What questions should a newbie ask an IFA?

Discussion

We have an IFA coming round this evening for a chat about what we can do with our finances.

I have already given them a breakdown of what is where in a spreadsheet and am looking to convert some of the cash to investments to get greater returns than having it in the bank.

Having never had experience of an IFA, what should I expect and what questions should I be asking to ensure they don't take the cash and put it all on black or something

Like do you give them a cheque and they invest it in the funds they pick or do they give you suggestions then you invest accordingly?

I have already given them a breakdown of what is where in a spreadsheet and am looking to convert some of the cash to investments to get greater returns than having it in the bank.

Having never had experience of an IFA, what should I expect and what questions should I be asking to ensure they don't take the cash and put it all on black or something

Like do you give them a cheque and they invest it in the funds they pick or do they give you suggestions then you invest accordingly?

Typically an IFA will offer guidance on investment vehicles, classes and tax issues etc, rather than picking individual shares and funds for you.

Not sure the figures involved, but perhaps take a look at fiveraday (run by Ginge R here) and others like Nutmeg etc. Robo investment, giving a diversified portfolio based on your attitude to risk.

Not sure the figures involved, but perhaps take a look at fiveraday (run by Ginge R here) and others like Nutmeg etc. Robo investment, giving a diversified portfolio based on your attitude to risk.

Wealth management is what you're looking for, typically for those with a decent wad to invest (may or may not describe you!).

Many, like you, hope an IFA will give them all of this and are disappointed. A good and experienced IFA may give you a lot of assistance in this area, but many will simply have passed the exams and know what products are available.

Many, like you, hope an IFA will give them all of this and are disappointed. A good and experienced IFA may give you a lot of assistance in this area, but many will simply have passed the exams and know what products are available.

What is classed as a decent wad, near 6 figures or something a bit less?

Looking on the unbiased page for their company, it does say one of the services they offer is financial planning/wealth management so they may cover what I am after.

Thanks for explaining the difference, I will see what they say this evening as it may not be what I am after as you say.

Looking on the unbiased page for their company, it does say one of the services they offer is financial planning/wealth management so they may cover what I am after.

Thanks for explaining the difference, I will see what they say this evening as it may not be what I am after as you say.

Edited by KTF on Monday 12th September 16:04

KTF said:

We have an IFA coming round this evening for a chat

Q1 (to ask yourself) Why's he coming to US and not us going to see him? No other "professional" (using the word very loosely) pops round to your house. On the other hand, double-glazing salesmen do!KTF said:

what questions should I be asking to ensure they don't take the cash and put it all on black or something

Q2 If we decide to pay you for advice, how will that advice "add value" to our situation?My suggestion: Have the chat, commit to nothing, definitely don't hand over a cheque - report back to this forum with the key points discussed.

My guess: He'll turn up, tell you how wonderful your house is, how wonderful your car is, how well you are doing in life, how well all of his other clients are doing etc etc etc. So make sure you keep bringing the conversation back to the basics of "how are you going to add value for us?".

Q3 "Exactly how much do you get paid, both for initial advice and into the future?"

Make sure the answers are clear, understandable and not buried in waffle. Remember, a small-looking fee can get big over time. For instance, 10 years isn't long in investing and 1% fee would take 10% of your money!

Q1: The guy coming round is a 'friend' in so far as I know him through the running club that I go to and he is coming over for an informal chat explaining what it is all about, what his company may be able to offer, etc. I am not expecting the double glazing salesman type pitch from him.

Q2: Yes, I will report back afterwards. I know how much interest I am getting from my various accounts so anything they offer will have to be better than that before I even break even. Not hard I assume but it is at least a figure.

Also why should I choose them vs the various robo options now available as I could just put the money into one of those instead rather than go via a middleman.

Q3: I realise there will be a fee involved but no idea what it will be or how it compares to other IFA/options so I see this as a fact finding exercise and I can then bounce the ideas off the people here - who have more knowledge about this than me from what I have read

Q2: Yes, I will report back afterwards. I know how much interest I am getting from my various accounts so anything they offer will have to be better than that before I even break even. Not hard I assume but it is at least a figure.

