Re-mortgage now or wait?

Discussion

youngsyr said:

Great if prices always rise, ruinous if they fall.

Very few people today have experienced negative equity, that doesn't mean its impossible.

That's the risk Vs reward choice that people have to take. Exactly the same as which stocks or funds you put your pension into. Stock with the balanced safe choice of default lifestyle funds or more SIPP style exotic or volatile markets. Very few people today have experienced negative equity, that doesn't mean its impossible.

youngsyr said:

Caddyshack said:

CharlesElliott said:

Houses are the only financial leverage that most people get involved in.

If you buy a 100,000 pound house with 20% deposit, then yes, you are paying a mortgage on 80K but you also get to benefit from the rise in house prices which - in almost all long term measures - is way above the interest rate you are paying.

So once you pay off your mortgage you benefit from house price inflation, but you no longer benefit from leverage…..that is, you could probably afford a mortgage on a property much more expensive than your current property and do the same leverage trick again.

There is nothing wrong with paying off a mortgage and being debt free, it is a wonderful situation to be in. But it is not the only option.

Yes, I have often thought that I should have borrowed the max and kept doing it to later enjoy the leveraged final value before down-sizing.If you buy a 100,000 pound house with 20% deposit, then yes, you are paying a mortgage on 80K but you also get to benefit from the rise in house prices which - in almost all long term measures - is way above the interest rate you are paying.

So once you pay off your mortgage you benefit from house price inflation, but you no longer benefit from leverage…..that is, you could probably afford a mortgage on a property much more expensive than your current property and do the same leverage trick again.

There is nothing wrong with paying off a mortgage and being debt free, it is a wonderful situation to be in. But it is not the only option.

Very few people today have experienced negative equity, that doesn't mean its impossible.

Caddyshack said:

Negative equity has only ever been a timing issue so far in history. I don’t think there has ever been a time in the last 100 years when prices have been much higher than they are now, it’s all relative and a 250k house in the 60’s would have been a far bigger percentage of earnings but the inflation has always been a good thing for a well timed down-size.

Very true but short dated debt contracts change the landscape during a period of negative equity and that's the new risk that wasn't present before. During previous periods of negative equity one didn't have to care if the property value had fallen 10-20% but instead just focus on being able to maintain the repayments. Fast forward to today and suddenly borrowers on fixed deals very much have to be aware of the risk of their margin potentially being totally wiped out and needing to reload with a new deposit in order to avoid some heavy penalties, regardless of whether their income status has even improved. Plus, from a wider perspective, if we know that for the last decade getting the first deposit together has been hard and taken years, we therefore know that the chances of people getting a second together very quickly are low to zero. edc said:

youngsyr said:

Great if prices always rise, ruinous if they fall.

Very few people today have experienced negative equity, that doesn't mean its impossible.

That's the risk Vs reward choice that people have to take. Exactly the same as which stocks or funds you put your pension into. Stock with the balanced safe choice of default lifestyle funds or more SIPP style exotic or volatile markets. Very few people today have experienced negative equity, that doesn't mean its impossible.

If you buy £40k shares, the most you can lose is the £40k purchase price.

Put down £40k as a deposit on a £200k mortgage and ;et's say it's destroyed in a terroist attack (not covered by insurance). You now owe the bank £160k and you have a pile of rubble to show for the £40k you've put down.

Edited by youngsyr on Saturday 16th March 22:56

ooid said:

Well, in London terms at least, your house do not much have any value, it's the land. 200k you bought is the land value and there happens to be a pile of bricks barely inhabitable (Victorian dump) anyway...

Developers typically work to around 1/3 of the property value being the land value.So in a £200k house, you'd expect the land to be worth around £70k.

So now you have a pile of rubble worth £70k *actually less, as you'll have to pay to clear it), for which your outlay is £40k, but you also owe the bank £160k.

And the bank aren't going to be happy with you owing that much with so little security...

youngsyr said:

Developers typically work to around 1/3 of the property value being the land value.

So in a £200k house, you'd expect the land to be worth around £70k.

Thanks So in a £200k house, you'd expect the land to be worth around £70k.

I'm pretty much involved with development currently (over 1.2 billion pounds). Again, that's an over simplification. The valuations do not work like that, it is highly location sensitive as much as other development cost factors.You do not assign top down proportional value. Also mortgage (securitization) does not work like that really. Even in commercial property debt, what we see in the office market, when there is extreme shift in values(south direction), many lenders chose to delay the terms and renegotiate with borrower instead.

What you buy in London (or similar hot/attractive areas in U.K.), is mostly land not the property itself.

