Pensions - are everyone's losing money or just mine

Discussion

kingston12 said:

They did. I am sure I can change it within the fund, but I wouldn't really know where to start! It is just frustrating that I could have made more money in a basic bank account (or under my mattress!) than they do.

Anyone can make money with the benefit of hindsight.You can ether the minimal investment risk and be satisfied with very low returns, or you can invest in riskier assets and be subject to mark-to-market volatility, Without knowing the asset strategy and the benchmark for the fund, there is no way of telling whether the investment manager has done a good job or not.

Highly unlikely that the employer will pay into a separate scheme for you.

kingston12 said:

I am not laughing so much now! The pension scheme that pays the 15% sent me their statement today - they have lost 8% of my fund as well!

Is there any way I can move out of my current employers scheme without losing the contribution?

Christ, what are you invested in, and who runs it? Unless you're indispensable to the firm, or senior enough to have influence, I very much doubt it. Is there any way I can move out of my current employers scheme without losing the contribution?

sidicks said:

227bhp said:

I was a bit bemused to see mine pays yearly until i'm 103.

I can't see me being around that long so wondering what the point is...

??I can't see me being around that long so wondering what the point is...

Won't it just pay until you die regardless of your age?

There is a lump sum offered at 65, but it's pretty miserly.

Ginge R said:

Christ, what are you invested in, and who runs it? Unless you're indispensable to the firm, or senior enough to have influence, I very much doubt it.

Punter Southall have invested it in the 'L&G Global Equity Current Hedged (50:50)' fund. There are quite a number of other options to look into, so I will at least try to diversify it a bit to see what does best.I Iike L+G, they're making lots of all the right noises with their Multi Asset/Multi Index funds. Your's isn't exactly stellar, but it's not a complete basketcase either. I'd be interesting to learn how it turned an 8% loss, surely not on scheme and additional PS overhead, because, on the surface of it, it's as cheap as chips, so there may be other factors you don't know about. Did you go in at an inopportune time, what was the period of the 8% loss?

It might be that if you move the goalposts by just a few weeks, the picture is very different. It's not just one year snapshots that count, Tn shows strong 5 year growth for the fund, is that reflected in your fund value? I'd be cautious of doing major tweaks with it now, unless you have a completely new life-stage strategy in mind. Equities are pretty much on the ceiling, there's nothing out there which could signify that growth will continue in the manner we've recently become accustomed to.

Equity and bond returns are becoming more correlated and could fall in unison, if we're finally seeing the demise of central bank intervention through QE (and the suppressed volatility which that bought), and a bitterly divisive and uncertain post US election outlook, it may be rocky again for a bit.

https://www.trustnet.com/Factsheets/Factsheet.aspx...

It might be that if you move the goalposts by just a few weeks, the picture is very different. It's not just one year snapshots that count, Tn shows strong 5 year growth for the fund, is that reflected in your fund value? I'd be cautious of doing major tweaks with it now, unless you have a completely new life-stage strategy in mind. Equities are pretty much on the ceiling, there's nothing out there which could signify that growth will continue in the manner we've recently become accustomed to.

Equity and bond returns are becoming more correlated and could fall in unison, if we're finally seeing the demise of central bank intervention through QE (and the suppressed volatility which that bought), and a bitterly divisive and uncertain post US election outlook, it may be rocky again for a bit.

https://www.trustnet.com/Factsheets/Factsheet.aspx...

kingston12 said:

I am not laughing so much now! The pension scheme that pays the 15% sent me their statement today - they have lost 8% of my fund as well!

Is there any way I can move out of my current employers scheme without losing the contribution?

It's not impossible. I worked for a company that did this, and I made my own calls on where to invest.Is there any way I can move out of my current employers scheme without losing the contribution?

Ginge R said:

I Iike L+G, they're making lots of all the right noises with their Multi Asset/Multi Index funds. Your's isn't exactly stellar, but it's not a complete basketcase either. I'd be interesting to learn how it turned an 8% loss, surely not on scheme and additional PS overhead, because, on the surface of it, it's as cheap as chips, so there may be other factors you don't know about. Did you go in at an inopportune time, what was the period of the 8% loss?

It might be that if you move the goalposts by just a few weeks, the picture is very different. It's not just one year snapshots that count, Tn shows strong 5 year growth for the fund, is that reflected in your fund value? I'd be cautious of doing major tweaks with it now, unless you have a completely new life-stage strategy in mind. Equities are pretty much on the ceiling, there's nothing out there which could signify that growth will continue in the manner we've recently become accustomed to.

