Other people's facepalm financial management

Discussion

jonah35 said:

I know a chap that bought the biggest house in london he could get as a btl a few years ago. Interest only. Hes made a good profit.

If someone had have bought a mayfair town house in 1875 on an interest only mortgage as a btl would that be a bad thing? Yes, you may still owe the fifty quid mortgage but his familynwould be laughing.

I was offered a flat in Islington by a customer in the early 1990s. I couldn't afford it as I was saving for my first house up here If someone had have bought a mayfair town house in 1875 on an interest only mortgage as a btl would that be a bad thing? Yes, you may still owe the fifty quid mortgage but his familynwould be laughing.

My 6 year old daughter has more in her pension than the bloke I'm sat next to at work (Ok so he will get some sort of state pension based on his NI payments and hes only recently had to opt in to the work pension). I pay 5% and get 10% from the company. Its free money and that's before you look at the money back on my SIPP contributions for both me and my children.

He did make some payments but then decided he wanted the extra in his pay packet. He couldn't work out why when he stopped paying he didnt see it reflected exactly the same amount in his paypacket. We spent days trying to explain that he now gets taxed on it when its in his wages, he still didnt get it after using the massive whiteboard and a projector to make my point. Potential on Compound interest on those savings blew his mind. We got up to some pretty big figures over 30 years with 3% returns per year on what he was putting into his pension but its all "now now now". It really frustrates me that people can be so ignorant. What winds me up is no doubt we will end up assisting people like this as they enter old ago wit us.

People think the future will look after itself and many people think they'll just have to work until they die. As I get older the future comes around too quick and I wish I saved more. Its a happy medium of living and enjoying life but also saving for the future. You only have to look at all these programs on Channel 4 and 5 recently showing the states some people live, we are heading for a massive issue.

My Mum works as home help and cares for disabled people and retired people. She visits people at 9am that pay for her help because of their savings and pensions and then at 11am she will visit someone who has no savings or pension and gets the help for free. The care she provides is exactly the same. Its difficult to know what to do but I think its better to plan for your future than not.

He did make some payments but then decided he wanted the extra in his pay packet. He couldn't work out why when he stopped paying he didnt see it reflected exactly the same amount in his paypacket. We spent days trying to explain that he now gets taxed on it when its in his wages, he still didnt get it after using the massive whiteboard and a projector to make my point. Potential on Compound interest on those savings blew his mind. We got up to some pretty big figures over 30 years with 3% returns per year on what he was putting into his pension but its all "now now now". It really frustrates me that people can be so ignorant. What winds me up is no doubt we will end up assisting people like this as they enter old ago wit us.

People think the future will look after itself and many people think they'll just have to work until they die. As I get older the future comes around too quick and I wish I saved more. Its a happy medium of living and enjoying life but also saving for the future. You only have to look at all these programs on Channel 4 and 5 recently showing the states some people live, we are heading for a massive issue.

My Mum works as home help and cares for disabled people and retired people. She visits people at 9am that pay for her help because of their savings and pensions and then at 11am she will visit someone who has no savings or pension and gets the help for free. The care she provides is exactly the same. Its difficult to know what to do but I think its better to plan for your future than not.

Edited by oldaudi on Friday 20th May 16:45

Jockman said:

Were they female?

Were they female?paolow said:

Jockman said:

Were they female?Not so long ago female police officers were the most expensive pension cost of all public workers.

Jockman said:

Is Employee contribution level 15% ? Crikey that's a fair bit.

Not so long ago female police officers were the most expensive pension cost of all public workers.

Contributions are from 12.4% to 13.8% (obviously from gross salary, so net cost is lower)Not so long ago female police officers were the most expensive pension cost of all public workers.

Benefits are more like 40-50%...

Edited by sidicks on Friday 20th May 16:56

sidicks said:

Jockman said:

Is Employee contribution level 15% ? Crikey that's a fair bit.

Not so long ago female police officers were the most expensive pension cost of all public workers.

Contributions are from 12.4% to 13.8% (obviously from gross salary, so net cost is lower)Not so long ago female police officers were the most expensive pension cost of all public workers.

Benefits are more like 40-50%...

Edited by sidicks on Friday 20th May 16:56

Ilovejapcrap said:

Couple of questions from me.

I'm in a pension with work but if I'm honest don't really take it that seriously.

My reasoning is I suspect the age I can get it by time I'm ready will be around 70 and I doubt I'll be around much longer than that.