Also why should I choose them vs the various robo options now available as I could just put the money into one of those instead rather than go via a middleman.

Q3: I realise there will be a fee involved but no idea what it will be or how it compares to other IFA/options so I see this as a fact finding exercise and I can then bounce the ideas off the people here - who have more knowledge about this than me from what I have read

Ok, as a quick summary whilst I remember.

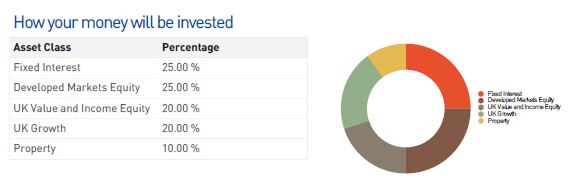

They do fact finding at the start to find out your attitude to risk, what you want to achieve, etc.

Then that is split into the various investment categories, pension, ISA, using this nucleus tool.

Then within each category you have a portfolio based on your risk.

The portfolios are whole of market and have various weighting - low risk is bonds, etc, high risk is oil exploration etc.

You can change them via the IFA but can see an overview any time via the tool.

In the tool you can click the investment category, click the portfolio to see the make up, drill down into the component parts, etc.

The portfolio composition is overseen by a company who can tweak the contents, monitor the returns, etc. to keep them current rather than the IFA try to keep tabs on 4000+ products all the time. Bit like the robo investment tools.

You can have custom built portfolios rather than the mass market robo ones but that costs more due to the work involved.

Management charge for an average risk client portfolio is 1.63%. This covers the IFA as the overseer of the whole process. The value add is them working out the tax efficient strategy then the portfolios in each bucket to use plus regular reviews. No money held by them, all paid in to the tool and invested in the funds.

At a high level the suggestion was to switch from the deposit accounts when the rates drop and regular savers when they mature and drip feed that into a stocks and shares ISA instead to maximise the tax efficiency. The type of ISA will depend on the attitude to risk.

They do fact finding at the start to find out your attitude to risk, what you want to achieve, etc.

Then that is split into the various investment categories, pension, ISA, using this nucleus tool.

Then within each category you have a portfolio based on your risk.

The portfolios are whole of market and have various weighting - low risk is bonds, etc, high risk is oil exploration etc.

You can change them via the IFA but can see an overview any time via the tool.

In the tool you can click the investment category, click the portfolio to see the make up, drill down into the component parts, etc.

The portfolio composition is overseen by a company who can tweak the contents, monitor the returns, etc. to keep them current rather than the IFA try to keep tabs on 4000+ products all the time. Bit like the robo investment tools.

You can have custom built portfolios rather than the mass market robo ones but that costs more due to the work involved.

Management charge for an average risk client portfolio is 1.63%. This covers the IFA as the overseer of the whole process. The value add is them working out the tax efficient strategy then the portfolios in each bucket to use plus regular reviews. No money held by them, all paid in to the tool and invested in the funds.

At a high level the suggestion was to switch from the deposit accounts when the rates drop and regular savers when they mature and drip feed that into a stocks and shares ISA instead to maximise the tax efficiency. The type of ISA will depend on the attitude to risk.

Edited by KTF on Monday 12th September 22:11

KTF said:

Management charge for an average risk client portfolio is 1.63%. This covers the IFA as the overseer of the whole process. No money held by them, all paid in to the tool and invested in the funds.

Hmmmm.It sounds as though he might have told you what he would take of it but hasn't told you what your total costs will be - you need to be aware there could be additional charges within the funds themselves. If the total costs creep up towards 2.5% it would mean 25% of your money in 10 years and will be a real drag on investment performance. Make sure you check.

