Your questions answered Vol 2 - IM Private Clients

Discussion

Ducati996R said:

I’ve just watched some of the you tube clips ….if only I understood it all…??.looks amazing thou ,,the main man comes across very well

It is very complex however the main takeaways are:Accelerated computing-why? Because training computers to see, hear and communicate takes a lot of data and time. But why do we need it? Discovery in health/medicine, physics, logistics, heavy industry, farming, climate. Classical computers are not able to deal with these challenges due to time and energy constraints. Humans are incapable of fully understanding the human genome. It's too big! GPU systems are exponentially faster and consume considerably less energy (they are green).

And the other point about Nvidia is AI is all about the total solution. Something no other vendor has and on software they are a decade ahead. Some have a half decent chip and half decent ethernet for bandwidth but they don't have the best, neither can they scale their systems nor have CUDA libraries and with that 2M CUDA developers to lean on.

You will find the naysayers don't have any credible retort other than making sound bite comments without any support, such as GOOG and MSFT designing their own chips. Yes for very specific tasks and its an immaterial spend in the general scheme of things. GOOG/Msft/Amazon's own chips are designed to run a given model and that is it, they can't run anything else.These 3 names have spent 50B+ with Nvidia over the last 24 months and have committed to spend 2, 3 4 times as much again. Why? Because the end user(customers) demand Nvidia as it is the gold standard, their developers won't work on anything else because it works so well

Nvidia have been very smart, cementing strong relationships with every major consultancy, Accenture, PWC, SAP, Siemens-all of them. Every CSP and hyperscaler.This is then rolled out to their customers and you have pretty much global domination. So you have an ecosystem that works seamlessly and it's almost impossible to displace. How is AMD getting a look? They can't, as Jensen Huang said 'even if their chips are free, they aren't cheap enough'.

A few interesting use cases. TSMC make the most advanced chips in the world. The set up of the lithography machines to start a new run of chips takes 2 months because the algorithm is so complex they used 8,000 servers running for 30 days to calculate the mask map(sounds crazy). Today they do it in 12 hours with a few GPU systems. Saving precious time and millions in energy costs plus the giant data centre is no longer needed just a broom closet. Money saved there plus their fabs can start churning out silicon gold faster

GPUs used in visual effects(movies) rendering pipelines can increase performance by as much as 46^2 while reducing energy consumption by 5x and capital expenses by 6x.

By switching to GPUs, the industry stands to save $900 million in acquisition costs worldwide and 215 gigawatt hours in energy consumed compared with using CPU-based render farms

Given the latest autonomous system Drive-Thor has just been released and adopted by the worlds biggest OEMs and biggest robotaxi taxi wannabes and logistics companies one could speculate that if the value in Tesla is monetisation of a robotaxi fleet, could Nvidia take this out too or at least compete vigorously with Tesla in this regard? Or will Tesla capitulate and start using Nvidia silicon too, like they do with their super computers to train their network.

Edited by AdamIM on Wednesday 20th March 13:03

mikeiow said:

Sheepshanks said:

Jasey_ said:

Doesn't seem like a generous deal to me !!

It's more than you'd get risk free anywhere else, and if you're a 40% tax payer it's like getting 10%.The psychology of numbers can be curious indeed!

Simpo Two said:

I work it the other way and think that you'd be paying 40% on your 5.8%. That's assuming you're still on higher rate after you retire of course, but either way pension income is subject to income tax.

Sure. I made that point, I think? Deferring it seems to make sense if you're a higher rate tax payer now (perhaps because you're still working) but won't be later (because you've stopped working).Of course if your retirement income is so massive that you can't arrange to keep it under the higher rate threshold then I suppose you might as well take the state pension now.

Sheepshanks said:

Simpo Two said:

I work it the other way and think that you'd be paying 40% on your 5.8%. That's assuming you're still on higher rate after you retire of course, but either way pension income is subject to income tax.

Sure. I made that point, I think? Deferring it seems to make sense if you're a higher rate tax payer now (perhaps because you're still working) but won't be later (because you've stopped working).Of course if your retirement income is so massive that you can't arrange to keep it under the higher rate threshold then I suppose you might as well take the state pension now.

AdamIM said:

tight fart said:

One last question for today.

If I wish to withdraw from a IM sipp and invest into my IM ISA, do I have to withdraw the funds to my bank, or can I move them across?

Hi Richard,If I wish to withdraw from a IM sipp and invest into my IM ISA, do I have to withdraw the funds to my bank, or can I move them across?

I'll check on this and get back to you

Regards

Adam

Simpo Two said:

AdamIM said:

tight fart said:

One last question for today.

If I wish to withdraw from a IM sipp and invest into my IM ISA, do I have to withdraw the funds to my bank, or can I move them across?