I'm only really in it as death in service could be handy for anyone left behind.

I know it seems an odd thing to say but I just kinda don't think I will see it. Also is it not possible to find one day someone's f ked up and you may not even have a pension ?

ked up and you may not even have a pension ?

It's just a lot of talk on this subject seems pension braised like it's solid and fool proof but I've always thought it not.

Please anyone comment on this it really is a subject as you can tell from my views I don't fully understand or know about.

Thanks

Do take your work scheme seriously and find out all you can about it. If you don't then you will almost certainly regret it later in life. I'm in a pension with work but if I'm honest don't really take it that seriously.

My reasoning is I suspect the age I can get it by time I'm ready will be around 70 and I doubt I'll be around much longer than that.

I'm only really in it as death in service could be handy for anyone left behind.

I know it seems an odd thing to say but I just kinda don't think I will see it. Also is it not possible to find one day someone's f

ked up and you may not even have a pension ?It's just a lot of talk on this subject seems pension braised like it's solid and fool proof but I've always thought it not.

Please anyone comment on this it really is a subject as you can tell from my views I don't fully understand or know about.

Thanks

Find out about the benefits, the opportunities, the risks and the alternatives.

So many people I know throw away free money due to ignorance.

Ilovejapcrap said:

Couple of questions from me.

I'm in a pension with work but if I'm honest don't really take it that seriously.

My reasoning is I suspect the age I can get it by time I'm ready will be around 70 and I doubt I'll be around much longer than that.

I'm only really in it as death in service could be handy for anyone left behind.

I know it seems an odd thing to say but I just kinda don't think I will see it. Also is it not possible to find one day someone's fked up and you may not even have a pension ?

It's just a lot of talk on this subject seems pension braised like it's solid and fool proof but I've always thought it not.

Please anyone comment on this it really is a subject as you can tell from my views I don't fully understand or know about.

Thanks

If you are a 40% tax payer it's a good option because you don't pay tax on your contributions, you pay the tax when you draw your pension, but after you have retired it is unlikely that your income will remain high enough for you to stay as a 40% tax payer, so you will end up paying 20% tax (or even 0% percent if your total income after retirement is under £11,000 annually). I'm in a pension with work but if I'm honest don't really take it that seriously.

My reasoning is I suspect the age I can get it by time I'm ready will be around 70 and I doubt I'll be around much longer than that.

I'm only really in it as death in service could be handy for anyone left behind.

I know it seems an odd thing to say but I just kinda don't think I will see it. Also is it not possible to find one day someone's f

ked up and you may not even have a pension ?It's just a lot of talk on this subject seems pension braised like it's solid and fool proof but I've always thought it not.

Please anyone comment on this it really is a subject as you can tell from my views I don't fully understand or know about.

Thanks

This + if you work for a company that is also going to put in 5% or whatever, then it really does add up to quite a decent amount.

Upon retirement you can take 25% of your money out your pension as a tax free lump sum!

It's still worth it if you are a 20% tax payer because you get the benefit of the employers contribution + the 25% tax free lump sum + you still get up to £11,000 annual income taxed at 0%.

For me, if I take the 25% tax free sum and work until I am 67, based on the forecast value of the pot I will have to live about two years and four months after retirement in order to see a profit over just putting the money in a bank account instead of a pension. Of course, the flip side of the coin is that money could have been put to use paying the mortgage or investing in something else.

This pension calculator is quite a useful tool:

https://www.hl.co.uk/pensions/interactive-calculat...

Ilovejapcrap said:

Also is it not possible to find one day someone's fked up and you may not even have a pension ?

I don't entirely understand this either. You hear a lot about this sort of thing on the news, when a big company goes under like BHS recently. I think this is something to do with large companies that manage their own pension pots rather than paying it into a proper pension company (provider, I think might be the right term?). BHS did not put enough money into the pot!ked up and you may not even have a pension ?I think if your employer is paying all the contributions into a proper provider then you won't have this problem. My employer uses Hargreaves Lansdown.

Any pensions people here who can confirm this is correct please?

Edited by AlexC1981 on Sunday 22 May 09:59

Ozzie Osmond said:

Two concepts,

1. Free money from your employer, and

2. Free money from the government.

Which of those is a problem?

OzOs

It's not free money from the government. It's YOUR money that YOU have earned and are deferring tax on until later in life.1. Free money from your employer, and

2. Free money from the government.

Which of those is a problem?