If you're a beginner at investing the fundamental points include,

- Keep the costs down

- Get some risk on (shares)

- Keep that risk down to what you feel you can handle, both in terms of how much money you put at risk and how risky the investments are

- Use a tax efficient method such as ISA or pension wherever possible

- Invest over a long period of time to suppress the risk of putting everything in just before a big market fall

- Don't panic when there is a market fall. History says things have always recovered in the past, although that doesn't predict the future.

- ...and if you're not paying through the nose for "advice" you shouldn't need to be a brilliant investor to achieve decent returns. So long as you're in the mainstream and nobody is taking a big slice of charges out of you things ought to turn out OK.

Also see what comments you get from other people on this forum. Some of them are pretty good at this stuff and may be able to offer useful suggestions (without straying into the regulated area of advice).

If you feel you do need/want "advice", at least at the outset, I'd find an IFA who will sell you that advice for a one-off fee. Even though it means writing a cheque at the outset, which feels like a cash hit, you won't be getting a slice taken out of you month after month, year after year.

To be honest if you're reasonably intelligent, willing to do some clicking around the internet and keep an eye on this finance forum you might find you don't need advice at all. On the other hand if you're age 50 with huge debts and family issues it would definitely be prudent to go through the full "advice" process!

Edited by Ozzie Osmond on Monday 12th September 22:45

I've not come across Nucleus before, but it looks a pretty good setup. If it includes all fund charges etc, I think 1.63% is reasonable although there's a slight premium for convenience. If it doesn't include fund charges, it's pretty expensive and ultimately you're paying 1.63% of your investment value every year for someone to click the buttons for you.

KTF said:

Ok, as a quick summary whilst I remember.

They do fact finding at the start to find out your attitude to risk, what you want to achieve, etc.

Then that is split into the various investment categories, pension, ISA, using this nucleus tool.

Then within each category you have a portfolio based on your risk.

The portfolios are whole of market and have various weighting - low risk is bonds, etc, high risk is oil exploration etc.

You can change them via the IFA but can see an overview any time via the tool.

In the tool you can click the investment category, click the portfolio to see the make up, drill down into the component parts, etc.

The portfolio composition is overseen by a company who can tweak the contents, monitor the returns, etc. to keep them current rather than the IFA try to keep tabs on 4000+ products all the time. Bit like the robo investment tools.

You can have custom built portfolios rather than the mass market robo ones but that costs more due to the work involved.

Management charge for an average risk client portfolio is 1.63%. This covers the IFA as the overseer of the whole process. The value add is them working out the tax efficient strategy then the portfolios in each bucket to use plus regular reviews. No money held by them, all paid in to the tool and invested in the funds.

At a high level the suggestion was to switch from the deposit accounts when the rates drop and regular savers when they mature and drip feed that into a stocks and shares ISA instead to maximise the tax efficiency. The type of ISA will depend on the attitude to risk.

Did the adviser ask you about debt (mortgage, loans, credit cards, other finance) or any protection needs you may have?They do fact finding at the start to find out your attitude to risk, what you want to achieve, etc.

Then that is split into the various investment categories, pension, ISA, using this nucleus tool.

Then within each category you have a portfolio based on your risk.

The portfolios are whole of market and have various weighting - low risk is bonds, etc, high risk is oil exploration etc.

You can change them via the IFA but can see an overview any time via the tool.

In the tool you can click the investment category, click the portfolio to see the make up, drill down into the component parts, etc.

The portfolio composition is overseen by a company who can tweak the contents, monitor the returns, etc. to keep them current rather than the IFA try to keep tabs on 4000+ products all the time. Bit like the robo investment tools.

You can have custom built portfolios rather than the mass market robo ones but that costs more due to the work involved.

Management charge for an average risk client portfolio is 1.63%. This covers the IFA as the overseer of the whole process. The value add is them working out the tax efficient strategy then the portfolios in each bucket to use plus regular reviews. No money held by them, all paid in to the tool and invested in the funds.

At a high level the suggestion was to switch from the deposit accounts when the rates drop and regular savers when they mature and drip feed that into a stocks and shares ISA instead to maximise the tax efficiency. The type of ISA will depend on the attitude to risk.

