Stamp duty - BTL but with a difference

Discussion

Hi

my partner moved in a few years back and has been renting her existing property out for this time.

I own this house and her name is not yet on the deed.

We are looking to remortgage her property and add my name to the deeds and eventually hers to this.

Are we liable to the new 2nd home stamp duty? I know it may seem like a silly question but where I see this as exempt as it isn't a new purchase, it is just adding someone else to the deeds, does the filthy Gideon see it the same way?

Thanks

my partner moved in a few years back and has been renting her existing property out for this time.

I own this house and her name is not yet on the deed.

We are looking to remortgage her property and add my name to the deeds and eventually hers to this.

Are we liable to the new 2nd home stamp duty? I know it may seem like a silly question but where I see this as exempt as it isn't a new purchase, it is just adding someone else to the deeds, does the filthy Gideon see it the same way?

Thanks

PH XKR said:

Hi

Are we liable to the new 2nd home stamp duty?

You will pay the extra 3% Stamp Duty if the transaction is liable to Stamp Duty in the normal course of events. Transfers of property may be subject to Stamp Duty.Are we liable to the new 2nd home stamp duty?

Being married sometimes makes a difference

https://www.gov.uk/guidance/sdlt-transferring-owne...

Our situation is as follows - House was in wifes name (she bought it before we got married) then moved abroad together 4 yrs ago. Whilst overseas we put the house in my name (re-mortgaged on residential with consent to let).

we'd like to keep this house as rental for future etc value 150-160k 75k on mortgage remaining, rents easily for 650 (could charge more but have good long-term tenants).

We are also looking for a larger family house - which I believe will attract the additional 3% stamp duty which is a not insignificant sum on property in 750 to 900k range.

Question is does the below mean we can avoid the additional 3%

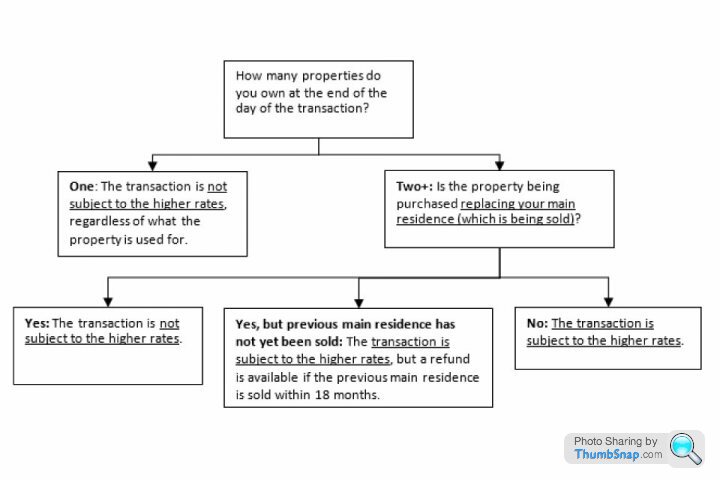

"Replacing a main residence

In most cases someone already owning a buy to let property, who wishes to move house, should not be liable for the higher SDLT rate. This is because there is no retrospective tax to pay on the existing buy to let property, and the owner plans to replace their main residence."

https://www.stampdutycalculator.org.uk/stamp-duty-...

we'd like to keep this house as rental for future etc value 150-160k 75k on mortgage remaining, rents easily for 650 (could charge more but have good long-term tenants).

We are also looking for a larger family house - which I believe will attract the additional 3% stamp duty which is a not insignificant sum on property in 750 to 900k range.

Question is does the below mean we can avoid the additional 3%

"Replacing a main residence

In most cases someone already owning a buy to let property, who wishes to move house, should not be liable for the higher SDLT rate. This is because there is no retrospective tax to pay on the existing buy to let property, and the owner plans to replace their main residence."

https://www.stampdutycalculator.org.uk/stamp-duty-...

Mezger said:

abroad together 4 yrs ago. Whilst overseas we put the house in my name (re-mortgaged on residential with consent to let).

So it's not your main residence, is it?Mezger said:

we'd like to keep this house as rental for future

Clearly not your main residence.Mezger said:

"In most cases someone already owning a buy to let property, who wishes to move house, should not be liable for the higher SDLT rate. This is because there is no retrospective tax to pay on the existing buy to let property, and the owner plans to replace their main residence."

But if you don't own an existing main residence you can't "replace" it so will be hit by the +3%Put simply you are very unlikely to get a definitive answer on an internet forum. You need a solicitor to look at where you have lived and when in UK, where you have lived and when abroad, how long the UK house has been owned etc etc.

I suspect the +3% Stamp Duty may be only one of your tax issues. That UK house will fall within the Capital Gains Tax regime if it's been rented out. And depending on your overall UK tax situation filing a CGT return might make Mr HMRC wonder whether the rent has been declared for tax.

IMO you need a paid professional to look at the whole situation.

Ozzie Osmond said:

Mezger said:

"In most cases someone already owning a buy to let property, who wishes to move house, should not be liable for the higher SDLT rate. This is because there is no retrospective tax to pay on the existing buy to let property, and the owner plans to replace their main residence."

But if you don't own an existing main residence you can't "replace" it so will be hit by the +3%Gassing Station | Finance | Top of Page | What's New | My Stuff