Equity and bond returns are becoming more correlated and could fall in unison, if we're finally seeing the demise of central bank intervention through QE (and the suppressed volatility which that bought), and a bitterly divisive and uncertain post US election outlook, it may be rocky again for a bit.

https://www.trustnet.com/Factsheets/Factsheet.aspx...

Thanks.It might be that if you move the goalposts by just a few weeks, the picture is very different. It's not just one year snapshots that count, Tn shows strong 5 year growth for the fund, is that reflected in your fund value? I'd be cautious of doing major tweaks with it now, unless you have a completely new life-stage strategy in mind. Equities are pretty much on the ceiling, there's nothing out there which could signify that growth will continue in the manner we've recently become accustomed to.

Equity and bond returns are becoming more correlated and could fall in unison, if we're finally seeing the demise of central bank intervention through QE (and the suppressed volatility which that bought), and a bitterly divisive and uncertain post US election outlook, it may be rocky again for a bit.

https://www.trustnet.com/Factsheets/Factsheet.aspx...

The loss was made over a period of April 2015 to April 2016. I'll have to check the previous statements, but I have been in the scheme for about 6 years, and judging by the total balance it has averaged about a 6% growth up until now.

If it is just a one off, I am not too worried but just aware that I can't afford too many like that!

It's recovered well since April, this may help. Oversimplistically maybe, the manager looks like he was doing really well, overcooked it a little, slammed the anchors on and then found himself in too high a gear coming out of the bend (to use an analogy). It'd be interesting to see his numbers.

If you really can't afford too many like that, take advice on, or consider derisking a little - you're in a particularly spicy basket. Do you need to take that sort of equity exposure, more to the point, can you afford to take a hit that usually comes with with a basket like that, when things slide?

If you really can't afford too many like that, take advice on, or consider derisking a little - you're in a particularly spicy basket. Do you need to take that sort of equity exposure, more to the point, can you afford to take a hit that usually comes with with a basket like that, when things slide?

Ginge R said:

It's recovered well since April, this may help. Oversimplistically maybe, the manager looks like he was doing really well, overcooked it a little, slammed the anchors on and then found himself in too high a gear coming out of the bend (to use an analogy). It'd be interesting to see his numbers.

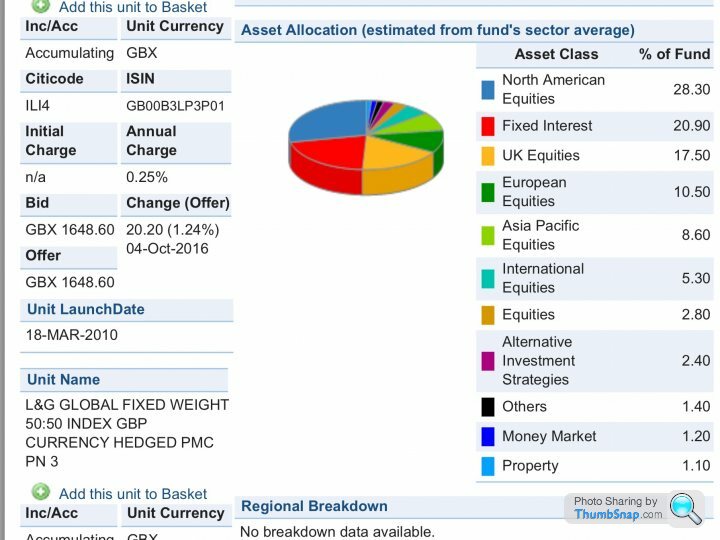

Errrr.... It's an index fund run to fixed weights 50% UK / 50% "overseas". There's no manager to overcook anything as no-one is exercising any judgement or discretion.On the other hand it's cheap - you are only paying 0.25% pa for it. Cheap of course isn't the same as good value. Your fund has gained 6.91% so far this year and 23.09% during the last 3 years, vs 17.86% and 37.59% for the average fund in the global equities sector.

The fund is meant "To capture the sterling total returns of the UK and overseas equity markets as represented by the FTSE All-Share Index in the UK and appropriate sub- divisions of the FTSE World Index overseas, with fixed asset allocation between the UK (50%) and overseas (50%). The overseas exposure of 50% is divided 17.5% in Europe (excluding UK), 17.5% in North America, 8.75% in Japan and 6.25% in Asia Pacific (excluding Japan)."

L&G no doubt calculate the index return on this basis. They could show you how well the fund has done at "capturing" these returns over time. That they don't show this obvious comparison suggests that they have likely failed to match the underlying constituent indices. The absence of this comparison is convenient for them, and for Punter Southall.

