where to put 80k?

Discussion

Luke. said:

soad said:

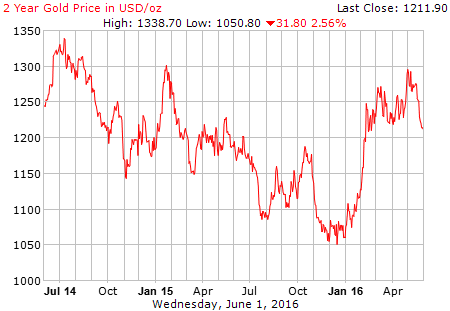

Buy gold. I sold mine a decade ago, prices have trebled now.

Now this tickles my fancy. Know nothing about gold. Good time to buy?

A limiting factor in things like 123 accounts is you need 2 direct debits on each, but you can have an account each and a joint one so that's £60k is you've got enough DDs and another account to shuffle money through so you meet the required monthly deposits (you can't pay it in from another santander account)

RizzoTheRat said:

Luke. said:

soad said:

Buy gold. I sold mine a decade ago, prices have trebled now.

Now this tickles my fancy. Know nothing about gold. Good time to buy? A limiting factor in things like 123 accounts is you need 2 direct debits on each, but you can have an account each and a joint one so that's £60k is you've got enough DDs and another account to shuffle money through so you meet the required monthly deposits (you can't pay it in from another santander account)

It still counts.

Storing large amounts of cash in a bank is pointless now that we have such low interest rates. This is why property and classic car prices have gone up so much, there is nowhere else worth putting your money.

The best instant access accounts I found were to put £20K in a Santander 123 account paying 3% and the rest of my money is in a Virgin Money account paying 1.31%. You can get 1.45% from the RCI bank but this is owned by Renault and backed by the French Government. All UK accounts are guaranteed for £75K by the government if the bank goes under. If RCI bank goes under you will be going cap in hand to the French Government for your money, so good luck with that one.

My advice would be to buy property with it.

The best instant access accounts I found were to put £20K in a Santander 123 account paying 3% and the rest of my money is in a Virgin Money account paying 1.31%. You can get 1.45% from the RCI bank but this is owned by Renault and backed by the French Government. All UK accounts are guaranteed for £75K by the government if the bank goes under. If RCI bank goes under you will be going cap in hand to the French Government for your money, so good luck with that one.

My advice would be to buy property with it.

Vocal Minority said:

jshell said:

Except there's more than 80 of them for sale on PH alone...apart from that, great punt!

As long as there is 100 guys looking to buy though...If they were such a good punt or investment at these prices there'd never be 80 for sale! Not in a million years.

Vocal Minority said:

jshell said:

Except there's more than 80 of them for sale on PH alone...apart from that, great punt!

As long as there is 100 guys looking to buy though...I have been contacted privately on two occasions by people looking to buy a good example and am quite confident that I could easily sell it for twice what I paid for it four years ago!

Of course, the bottom could fall out of the market just as quickly, but I'm not in it for the investment as it's a keeper.

Garvin said:

Vocal Minority said:

jshell said:

Except there's more than 80 of them for sale on PH alone...apart from that, great punt!

As long as there is 100 guys looking to buy though...I have been contacted privately on two occasions by people looking to buy a good example and am quite confident that I could easily sell it for twice what I paid for it four years ago!

Of course, the bottom could fall out of the market just as quickly, but I'm not in it for the investment as it's a keeper.

h0b0 said:

The other benefit of P2P investments for me is that I can be in charge of the investment myself. Due to my wife's job in finance we are very restricted in what we can do and who manages the money. I just sold a small amount of stock and she received and email saying that if we do that again she will be fired!

For me there is a "cooling off" period for any purchases and sales of stock. This cooling off period equates to "missing the boat" period or even worse "watching my money go down the drain while others jump" period. It can be up to 6 months on an investment so any investing I do is already mid term and restricted.

Insider trading? For me there is a "cooling off" period for any purchases and sales of stock. This cooling off period equates to "missing the boat" period or even worse "watching my money go down the drain while others jump" period. It can be up to 6 months on an investment so any investing I do is already mid term and restricted.

I can't think of any other reason why your wife would be fired for her husband selling privately owned stock?

jshell said:

Garvin said:

Vocal Minority said:

jshell said:

Except there's more than 80 of them for sale on PH alone...apart from that, great punt!

As long as there is 100 guys looking to buy though...I have been contacted privately on two occasions by people looking to buy a good example and am quite confident that I could easily sell it for twice what I paid for it four years ago!

Of course, the bottom could fall out of the market just as quickly, but I'm not in it for the investment as it's a keeper.

menguin said:

h0b0 said:

The other benefit of P2P investments for me is that I can be in charge of the investment myself. Due to my wife's job in finance we are very restricted in what we can do and who manages the money. I just sold a small amount of stock and she received and email saying that if we do that again she will be fired!