OzOs

Which to me makes it an even easier choice.

Know of a couple who, every time we meet, tell the wife and I about their continuing financial genius.

10 years ago bought a house at the top of the market in the area that they then spent £100k and 4 years doing up. So bad that their first family Christmas at home in it was 2011. Boasted they got a 10 year fixed interest only mortgage at 5.2%.

Then a couple of years ago told us that we must put our money into Premimim Bonds and that they've got the maximum. They tell us all the £25,£50 wins they get on their (I think) £80k in the bonds; no other savings to speak of as there is nothing better than PBs.

Then they just paid to break out of their fixed rate mortgage in 2015. Got a fixed rate IO again for 10 years at 3.3%.

Repeat: Keep on telling us to get Premium Bonds.

They rely / ponce on parents to take them and their kids on holiday. And they tell us about this bit of financial wizardry as well. Every has parents that take them on holiday don't they?

Then parents give them money - think £5k/£10k chunks when they feel like it.

Number of times they've asked us what we do with our money is zero. They've no idea what we do. Just tell us about their ongoing genius.

The shame is that the other couple we go out with usually (it's the wife's friends) aren't that well off and also have to listen to the cobblers they spout.

Going out with these financial geniuses is a gift that keeps on giving.

10 years ago bought a house at the top of the market in the area that they then spent £100k and 4 years doing up. So bad that their first family Christmas at home in it was 2011. Boasted they got a 10 year fixed interest only mortgage at 5.2%.

Then a couple of years ago told us that we must put our money into Premimim Bonds and that they've got the maximum. They tell us all the £25,£50 wins they get on their (I think) £80k in the bonds; no other savings to speak of as there is nothing better than PBs.

Then they just paid to break out of their fixed rate mortgage in 2015. Got a fixed rate IO again for 10 years at 3.3%.

Repeat: Keep on telling us to get Premium Bonds.

They rely / ponce on parents to take them and their kids on holiday. And they tell us about this bit of financial wizardry as well. Every has parents that take them on holiday don't they?

Then parents give them money - think £5k/£10k chunks when they feel like it.

Number of times they've asked us what we do with our money is zero. They've no idea what we do. Just tell us about their ongoing genius.

The shame is that the other couple we go out with usually (it's the wife's friends) aren't that well off and also have to listen to the cobblers they spout.

Going out with these financial geniuses is a gift that keeps on giving.

LeoSayer said:

Well said.

Tax reliefs aren't a handout from the government.

I agree 100%, but you may be surprised that the treasury doesn't. In meetings that I had with them a couple of years ago they returned constantly to the refrain that the state "spends £Xbn on tax relief for pension contributions" and that "YY% of this goes straight into the pockets of higher rate taxpayers; a subsidy for the wealthy that is no longer acceptable and cannot continue".Tax reliefs aren't a handout from the government.

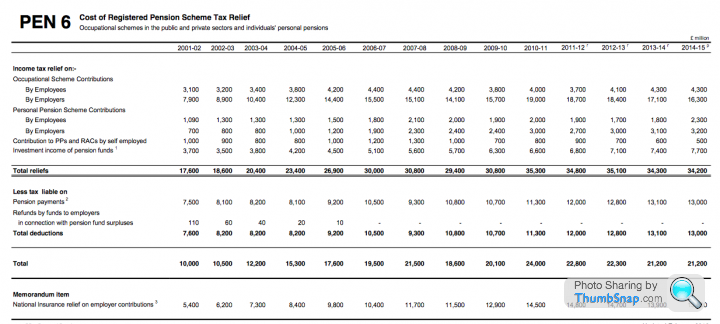

Note the tell-tale language in this table from the ONS:

The state has a different view on whose money it is in the first place!

Edited by iantr on Monday 23 May 16:50

iantr said:

I agree 100%, but you may be surprised that the treasury doesn't. In meetings that I had with them a couple of years ago they returned constantly to the refrain that the state "spends £Xbn on tax relief for pension contributions" and that "YY% of this goes straight into the pockets of higher rate taxpayers; a subsidy for the wealthy that is no longer acceptable and cannot continue".

In fairness the money comes in (as you pay your taxes) and then goes out again (as rebates), so it is an income and expenditure for them.And it does mostly go to higher rate payers!

Gassing Station | Finance | Top of Page | What's New | My Stuff