Also - and crucially - did the adviser tell you exactly when s/he charged for his/her services?

If not I would be somewhat worried myself as it is impossible to conduct a full review without knowledge of the whole picture. Not stating his/her fees is also very worrying.

Managing the full picture is the job of a financial adviser. They don't manage your investments, the investment manager they select does this.

The way it was explained was that the 1.63% was made up of the nucleus platform, the fund charge that sit in the pots within nucleus and their fee. It is split into 12 and taken monthly. The fee was an example as it varies depending on the fund mix in each risk category.

Their visit last night was primarily to have a chat about the overall process and explain how it all works. If I go with them then they would do the whole fact finding process to decide the risk rating, etc. The setup fee would be £500 which covers the due diligence, setting up the account on nucleus, etc. then the % charge each year.

Their visit last night was primarily to have a chat about the overall process and explain how it all works. If I go with them then they would do the whole fact finding process to decide the risk rating, etc. The setup fee would be £500 which covers the due diligence, setting up the account on nucleus, etc. then the % charge each year.

OP - just as a comparison.

I had an IFA meeting the other day BUT I purely wanted to discuss pensions as I have a number of them and could retire in 18 months time.

The IFA did a complete fact find on my wealth, income, debt etc and an analysis of my attitude to risk and then told me up front that to do an analysis of all my pensions and then a report suggesting any changes would be a fixed fee. He then said that as a follow-up if I wanted him to move the pensions according to the report (if any movement was needed) would be another fixed fee and then if I wanted annual reviews and ongoing management it would be a percentage of the value of my funds.

Right away I knew what all my upfront and ongoing costs would be and thus I am in a position to take some services and not others that I am happy to do myself and fully understand the financial exposure.

I had an IFA meeting the other day BUT I purely wanted to discuss pensions as I have a number of them and could retire in 18 months time.

The IFA did a complete fact find on my wealth, income, debt etc and an analysis of my attitude to risk and then told me up front that to do an analysis of all my pensions and then a report suggesting any changes would be a fixed fee. He then said that as a follow-up if I wanted him to move the pensions according to the report (if any movement was needed) would be another fixed fee and then if I wanted annual reviews and ongoing management it would be a percentage of the value of my funds.

Right away I knew what all my upfront and ongoing costs would be and thus I am in a position to take some services and not others that I am happy to do myself and fully understand the financial exposure.

castroses said:

'Their visit...' ???

I thought it was just your friend from the running club?

If 'they' turned up as a team then that does sound very 'double glazing salesman' like.

I'd avoid.

It was the guy I know. Bad choice of words on my part. No double glazing salesman tactics just explaining to me the process involved and the options available. The nuts and bolts would be worked out if I went with them, filled in the risk questionnaire, financial questionnaire, etc.I thought it was just your friend from the running club?

If 'they' turned up as a team then that does sound very 'double glazing salesman' like.

I'd avoid.

garyhun said:

The IFA did a complete fact find on my wealth, income, debt etc and an analysis of my attitude to risk and then told me up front that to do an analysis of all my pensions and then a report suggesting any changes would be a fixed fee. He then said that as a follow-up if I wanted him to move the pensions according to the report (if any movement was needed) would be another fixed fee and then if I wanted annual reviews and ongoing management it would be a percentage of the value of my funds.

Right away I knew what all my upfront and ongoing costs would be and thus I am in a position to take some services and not others that I am happy to do myself and fully understand the financial exposure.

This would happen if I signed up with them as the formal process. Last night was an informal chat as shuch giving example fees as they did not know my full financial circumstance.Right away I knew what all my upfront and ongoing costs would be and thus I am in a position to take some services and not others that I am happy to do myself and fully understand the financial exposure.

The paperwork they left explained the stages involved - initial meeting, report produced inc all fees based on their recommendations, second meeting to go over the report.

Last night was like a pre-meeting as such. No specifics, just explaining what they do as I am not familiar with the options available.

Gassing Station | Finance | Top of Page | What's New | My Stuff