Stamp duty question - Main residence for landlord

Discussion

Hopefully someone will be able to offer some advice.

I lived abroad for a number of years and brought two properties in UK that are rented out. I returned to UK last summer and started looking to buy a home. One of the rental properties became vacant and so I moved in for six weeks to oversee some refurbs and then sold it in November 2015. I had been staying with parents or house sitting for an overseas friends in between this time.

I'm now in a position to buy my first "home". The sale has dragged out and now looks like it will complete post April 2016.

Does anyone know if I can count the six weeks in the buy to let as my main residence and as such paying the lower stamp duty on my first home?

Thanks in advance.

I lived abroad for a number of years and brought two properties in UK that are rented out. I returned to UK last summer and started looking to buy a home. One of the rental properties became vacant and so I moved in for six weeks to oversee some refurbs and then sold it in November 2015. I had been staying with parents or house sitting for an overseas friends in between this time.

I'm now in a position to buy my first "home". The sale has dragged out and now looks like it will complete post April 2016.

Does anyone know if I can count the six weeks in the buy to let as my main residence and as such paying the lower stamp duty on my first home?

Thanks in advance.

Not if you don't still own it. If i'm reading it correctly, you own one property now which is rented out, and your parents would be considered to be your main residence. Under the current plans for the new rules, you'll need to pay the extra 3% on each of the bands, as buying your new house will increase the number of houses you own.

They haven't 100% confirmed the final scheme details but i doubt the main components of the scheme will change.

They haven't 100% confirmed the final scheme details but i doubt the main components of the scheme will change.

I'm in exactly the same position as the OP, one house owned as a BTL, we're currently in rented (main residence), and in the middle of buying a new house to be our main residence.

Under the proposals, their aim is quite simply to say that if the transaction increases the number of properties you own, then you'll need to pay the extra 3%. The only way of avoiding it is if you're also selling your main residence, i.e. you can move from one main residence to another and not pay, but the one you're leaving must be one you own, and are selling.

This is the current proposed rules but as always with HMRC, they haven't confirmed the final details as these will be done during the next Budget before April. No solicitor that i've spoken to will confirm 100% the exact rules as they don't know either!

Otherwise all that would happen is that people would move out of their own house, into temporary rented, before buying another and I think that would be too obvious a loophole.

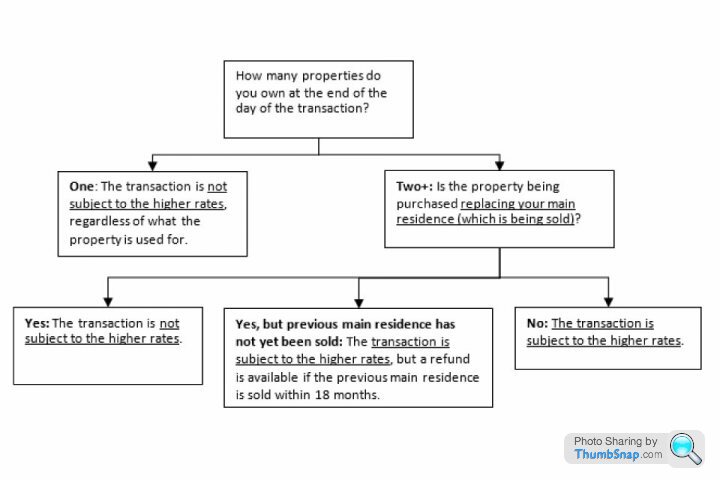

Here's HMRC's example from their consultation:

Example 9:

N purchases her first property, which she will use as a buy-to-let. At the end of the day of the transaction she owns one property, so she will not pay the higher rates of SDLT, even though she is not using it as her main residence.

Two years later, N purchases a residential property which she will use as her main residence, but she decides to keep her buy-to-let property. In this instance, as she has two properties at the end of the day of the transaction and has not replaced a main residence (as she has not sold a previous main residence), the higher rates will apply

Under the proposals, their aim is quite simply to say that if the transaction increases the number of properties you own, then you'll need to pay the extra 3%. The only way of avoiding it is if you're also selling your main residence, i.e. you can move from one main residence to another and not pay, but the one you're leaving must be one you own, and are selling.

This is the current proposed rules but as always with HMRC, they haven't confirmed the final details as these will be done during the next Budget before April. No solicitor that i've spoken to will confirm 100% the exact rules as they don't know either!

