Re-mortgage now or wait?

Discussion

usn90 said:

I’m about to lock in a tracker deal with Santander, my current deal ends in October.

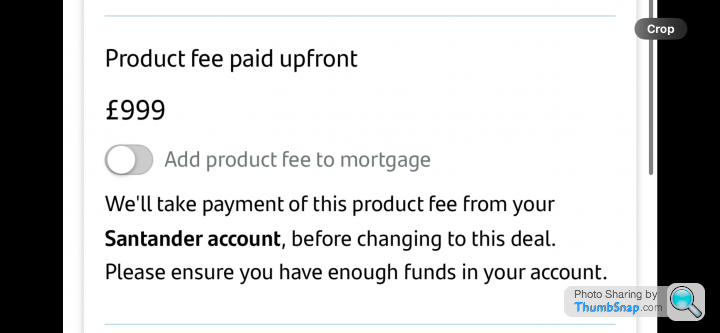

The £999 product fee, will I pay this now or around the time my current deal expires,

Normally when the product starts, I would never give a lender the money before the deal…you may want to pull out last minute and then you have the hassle of recovering the money. If you add it to the loan you then have the luxury of as much time as you like to pay it off after completion. Just pay it soon after the mortgage starts, just like any other mortgage overpayment.The £999 product fee, will I pay this now or around the time my current deal expires,

Caddyshack said:

Normally when the product starts, I would never give a lender the money before the deal…you may want to pull out last minute and then you have the hassle of recovering the money. If you add it to the loan you then have the luxury of as much time as you like to pay it off after completion. Just pay it soon after the mortgage starts, just like any other mortgage overpayment.

So if I add the fee to the loan, the first £999+ overpayment I make in effect paying off the fee?Makes sense after writing it I guess

usn90 said:

So if I add the fee to the loan, the first £999+ overpayment I make in effect paying off the fee?

Makes sense after writing it I guess

Day one of the transferring over to the new rate, pay off £999.......saves paying it upfront, has the same effect on your mortgage balance......although technically it eats into your 10% overpayment allowance......Makes sense after writing it I guess

Sarnie said:

Day one of the transferring over to the new rate, pay off £999.......saves paying it upfront, has the same effect on your mortgage balance......although technically it eats into your 10% overpayment allowance......

Not in the case of the tracker which has unlimited overpayments.So there’s zero reason to pay it any earlier in that case

usn90 said:

Just before I accept the offer

I realise I can change to a better deal before October should one come along.

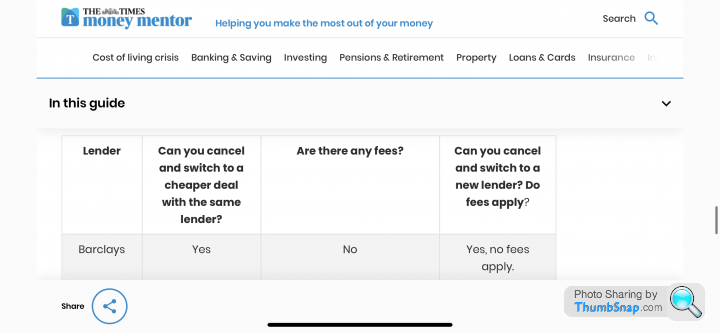

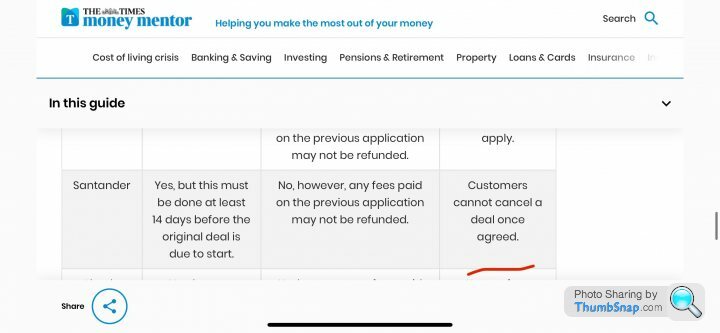

But what if that deal is with another lender, can I still cancel the Santander deal and remortgage with a new lender with no penalty?

Yes you can as the contract hadn’t started I realise I can change to a better deal before October should one come along.

But what if that deal is with another lender, can I still cancel the Santander deal and remortgage with a new lender with no penalty?

craigjm said:

usn90 said:

Just before I accept the offer

I realise I can change to a better deal before October should one come along.

But what if that deal is with another lender, can I still cancel the Santander deal and remortgage with a new lender with no penalty?

Yes you can as the contract hadn’t started I realise I can change to a better deal before October should one come along.

But what if that deal is with another lender, can I still cancel the Santander deal and remortgage with a new lender with no penalty?

There is a new product out with Accord which works on a £5,000 deposit for purchases up to £500k, this can be a 95% mortgage or 99% mortgage. It must fit within 4.49 income multiple.

It is not a remortgage but I thought it would be an interesting subject:

Who's it for?

At least one applicant must be a first time buyer (defined as never having owned a property in the past) and no background properties on the application

Applicants with a minimum £5K deposit

Applications that achieve the higher credit score required for lending above 95% LTV

How does it work?

The good news is you don’t need to do anything differently. Simply visit our website to use our online affordability calculator and submit your DIP as normal - MSO will do the rest. You just need to ensure your client meets the eligibility requirements.

What else do you need to know?