A large part of the underperformance vs sector this year will be because of the currency hedged nature of the fund. To be fair, if the Brexit vote had gone the other way and GBP had strengthened this would look like a smart move not a minor disaster.

It's a Subway sandwich fund - superficially attractive but cheap because it is factory made with cheap ingredients. It no doubt meets the risk-management needs of everyone (trustees, advisers, scheme sponsors) who could be on the hook for anything. Unfortunately their needs aren't necessarily the same as yours.

WindyCommon said:

Errrr.... It's an index fund run to fixed weights 50% UK / 50% "overseas". There's no manager to overcook anything as no-one is exercising any judgement or discretion.

On the other hand it's cheap - you are only paying 0.25% pa for it. Cheap of course isn't the same as good value. Your fund has gained 6.91% so far this year and 23.09% during the last 3 years, vs 17.86% and 37.59% for the average fund in the global equities sector.

Surely the relevant comparison is NOT with the Global Equities sector in isolation!On the other hand it's cheap - you are only paying 0.25% pa for it. Cheap of course isn't the same as good value. Your fund has gained 6.91% so far this year and 23.09% during the last 3 years, vs 17.86% and 37.59% for the average fund in the global equities sector.

WindyCommon said:

The fund is meant "To capture the sterling total returns of the UK and overseas equity markets as represented by the FTSE All-Share Index in the UK and appropriate sub- divisions of the FTSE World Index overseas, with fixed asset allocation between the UK (50%) and overseas (50%). The overseas exposure of 50% is divided 17.5% in Europe (excluding UK), 17.5% in North America, 8.75% in Japan and 6.25% in Asia Pacific (excluding Japan)."

L&G no doubt calculate the index return on this basis. They could show you how well the fund has done at "capturing" these returns over time. That they don't show this obvious comparison suggests that they have likely failed to match the underlying constituent indices. The absence of this comparison is convenient for them, and for Punter Southall.

Do you have the data?L&G no doubt calculate the index return on this basis. They could show you how well the fund has done at "capturing" these returns over time. That they don't show this obvious comparison suggests that they have likely failed to match the underlying constituent indices. The absence of this comparison is convenient for them, and for Punter Southall.

WindyCommon said:

A large part of the underperformance vs sector this year will be because of the currency hedged nature of the fund. To be fair, if the Brexit vote had gone the other way and GBP had strengthened this would look like a smart move not a minor disaster.

Indeed, but if it said 'currency hedged' on the tin, that's what it should be compared against!WindyCommon said:

It's a Subway sandwich fund - superficially attractive but cheap because it is factory made with cheap ingredients. It no doubt meets the risk-management needs of everyone (trustees, advisers, scheme sponsors) who could be on the hook for anything. Unfortunately their needs aren't necessarily the same as yours.

As always it's important to understand what you are buying (and what you are NOT buying!).

WindyCommon said:

Errrr.... It's an index fund run to fixed weights 50% UK / 50% "overseas". There's no manager to overcook anything as no-one is exercising any judgement or discretion.

Hi Ian,In reality, hardly any active fund has just one manager either, but we still refer to the team as 'The Manager'. In this instance, the task is promulgated as being down to "LGIM Index Fund Management Team", with invariably a titular head, but carrying the responsibility, and farming the tasks out to teams of specialists. There are still parameters that have to be set, and all indexed funds are invested, proportionately, in ways and in weights that are set up at outset. Look at the L+G (seeing as we're being topical) and check its 350 Tracker - its tracking error is somewhere in the region of 18% at variance to its benchmark. Others, c.3/4%.

That's down to 'the manager', albeit a notional one. You'll see reference in the fact sheet.

http://www.fundslibrary.co.uk/fundslibrary.dataret...

It looks as if something like 1.8% is allocated to alternative strategies, which may indicate the hedge. I don't know who called that, or how it turned out, or indeed, how this particular fund is weighted, but whatever it was doing it was certainly stoking along nicely, and then it hit the buffers a little, and when the market picked up the other month, it was (and remains) sluggish catching up. That, I have no doubt, will be largely down to the hedge. I don't know how you could suggest an adviser would be happy using it. If there's no transparency or understanding, I certainly wouldn't. Advisers are not its intended route to market though (I imagine).