Otherwise all that would happen is that people would move out of their own house, into temporary rented, before buying another and I think that would be too obvious a loophole.

Here's HMRC's example from their consultation:

Example 9:

N purchases her first property, which she will use as a buy-to-let. At the end of the day of the transaction she owns one property, so she will not pay the higher rates of SDLT, even though she is not using it as her main residence.

Two years later, N purchases a residential property which she will use as her main residence, but she decides to keep her buy-to-let property. In this instance, as she has two properties at the end of the day of the transaction and has not replaced a main residence (as she has not sold a previous main residence), the higher rates will apply

Edited by MrChips on Sunday 7th February 10:20

Whilst the detail is awaited my understanding is that however many properties you own at the outset, if your overall game plan is to sell them ALL and replace them with ONE new house which will be your MAIN RESIDENCE then the 3% Stamp Duty surcharge does not apply. This appears to be the case even the new main residence happens to be bought before all the other sales reach completion.

I wish it wasn't the case, but unfortunately Mr Chips is right. Owning a BTL before owning a home WILL attract the higher rate. The difference in tax is significant.

I'm sure this is not the intention of the new ruling. Surely it should be excluded if the house will be your long-term home regardless of where you live prior.

I'm sure this is not the intention of the new ruling. Surely it should be excluded if the house will be your long-term home regardless of where you live prior.

I think there are still a whole set of circumstance whereby how they will apply the rules will differ even if the end result is the same.

In our example, how they take into account the "primary residence" isn't crystal clear. If they classed your BTL as your main residence (as you don't own any other houses), then selling within 18 months means you get a refund. If they classed your parents as your main residence, then even if you sell your BTL within 18 months, can you still get a refund?

The effect on the market is the same (i.e. releasing a house to market, out of your ownership), but the current plans aren't clear on what evidence you'd need to show the other house was previously your main residence.

When I move into my new place, our old house (now rented) will be remortgaged with a BTL mortgge, so will that start the 18month clock? Or will it have started from when we moved out?

We'll have to wait until the final scheme is published in March but I suspect there will be many people paying this 3% when their transaction was never the intended target (i.e. people keeping a house to rent out, or buying one to rent out).

In our example, how they take into account the "primary residence" isn't crystal clear. If they classed your BTL as your main residence (as you don't own any other houses), then selling within 18 months means you get a refund. If they classed your parents as your main residence, then even if you sell your BTL within 18 months, can you still get a refund?

The effect on the market is the same (i.e. releasing a house to market, out of your ownership), but the current plans aren't clear on what evidence you'd need to show the other house was previously your main residence.

When I move into my new place, our old house (now rented) will be remortgaged with a BTL mortgge, so will that start the 18month clock? Or will it have started from when we moved out?

We'll have to wait until the final scheme is published in March but I suspect there will be many people paying this 3% when their transaction was never the intended target (i.e. people keeping a house to rent out, or buying one to rent out).

Ozzie Osmond said:

MrChips said:

I suspect there will be many people paying this 3% when their transaction was never the intended target (i.e. people keeping a house to rent out, or buying one to rent out).

Surely that's exactly the target zone. Namely, people who choose to own more than one property."....... intended target (people keeping a house to rent out, or buying one to rent out)"

There is CGT relief for private residents, and there are exemptions to SDLT when someone is replacing their home. What confuses me is why would someone incur the higher rate just because they are not yet "home" owners. Surely buying your first home should be exempt.

I would include the higher SDLT as part of my decision when considering an additional BTL; as a business decision. However, I do not feel it should impact my costs to buying my home.

I would include the higher SDLT as part of my decision when considering an additional BTL; as a business decision. However, I do not feel it should impact my costs to buying my home.

simontrent said:

What confuses me is why would someone incur the higher rate just because they are not yet "home" owners. Surely buying your first home should be exempt.

I think the whole 3% thing is on "additional" properties, so everyone gets their first property with the lower, normal Stamp Duty whether they live in it or rent it out.The 3% kicks in when you buy a second home or buy another property to rent out.

My personal hobby-horse is that Stamp Duty actually operates as a "living in the South East tax".

[MrChips - I see what you mean. We are in agreement.]

simontrent said:

There is CGT relief for private residents, and there are exemptions to SDLT when someone is replacing their home. What confuses me is why would someone incur the higher rate just because they are not yet "home" owners. Surely buying your first home should be exempt.

