BTL vs Shares (Funds) vs Alternatives

Discussion

drainbrain said:

Not that I'm against capital gain - far from it. But when inflation is built into the calculation then the gains can sometimes feel pretty poor. However, I've had a great few decades in btl and would certainly stick all my eggs in it again given the opportunity. Having said that, I've spent the last few years turning a largish leveraged portfolio (100's) into a small and unburdened one with a plan to reduce to 50 over the next 12 months and use some of the capital to diversify into financing redevelopment.

I'm no longer in the agency business but things seem to be becoming increasingly more negative from that perspective. Everything is becoming hugely overburdened with legislation and regulation. The latest thing in Scotland is compulsory regular checking for Legionella. I mean I ask you….Legionella! An agency now has to drag these things, like EPCertifying , Legionella checking, elec appliance checking etc in-house by having a staff member go on whatever training course is required to be able to carry out these functions which of course are then charged to the landlord. But agents want to market and manage properties, not spend their days (and resources) on fairly futile administration exercises that really are of little or no benefit to almost everyone.

Nice to see England following Scotland into banning the 'scam' type agency expenses. We're now in an era where there's no room for any extra costs in finding accommodation and agents really have to recognise that.

That's some interesting insight, and an impressive portfolio you've built! I'm no longer in the agency business but things seem to be becoming increasingly more negative from that perspective. Everything is becoming hugely overburdened with legislation and regulation. The latest thing in Scotland is compulsory regular checking for Legionella. I mean I ask you….Legionella! An agency now has to drag these things, like EPCertifying , Legionella checking, elec appliance checking etc in-house by having a staff member go on whatever training course is required to be able to carry out these functions which of course are then charged to the landlord. But agents want to market and manage properties, not spend their days (and resources) on fairly futile administration exercises that really are of little or no benefit to almost everyone.

Nice to see England following Scotland into banning the 'scam' type agency expenses. We're now in an era where there's no room for any extra costs in finding accommodation and agents really have to recognise that.

When you say financing redevelopment, do you mean lending to builders in return for a share of profits when projects are completed? I imagine the return on this is better than BTL, within a shorter timeframe and with more guarantees?

simong800 said:

Yes I was surprised at how high the "price of entry" is now in terms of deposit requirements. Did it always used to be 35-40% needed?

So much has changed re. lending since The Great Humiliation that it's impossible to recognise it in the same way. It also seems to have become much more homogenised as well, as opposed to pre-Humiliation days when individuals made different deals in different ways. Of course borrowers strategies have changed (evolved?) too, and I must say I don't really understand why either a lender or a borrower would want to do IO business for btl. It really doesn't make sense for anyone - apart from for 'btl' which is really 'btsell'. Seriously. Anyone who says different is wrong. In fact, let me go further. If the repayments of a cap-and-int loan means that the property will generate no or next-to-no income then the deal shouldn't be done. That's worth making a rule. The exception being if the repayment loan is of the shortest duration. 4 or 5 years very max.From '05 to '09 I worked with RBS Corporate with a portfolio loan based on the 'global' value of the portfolio. One covenant was that the 'global' LTV shouldn't exceed 75%. Of course the repayment instalments meant that the LTV was always lowering and when prices were rocketing it meant the LTV was lowering even faster. So often enough when another property was to be added in to the portfolio, especially one obtainable BMV, 100% of the purchase price could be borrowed. However, the greatest of care needs to be taken with several aspects of this strategy, not least keeping an eye on the notion of 'marking to market', and I certainly wouldn't advocate over-borrowing for anyone, never mind the 'property guru' insanity of borrowing every penny including funding deposits from credit cards etc.

Don't get me wrong, I LIKE (very much like) funding stunts with OPM. But OPM requires to be respected and should be approached on the principle that OPM requires to be repaid if the 'brilliant idea' goes wrong.

sidicks said:

drainbrain said:

But can you take a pot of cash and invest in equities for income from the get-go - as you can if you buy, say, a tenanted property?

Yes.simong800 said:

When you say financing redevelopment, do you mean lending to builders in return for a share of profits when projects are completed? I imagine the return on this is better than BTL, within a shorter timeframe and with more guarantees?

Basically working with a builder. I'd probably enjoy participating in the land/project hunt and work with the marketing of the end product but main role would be as the money alongside a builder partner if I can find a good one who's up for it.It's really so different to btl that its returns and guarantees are barely comparable. Sure the overall profit on an individual project returns quicker, but btl's the 'gift that keeps giving', isn't it? As to 'guarantees', well I'll stick with 'death and taxes'

TBH I'd consider development as far far more risky.

