Child Benefit Tax Charge

Discussion

Hypothetically speaking, if by the time January 2025 came around, and you had forgotten to file for 23-24 tax year (where you are due to pay some Child Benefit back for the first time) because you were now under the threshold in 24-25, what would the expected consequences be?

I assume HMRC would pick it up and punish you accordingly? Would punishment just be paying back what you owe or would there be penalties involved?

I assume HMRC would pick it up and punish you accordingly? Would punishment just be paying back what you owe or would there be penalties involved?

Beethree said:

Hypothetically speaking, if by the time January 2025 came around, and you had forgotten to file for 23-24 tax year (where you are due to pay some Child Benefit back for the first time) because you were now under the threshold in 24-25, what would the expected consequences be?

I assume HMRC would pick it up and punish you accordingly? Would punishment just be paying back what you owe or would there be penalties involved?

I am in the (un)fortunate position where for the first time (23/24) I am not entitled to receive any child benefit payment. I believe from reading this thread and discussions with colleagues who have ended up in similar situations that it's just a case of paying back what you owe. (In my case 100%) and I believe that you have the option of having your tax code modified to allow for this, or paying in a lump sum.I assume HMRC would pick it up and punish you accordingly? Would punishment just be paying back what you owe or would there be penalties involved?

So if this new rule comes in with the new tax year and you become entitled to keep some again, when is the best time to re-apply?

Could you make your first payment in April and get it to include 12 weeks backdated? I guess not but it would technically all be paid in the 24/25 tax year. You've technically been eligible for child benefit all year, just opted not to receive it.

Could you make your first payment in April and get it to include 12 weeks backdated? I guess not but it would technically all be paid in the 24/25 tax year. You've technically been eligible for child benefit all year, just opted not to receive it.

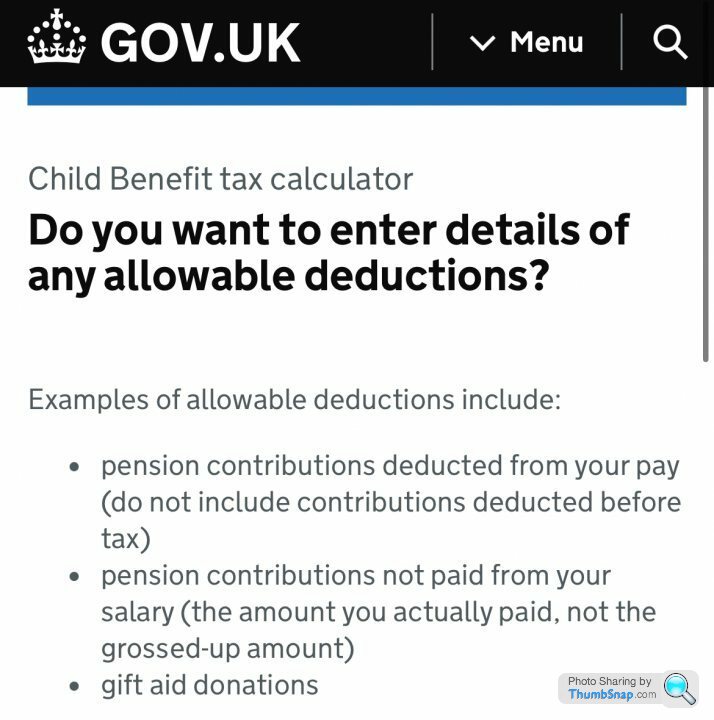

When trying to work out how much of the charge I'd be exposed to this year I did a bit of digging. The calculator on the gov.uk website states the following:

So I took the gross values for my:

Base salary

Shift allowance

Bonus

Overtime

Medical Care Benefit

I then subtracted the following Salary Sacrifice items:

5% Pension Contribution

2.5% Voluntary Pension Contribution

Additional Annual Leave Purchase

Cycle to Work Voucher

I also salary sacrifice £1800 per annum to a company Share Incentive Plan, however at the time I phoned HMRC and was told that this would not be included in the calculation for HICBC as technically I was still receiving the payment - but just investing it instead. However it definitely reflects in the 'taxable pay' on my Payslip. Can anyone who has gone through the self assessment process either confirm or deny this?

