So why is the FTSE 100 nearly at a 52w high?

Discussion

avinalarf said:

So they are prepared to sacrifice the income of the retiree to keep unemployment at bay.

Yes, but you're 8 years late to be making that particular point.As I have said many times these policies have destroyed the value of money (not its spending power, its real worth as something to hold) and IMO there's a real risk that confidence in money will eventually be undermined as well. Miraculously inflation has remained low to date as a result of immigrant workers suppressing wage inflation - but UK has recently voted, apparently, to suppress immigration so all that may change. Obviously our friends in Greece and elsewhere are doing their best to accelerate the process of destroying money.

walm said:

That obviously true if you have 100% of your assets in the exact bond you want which provides the income you need.

Most don't, do they?

Let's keep it simple - anyone hoarding cash is worse off.

Anyone wanting to lower their risk on retirement is worse off.

Or let's take a real world example.

If you had everything in investment grade bonds, the index is up from 189 to 203 over the last year.

So a 7.4% rise.

http://finra-markets.morningstar.com/MarketData/De...

But the annuity rate you can get (on £100k at 65) has dropped from around £5,800 per annum to £4,915.

That's a 15% drop.

http://www.sharingpensions.co.uk/annuity-rates-cha...

So the rise has NOT offset the drop.

Again, sure if you were in super risky assets right up to retirement then YES you might be fine!

No, the low risk assets (to hedge the cost of an annuity) in the run up to retirement are long-dated government bonds. See how these fared in the same period...Most don't, do they?

Let's keep it simple - anyone hoarding cash is worse off.

Anyone wanting to lower their risk on retirement is worse off.

Or let's take a real world example.

If you had everything in investment grade bonds, the index is up from 189 to 203 over the last year.

So a 7.4% rise.

http://finra-markets.morningstar.com/MarketData/De...

But the annuity rate you can get (on £100k at 65) has dropped from around £5,800 per annum to £4,915.

That's a 15% drop.

http://www.sharingpensions.co.uk/annuity-rates-cha...

So the rise has NOT offset the drop.

Again, sure if you were in super risky assets right up to retirement then YES you might be fine!

bad company said:

walm said:

people who are close to retirement don't tend to have huge equity exposure so will have missed much of the rally.

Really? Surely those close to retirement would chose equity funds and/or bonds to maximize income.That's what I did.

- Greatly increased life expectancy

- Low bond yields

- Risk of future inflation

- Availability of SIPP drawdown.

Ozzie Osmond said:

I find this interesting because it seems to me that "switching to bonds as retirement approaches" is perhaps outdated. In fact, quite possibly a very bad strategy. Why?

Risk of low bond yields and future inflation is precisely why you move into long-dated inflation-linked government bond assets as you approach retirement, hence providing protection against the sort of moves seen post Brexit, as discussed in this thread!- Greatly increased life expectancy

- Low bond yields

- Risk of future inflation

- Availability of SIPP drawdown.

sidicks said:

Risk of low bond yields and future inflation is precisely why you move into long-dated inflation-linked government bond assets as you approach retirement, hence providing protection against the sort of moves seen post Brexit, as discussed in this thread!

Do people really need protection against a 15% rise in equity markets? Not me!And if stock markets fall they have always recovered over the next few years, so as long as you don't sell in a panic at the bottom there isn't a problem.

One of my bug-bears is that the UK corporate pensions industry has been destroyed by, amongst other things, the flight from equity risk.

Ozzie Osmond said:

Do people really need protection against a 15% rise in equity markets? Not me!

And if stock markets fall they have always recovered over the next few years, so as long as you don't sell in a panic at the bottom there isn't a problem.

Protection against bond yields. And if stock markets fall they have always recovered over the next few years, so as long as you don't sell in a panic at the bottom there isn't a problem.

Ozzie Osmond said:

One of my bug-bears is that the UK corporate pensions industry has been destroyed by, amongst other things, the flight from equity risk.

Hedging fixed / inflation linked liabilities with equities can lead to massive deficits...Ginge R said:

the dampened volatility is worth a premium in its own right.

If that is correct, how is the dampened volatility valued? It seems to me that like all insurance it has a cost and to me that cost doesn't look worth incurring with a twenty to thirty year time horizon.Any way, if and when interest rates rise won't bond prices collapse? Aha you reply, but they're index-linked so it doesn't matter. But buying them now looks mighty expensive to me compared with the risk of running equities.

sidicks said:

Hedging fixed / inflation linked liabilities with equities can lead to massive deficits...

Yes, but so what? Unless and until the deficit crystallises the deficit is just numbers on a piece of paper. What I find unrealistic is the "assumption" that if the market falls it will never recover - whereas history to date has shown that when the market falls it always recovers.Put simply, it appears to me that the price of "safety" is too high to be worth paying. This is presumably why corporate DB pensions have ceased to exist - it's not worth the huge cost of making a future pension promise backed by index-linked bonds. Meanwhile private investors are being encouraged to take on exactly the risks that corporates are running away from, and the government doesn't bother to face the risk at all. It's all very strange.

Yes, I can see that if a private individual is 55 with a huge "pot" it can theoretically make sense to start de-risking. But if the pot is huge, do they need to de-risk at all? Why not stay in the game for even more growth.

If the pot is small at age 55, as many will be, it seems risky to start reducing potential further growth and locking in a low pension. Equity growth over 10 to 20 years has usually been rather good.