TBH I'd consider development as far far more risky.drainbrain said:

sidicks said:

drainbrain said:

But can you take a pot of cash and invest in equities for income from the get-go - as you can if you buy, say, a tenanted property?

Yes.drainbrain said:

So what would YOU do with a large sum right now to generate income and also to retain (tho not necessarily increase) value ? Equities or property? (You're only allowed to choose, so 'both' isn't an answer). Assume 'passive' investment and managed property.

Portfolio of FTSE 100 equities with a call overwriting strategy on top.NickCQ said:

Most BTL mortgages these days are I/O, so it is unlikely that you will pay down the principal balance significantly through the lifetime of the loan. I read a UBS research report that estimates that after the recent BTL tax changes the expected net yield on an average BTL is 0%, i.e. there is no cash left over from the rental income after paying interest, maintenance and taxes. You'd have to do your own numbers but it's not going to be great.

S&S ISA really is the hassle free solution. Invest £20k per annum totally tax free in low cost index tracker funds and over a long enough time period you will make the compound market return, which for equities is between 5 and 10%. You may do slightly better or worse depending on when you buy in and when you liquidate. But if you are cost averaging properly on entry you can also reduce those risks, similarly if you carry out a phased liquidation of your portfolio in retirement. It takes me approximately 1 hour at the beginning of each financial year to transfer £20k to my S&S ISA, select funds and invest. Then I go back to my day job for another year (and posting drivel on PH of course).

But... your upside is much lower vs property. If your 75% leveraged BTL goes up in value by 50% (not unheard of in the UK market), then you have made 3x your money on the equity before rental income or taxes. Hard to achieve with S&P / FTSE trackers in a reasonable timeframe. But if the property goes down by 25%, then you have lost all your money - as sidicks says this is the power of leverage.

Thanks, that's an interesting post regarding the S&S potential, like I say, I probably wouldn't buy any more btl right now as I don't really want any more debt or to have all my eggs in one basket. So I'm interested in further reading on the tax benefits etc of S&S.S&S ISA really is the hassle free solution. Invest £20k per annum totally tax free in low cost index tracker funds and over a long enough time period you will make the compound market return, which for equities is between 5 and 10%. You may do slightly better or worse depending on when you buy in and when you liquidate. But if you are cost averaging properly on entry you can also reduce those risks, similarly if you carry out a phased liquidation of your portfolio in retirement. It takes me approximately 1 hour at the beginning of each financial year to transfer £20k to my S&S ISA, select funds and invest. Then I go back to my day job for another year (and posting drivel on PH of course).

But... your upside is much lower vs property. If your 75% leveraged BTL goes up in value by 50% (not unheard of in the UK market), then you have made 3x your money on the equity before rental income or taxes. Hard to achieve with S&P / FTSE trackers in a reasonable timeframe. But if the property goes down by 25%, then you have lost all your money - as sidicks says this is the power of leverage.

However, I keep hearing that most btl loans are interest only. That maybe so but I know an awful lot of people into btl and very few are Into interest only lending. I've certainly never even been offered an interest only loan. Like other posters have mentioned it seems to push away one of the benefits of btl. Unless of course they are reinvesting that money into something safe and long term. Anyway, I can assure you my btl is profitable this year, and will be profitable come 2020 when the tax changes are in full effect. Any btl investors that did their sums based on interest only are likely to hit a financial wall within the next few years.

sidicks said:

drainbrain said:

So what would YOU do with a large sum right now to generate income and also to retain (tho not necessarily increase) value ? Equities or property? (You're only allowed to choose, so 'both' isn't an answer). Assume 'passive' investment and managed property.

Portfolio of FTSE 100 equities with a call overwriting strategy on top.Next year (possibly even later but probably 2017) I'm due a large (6 zero) payoff which will need a home and I am hoping to NOT invest it in property or in any trading business entity either actively or passively. Unfortunately those are all I really know, so it's time to take a plunge into the abyss.

This 'retirement' caper isn't really working out at all well. In fact it's gradually edging its way to the bin. And passive investment's no answer either. There are 100% definitely people who don't suit retirement. That doesn't mean there's no leisure time or interests - quite the opposite. It's just the uncoupling from 'involvements' that doesn't want to happen. Much more attention needs to be paid to this by people who foresee an OAP crisis on the horizon because there's an answer in there to the old age survival question.

drainbrain said:

I am going to take that answer very seriously.