I would include the higher SDLT as part of my decision when considering an additional BTL; as a business decision. However, I do not feel it should impact my costs to buying my home.

except of course they do own one private residence just choose to let it out ... I would include the higher SDLT as part of my decision when considering an additional BTL; as a business decision. However, I do not feel it should impact my costs to buying my home.

I am currently buying a new home, which may or may not complete before 1 April depending on what problems come up. The opinion of my conveyancer is that the extra SDLT won't come in this April and will be delayed 6 or 12 months. Mainly because (they are a very large firm) they are being inundated with people asking for advice on the whole shenanigans and as things stand they are unable to give it. That chart that is posted above is from a consultation document and is NOT yet tax law, hence they cannot give anyone advice at this time. Which is a completely ridiculous situation, to be less than 2 months from proposed implementation date, and not be able to fully advise on transactions that typically take 2 - 3 months to complete. So they claim that they and other conveyancing / financial advice firms are lobbying HMRC to kick it back a bit.

We will see.

I've set aside the extra SDLT anyway, if I have to pay it then the new kitchen will have to wait another year, if I don't end up paying it then we can get on with the new kitchen as soon as we move in.

We will see.

I've set aside the extra SDLT anyway, if I have to pay it then the new kitchen will have to wait another year, if I don't end up paying it then we can get on with the new kitchen as soon as we move in.

Hi Guys,

I could do with a bit of help if possible!

I've always lived with parents, and also own a few buy-to-let's. I'm not buying a new build with my partner, and I'm trying to work out if I'll be hit with the new higher rate stamp duty tax. I've spoken with two solicitors who reckon I won't be, but can't be 100% sure until the budget.

Anyone have any ideas?

Thanks!

Brad

I could do with a bit of help if possible!

I've always lived with parents, and also own a few buy-to-let's. I'm not buying a new build with my partner, and I'm trying to work out if I'll be hit with the new higher rate stamp duty tax. I've spoken with two solicitors who reckon I won't be, but can't be 100% sure until the budget.

Anyone have any ideas?

Thanks!

Brad

Bcox91 said:

Hi Guys,

I could do with a bit of help if possible!

I've always lived with parents, and also own a few buy-to-let's. I'm not buying a new build with my partner, and I'm trying to work out if I'll be hit with the new higher rate stamp duty tax. I've spoken with two solicitors who reckon I won't be, but can't be 100% sure until the budget.

Anyone have any ideas?

Thanks!

Brad

quite possibly as the end result is that you end up with a number of propertiesI could do with a bit of help if possible!

I've always lived with parents, and also own a few buy-to-let's. I'm not buying a new build with my partner, and I'm trying to work out if I'll be hit with the new higher rate stamp duty tax. I've spoken with two solicitors who reckon I won't be, but can't be 100% sure until the budget.

Anyone have any ideas?

Thanks!

Brad

mph1977 said:

Bcox91 said:

Hi Guys,

I could do with a bit of help if possible!

I've always lived with parents, and also own a few buy-to-let's. I'm not buying a new build with my partner, and I'm trying to work out if I'll be hit with the new higher rate stamp duty tax. I've spoken with two solicitors who reckon I won't be, but can't be 100% sure until the budget.

Anyone have any ideas?

Thanks!

Brad

quite possibly as the end result is that you end up with a number of propertiesI could do with a bit of help if possible!

I've always lived with parents, and also own a few buy-to-let's. I'm not buying a new build with my partner, and I'm trying to work out if I'll be hit with the new higher rate stamp duty tax. I've spoken with two solicitors who reckon I won't be, but can't be 100% sure until the budget.

Anyone have any ideas?

Thanks!

Brad

Thanks all, I know the extra tax is aimed at those investing in a 'buy to let' or a 'second home' in theory I'm doing neither, as my 'home' is currently my parents house!

I don't think I fall into the category of paying higher rate SDLT in theory, but as I do presently own other UK property (but to lets) it may apply. I'll have to see what happens in Marchs budget!

Good old George Osborne!

I don't think I fall into the category of paying higher rate SDLT in theory, but as I do presently own other UK property (but to lets) it may apply. I'll have to see what happens in Marchs budget!

Good old George Osborne!

Gassing Station | Finance | Top of Page | What's New | My Stuff