BTL Tax rules post 2020 - am i on the right track?

Discussion

Hello Finance gurus. I'm in the process of trying to figure out if a new BTL is going to be worth while given the changes in tax which are coming.

I've attempted a back of a fag packet calculation below.

Does this calculation look "roughly" correct or am i on the complete wrong track here?

The assumption is that post 2020 my total earnings will push me into the higher tax band.

Would appreciate your collective views!

I've attempted a back of a fag packet calculation below.

Does this calculation look "roughly" correct or am i on the complete wrong track here?

The assumption is that post 2020 my total earnings will push me into the higher tax band.

Would appreciate your collective views!

If you want to let me have an e-mail address, I will let you have a copy of the before/after tax changes tool that I have discussed with some clients.

One point - you have correctly removed the 10% wear & tear allowance but its likely you will have other allowable repairs/renewals costs to deduct.

ETA: A negative after-tax result is not unusual once all the changes occur - I have seen worse results than the OP's which mean capital will be eroded with ongoing negative cashflow.

David

One point - you have correctly removed the 10% wear & tear allowance but its likely you will have other allowable repairs/renewals costs to deduct.

ETA: A negative after-tax result is not unusual once all the changes occur - I have seen worse results than the OP's which mean capital will be eroded with ongoing negative cashflow.

David

Edited by sumo69 on Sunday 18th October 21:25

The more I look at it the more fundamentally wrong those figures become. What worries me most isn't so much that the OP has got it wrong but that other people are jumping up and saying it's correct!

Rent 950

less Mortgage 683

less service charge 86

less agent 76

less VAT on agent 15

net cash received = 90

So in a full year 12 x 90 = 1,080 net cash received

And that's BEFORE tax!

......or have I lost the plot?

Rent 950

less Mortgage 683

less service charge 86

less agent 76

less VAT on agent 15

net cash received = 90

So in a full year 12 x 90 = 1,080 net cash received

And that's BEFORE tax!

......or have I lost the plot?

Ozzie Osmond said:

And tax relief is changing from 40% to 20%, not from 100% to 20%.

Not quite - currently 100% tax relief reducing taxable income but this is changing to 0% tax relief increasing taxable income by 100% of the interest with a 20% tax credit for the interest.So lots of basic rate taxpayers will then be higher rate, income > £50k means withdrawal of child benefit, income > £100k means withdrawal of personal allowances etc etc.

A minefield waiting to go bang!

David

Edited by sumo69 on Tuesday 20th October 01:46

sumo69 said:

A minefield waiting to go bang!

As I have suggested many times on here and despite the onward rush of participants, BTL is not the answer to every investment/savings question. Real costs are often far higher than people expect or admit. Personally I hope the reduction in tax relief will bring some common sense to bear.Not my area of expertise but there is an article about it here (with some illustrative figures):

http://www.accountingweb.co.uk/article/huge-tax-bi...

http://www.accountingweb.co.uk/article/huge-tax-bi...

Ozzie Osmond said:

The more I look at it the more fundamentally wrong those figures become. What worries me most isn't so much that the OP has got it wrong but that other people are jumping up and saying it's correct!

Rent 950

less Mortgage 683

less service charge 86

less agent 76

less VAT on agent 15

net cash received = 90

So in a full year 12 x 90 = 1,080 net cash received

And that's BEFORE tax!

......or have I lost the plot?

No, you haven't lost the plot. Just realised that i wasn't including my tax deductible items (service charge & agents fees) from my final calculation. Doh. Rent 950

less Mortgage 683

less service charge 86

less agent 76

less VAT on agent 15

net cash received = 90

So in a full year 12 x 90 = 1,080 net cash received

And that's BEFORE tax!

......or have I lost the plot?

PurpleMoonlight said:

Why is the tax assessment changing from all at 20% to all at 40%?

If you have some scope for 20% now will you not still have some come 2020?