Mine is up in October

Currently Santander are offering me

7 year fix , 4.23%, £0 fee

5 year fix., 4.34%. £ 999 fee

2 year fix. , 4.64%. £999 fee

2 year tracker. 5.51%. £999 fee

Lifetime tracker. 5.72%. £999 fee

Ideally I want a tracker, I’ve currently 20 years remaining, 15% ltv

It was a 38 year term 5 years ago, however I’ve maxed out the annual 10% overpayments, according to man maths I could pay off the lot within 3-4 years with unlimited overpayments

Currently Santander are offering me

7 year fix , 4.23%, £0 fee

5 year fix., 4.34%. £ 999 fee

2 year fix. , 4.64%. £999 fee

2 year tracker. 5.51%. £999 fee

Lifetime tracker. 5.72%. £999 fee

Ideally I want a tracker, I’ve currently 20 years remaining, 15% ltv

It was a 38 year term 5 years ago, however I’ve maxed out the annual 10% overpayments, according to man maths I could pay off the lot within 3-4 years with unlimited overpayments

usn90 said:

, according to man maths I could pay off the lot within 3-4 years with unlimited overpayments

You could overpay, or you could use that money to speculate and then pull out once matured to pay down your mortgage.Depends on your attitude to risk, but as an example ETF's tracking S&P or FTSE are tracking (not just now but historically over any long enough timeline at double digits...

Life is one big roulette wheel 🙂

ooid said:

Well, in London terms at least, your house do not much have any value, it's the land. 200k you bought is the land value and there happens to be a pile of bricks barely inhabitable (Victorian dump) anyway...

Try explaining that to one's insurance company though!!! Never found one who appreciates that the ground doesn't present enormous risk.

youngsyr said:

edc said:

youngsyr said:

Great if prices always rise, ruinous if they fall.

Very few people today have experienced negative equity, that doesn't mean its impossible.

That's the risk Vs reward choice that people have to take. Exactly the same as which stocks or funds you put your pension into. Stock with the balanced safe choice of default lifestyle funds or more SIPP style exotic or volatile markets. Very few people today have experienced negative equity, that doesn't mean its impossible.

If you buy £40k shares, the most you can lose is the £40k purchase price.

Put down £40k as a deposit on a £200k mortgage and ;et's say it's destroyed in a terroist attack (not covered by insurance). You now owe the bank £160k and you have a pile of rubble to show for the £40k you've put down.

Edited by youngsyr on Saturday 16th March 22:56

Better blue chip equity comparison v leveraged property would be to compare a blue chip equity portfolio that is held on leverage via spreadbets.

In simple terms, resi property in the U.K. is less volatile than even defensive blue chips so you would directly compare using identical margin percentages but when considering leverage risk using a benchmark that benchmark does have to also be suitably leveraged.

In ultra simplistic and crude terms, let's double the equity margin requirement over resi property for a basic starter.

£200k property with £40k initial deposit (20%), 5% funding cost, high transaction costs, let's guess at 5% (£10k in fees,,taxes and other purchase costs) and a negative yield of several percent, let's randomly say 3. 2 yr fix.

£200k defensive blue chip U.K. equity portfolio with a 40% deposit as a spreadbet, £80k down. Funding higher at around 7-8% but entry and exit costs are all but zero, has a positive yield around 3% so a net yield around 5.

We obviously have to ignore things like a roof over one's head being an unavoidable cost, funding on the spreadbet being levied on 100% of nominal, lender default risk etc. It is, afterall, a very crude example so as to paint a better picture re leverage risk.

Both start falling in value. The equities can only fall in value due to actual transaction activity. Meanwhile, the resi property can just fall in value because lender's surveyors change their outlook. Surveyors going from being bullish and over valuing by 5+% to simply becoming more bearish and undervaluing by 5% suddenly means resi property has randomly fallen 10% for no other reason than the consensus whim of the people to guess a rough number to help underpin the lender's risk profile. But both markets fall by 10%, or £20k. And this is the bit that I'm really not sure many mortgage holders technically appreciate: that £20k is worn 100% by the person holding the asset. It nets off directly against the deposit they put down.

The equity holder must pay in more margin as the stock values decline. Maintaining the margin at 40% of current can be a toxic shock if the market were to crash suddenly but in most cases it's a slow trend that requires regular margin to ups that are manageable.

The property holder actually notices nothing at first. Nothing actually changes for them initially as their remargining points aren't end of day, mark to market but set by terms of the discounted fix agreement where they've accepted a fixed funding rate in exchange for taking on certain other risks. One of those risks being that in 2 years time they will be remargined and if they fail to maintain their margin will be charged a higher premium to possibly being charged the SVR which isn't even a real financial product but a sales tool to encourage the taking of fixed deals, to worse, being put into special measures, default light where they get to still live in the property and pay huge costs but they aren't buying that property any longer and are in reality trapped tenants at the mercy of the lender who now really does own the property. At the point of contract rollover, the asset is now valued at £180k, the initial deposit has been cut in half from £40k to £20k so the LTV has gone from 80% to 89% which we know will be rounded to 90%. In order for the mortgage holder to maintain the lower fix rate on the rollover they must reload their margin back to 20% so find a fresh £16k cash to send to the lender. Or they don't and rollover on less competitive terms regardless of the state of their income and personal security.

