Your Investment performance for 2016.

Discussion

No idea what my 'annualised' figure is but overall I am up 22/23% in my Vanguard S&S ISA.

Quite a few years back I was buying individual stocks, made and lost money but likely lost more due to the trading fees from constantly buying and selling trying to 'time' the peaks and troughs. I made and lost a fair bit on AIM too, it's like the wild west out there....

Then sold out the lot and switched to a single global fund via Vanguard about 3 years back.

March/April this year was a testing period with the big market drop but helped me to build some mental fortitude to sitting on a big loss and rather than sell at a loss (as I would of in my early days) I did the complete opposite and bought more!

I will dabble in individual stocks again but for now am content with using a single global fund,less stressful and I find that I resist the urge to tinker with it. I'm not chasing the biggest returns but rather more consistent reasonable returns whilst keeping my costs as low as possible.

Quite a few years back I was buying individual stocks, made and lost money but likely lost more due to the trading fees from constantly buying and selling trying to 'time' the peaks and troughs. I made and lost a fair bit on AIM too, it's like the wild west out there....

Then sold out the lot and switched to a single global fund via Vanguard about 3 years back.

March/April this year was a testing period with the big market drop but helped me to build some mental fortitude to sitting on a big loss and rather than sell at a loss (as I would of in my early days) I did the complete opposite and bought more!

I will dabble in individual stocks again but for now am content with using a single global fund,less stressful and I find that I resist the urge to tinker with it. I'm not chasing the biggest returns but rather more consistent reasonable returns whilst keeping my costs as low as possible.

mikeiow said:

GT03ROB said:

Countdown said:

Via a First Direct S&S platform (they charge £11/qtr). The majority is in an ISA, and the majority of investments are in Vanguard trackers. I can see what my biggest losers are (I bought HSBC at approx £5.50 a share average, it’s now trading at under £4,,,,I think about 10% of my portfolio is in HSBC)

To be fair the amount I had to invest at the beginning was relatively small (less than £5k per annum). It increased a lot over the last few years so I’d say probably 70% of my investments have been over the last 3-4 years.

10% in one stock...To be fair the amount I had to invest at the beginning was relatively small (less than £5k per annum). It increased a lot over the last few years so I’d say probably 70% of my investments have been over the last 3-4 years.

.... it sounds like you have been heavily into UK banking & oils. Basically FTSE 100. I’d step back & really look at what you have. Then ask yourself is it balanced across global markets & sectors.

.... it sounds like you have been heavily into UK banking & oils. Basically FTSE 100. I’d step back & really look at what you have. Then ask yourself is it balanced across global markets & sectors. I’m no expert but on a 15yr view I’ve averaged a 8.5% return per year. Over the years that compounds into a nice little increase. You need to find a strategy you are comfortable with & understand.. Over time I shift where my emphasis is but always look long term and rarely back single companies, but will back single sectors eg Gold or countries eg India

Invest in the world......

In the video below he talks about the risks and psychology of owning individual stocks.

https://youtu.be/AecvTErBQY8

VR99 said:

I will dabble in individual stocks again but for now am content with using a single global fund,less stressful and I find that I resist the urge to tinker with it. I'm not chasing the biggest returns but rather more consistent reasonable returns whilst keeping my costs as low as possible.

Likewise. 90% of my overall portfolio are held in diversified passive tracker funds with solid reputable companies (mostly Vanguard and some in Fidelity). I do have 10% in an active fund (with 4 x fund cost over a passive fund!), but I don't chase the top performing fund, and broadly just accept the market return i.e. bit like the tortoise slow and steady approach. Given I no longer draw a working income, preservation of my capital is higher on my priority list, so my portfolio is probably more conservative than most, but I have followed the passive tracker strategy and adjust the risk level to suit since day 1. Then I simply let the best investment tool (time) do it's job. I started investing in August 2020. Between then and now I have bought £20k of stock, including $5k of Tesla at the outset. Somehow I have increased this to £30,500. This was a risky strategy of listening for tips on here and Twitter, not be recommended but my Tesla share increases meant that I could take a change.