This year I'm having to pay it all back, and as such I have (just last week) cancelled the payment. however with the good news from today's budget I can reinstate the payment and then see what else I can sacrifice to minimise the charge going forward - just trying to confirm what is definitely deductible.

So I took the gross values for my:

Base salary

Shift allowance

Bonus

Overtime

Medical Care Benefit

I then subtracted the following Salary Sacrifice items:

5% Pension Contribution

2.5% Voluntary Pension Contribution

Additional Annual Leave Purchase

Cycle to Work Voucher

I also salary sacrifice £1800 per annum to a company Share Incentive Plan, however at the time I phoned HMRC and was told that this would not be included in the calculation for HICBC as technically I was still receiving the payment - but just investing it instead. However it definitely reflects in the 'taxable pay' on my Payslip. Can anyone who has gone through the self assessment process either confirm or deny this?

This year I'm having to pay it all back, and as such I have (just last week) cancelled the payment. however with the good news from today's budget I can reinstate the payment and then see what else I can sacrifice to minimise the charge going forward - just trying to confirm what is definitely deductible.

Here's a useful link if you want to see how todays budget effects you financially going in to the next tax year.

Supposedly I'm going to be better off by about £3000, remains to be seen!

https://www.telegraph.co.uk/money/tax/income/tax-c...

Supposedly I'm going to be better off by about £3000, remains to be seen!

https://www.telegraph.co.uk/money/tax/income/tax-c...

John3l said:

When trying to work out how much of the charge I'd be exposed to this year I did a bit of digging. The calculator on the gov.uk website states the following:

So I took the gross values for my:

Base salary

Shift allowance

Bonus

Overtime

Medical Care Benefit

I then subtracted the following Salary Sacrifice items:

5% Pension Contribution

2.5% Voluntary Pension Contribution

Additional Annual Leave Purchase

Cycle to Work Voucher

I also salary sacrifice £1800 per annum to a company Share Incentive Plan, however at the time I phoned HMRC and was told that this would not be included in the calculation for HICBC as technically I was still receiving the payment - but just investing it instead. However it definitely reflects in the 'taxable pay' on my Payslip. Can anyone who has gone through the self assessment process either confirm or deny this?

This year I'm having to pay it all back, and as such I have (just last week) cancelled the payment. however with the good news from today's budget I can reinstate the payment and then see what else I can sacrifice to minimise the charge going forward - just trying to confirm what is definitely deductible.

I reckon they're wrong on the share thing. It's salary sacrifice. No different to the pension really (you've just invested it in a different "wrapper").So I took the gross values for my:

Base salary

Shift allowance

Bonus

Overtime

Medical Care Benefit

I then subtracted the following Salary Sacrifice items:

5% Pension Contribution

2.5% Voluntary Pension Contribution

Additional Annual Leave Purchase

Cycle to Work Voucher

I also salary sacrifice £1800 per annum to a company Share Incentive Plan, however at the time I phoned HMRC and was told that this would not be included in the calculation for HICBC as technically I was still receiving the payment - but just investing it instead. However it definitely reflects in the 'taxable pay' on my Payslip. Can anyone who has gone through the self assessment process either confirm or deny this?

This year I'm having to pay it all back, and as such I have (just last week) cancelled the payment. however with the good news from today's budget I can reinstate the payment and then see what else I can sacrifice to minimise the charge going forward - just trying to confirm what is definitely deductible.

Those share schemes are quite rigid with when you can take money out and not get taxed for exactly this reason.

I ended up doing really well out of one a few years ago as the parent company (whose shares I had been buying) sold the company I worked for. This meant I could take the money out tax free - worked out brilliantly!

Milner993 said:

Here's a useful link if you want to see how todays budget effects you financially going in to the next tax year.

Supposedly I'm going to be better off by about £3000, remains to be seen!

https://www.telegraph.co.uk/money/tax/income/tax-c...

£2600 for me which I think is the max possible saving on the NI cuts for two people. Supposedly I'm going to be better off by about £3000, remains to be seen!

https://www.telegraph.co.uk/money/tax/income/tax-c...