I'm sat on the edge of the 20/40% band at the moment, so the fact that the full rental amount will be taxable will push me right over into the higher band.If you have some scope for 20% now will you not still have some come 2020?

Ozzie Osmond said:

As I have suggested many times on here and despite the onward rush of participants, BTL is not the answer to every investment/savings question. Real costs are often far higher than people expect or admit. Personally I hope the reduction in tax relief will bring some common sense to bear.

Yep, common sense. So they're changing the tax rules to put people off investing in BTL, so they prop up the disaster that is waiting to happen stock market! Or, we can pretend it's to help 'control' house prices.

F

I'm in a similar position to caymenbill but reckon I can keep below the 40% bracket. But I've invested in BTL and like CoolHands says don't want to be making a loss. I think the outcome will be different though. Landlords can't just hike the rent. That's because there's so many BTL'ers without any mortgages, who won't be effected by this, who don't need to hike their rents. Where I have properties there's very little room for movement on rent. You can't just add £100 quid per month. It's very much set that a 2 bed in that area or a 3 bed in that area is X amount rent.

If BTL'ers don't want to invest then prices will drop. Simple supply and demand dictates this. Prices will drop until those FTBers who feel like they can't afford to buy will start to buy. And prices will drop until BTL'ers can reach the figures they need to invest.

Nobody knows what house prices will do. Anyone's guess is just that. But my guess is prices will start to stall by mid summer 2016.

CoolHands said:

so landlords won't want to make a loss so won't invest. So what will people rent? As they still won't be able to afford their own property. Or LL en masse increase rent by hell of a lot to make profit. Could make things worse.

I'm in a similar position to caymenbill but reckon I can keep below the 40% bracket. But I've invested in BTL and like CoolHands says don't want to be making a loss. I think the outcome will be different though. Landlords can't just hike the rent. That's because there's so many BTL'ers without any mortgages, who won't be effected by this, who don't need to hike their rents. Where I have properties there's very little room for movement on rent. You can't just add £100 quid per month. It's very much set that a 2 bed in that area or a 3 bed in that area is X amount rent.

If BTL'ers don't want to invest then prices will drop. Simple supply and demand dictates this. Prices will drop until those FTBers who feel like they can't afford to buy will start to buy. And prices will drop until BTL'ers can reach the figures they need to invest.

Nobody knows what house prices will do. Anyone's guess is just that. But my guess is prices will start to stall by mid summer 2016.

caymanbill said:

Hello Finance gurus. I'm in the process of trying to figure out if a new BTL is going to be worth while given the changes in tax which are coming.

I've attempted a back of a fag packet calculation below.

Does this calculation look "roughly" correct or am i on the complete wrong track here?

The assumption is that post 2020 my total earnings will push me into the higher tax band.

Would appreciate your collective views!

Dont forget as Interest rates eventually rise so will your mortgage and in turn your tax bill.I've attempted a back of a fag packet calculation below.

Does this calculation look "roughly" correct or am i on the complete wrong track here?

The assumption is that post 2020 my total earnings will push me into the higher tax band.

Would appreciate your collective views!

caymanbill said:

Ozzie Osmond said:

The more I look at it the more fundamentally wrong those figures become. What worries me most isn't so much that the OP has got it wrong but that other people are jumping up and saying it's correct!

Rent 950

less Mortgage 683

less service charge 86

less agent 76

less VAT on agent 15

net cash received = 90

So in a full year 12 x 90 = 1,080 net cash received

And that's BEFORE tax!

......or have I lost the plot?

No, you haven't lost the plot. Just realised that i wasn't including my tax deductible items (service charge & agents fees) from my final calculation. Doh. Rent 950

less Mortgage 683

less service charge 86

less agent 76

less VAT on agent 15

net cash received = 90

So in a full year 12 x 90 = 1,080 net cash received

And that's BEFORE tax!

......or have I lost the plot?

Are you going to be based in the UK?