Ginge R said:

Hi Ian,

In reality, hardly any active fund has just one manager either, but we still refer to the team as 'The Manager'. In this instance, the task is promulgated as being down to "LGIM Index Fund Management Team", with invariably a titular head, but carrying the responsibility, and farming the tasks out to teams of specialists. There are still parameters that have to be set, and all indexed funds are invested, proportionately, in ways and in weights that are set up at outset. Look at the L+G (seeing as we're being topical) and check its 350 Tracker - its tracking error is somewhere in the region of 18% at variance to its benchmark. Others, c.3/4%.

That's down to 'the manager', albeit a notional one. You'll see reference in the fact sheet.

http://www.fundslibrary.co.uk/fundslibrary.dataret...

It looks as if something like 1.8% is allocated to alternative strategies, which may indicate the hedge. I don't know who called that, or how it turned out, or indeed, how this particular fund is weighted, but whatever it was doing it was certainly stoking along nicely, and then it hit the buffers a little, and when the market picked up the other month, it was (and remains) sluggish catching up. That, I have no doubt, will be largely down to the hedge. I don't know how you could suggest an adviser would be happy using it. If there's no transparency or understanding, I certainly wouldn't. Advisers are not its intended route to market though (I imagine).

Hi Al. It wasn't me that attributed sentience (or gender..!) to the manager of this fund.In reality, hardly any active fund has just one manager either, but we still refer to the team as 'The Manager'. In this instance, the task is promulgated as being down to "LGIM Index Fund Management Team", with invariably a titular head, but carrying the responsibility, and farming the tasks out to teams of specialists. There are still parameters that have to be set, and all indexed funds are invested, proportionately, in ways and in weights that are set up at outset. Look at the L+G (seeing as we're being topical) and check its 350 Tracker - its tracking error is somewhere in the region of 18% at variance to its benchmark. Others, c.3/4%.

That's down to 'the manager', albeit a notional one. You'll see reference in the fact sheet.

http://www.fundslibrary.co.uk/fundslibrary.dataret...

It looks as if something like 1.8% is allocated to alternative strategies, which may indicate the hedge. I don't know who called that, or how it turned out, or indeed, how this particular fund is weighted, but whatever it was doing it was certainly stoking along nicely, and then it hit the buffers a little, and when the market picked up the other month, it was (and remains) sluggish catching up. That, I have no doubt, will be largely down to the hedge. I don't know how you could suggest an adviser would be happy using it. If there's no transparency or understanding, I certainly wouldn't. Advisers are not its intended route to market though (I imagine).

The tracking error - the dirty secret of the passive industry - will be largely attributable to implementation inefficiencies not to the manager exercising discretion in any way.

No-one "called" the hedge either. As sidicks pointed out earlier it's intrinsic to the fund so won't be the subject of debate or judgement - just another automated process.

I agree with your observation that advisers shouldn't use funds they don't understand.

I'm not so sure about inefficiencies, more, 'characteristics'..?

Some of which relate to its weighting policy (even volatility of benchmarks against an identical index can be different), but given that booking charges, various disbursements, fees and costs also affect tracking error, in old money, we'd call it (more kindly) 'overhead'.

LG's fund would be a great chance to dip into a passive to discover the other little secret of the passive world.. 'active risk'. We all know passives have management teams, which have overhead. The worry for management houses is that when people cotton on, they'll also want to know why some managers can't attach closer pricing to active funds.

If advisers can't understand a product, it's fair to assume that most retail clients either. So, the more important issue here is why this is being sold as an occupational fund. I wonder how many who hold it, understand it. Could I understand how the hedge works? Sure, but you'd have to set aside a week learning about it in sufficient depth to then someone, who's eyes would glaze over after five minutes. Crazy.

Interesting thoughts from the Regulator yesterday, which could prove illuminating.

https://www.fca.org.uk/news/press-releases/fca-pub...

Some of which relate to its weighting policy (even volatility of benchmarks against an identical index can be different), but given that booking charges, various disbursements, fees and costs also affect tracking error, in old money, we'd call it (more kindly) 'overhead'.

LG's fund would be a great chance to dip into a passive to discover the other little secret of the passive world.. 'active risk'. We all know passives have management teams, which have overhead. The worry for management houses is that when people cotton on, they'll also want to know why some managers can't attach closer pricing to active funds.

If advisers can't understand a product, it's fair to assume that most retail clients either. So, the more important issue here is why this is being sold as an occupational fund. I wonder how many who hold it, understand it. Could I understand how the hedge works? Sure, but you'd have to set aside a week learning about it in sufficient depth to then someone, who's eyes would glaze over after five minutes. Crazy.

Interesting thoughts from the Regulator yesterday, which could prove illuminating.

https://www.fca.org.uk/news/press-releases/fca-pub...