FreeLitres said:

On BBC news, they just did a piece on the budget and a nurse in Newcastle said that when she works unsociable hours, her pay goes above the £50k threshold so she welcomes the changes.

Nurse... in Newcastle... £50k...

Is this normal?

Unsociable hours and a bit of overtime, probably pretty easy. Nurse... in Newcastle... £50k...

Is this normal?

John3l said:

Beethree said:

Hypothetically speaking, if by the time January 2025 came around, and you had forgotten to file for 23-24 tax year (where you are due to pay some Child Benefit back for the first time) because you were now under the threshold in 24-25, what would the expected consequences be?

I assume HMRC would pick it up and punish you accordingly? Would punishment just be paying back what you owe or would there be penalties involved?

I am in the (un)fortunate position where for the first time (23/24) I am not entitled to receive any child benefit payment. I believe from reading this thread and discussions with colleagues who have ended up in similar situations that it's just a case of paying back what you owe. (In my case 100%) and I believe that you have the option of having your tax code modified to allow for this, or paying in a lump sum.I assume HMRC would pick it up and punish you accordingly? Would punishment just be paying back what you owe or would there be penalties involved?

Unless I missed something I wasn't given the lump sum option (probably wouldn't have had it available to just do that anyway) and the system told me they have applied an adjustmemt to my tax code for the 24/25 tax year.

I actually did my SA for 22/23 as soon as I could in the hope that my tax code would change immediately and the repaying process could start immediately in 23/24 to get it over and done with. Was a little surprised when it said it would take effect from the start of the following tax year.

FreeLitres said:

On BBC news, they just did a piece on the budget and a nurse in Newcastle said that when she works unsociable hours, her pay goes above the £50k threshold so she welcomes the changes.

Nurse... in Newcastle... £50k...

Is this normal?

Nurse is quite a vague job description, there's alot roles you can put under that word. Entirely possible. Nurse... in Newcastle... £50k...

Is this normal?

FreeLitres said:

On BBC news, they just did a piece on the budget and a nurse in Newcastle said that when she works unsociable hours, her pay goes above the £50k threshold so she welcomes the changes.

Nurse... in Newcastle... £50k...

Is this normal?

It's after pension conributions as well, I think NHS employee contributions are 9 or 10% so she earns more than 50kNurse... in Newcastle... £50k...

Is this normal?

Nurses are professionally qualified people so they can earn very good money (and quite rightly too). Here's a pay scale indicator which gives a good idea as to how high a nurse's salary can go if he/she has the required experience -

https://www.nurses.co.uk/careers-hub/nursing-pay-g...

https://www.nurses.co.uk/careers-hub/nursing-pay-g...

Average pay for a nurse with 5 years experience is £35-38k. A senior nurse that has got 5-6 years experience is on over £40k. If some of the hours they work are unsocial then the pay is boosted 30-60% for those shifts. Overtime is time and a half. More if they work as agency.

If they work in inner London then there an extra 20% (with an upper and lower cap.)

Achievable to earn alot of money if you want it.

I'm my industry the basic is £55k, no extra money for unsociable or location but time and a half for overtime and people earn into the £80ks.

1 day a month extra gets me £4.8k a year, some do 10 days a month (we only work 14-15 days a month), although they don't sustain that pace for the year.

If they work in inner London then there an extra 20% (with an upper and lower cap.)

Achievable to earn alot of money if you want it.

I'm my industry the basic is £55k, no extra money for unsociable or location but time and a half for overtime and people earn into the £80ks.

1 day a month extra gets me £4.8k a year, some do 10 days a month (we only work 14-15 days a month), although they don't sustain that pace for the year.

Edited by Hondashark on Thursday 7th March 08:14

My wife and I had a baby at the end of January so was looking into Child benefits and was a bit annoyed that as I earn somewhere between 50-60K based on bonuses that I would have had to pay back a far chunk even though my wife isn't working now. So this is a very welcome change! I'm about to apply for the benefit now that our baby is registered and i'm aware it is back dated to birth for up to 3 months. Will I have to do a self assessment on those 2 months between birth and the start of the new financial year?

Strictly speaking, yes as you will be entitled to SOME Child Benefit for 2023/24 but not ALL of it.

