House prices at an all time high.... Bad time to buy?

Discussion

bigunit00 said:

I doubt prices in places like Putney (or other blue chip postcodes in London) are going to fall anytime soon. Market may cool off a bit but nice places will always sell as demand will more than likely outstrip supply (I would probably steer clear of the new build stuff there where they want circa £1m for a 2 bed apartment). If you view as long term investment I would just buy now and get on the ladder. The £600k asset you buy now in a blue chip London postcode will probably be worth circa twice that in ten years. Trying to "time the market" is more relevant for those who are speculating over short time horizons.

http://moneyweek.com/merryns-blog/signs-that-the-london-property-market-is-cooling/Mmmmmm.....

Kensington and Chelsea prices down 14% over last year.

http://moneyweek.com/merryns-blog/buying-in-london...

The average sale price of all apartments in the SW8 postcode has fallen by about 16% to £818,000 in the last year.

But yeah, buy and ride it out. They have further to fall though....?

Tough one. I used to be very much in the house price crash camp and rented for years.

Nearly bought in 2008 as prices seemed to be going up and up.

Dodged a Bullet, was south east ireland and prices still haven't recovered.

Then rented in the UK till 2010 and bought. Paid off a chunk since then and the rent part of the mortgage - interest - is reducing all the time.

Renting is not dead money if it gives you flexibility or the rent is similar to the interest part of a mortgage so you can still save.

Look at it this way... will you get a lower interest rate anytime other than now? Interest adds a huge cost to buying a house. Prices may drop a bit but I don't see interest rayes going anywhere for a long while... offsets the risk IMO.

Nearly bought in 2008 as prices seemed to be going up and up.

Dodged a Bullet, was south east ireland and prices still haven't recovered.

Then rented in the UK till 2010 and bought. Paid off a chunk since then and the rent part of the mortgage - interest - is reducing all the time.

Renting is not dead money if it gives you flexibility or the rent is similar to the interest part of a mortgage so you can still save.

Look at it this way... will you get a lower interest rate anytime other than now? Interest adds a huge cost to buying a house. Prices may drop a bit but I don't see interest rayes going anywhere for a long while... offsets the risk IMO.

Money has never, ever, been cheaper.

There is a lack of property supply in certain key areas, subsequently many areas previously overlooked are becoming recognised and seeing huge leaps in prices. Thus we are where we are.

You cant fight the system, you just have to roll with the punches and adjust your outlook. Retrospectively the best adjustment made for the last decade has been to borrow cheap money and buy hard assets. I dont see this changing for the short to medium term.

There is a lack of property supply in certain key areas, subsequently many areas previously overlooked are becoming recognised and seeing huge leaps in prices. Thus we are where we are.

You cant fight the system, you just have to roll with the punches and adjust your outlook. Retrospectively the best adjustment made for the last decade has been to borrow cheap money and buy hard assets. I dont see this changing for the short to medium term.

It's bonkers

I bought my first property in 1995

In 2000 I sold it for x3 what I paid after a bit of wallpapering and a new dishwasher and moved a mile up the road

In 2004 we sold the new place for 'only' a 30% profit and rented for a bit

The market had plateaued but the kids were getting cheesed off not being able to put posters on their walls so we bought in early 2005

To this day I admit we paid too much money for our current gaff

Next door sold before Christmas for a lot more than we paid 11y ago so clearly I was wrong

To repeat - it's bonkers

We live in a non specific northern town

There is no way a teacher/policeman/policewoman/nurse and their family could ever afford to live in our street let alone the nice bits of town

And as for London..........

But the government still support the market with low interest rates, shared ownership and first time buyer ISA initiatives therefore the market isnt about to take a dive anytime soon

But, but, but if the above professions cant afford to live in a s

t northern town then what chance do they have in London and the SE?

t northern town then what chance do they have in London and the SE?Yes I get that London is aspirational, lovely and a magnet for money but eventually the bloke who empties the dog s

t bin in Holland Park wont be able to afford to live within a reasonable commute let alone a nurse, physio or heart surgeon and the same is broadly true of the rest of the countryHowever property is a safe thing innit?

Supply and demand etc etc etc

Behemoth said:

...the key factor longer term is lack of supply. I don't see that changing, especially in London. Why is HK so expensive? Nowhere to build. Why is London so expensive? Next to nothing being built.

Have you been to London and looked around recently? There are new high-density towers being built all over the place. Over 50,000 new apartments in build apparently. Many of these were being sold "off-plan" at shows in China, Russia etc. For a variety of reasons (some domestic/currency driven, some related to SDLT changes here) that spring is flowing less freely.I'd be careful. Certainly with new-builds in up-and-coming areas.

iantr said:

Have you been to London and looked around recently? There are new high-density towers being built all over the place. Over 50,000 new apartments in build apparently. Many of these were being sold "off-plan" at shows in China, Russia etc. For a variety of reasons (some domestic/currency driven, some related to SDLT changes here) that spring is flowing less freely.