Using Vanguard, primarily LifeStrategy 80, my return for 2020 is 11%.

Given how diversified it is, I am quite content. Tends to show that for every loser, there tends to be a winning stock. It is quite heavily invested in the US so with £Sterling likely to rise against the $US post Brexit and the US plateauing post-Trump, i am not sure how it will do in 2021.

Given how diversified it is, I am quite content. Tends to show that for every loser, there tends to be a winning stock. It is quite heavily invested in the US so with £Sterling likely to rise against the $US post Brexit and the US plateauing post-Trump, i am not sure how it will do in 2021.

rockin said:

I had a brief click to see how major stock markets performed in 2020,

USA - up 16% (S&P 500)

Europe - down 6% (Eurostoxx average)

UK - down 14% (FTSE 100, down 11% if you take dividends into account)

The USA indices are up, but on just a few companies.USA - up 16% (S&P 500)

Europe - down 6% (Eurostoxx average)

UK - down 14% (FTSE 100, down 11% if you take dividends into account)

Take out the top performers and the funds would look just like the FTSE and Euro markets.

In a sense you are over-exposed to just a few companies by tracking or buying those indices right now (or in the last 3-6 months)

It’s going to be a day of reckoning for the FAANGS (etc)... some will prevail, some won’t.

It’s like Dotcom all over again.

That is IMO one of the reasons not to focus too much on buying passive index funds. I’d rather pay someone, somewhere to think about what they’re buying and why they’re buying it. Similarly I don’t find benchmarks particularly useful because they tend to restrict divergence from the norm.

The secret IMO is to get equity returns without too much risk. The problem remains that when a market drops it tends to take everything with it - then you need to hold your nerve and not sell in a panic. If you’re invested in the right things they should, hopefully, come back over time.

The current boom in global stock markets is beyond my understanding. I fear it may be driven by a combination of zero interest rates and the classic bubble of “people not wanting to miss out”. Looks odd IMO that both stocks and precious metals are rocketing at the same time. Sure, there’s relative dollar weakness involved, but if the dollar’s weakening then what’s the underlying message?

The secret IMO is to get equity returns without too much risk. The problem remains that when a market drops it tends to take everything with it - then you need to hold your nerve and not sell in a panic. If you’re invested in the right things they should, hopefully, come back over time.

The current boom in global stock markets is beyond my understanding. I fear it may be driven by a combination of zero interest rates and the classic bubble of “people not wanting to miss out”. Looks odd IMO that both stocks and precious metals are rocketing at the same time. Sure, there’s relative dollar weakness involved, but if the dollar’s weakening then what’s the underlying message?

Yep everything is going up.

When stimulus replaces GDP and malinvestment is rife, the key is finding the real value at a reasonable price.

I still think pure agri land is a good bet as it’s not gone up with everything else... though it’s medium term value had been driven in the UK by APR.

Plus it’s recent value has likely been subdued by brexit worries, which are now largely settled.

When stimulus replaces GDP and malinvestment is rife, the key is finding the real value at a reasonable price.

I still think pure agri land is a good bet as it’s not gone up with everything else... though it’s medium term value had been driven in the UK by APR.

Plus it’s recent value has likely been subdued by brexit worries, which are now largely settled.

Looking at answering this question, pretty close to wandering in to the land of "lies, damn lies and statistics"

31/12/19 my ISA, opened 23/11/18, was up 8.99% all in. That includes shares I bed & ISA'd in, funds bought, bond ETFs bought.

31/12/20 my ISA was up 14.7% all in. That includes all the new purchases throughout 2020.

Funds, bonds & ETFs bought in 2020, up 10.65%. This would have been better if I had not chosen to start with metals around September, but they've jumped a bit in the last few days in fairness.

2021, I need to do some re-balancing as I am heavily over-exposed to the UK and USA. Bonds are likely to get punted off as they were a great idea from a "How to Own the World" angle, but really, I'm after growth not wealth preservation or income.

31/12/19 my ISA, opened 23/11/18, was up 8.99% all in. That includes shares I bed & ISA'd in, funds bought, bond ETFs bought.