Ozzie Osmond said:

If that is correct, how is the dampened volatility valued? It seems to me that like all insurance it has a cost and to me that cost doesn't look worth incurring with a twenty to thirty year time horizon.

Any way, if and when interest rates rise won't bond prices collapse? Aha you reply, but they're index-linked so it doesn't matter. But buying them now looks mighty expensive to me compared with the risk of running equities.

It's measured in the impact of sequential returns and the ravaging that can happen. If there's no new money coming in, then you can assume that you've achieved the objective and it's more important now, to ring-fence existing wealth and not just continue to grow it for the sake of it.Any way, if and when interest rates rise won't bond prices collapse? Aha you reply, but they're index-linked so it doesn't matter. But buying them now looks mighty expensive to me compared with the risk of running equities.

I agree, buying them now would be more expensive. Hence, plan ahead/buy and hold. Tweek where necessary but measure twice, cut once. Don't forget.. the only UK pension fund solely invested in gilt is the Bank of England pension fund. Ask yourself why.

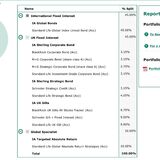

This is one of my personal portfolios, it's suitable for me and not a recommendation for anyone else. I reduced my GARS exposure, back in March.

Ozzie Osmond said:

Yes, but so what? Unless and until the deficit crystallises the deficit is just numbers on a piece of paper. What I find unrealistic is the "assumption" that if the market falls it will never recover - whereas history to date has shown that when the market falls it always recovers.

For a mature scheme (as most UK DB schemes are), real people's pensions are being paid out and hence you need to fund those pensions, you can't just wait until markets recover. And therefore you end up crystallising a loss in your scenario.You also risk not being able to close a subsequent deficit and members losing their pensions - see BHS etc!

Ozzie Osmond said:

Put simply, it appears to me that the price of "safety" is too high to be worth paying. This is presumably why corporate DB pensions have ceased to exist - it's not worth the huge cost of making a future pension promise backed by index-linked bonds. Meanwhile private investors are being encouraged to take on exactly the risks that corporates are running away from, and the government doesn't bother to face the risk at all. It's all very strange.

Pre-retirement, then equities still make sense, but approaching retirement and certainly in-retirement that's a massive investment risk for a sponsor (or an individual) to be running, one that can feasibly put the solvency of the sponsor at risk.Ozzie Osmond said:

Yes, I can see that if a private individual is 55 with a huge "pot" it can theoretically make sense to start de-risking. But if the pot is huge, do they need to de-risk at all? Why not stay in the game for even more growth.

Growth is not guaranteed!Ozzie Osmond said:

If the pot is small at age 55, as many will be, it seems risky to start reducing potential further growth and locking in a low pension. Equity growth over 10 to 20 years has usually been rather good.

The recommendation is not to remove all equity risk within 10 years from retirement, normally a 'lifestyle' approach phases in the bond allocation from the equity allocation linearly over the period, so from 100% equity to 100% bonds over the 10 years.Edited by sidicks on Monday 15th August 13:21

Ozzie Osmond said:

Ginge R said:

the dampened volatility is worth a premium in its own right.

If that is correct, how is the dampened volatility valued? It seems to me that like all insurance it has a cost and to me that cost doesn't look worth incurring with a twenty to thirty year time horizon.Any way, if and when interest rates rise won't bond prices collapse? Aha you reply, but they're index-linked so it doesn't matter. But buying them now looks mighty expensive to me compared with the risk of running equities.

A typical way of looking at the relative value of equities to government bonds is to take consensus earnings forecasts and use those to value the equities as if they were bonds; you know their current market price, you know the market's earning expectation, you can calculate an internal rate of return. Investors demand a higher expected return from equities than bonds because of the greater volatility of equity prices. The spread between bond yields and the IRR above is a measure of that demanded extra return.

I have no idea what that risk premia is these days :-) ... helpful I know. Ten years ago, I'd have had it at my fingertips because we used it as a key indicator of market sentiment. It'd be interesting to see what those numbers look like these days. Since rates have collapsed to virtually zero, the PV of future cashflows is much more sensitive to changes in interest rates than it used to be, so perhaps backing risk premia out of earnings forecasts and equity prices now just leads to noise. It'd be interesting to know if anyone has any figures.

Edited by ATG on Monday 15th August 13:41

Ozzie Osmond said:

^^^ Thanks both for your replies.

It really is a fine juggling exercise trying to find an approach that's "safe enough" whilst remaining affordable.

Indeed, I don't thing there is a right or wrong answer, but you do need to fully understand the risks you are exposed to if you move away from a 'matching' position.It really is a fine juggling exercise trying to find an approach that's "safe enough" whilst remaining affordable.

Ozzie Osmond said:

bad company said:

walm said:

people who are close to retirement don't tend to have huge equity exposure so will have missed much of the rally.

Really? Surely those close to retirement would chose equity funds and/or bonds to maximize income.That's what I did.

- Greatly increased life expectancy

- Low bond yields

- Risk of future inflation

- Availability of SIPP drawdown.

I also still have National Savings Certificates which pay RPI + 0.05% tax free which isn't bad these days and gives me a fall back if there was a 1929 type crash.

Gassing Station | Finance | Top of Page | What's New | My Stuff