I'd be careful. Certainly with new-builds in up-and-coming areas.

Yes, frequently. I own property in London and am well aware of the SE Asia off plan selling. One took place in a block I have long been invested in. I maintain there's nowhere near enough residential being built to satisfy demand for a city this size.I'd be careful. Certainly with new-builds in up-and-coming areas.

btw, Just as you were writing your comment, someone at the Telegraph was crafting a different opinion

http://www.telegraph.co.uk/finance/property/news/1...

Jakey123 said:

I am located in the south east (Unfortunately for myself).

Anyone have any thoughts? It seems like they are hitting a ceiling when you compare average income ( 27k ish?) to average house prices (£240k in the south east last year) they are wayyyy out of correlation. You will be maxing out on your mortgage at no more than 130k. Needing at least 50k up front to get you into a one bed flat in a questionable area.

I'm also in the South East, first-time buyer on £32k a year- I can borrow up to £150k. To stay within 10 miles of where I currently live & work, a 1-bed flat starts at around £180k in the 'average' areas.Anyone have any thoughts? It seems like they are hitting a ceiling when you compare average income ( 27k ish?) to average house prices (£240k in the south east last year) they are wayyyy out of correlation. You will be maxing out on your mortgage at no more than 130k. Needing at least 50k up front to get you into a one bed flat in a questionable area.

A family member sold their small 2-bed terrace 18 months ago for £215k, it has just sold again less than 2 years later (without even being decorated) for £275k.

My parents still live in a council house on an estate of around 150 houses, theirs is one of only a handful of properties still owned by the housing association- it's a decent sized 3-bed semi, (with a driveway that fits 3 cars and a rear garden that could fit another 2 houses) in a rural village just outside Oxford- this is a 'council house' currently worth around £330k.

They have lived their 30 years and according to the 'Right-to-buy' scheme they could buy it for less than £200k, but having always ran a small self-employed business they were never able to take a mortgage out. But it's easy to see why there are no council houses left when that kind of opportunity is available.

I'm currently saving £1,000 a month towards a deposit but the average prices are going up considerably more than that! So I'm now looking at shared ownership schemes as the only viable way of getting anywhere (I actually have a viewing tomorrow), it's not ideal but when basic 2-beds in the cheapest areas are already around £275k it's not like I have much choice.

I'm not sure what you are paying in rent at the moment, but around here the going rate for a 1-bed flat is around £900/month (before bills). The mortgage I've been offered on £150k worked out at around £550/month with the option to overpay. To me the choice between those two options is clear as day. Or at least it would be if £150k + £16.5k deposit was actually enough to buy!

So I would say get onboard as soon as you can, as unsustainable as it looks I simply can't see anything changing in the South East anytime soon. There are actually a ton of houses going up around us currently- my drive to work has become a constant battle of navigating all the contractors vehicles/building supply deliveries parked on the road for about 2 miles, but unfortunately they are all 4/5/6 bed 'mini-mansions' starting at around £800k...

Edited by Squirrelofwoe on Friday 29th January 09:55

Jakey123 said:

http://moneyweek.com/merryns-blog/signs-that-the-l...

Mmmmmm.....

Kensington and Chelsea prices down 14% over last year.

http://moneyweek.com/merryns-blog/buying-in-london...

The average sale price of all apartments in the SW8 postcode has fallen by about 16% to £818,000 in the last year.

But yeah, buy and ride it out. They have further to fall though....?

My word. I knew Money Week was lightweight but those articles you've linked to are garbage. Prices in RBKC have fallen by 14% in a year? What prices? Asking prices? Sold prices? That's a crash which as far as I'm aware no one but the author is aware of. I think you'd also find that the vast majority of owners would just hang on to their houses if a crash like this materialised. Good areas in London may fall at certain points on low sales volumes but ultimately people will just stay put. Mmmmmm.....

Kensington and Chelsea prices down 14% over last year.

http://moneyweek.com/merryns-blog/buying-in-london...

The average sale price of all apartments in the SW8 postcode has fallen by about 16% to £818,000 in the last year.

But yeah, buy and ride it out. They have further to fall though....?

As for the Nine Elms article, its conflation of far eastern property gamblers and the wider London market is laughable.

If you want to buy, like an area, can afford the house and intend to stay there for a bit, buy it and enjoy.