The service charge - If for a flat then that figure may go up or down you may be surcharged. - have you checked out the managements companies budgets that look after the flats? ie what reserve fund they hold, what work is planned etc, how well its looked after? (we used to look after blocks of flats as well)

Your main benefit of being a BTL owner should be the capital growth not necessarily the income.

Edited by superlightr on Tuesday 20th October 15:46

superlightr said:

Your main benefit of being a BTL owner should be the capital growth not necessarily the income.

This is the key benefit if you are borrowing a significant proportion of the money to invest - it's a geared investment.Edited by superlightr on Tuesday 20th October 15:46

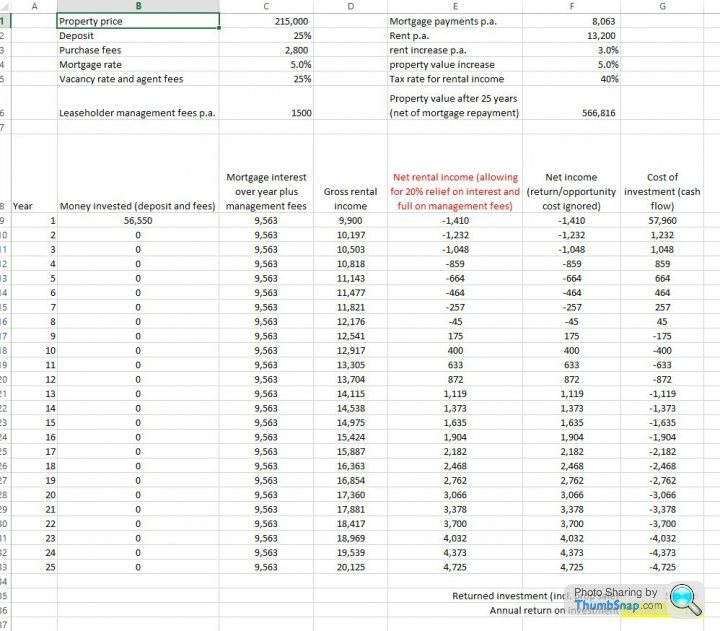

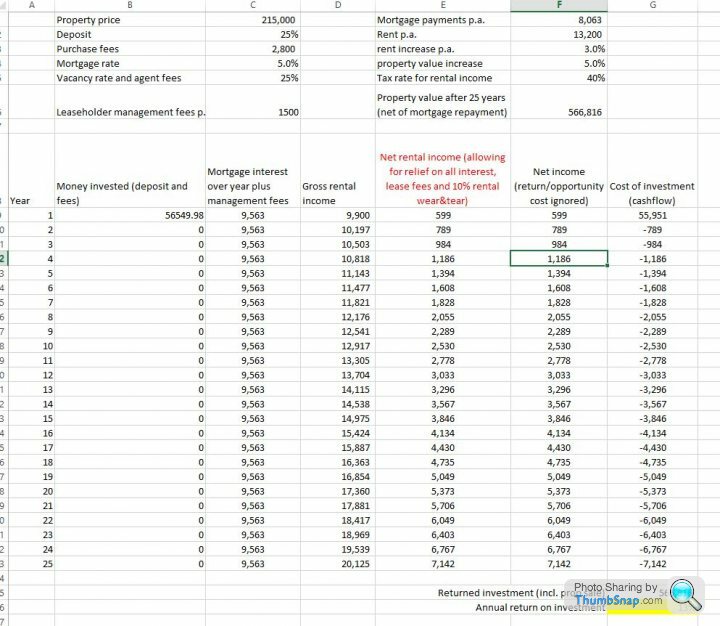

I put some figures together for a comparison of cash-flow and return under old rules and new rules, over a 25 year term. More assumptions have been made than you can shake a stick at but it illustrates that a "typical" buy-to-let flat could easily be cash-flow negative for many years under the new rules but that the bulk of the return will be from the assumed capital appreciation (CGT ignored for the comparison).

Gassing Station | Finance | Top of Page | What's New | My Stuff