For me there is a "cooling off" period for any purchases and sales of stock. This cooling off period equates to "missing the boat" period or even worse "watching my money go down the drain while others jump" period. It can be up to 6 months on an investment so any investing I do is already mid term and restricted.

Insider trading? For me there is a "cooling off" period for any purchases and sales of stock. This cooling off period equates to "missing the boat" period or even worse "watching my money go down the drain while others jump" period. It can be up to 6 months on an investment so any investing I do is already mid term and restricted.

I can't think of any other reason why your wife would be fired for her husband selling privately owned stock?

(Not that you should - it's terribly boring!)

If his wife worked for an investment fund that had also invested in the stock in question, he could be accused of front-running the fund. His wife has a fiduciary duty to maximise her investors' returns and having the husband get a sell order in first is the exact opposite of that!!

Most likely the company just has hugely restrictive PA trading rules in order to appear whiter-than-white while adhering to all the various rules from multiple regulators.

Generally it ends up easier just to stick everything in an ETF and forget about it rather than trade individual stocks if you still want equity exposure, IMHO.

Joey Deacon said:

The best instant access accounts I found were to put £20K in a Santander 123 account paying 3% and the rest of my money is in a Virgin Money account paying 1.31%. You can get 1.45% from the RCI bank but this is owned by Renault and backed by the French Government. All UK accounts are guaranteed for £75K by the government if the bank goes under. If RCI bank goes under you will be going cap in hand to the French Government for your money, so good luck with that one.

all Euro banks operate the same scheme - why would claiming on the French version be worse than claiming from the UK FSCS?https://www.rcibank.co.uk/security/guarantee-schem...

walm said:

That's probably because you don't know anything about FCA/SEC regulation combined with in-house personal account trading rules.

(Not that you should - it's terribly boring!)

If his wife worked for an investment fund that had also invested in the stock in question, he could be accused of front-running the fund. His wife has a fiduciary duty to maximise her investors' returns and having the husband get a sell order in first is the exact opposite of that!!

Most likely the company just has hugely restrictive PA trading rules in order to appear whiter-than-white while adhering to all the various rules from multiple regulators.

Generally it ends up easier just to stick everything in an ETF and forget about it rather than trade individual stocks if you still want equity exposure, IMHO.

Indeed - I am completely ignorant about that particular field of regulation - my day job involves enough in my sector to put me to sleep (Not that you should - it's terribly boring!)

If his wife worked for an investment fund that had also invested in the stock in question, he could be accused of front-running the fund. His wife has a fiduciary duty to maximise her investors' returns and having the husband get a sell order in first is the exact opposite of that!!

Most likely the company just has hugely restrictive PA trading rules in order to appear whiter-than-white while adhering to all the various rules from multiple regulators.

Generally it ends up easier just to stick everything in an ETF and forget about it rather than trade individual stocks if you still want equity exposure, IMHO.

Thanks for explaining though, makes sense.

May be in a similar position shortly, thought about investing in a car. Scrapped that though, nowhere to store it.

Soooo large deposit on another property to do-up and sell? Difficult to put hours in with a full-time job although the other half is better at DIY than me and works part time.

Perhaps premium bonds, low risk and non-existent effort but 70+k is a lot to put into them and return is tiny compared to what could be made on a house.

Bugger me. No idea.

Soooo large deposit on another property to do-up and sell? Difficult to put hours in with a full-time job although the other half is better at DIY than me and works part time.

Perhaps premium bonds, low risk and non-existent effort but 70+k is a lot to put into them and return is tiny compared to what could be made on a house.

Bugger me. No idea.

Speed_Demon said:

May be in a similar position shortly, thought about investing in a car. Scrapped that though, nowhere to store it.

Soooo large deposit on another property to do-up and sell? Difficult to put hours in with a full-time job although the other half is better at DIY than me and works part time.

Perhaps premium bonds, low risk and non-existent effort but 70+k is a lot to put into them and return is tiny compared to what could be made on a house.

Bugger me. No idea.

Yep. I absolutely hate DIY. Though I did learn a lot on the old house. That's the only thing putting me off another property. That and the fact that prices are so high at the moment that if they fall we stand to lose and not gain.Soooo large deposit on another property to do-up and sell? Difficult to put hours in with a full-time job although the other half is better at DIY than me and works part time.

Perhaps premium bonds, low risk and non-existent effort but 70+k is a lot to put into them and return is tiny compared to what could be made on a house.

Bugger me. No idea.

JoeMarano said:

Yep. I absolutely hate DIY. Though I did learn a lot on the old house. That's the only thing putting me off another property. That and the fact that prices are so high at the moment that if they fall we stand to lose and not gain.

So where are you living now, in a tent? The back of an old Transit?

Gassing Station | Finance | Top of Page | What's New | My Stuff