Ginge R said:

I'm not so sure about inefficiencies, more, 'characteristics'..?

Some of which relate to its weighting policy (even volatility of benchmarks against an identical index can be different), but given that booking charges, various disbursements, fees and costs also affect tracking error, in old money, we'd call it (more kindly) 'overhead'.

Inefficiency is the umbrella term typically used to capture all of the above and more. It isn't perjorative so doesn't need to be refashioned.Some of which relate to its weighting policy (even volatility of benchmarks against an identical index can be different), but given that booking charges, various disbursements, fees and costs also affect tracking error, in old money, we'd call it (more kindly) 'overhead'.

Perhaps the interesting point is that index funds frequently underperform the indices they seek to replicate. The passive industry is quick to observe that indices beat active funds. They beat passive funds too...!

Sort of on this topic.. my employer provides a scheme where I can effectively monitor, change and amend my pension contributions, as well as move the funds around. We use a provider called Orbit, who I believe are now part of Capita.

Question for the IFA's on here. Where employees have these facilities, which are great, where should I get proper advice around where to invest? At the moment it seems to be pot luck in selecting the right funds, maybe based upon risk factor or the best fund that has been performing in the last 12 months. Do IFA's provide advice on which funds to invest? Sorry if it is a stupid question...

G

Question for the IFA's on here. Where employees have these facilities, which are great, where should I get proper advice around where to invest? At the moment it seems to be pot luck in selecting the right funds, maybe based upon risk factor or the best fund that has been performing in the last 12 months. Do IFA's provide advice on which funds to invest? Sorry if it is a stupid question...

G

If you post up the names of funds in which you're invested or thinking about you may get useful comments from people on this forum. If you're over age 50 it would be worth mentioning what % of your total value is in each fund - there's no need to mention the actual ££ amounts.

Whether or not it's worth spending money for "advice" on this is always debateable. Depends on your own level of confidence and how much trust you're willing to put in someone else - who may or may not be any good and certainly isn't taking any risk; the risk is still yours.

Whether or not it's worth spending money for "advice" on this is always debateable. Depends on your own level of confidence and how much trust you're willing to put in someone else - who may or may not be any good and certainly isn't taking any risk; the risk is still yours.

WindyCommon said:

Inefficiency is the umbrella term typically used to capture all of the above and more. It isn't perjorative so doesn't need to be refashioned.

Perhaps the interesting point is that index funds frequently underperform the indices they seek to replicate. The passive industry is quick to observe that indices beat active funds. They beat passive funds too...!

Indeed. One reason why charges are so opaque?Perhaps the interesting point is that index funds frequently underperform the indices they seek to replicate. The passive industry is quick to observe that indices beat active funds. They beat passive funds too...!

Only this sector could make costs and charges look like a reluctant but necessary evil. Profits aren’t reduced, they’re adjusted or revised, fraud is now (in many instances) 'mis-selling', a rich person is one who is high-net-worth and we don't have interest free loans, we now have zero percent finance. But the biggest financial services sector rebranding scam? Rebranding debt as credit. Absolute genius.

I take your point completely about poor passives/good passives - I'm not a passive slave. LG, Scottish Widows, Virgin FTSE100 Tracker, utterly awful things. A passive will (usually) beat another passive due to its weighting. Actives are far more prone to conviction bias (dear god, I'm speaking in financial services lingo now, too), conviction error etc.. even, as I heard strongly implied the other day, recency bias. I was stunned. From a highly regarded fund manager, too.

Gio G said:

Sort of on this topic.. my employer provides a scheme where I can effectively monitor, change and amend my pension contributions, as well as move the funds around. We use a provider called Orbit, who I believe are now part of Capita.

Question for the IFA's on here. Where employees have these facilities, which are great, where should I get proper advice around where to invest? At the moment it seems to be pot luck in selecting the right funds, maybe based upon risk factor or the best fund that has been performing in the last 12 months. Do IFA's provide advice on which funds to invest? Sorry if it is a stupid question...

G

Ask your employer if they provide an advice service, your HR dept is probably your first port of call. Crapi.. sorry, Capita, is quite a slick proposition - are there such things as pension strategies or general investment suggestions? Question for the IFA's on here. Where employees have these facilities, which are great, where should I get proper advice around where to invest? At the moment it seems to be pot luck in selecting the right funds, maybe based upon risk factor or the best fund that has been performing in the last 12 months. Do IFA's provide advice on which funds to invest? Sorry if it is a stupid question...

G

Gassing Station | Finance | Top of Page | What's New | My Stuff