If we consider a 20% drop across 5 years and the mortgage being a 5 year fix secured with a 20% deposit then we start to see a bigger potential risk. At the point of contract rollover there is no initial deposit remaining. It has all been lost by the falling value of the asset. The mortgage holder if they cannot conjure up a completely fresh deposit, even the smallest possible to try and obtain even the most basic of deals then it's off to the farm for them, it's technically game over. It's cash out and agree terms on how to settle the inevitable negative balance after transaction costs or bend over for milking for the end of days.

Their only hope would be that God, nee Westminster, randomly steps in to save them from descending to the lowest of the 7 rings of hell.

Before the days of the 'fix' which has given lenders the power to remargin their risk book on a short term basis which in turn gives the bonds a better credit rating, which in turn, allows for more lending business to be written and on lower margins, which technically increases the default risk as we all know few mortgage holders can pluck tens of thousands out of thin air because as the lender we already know they're worth f

k all because they've had to opt for a low deposit lend. There lies a separate madness in the market that to make the bonds lower risk one increases the risk of the constituent debts. Anyway, in the days before the fix it was arguably really smart and prudent to just over pay the mortgage directly if permitted to do so, post fix I'm not convinced this is such a smart idea. I would prefer to book the overpayments to an account in my name and under my control until such a time that it's value was at least equivalent to a fresh deposit on the property or until the LTV had come close to 50% or even under 70% still removes the worst of the risk. Once that security blanket was in place or the LTV been reduced significantly by asset inflation then I'd consider sending the overpayment directly to the lender.

k all because they've had to opt for a low deposit lend. There lies a separate madness in the market that to make the bonds lower risk one increases the risk of the constituent debts. Anyway, in the days before the fix it was arguably really smart and prudent to just over pay the mortgage directly if permitted to do so, post fix I'm not convinced this is such a smart idea. I would prefer to book the overpayments to an account in my name and under my control until such a time that it's value was at least equivalent to a fresh deposit on the property or until the LTV had come close to 50% or even under 70% still removes the worst of the risk. Once that security blanket was in place or the LTV been reduced significantly by asset inflation then I'd consider sending the overpayment directly to the lender. I'm always overly cautious when it comes to these life defining risks as the my view is that the odds aren't actually relevant when the well-being of you and the family and how you will live the rest of your life is at stake. Russian Roulette is still Russian Roulette whether the pistol has 6 chambers or 600. And of course, I have massively overly simplified things but I really don't think many mortgage holders genuinely understand leverage. Few leverage traders even understand it which is why they almost all, to a person, always lose and why we just don't bother hedging their positions other than to manage our own concentration risk.

In commercial real estate debt 'a cash trap' also plays role before default for further protect?on. The lender keeping a side specific amount to protect the principal payments in the event of massive valuation changes and that secured amount can help the re*finance for the borrower. One can simply put a self insurance for an home asset value. (as much as you can afford). There are already insurance products keeping the building anyway or mortgage payments insured such as critical life and etc.

Whilst I appreciate negative equity can strike anywhere, it's really only likely to be a terminal issue in places where NRAM mortgages were popular and people kept remortgaging to buy rubbish, tat and the wife a boob job.

If you managed to get a NRAM mortgage in a desirable area of London back in the day-we'll done you won the lottery. If you did it on a 2 up 2 down in Peterlee or hartlepool, well, that's a shame.

Bottom line is that most people have the option of a product transfer where there isn't a full underwriting process applied, and I am sure that unless the property is in some godforsaken st hole the bank will value it at roughly whatever you paid originally. Yes exceptions apply but I doubt a lot of people other than utter idiots buying sub prime rubbish get caught out.

If you managed to get a NRAM mortgage in a desirable area of London back in the day-we'll done you won the lottery. If you did it on a 2 up 2 down in Peterlee or hartlepool, well, that's a shame.

Bottom line is that most people have the option of a product transfer where there isn't a full underwriting process applied, and I am sure that unless the property is in some godforsaken s

t hole the bank will value it at roughly whatever you paid originally. Yes exceptions apply but I doubt a lot of people other than utter idiots buying sub prime rubbish get caught out. ooid said:

youngsyr said:

Developers typically work to around 1/3 of the property value being the land value.

So in a £200k house, you'd expect the land to be worth around £70k.

Thanks So in a £200k house, you'd expect the land to be worth around £70k.