A phone call to HMRC might allow you to escape actually having to sign up for Self Assessment just to make the adjustment for 2023/24. HMRC has gathered up almost 1 million extra Self Assessment tax returns entirely due to the CBC (Child Benefit Charge).

George Osborne - don't you just love him.

A phone call to HMRC might allow you to escape actually having to sign up for Self Assessment just to make the adjustment for 2023/24. HMRC has gathered up almost 1 million extra Self Assessment tax returns entirely due to the CBC (Child Benefit Charge).

George Osborne - don't you just love him.

blank said:

John3l said:

When trying to work out how much of the charge I'd be exposed to this year I did a bit of digging. The calculator on the gov.uk website states the following:

So I took the gross values for my:

Base salary

Shift allowance

Bonus

Overtime

Medical Care Benefit

I then subtracted the following Salary Sacrifice items:

5% Pension Contribution

2.5% Voluntary Pension Contribution

Additional Annual Leave Purchase

Cycle to Work Voucher

I also salary sacrifice £1800 per annum to a company Share Incentive Plan, however at the time I phoned HMRC and was told that this would not be included in the calculation for HICBC as technically I was still receiving the payment - but just investing it instead. However it definitely reflects in the 'taxable pay' on my Payslip. Can anyone who has gone through the self assessment process either confirm or deny this?

This year I'm having to pay it all back, and as such I have (just last week) cancelled the payment. however with the good news from today's budget I can reinstate the payment and then see what else I can sacrifice to minimise the charge going forward - just trying to confirm what is definitely deductible.

I reckon they're wrong on the share thing. It's salary sacrifice. No different to the pension really (you've just invested it in a different "wrapper").So I took the gross values for my:

Base salary

Shift allowance

Bonus

Overtime

Medical Care Benefit

I then subtracted the following Salary Sacrifice items:

5% Pension Contribution

2.5% Voluntary Pension Contribution

Additional Annual Leave Purchase

Cycle to Work Voucher

I also salary sacrifice £1800 per annum to a company Share Incentive Plan, however at the time I phoned HMRC and was told that this would not be included in the calculation for HICBC as technically I was still receiving the payment - but just investing it instead. However it definitely reflects in the 'taxable pay' on my Payslip. Can anyone who has gone through the self assessment process either confirm or deny this?

This year I'm having to pay it all back, and as such I have (just last week) cancelled the payment. however with the good news from today's budget I can reinstate the payment and then see what else I can sacrifice to minimise the charge going forward - just trying to confirm what is definitely deductible.

Those share schemes are quite rigid with when you can take money out and not get taxed for exactly this reason.

I ended up doing really well out of one a few years ago as the parent company (whose shares I had been buying) sold the company I worked for. This meant I could take the money out tax free - worked out brilliantly!

When I was a Practice Manager in a GP Practice the accountants always recommended GPs claim for child benefit and pay the money back, because of eventualities like the budget yesterday, getting credit for the pensionable pay of a non working partner or if tragedy struck and them having to stop work It isnt always easy to get government systems to reinstate things afterwards.

They didn't have to budget to the same extent as some on this thread as they were way over any thresholds to mitigate not paying it back, but they very much actively refused work that put them over the 40% tax bracket. The tax tail wagging the dog.

I kind of wish our tax law didn't have these stupid anomalies as so much effort goes into thinking of ways not to pay or keeping below a threshold, when that time could be spent on being more productive and flying well past them.

We are too busy staying below thresholds leading to perverse disincentives throttling productivity, promotions and the tax take.

A trawl of HMRC databases would probably show disproportionate pooling of tax payments around thresholds.

They didn't have to budget to the same extent as some on this thread as they were way over any thresholds to mitigate not paying it back, but they very much actively refused work that put them over the 40% tax bracket. The tax tail wagging the dog.

I kind of wish our tax law didn't have these stupid anomalies as so much effort goes into thinking of ways not to pay or keeping below a threshold, when that time could be spent on being more productive and flying well past them.

We are too busy staying below thresholds leading to perverse disincentives throttling productivity, promotions and the tax take.

A trawl of HMRC databases would probably show disproportionate pooling of tax payments around thresholds.

Gassing Station | Finance | Top of Page | What's New | My Stuff