5 Year Fixed Rate product

Maximum age of 70 at the end of the mortgage term

Available for LTVs between 95.01% LTV and 99% LTV

Available for house purchases above £100K up to £500K

Minimum loan above £95K

Maximum loan £495K

Maximum LTI 4.49

Only available for Capital & Interest

Available for new house purchase business only

Subject to affordability, criteria and credit score

In line with Consumer Duty requirements, Accord’s Fair Value Assessment in regard to Residential First Time Buyers has been updated.

Excludes:

Purchases of flats, new builds and properties in Northern Ireland

Not available for applications where any applicant does not have permanent right to reside in the UK

It is not a remortgage but I thought it would be an interesting subject:

Who's it for?

At least one applicant must be a first time buyer (defined as never having owned a property in the past) and no background properties on the application

Applicants with a minimum £5K deposit

Applications that achieve the higher credit score required for lending above 95% LTV

How does it work?

The good news is you don’t need to do anything differently. Simply visit our website to use our online affordability calculator and submit your DIP as normal - MSO will do the rest. You just need to ensure your client meets the eligibility requirements.

What else do you need to know?

5 Year Fixed Rate product

Maximum age of 70 at the end of the mortgage term

Available for LTVs between 95.01% LTV and 99% LTV

Available for house purchases above £100K up to £500K

Minimum loan above £95K

Maximum loan £495K

Maximum LTI 4.49

Only available for Capital & Interest

Available for new house purchase business only

Subject to affordability, criteria and credit score

In line with Consumer Duty requirements, Accord’s Fair Value Assessment in regard to Residential First Time Buyers has been updated.

Excludes:

Purchases of flats, new builds and properties in Northern Ireland

Not available for applications where any applicant does not have permanent right to reside in the UK

Caddyshack said:

There is a new product out with Accord which works on a £5,000 deposit for purchases up to £500k, this can be a 95% mortgage or 99% mortgage. It must fit within 4.49 income multiple.

What's the interest rate(s)?The news made it seem like it was a govt scheme rather than one lender, but I wasn't listening that carefully. (They also neglected the interest rate)

My concern would be negative equity. But probably better than renting over the long term. Lack of deposit needed is a big draw to those living with parents struggling to raise 20/30/40/50k

johnboy1975 said:

Caddyshack said:

There is a new product out with Accord which works on a £5,000 deposit for purchases up to £500k, this can be a 95% mortgage or 99% mortgage. It must fit within 4.49 income multiple.

What's the interest rate(s)?The news made it seem like it was a govt scheme rather than one lender, but I wasn't listening that carefully. (They also neglected the interest rate)

My concern would be negative equity. But probably better than renting over the long term. Lack of deposit needed is a big draw to those living with parents struggling to raise 20/30/40/50k

craigjm said:

johnboy1975 said:

Caddyshack said:

There is a new product out with Accord which works on a £5,000 deposit for purchases up to £500k, this can be a 95% mortgage or 99% mortgage. It must fit within 4.49 income multiple.

What's the interest rate(s)?The news made it seem like it was a govt scheme rather than one lender, but I wasn't listening that carefully. (They also neglected the interest rate)

My concern would be negative equity. But probably better than renting over the long term. Lack of deposit needed is a big draw to those living with parents struggling to raise 20/30/40/50k

Caddyshack said:

craigjm said:

johnboy1975 said:

Caddyshack said:

There is a new product out with Accord which works on a £5,000 deposit for purchases up to £500k, this can be a 95% mortgage or 99% mortgage. It must fit within 4.49 income multiple.

What's the interest rate(s)?The news made it seem like it was a govt scheme rather than one lender, but I wasn't listening that carefully. (They also neglected the interest rate)

My concern would be negative equity. But probably better than renting over the long term. Lack of deposit needed is a big draw to those living with parents struggling to raise 20/30/40/50k

Caddyshack said:

craigjm said:

johnboy1975 said:

Caddyshack said:

There is a new product out with Accord which works on a £5,000 deposit for purchases up to £500k, this can be a 95% mortgage or 99% mortgage. It must fit within 4.49 income multiple.

What's the interest rate(s)?The news made it seem like it was a govt scheme rather than one lender, but I wasn't listening that carefully. (They also neglected the interest rate)

My concern would be negative equity. But probably better than renting over the long term. Lack of deposit needed is a big draw to those living with parents struggling to raise 20/30/40/50k

DonkeyApple said:

Caddyshack said:

craigjm said:

johnboy1975 said:

Caddyshack said:

There is a new product out with Accord which works on a £5,000 deposit for purchases up to £500k, this can be a 95% mortgage or 99% mortgage. It must fit within 4.49 income multiple.

What's the interest rate(s)?The news made it seem like it was a govt scheme rather than one lender, but I wasn't listening that carefully. (They also neglected the interest rate)

My concern would be negative equity. But probably better than renting over the long term. Lack of deposit needed is a big draw to those living with parents struggling to raise 20/30/40/50k

I can see this being attractive to young professionals on the way up with income etc.

ooid said:

Excluding flats a bit OTT.

Quite weird assumptions

Property type:House

Purchase price:500k

Deposit:5k

Credit score:High

Rates: >5.99

Love to see who fits into this?

I think flats can be a bit more volatile on pricing and have ground rent and service charges to consider.Quite weird assumptions

Property type:House

Purchase price:500k

Deposit:5k

Credit score:High

Rates: >5.99

Love to see who fits into this?

You can get a 3 bed semi near me for 500k

I would think a young professional couple would fit that quite well.

Gassing Station | Finance | Top of Page | What's New | My Stuff