I'm pretty much involved with development currently (over 1.2 billion pounds). Again, that's an over simplification. The valuations do not work like that, it is highly location sensitive as much as other development cost factors.You do not assign top down proportional value. Also mortgage (securitization) does not work like that really. Even in commercial property debt, what we see in the office market, when there is extreme shift in values(south direction), many lenders chose to delay the terms and renegotiate with borrower instead.

What you buy in London (or similar hot/attractive areas in U.K.), is mostly land not the property itself.

youngsyr said:

Apologies, but I didn't mention London (or similar hot/attractive areas in the UK), you did. I thought that would be clear considering we are talking about house prices of £200k.

Your post was in response to one about London so thanks for the clarification

youngsyr said:

ooid said:

Well, in London terms at least, your house do not much have any value, it's the land. 200k you bought is the land value and there happens to be a pile of bricks barely inhabitable (Victorian dump) anyway...

Developers typically work to around 1/3 of the property value being the land value.So in a £200k house, you'd expect the land to be worth around £70k.

So now you have a pile of rubble worth £70k *actually less, as you'll have to pay to clear it), for which your outlay is £40k, but you also owe the bank £160k.

And the bank aren't going to be happy with you owing that much with so little security...

Caddyshack said:

There are conspiracy theory threads in other places on PH.

Even if there was a collapse, the wealthy would get the money back and the poor would be poor again, humans are creatures of habit.

I don't disagree, I was playing devil's advocate in regard to the question of what is the financial argument against buying a bigger house with more borrowing, as long as you can afford it, vs paying it off and being debt free. Even if there was a collapse, the wealthy would get the money back and the poor would be poor again, humans are creatures of habit.

I do however think that there are now too many people discussing where the dollar will be in the future? Will a BRICS backed currency be a true contender? And if the dollar does have a serious fall from grace what will happen? To simply say this is conspiracy theories, it is people asking what the worst case scenario could be.

Will it happen? I doubt it.

I agree with your later comment, why not borrow as much as you can in the early years? Especially when there were more interest only products and self cert etc.

I wish I had stretched myself more.

My best mate did this, kept pushing himself to the limit with interest only products in Kensington, started in Notting Hill when you could still buy something for a reasonable sum in the 90s, and now, he's in a beautiful £2.5m 16th century place just outside Bath.

It has two rentals on the grounds and stables, the income from those will have it all paid off in 12 years, and he has only started paying off the capital for the first time last year, (obviously lots of equity built up from the constant upgrading through the years) he has just turned 50.

He is now at the point where he is converting one of the old outbuildings and says he will probably end up retiring into that place, either rent or sell the rest off.

I don't think it would be as easy to do that today with the products available? But I don't know, maybe it is?

Some rate decreases from NatWest - https://theintermediary.co.uk/2024/03/natwest-make...

22 said:

youngsyr said:

Apologies, but I didn't mention London (or similar hot/attractive areas in the UK), you did. I thought that would be clear considering we are talking about house prices of £200k.

Your post was in response to one about London so thanks for the clarification youngsyr said:

ooid said:

Well, in London terms at least, your house do not much have any value, it's the land. 200k you bought is the land value and there happens to be a pile of bricks barely inhabitable (Victorian dump) anyway...

Developers typically work to around 1/3 of the property value being the land value.So in a £200k house, you'd expect the land to be worth around £70k.

So now you have a pile of rubble worth £70k *actually less, as you'll have to pay to clear it), for which your outlay is £40k, but you also owe the bank £160k.

And the bank aren't going to be happy with you owing that much with so little security...

usn90 said:

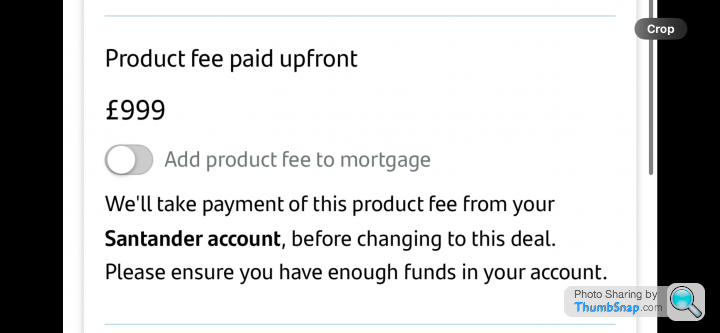

I’m about to lock in a tracker deal with Santander, my current deal ends in October.

The £999 product fee, will I pay this now or around the time my current deal expires,

Normally when the product starts, I would never give a lender the money before the deal…you may want to pull out last minute and then you have the hassle of recovering the money. If you add it to the loan you then have the luxury of as much time as you like to pay it off after completion. Just pay it soon after the mortgage starts, just like any other mortgage overpayment.The £999 product fee, will I pay this now or around the time my current deal expires,

Gassing Station | Finance | Top of Page | What's New | My Stuff