Hi Richard,If I wish to withdraw from a IM sipp and invest into my IM ISA, do I have to withdraw the funds to my bank, or can I move them across?

I'll check on this and get back to you

Regards

Adam

tight fart said:

No, the sipp withdrawal would trigger the tax, just wondering if it has to be taken out of IM and sent back.

The dashboard allows 'scheme to scheme' cash transfers for everything except pensions so the answer is clearly, no, you would have to trigger the tax and make a new contribution into the alt wrapper.

AdamIM said:

Insurancejon said:

Quick question. How do I cancel a monthly direct debit instruction on an IM is a?

On the website or on my banking app?

Hi Jon,On the website or on my banking app?

On lower/footer section you will see 'Contributions'/Manage/amend contribution(link)/Cancel

Regards

Adam

I have Commercial Property in my IM Pension, I normally pay the rents into the Pension annually but I may consider paying them in monthly via DD. I have looked at the Contributions/Manage, however it gives 2 options of Personal or Employer, of which these do not meet this payment. Can you please advise which option I would need to select?

Kind regards

Alan

ajh349 said:

AdamIM said:

Insurancejon said:

Quick question. How do I cancel a monthly direct debit instruction on an IM is a?

On the website or on my banking app?

Hi Jon,On the website or on my banking app?

On lower/footer section you will see 'Contributions'/Manage/amend contribution(link)/Cancel

Regards

Adam

I have Commercial Property in my IM Pension, I normally pay the rents into the Pension annually but I may consider paying them in monthly via DD. I have looked at the Contributions/Manage, however it gives 2 options of Personal or Employer, of which these do not meet this payment. Can you please advise which option I would need to select?

Kind regards

Alan

Historical 'Rent' and other contributions have been entered with a description of a limited company-the employer so using that option would be consistent. A couple of others are showing as personal contributions.

Regards

Adam

AdamIM said:

ajh349 said:

AdamIM said:

Insurancejon said:

Quick question. How do I cancel a monthly direct debit instruction on an IM is a?

On the website or on my banking app?

Hi Jon,On the website or on my banking app?

On lower/footer section you will see 'Contributions'/Manage/amend contribution(link)/Cancel

Regards

Adam

I have Commercial Property in my IM Pension, I normally pay the rents into the Pension annually but I may consider paying them in monthly via DD. I have looked at the Contributions/Manage, however it gives 2 options of Personal or Employer, of which these do not meet this payment. Can you please advise which option I would need to select?

Kind regards

Alan

Historical 'Rent' and other contributions have been entered with a description of a limited company-the employer so using that option would be consistent. A couple of others are showing as personal contributions.

Regards

Adam

If the property is held in the SIPP then the rental payments should not be paid as "contributions". The rent is payable directly to the SIPP as the property is owned by the SIPP and is treated as an asset so the rent is a return on a holding within the SIPP not a new contribution.

Drop me a pm at nik.burrows@imprivateclients.com and I'll take look at your set up to make sure all is OK

Cheers

Nik

-Cappo- said:

-Cappo- said:

Another one here, I've been on the cusp of crossing a significantly screenshottable threshold for a few weeks now. It goes up a bit, up a bit, up a bit, up a bit, DOWN A BIT. Rinse and repeat!

The funds, they mock me....

And…..boom! Sterling work, IM The funds, they mock me....

superlightr said:

Does IM offer a tracker of the Russell 2000?

Im keen to move some funds into a small cap fund.

Hi SLIm keen to move some funds into a small cap fund.

No we don't

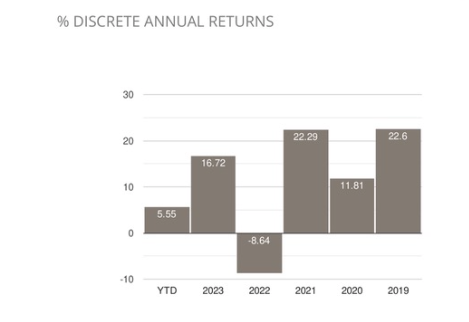

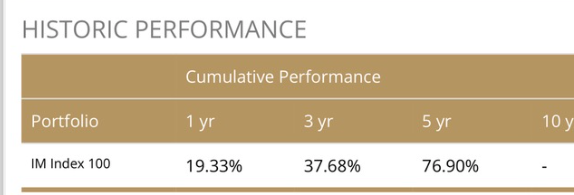

Compared to IM 100 Index as at 29/2. YTD March 22 is +8.8%

I would describe the Russell performance as, unremarkable.

Regards

Adam

Edited by AdamIM on Saturday 23 March 09:57

Thats around 12.3% compounded for 5 years cf 6.89!

Edited by AdamIM on Saturday 23 March 10:10

Edited by AdamIM on Saturday 23 March 10:11

Gassing Station | Finance | Top of Page | What's New | My Stuff