31/12/20 my ISA was up 14.7% all in. That includes all the new purchases throughout 2020.

Funds, bonds & ETFs bought in 2020, up 10.65%. This would have been better if I had not chosen to start with metals around September, but they've jumped a bit in the last few days in fairness.

2021, I need to do some re-balancing as I am heavily over-exposed to the UK and USA. Bonds are likely to get punted off as they were a great idea from a "How to Own the World" angle, but really, I'm after growth not wealth preservation or income.

LeoSayer said:

How does one invest, other than errrr.... buying a field?

Yup, that's the usual method!It's a bizarre would where small pony paddocks in the right area are worth a fortune, nice houses in the right area with a few acres are worth a fortune but straightforward agri land is, say, £8k to £10k an acre. You're unlikely to get fat on it but with interest rates at 0%.....

Inevitably there arise questions like transaction costs? gates? fences? water supply? travellers? tenants? and so on. If only life was easy.

hstewie said:

hstewie said:

Well done Charlie. Perhaps you hold US businesses such as Alphabet, Tesla, Amazon etc..

The next 10 years of Tesla will be interesting to watch. Do you think the enormous market valuation now, assumes that Daimler, VW, Toyota, Ford, GM etc., might never be able to sell many electric cars?

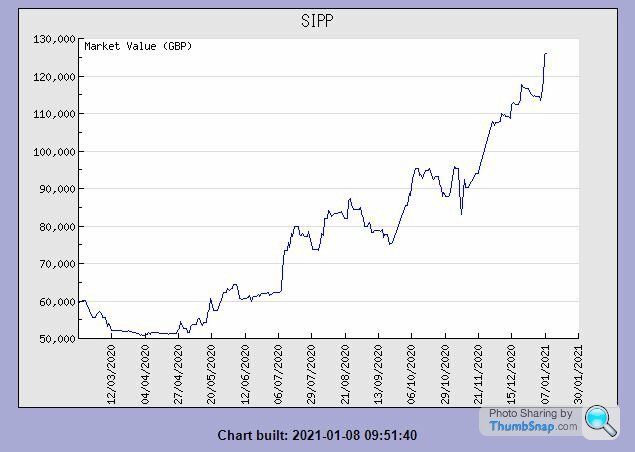

Your chart has ommited the 'exciting' early part of the 2020 calendar year.

The only big named US stock I hold is 15 Tesla, bought them after the split last year.

But the massively profitable US one for me is Enphase, I only invested in them as I use their microinverters on my roof and they've now gone into battery storage. Currently at 372% profit for me.

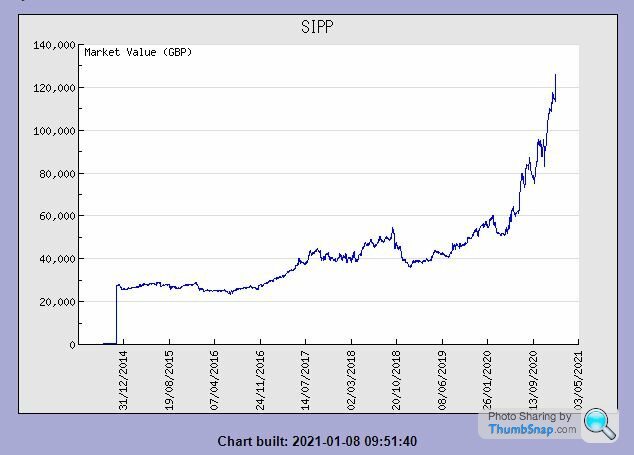

Here's the entire chart since I started in 2014. I took my various company pensions since 1994 and moved them into the SIPP after reading Robbie Burns' Naked Trader.

But the massively profitable US one for me is Enphase, I only invested in them as I use their microinverters on my roof and they've now gone into battery storage. Currently at 372% profit for me.

Here's the entire chart since I started in 2014. I took my various company pensions since 1994 and moved them into the SIPP after reading Robbie Burns' Naked Trader.

Edited by CharlieCrocodile on Friday 8th January 12:39

Gassing Station | Finance | Top of Page | What's New | My Stuff