Edited by poocherama on Friday 29th January 10:31

Jakey123 said:

Anyone have any thoughts? It seems like they are hitting a ceiling when you compare average income ( 27k ish?) to average house prices (£240k in the south east last year) they are wayyyy out of correlation. You will be maxing out on your mortgage at no more than 130k. Needing at least 50k up front to get you into a one bed flat in a questionable area.

You're missing a massive change in society that has happened over the last 50 years. Society has changed from a typical house having a man earning the money and a woman staying at home. The typical home now has two incomes so you need to look at house prices against household income instead of individual income levels.Using your figures, a typical average household income is therefore £54k with double the tax free threshold so more like a single income of £60k. £60k with a 4 times income multiple mortgage is £240k. This is easily sustainable so there is no reason for this to cause a crash. A crash might still happen but not for this reason!

Unfortunately you have to accept that if you are hoping to buy a house as an individual, you are competing in the market against couples who have more buying power. If you want to blame anyone, blame the feminists and start arguing for a return to old fashioned ideals

The easy way to buy a house in the south east is to copy millions of others and find a partner you want to spend your life with.

Jakey123 said:

It seems like they are hitting a ceiling when you compare average income ( 27k ish?) to average house prices (£240k in the south east last year) they are wayyyy out of correlation. You will be maxing out on your mortgage at no more than 130k. Needing at least 50k up front to get you into a one bed flat in a questionable area.

I did similar sums to this back in 1999 when I was about 20/21 years old and on the hunt for my first place. At that point I was looking at a flat that was about £80k in Southampton. I was on about £22k at the time and with a deposit of about £8k going over the traditional 3:1 mortgage ratio seemed risky. As a starter home I thought that its value must be at its peak as, simply put, an averagely paid singleton would be maxxed out at the borrowing ratios so it simply couldn't have scope to go higher.

Then what happened was....

Lenders forgot about a 3:1 principle and 4:1 was easily found, then 5:1, then 6:1, then self-cert meant anything:1.

Then couples moved in to what was perhaps previously more single-person dwellings, desperate to get some foot on the ladder. A one bed flat or house that was previously the preserve of the bachelor/bachelorette became acceptable to a couple.

Others desperate to get on the ladder would then club together and buy with a friend, or a sibling, to prove for two incomes to buy a smaller place previously limited to one salary.

Parents started gifting large deposits and chipping in more regularly.

BTL'ers had access to funds and were not restricted to the same ratio.

The cursory fag packet calculation that would limit a starter home to a ratio as against a salary of what one might perceive to be the stereotypical purchaser was skewed by so many factors it was a nonsense.

Thankfully I didn't listen to my own rational at the time.

I don't know where I sit on prices at the minute, but I know attempting to link house price inflation to a typical buyer was massively unreliable.

number2 said:

I remember talking with a friend of mine back in 2001, we were both asking how on earth the price rises could continue, with property already becoming unaffordable for many. This was near the beginning of the boom...

If you find somewhere you want to live (rather than "invest") and can afford it, buy it. Factor in moves in the economy into your own affordability calculations - when/if house prices fall it's generally due to other macro factors - an economic downturn possibly, which may mean that employment is at risk. A mortgage taken at a stretch (if that's still possible) is harder to fund through savings, family help, and a pay cut.

^^^ I was going to say this.If you find somewhere you want to live (rather than "invest") and can afford it, buy it. Factor in moves in the economy into your own affordability calculations - when/if house prices fall it's generally due to other macro factors - an economic downturn possibly, which may mean that employment is at risk. A mortgage taken at a stretch (if that's still possible) is harder to fund through savings, family help, and a pay cut.

OP, If you want a home, and can afford to buy one that you like, buy it.

If you want to invest in property, perhaps consider that:

1. interest rates are more likely to rise than not, putting pressure on affordability

2. current BTL changes and government initiatives are skewing the market a bit, producing extra demand that will not be there forever

3. there are ways to invest in property with lower entry price, greater liquidity, and lower cost than just buying a flat/house

Do not accord much wisdom to what I say though, as I also bought my home in Central London in 2001, thinking that everything was overpriced, and prepared for a fall in house prices, and in the mindset that the value of my home is irrelevant. It happened in 2008, and although prices didn't go back to 2001 prices, the value remains irrelevant to me as its my home.

Might be worth a scan of the huge house prices thread http://www.pistonheads.com/gassing/topic.asp?h=0&a...

Behemoth said:

iantr said:

Have you been to London and looked around recently? There are new high-density towers being built all over the place. Over 50,000 new apartments in build apparently. Many of these were being sold "off-plan" at shows in China, Russia etc. For a variety of reasons (some domestic/currency driven, some related to SDLT changes here) that spring is flowing less freely.

I'd be careful. Certainly with new-builds in up-and-coming areas.

