year minimum. Just wait it out imho. Iv got 2 flats now, i lived at home and just watched the money roll in even though i was only on £19k at the time (i paid rent to my parents). £18k and £120k flat does not stack up im afraid.

I know 2 people with shared ownership

They both seem to be different set ups but.

The girl I know was told she had to sell her house for less than the estate agent valued it as as the person / group who had part ownership was some kind of charity thing to help people get a house.and their guide lines would not allow her to make a profit from it or something to that affect.

The 2nd hav to pay some kind of rent on the bit they don't earn and fill in 2 million forms to hang a picture.

If possible I'd try to steer clear.

They both seem to be different set ups but.

The girl I know was told she had to sell her house for less than the estate agent valued it as as the person / group who had part ownership was some kind of charity thing to help people get a house.and their guide lines would not allow her to make a profit from it or something to that affect.

The 2nd hav to pay some kind of rent on the bit they don't earn and fill in 2 million forms to hang a picture.

If possible I'd try to steer clear.

The main type of shared ownership is the one where you own a % pay rent on the rest and have the ability to buy it fully in time and obviously then pay no rent.

The less common is the one where again you purchase a % (usually higher than above) but you pay no rent on the unbought portion, this can be more restrictive and is often used solely for people with local links to the community but where they are priced out.

My advice would be to avoid, other than possibly a family getting in a two bed house rather than buying outright a flat.

These schemes, like the homebuy one and the new first time buyers savings thing are all trying to make things that are unaffordable appear affordable. Perhaps they help a little but they are small subsidies so can be a leg up to some or a future burden to others.

Research things fully if you do go this route........

The less common is the one where again you purchase a % (usually higher than above) but you pay no rent on the unbought portion, this can be more restrictive and is often used solely for people with local links to the community but where they are priced out.

My advice would be to avoid, other than possibly a family getting in a two bed house rather than buying outright a flat.

These schemes, like the homebuy one and the new first time buyers savings thing are all trying to make things that are unaffordable appear affordable. Perhaps they help a little but they are small subsidies so can be a leg up to some or a future burden to others.

Research things fully if you do go this route........

Just to counter the recent negative posts about shared ownership, my first property was a housing association flat, which we bought on a shared ownership scheme for a 50% share. The rent on the remaining 50% was approx. £350 per month and this was for a two bed flat in central London, which I think is very reasonable.

We sold the flat a couple of years ago when we bought our current house, and we had no problems with selling. In fact there were loads of interested buyers available from the Housing Association waiting list, therefore we did not need to instruct an estate agent to market the property.

When we sold the flat, after having it for nearly 10 years, we made a healthy profit of £50,000, just on our 50% share, which covered the deposit on the new house.

Based on the above, I have not had any bad experiences during our shared ownership period, and I would say don't discount this as an option to buying your first property. Just make sure that you research the terms and conditions as different landlords may have different policies.

We sold the flat a couple of years ago when we bought our current house, and we had no problems with selling. In fact there were loads of interested buyers available from the Housing Association waiting list, therefore we did not need to instruct an estate agent to market the property.

When we sold the flat, after having it for nearly 10 years, we made a healthy profit of £50,000, just on our 50% share, which covered the deposit on the new house.

Based on the above, I have not had any bad experiences during our shared ownership period, and I would say don't discount this as an option to buying your first property. Just make sure that you research the terms and conditions as different landlords may have different policies.

Id guess that was mainly due to being in the housing bubble of london though. There are zero waiting lists for properties like that in sheffield/manch/liverpool etc. looks like it worked for you and made profit due to the rise of london really.

But yeah it could work in the right situations but for places like liverpool where flats are affordable i just dont see the need. Stay at home an extra year and raise the extra deposit, simple.

But yeah it could work in the right situations but for places like liverpool where flats are affordable i just dont see the need. Stay at home an extra year and raise the extra deposit, simple.

Gassing Station | Finance | Top of Page | What's New | My Stuff