Next year (possibly even later but probably 2017) I'm due a large (6 zero) payoff which will need a home and I am hoping to NOT invest it in property or in any trading business entity either actively or passively. Unfortunately those are all I really know, so it's time to take a plunge into the abyss.

This 'retirement' caper isn't really working out at all well. In fact it's gradually edging its way to the bin. And passive investment's no answer either. There are 100% definitely people who don't suit retirement. That doesn't mean there's no leisure time or interests - quite the opposite. It's just the uncoupling from 'involvements' that doesn't want to happen. Much more attention needs to be paid to this by people who foresee an OAP crisis on the horizon because there's an answer in there to the old age survival question.

You asked a serious question so I answered accordingly.Next year (possibly even later but probably 2017) I'm due a large (6 zero) payoff which will need a home and I am hoping to NOT invest it in property or in any trading business entity either actively or passively. Unfortunately those are all I really know, so it's time to take a plunge into the abyss.

This 'retirement' caper isn't really working out at all well. In fact it's gradually edging its way to the bin. And passive investment's no answer either. There are 100% definitely people who don't suit retirement. That doesn't mean there's no leisure time or interests - quite the opposite. It's just the uncoupling from 'involvements' that doesn't want to happen. Much more attention needs to be paid to this by people who foresee an OAP crisis on the horizon because there's an answer in there to the old age survival question.

I wouldn't do it myself though, I'd find an expert to do it for me in a pooled fund!

But I'm fully aware that if the market tickets upwards I have a severely limited upside (you indicated you were focussed on income not capital gain) and I still have downside risk if the market falls in the short term, regardless of how well the fund managed does his job.

Edited by sidicks on Wednesday 30th November 15:37

sidicks said:

I wouldn't do it myself though, I'd find an expert to do it for me in a pooled fund!

Given an albeit limited history of equity investment that entirely comprises of turning a larger sum of money into a smaller sum I think that's a fair certainty as to how it will be progressed.There will always be a demand for property as no government builds enough to meet demand which keeps property high and rental demand higher. If your view on BTL as your post suggests is to cover a repayment mortgage for 10 years, get it debt free and only then rely on it for any income then IMO it's never too late and combined with your S&S investments you should build up a healthy retirement pot over the years.

I would suggest a decent agent does everything for you taking away any hassle to allow you to concentrate full time on the business. With a good property, agent and tenants you shouldn't need to speak to anyone more than a couple of times a year I don't.

I would suggest a decent agent does everything for you taking away any hassle to allow you to concentrate full time on the business. With a good property, agent and tenants you shouldn't need to speak to anyone more than a couple of times a year I don't.

BoRED S2upid said:

There will always be a demand for property as no government builds enough to meet demand which keeps property high and rental demand higher

That's true, but rents and prices do not always move in lockstep. Yields are lower now than they have ever been in all fixed-income asset classes. If this were to change I would imagine property prices would start to decline with minimal decline in rental income.

drainbrain said:

sidicks said:

I wouldn't do it myself though, I'd find an expert to do it for me in a pooled fund!

Given an albeit limited history of equity investment that entirely comprises of turning a larger sum of money into a smaller sum I think that's a fair certainty as to how it will be progressed.sidicks said:

drainbrain said:

sidicks said:

I wouldn't do it myself though, I'd find an expert to do it for me in a pooled fund!

Given an albeit limited history of equity investment that entirely comprises of turning a larger sum of money into a smaller sum I think that's a fair certainty as to how it will be progressed.drainbrain said:

Well actually I was agreeing with you that an expert will be essential given that any previous efforts at 'investment' by me including individual share buying or via policies has turned into an unmitigated financial disaster. With the exception of Abbey National shares. Which as I recall I got for nothing, making it hard to sell them at a loss.

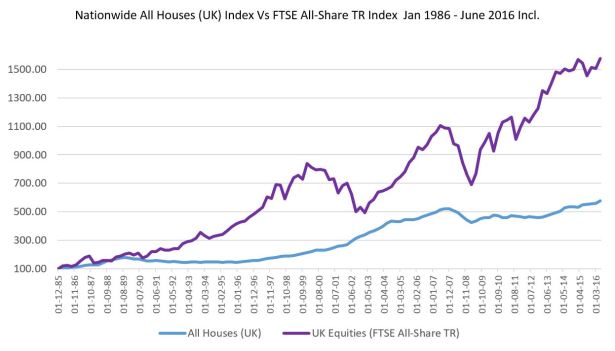

Buying individual shares is a massive risk - very binary outcomesSee the performance of the equity index over a long time horizon above!

Gassing Station | Finance | Top of Page | What's New | My Stuff