Yes, frequently. I own property in London and am well aware of the SE Asia off plan selling. One took place in a block I have long been invested in. I maintain there's nowhere near enough residential being built to satisfy demand for a city this size.I'd be careful. Certainly with new-builds in up-and-coming areas.

btw, Just as you were writing your comment, someone at the Telegraph was crafting a different opinion

http://www.telegraph.co.uk/finance/property/news/1...

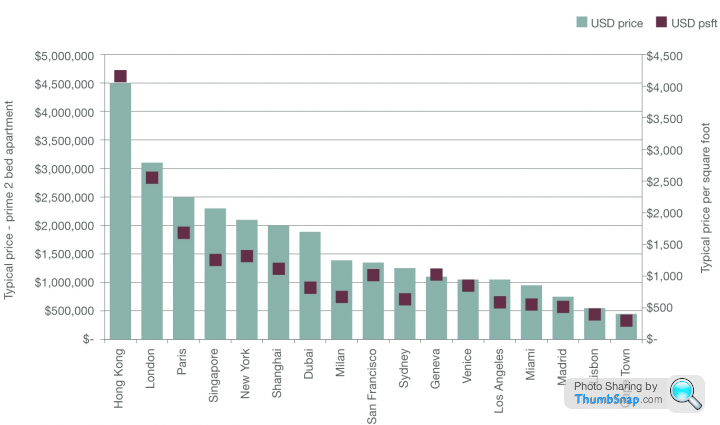

I can't. Here's an example: 794sq ft for £1.3m. http://www.rightmove.co.uk/property-for-sale/prope... That's knocking on the door of £170/sq ft, consistent with this chart from Savills last Sept. I'm not entirely convinced that this one would tick all of the boxes to be considered "Prime" either, but it does have a river view so let's say it does for the sake of discussion.

I think it is extraordinary that you can get 50% more for your money in NYC than in London. Surely the elastic is too stretched.

For the well paid London professionals who can finance property at this level, I think that there is all too great a chance of purchases ending in tears. We'll see. Let's bookmark and revisit in a few years time!

For now I am content to be on the other side of this particular trade.

Edited by iantr on Friday 29th January 16:47

More international info here to while away the hours. I suspect a Savill's pointy-shoe type carefully drew their Excel chart from this, with concentrated tongue hanging from side of mouth

http://www.globalpropertyguide.com/most-expensive-...

Off plan new build has never attracted me - a bit like new cars, they seem to drop in value just as soon as they have a first owner. I've witnessed the marketing & high pressure sales pitches. I've seen the reality. I've puked into the nearest available bag, thankful I was merely watching from the sidelines and not invested.

The only new build I'd ever do would be one I designed for myself - and that'd certainly be for love & lifelong, not for money.

http://www.globalpropertyguide.com/most-expensive-...

Off plan new build has never attracted me - a bit like new cars, they seem to drop in value just as soon as they have a first owner. I've witnessed the marketing & high pressure sales pitches. I've seen the reality. I've puked into the nearest available bag, thankful I was merely watching from the sidelines and not invested.

The only new build I'd ever do would be one I designed for myself - and that'd certainly be for love & lifelong, not for money.

https://www.gov.uk/government/uploads/system/uploa...

January report on price rises (everything, pretty much, has gone up)

Interesting reading.

January report on price rises (everything, pretty much, has gone up)

Interesting reading.

alock said:

Jakey123 said:

Anyone have any thoughts? It seems like they are hitting a ceiling when you compare average income ( 27k ish?) to average house prices (£240k in the south east last year) they are wayyyy out of correlation. You will be maxing out on your mortgage at no more than 130k. Needing at least 50k up front to get you into a one bed flat in a questionable area.

You're missing a massive change in society that has happened over the last 50 years. Society has changed from a typical house having a man earning the money and a woman staying at home. The typical home now has two incomes so you need to look at house prices against household income instead of individual income levels.Using your figures, a typical average household income is therefore £54k with double the tax free threshold so more like a single income of £60k. £60k with a 4 times income multiple mortgage is £240k. This is easily sustainable so there is no reason for this to cause a crash. A crash might still happen but not for this reason!

Unfortunately you have to accept that if you are hoping to buy a house as an individual, you are competing in the market against couples who have more buying power. If you want to blame anyone, blame the feminists and start arguing for a return to old fashioned ideals

The easy way to buy a house in the south east is to copy millions of others and find a partner you want to spend your life with.

Having said that, a reasonably big thing on the couples vs singleton front is the ability to take greater risks. Even on equivalent income, if one of couple gets the Spanish Archer, the other income keeps the wolves out, even if iphone, eating out and the like have to be reigned in, but singleton has to take account of that and some, possibly reducing potential available mortgage multiple and deposit.

Gassing Station | Finance | Top of Page | What's New | My Stuff