Car finance - hidden commission payments

Discussion

MB Finance got back to me and said

MB Finance said:

Thank you for your email asking for confirmation of whether we paid the dealer a discretionary commission for your introduction to us.

After checking our records, we can tell you that we did pay a scaled discretionary commission to the dealer. We'll treat your email as your complaint, unless otherwise advised by you. We normally have eight weeks to send you a final response letter, but the pause introduced by the Financial Conduct Authority (FCA) means the period starting on 11 January 2024 and ending on (and including) 25 September 2024 is not counted when calculating this eight week period.

So they have up to 8 weeks after September 25 to respond I take it ?After checking our records, we can tell you that we did pay a scaled discretionary commission to the dealer. We'll treat your email as your complaint, unless otherwise advised by you. We normally have eight weeks to send you a final response letter, but the pause introduced by the Financial Conduct Authority (FCA) means the period starting on 11 January 2024 and ending on (and including) 25 September 2024 is not counted when calculating this eight week period.

axel1990chp said:

I had a physical letter arrive in the post yesterday from Black Horse, requesting all the information I have already given them in the email to be sent to them via email…

Strangely enough, it is addressed to the address in question, states me by name in the letter, and also references my vehicle and registration on it too.

Are they trying to pull a fast one and hope people “fail to respond to our correspondence” so they can worm out of any potential future claims?

I’ll send it this eve, just to be sure, again.

Id imagine it’s stop a claims management company claiming on your behalf, or if there is/was a risk that the dealers database had been hacked.Strangely enough, it is addressed to the address in question, states me by name in the letter, and also references my vehicle and registration on it too.

Are they trying to pull a fast one and hope people “fail to respond to our correspondence” so they can worm out of any potential future claims?

I’ll send it this eve, just to be sure, again.

Random_Person said:

I have still not even had an acknowledgement of the 4 emails I sent of almost 3 weeks ago.

ML’s advice was not to worry about that particularly although it does seem a bit strange that you didn’t even get an auto reply?With the 2 that I only got an auto reply ( 28 days time etc ) to I did in fact resend with a placating couple of added lines.

OddCat said:

To those who actually arranged car finance in a dealership, were these "you can have a discount but only if you take the finance" deals real ?

Did people really only get a discount if they took the finance and people who paid 'cash' paid more ?

I got 2k off a car and kept the finance 6 months paying it off. Still paid a bit of interest but sod all.Did people really only get a discount if they took the finance and people who paid 'cash' paid more ?

Wifes car we got 3 years servicing if we took finance - cleared it on the 3rd month cost like £20 in interest .

OddCat said:

To those who actually arranged car finance in a dealership, were these "you can have a discount but only if you take the finance" deals real ?

Did people really only get a discount if they took the finance and people who paid 'cash' paid more ?

On new cars, yes - finance deposit contributions are typically made by the captive finance provider such as VWFS, BMW FS, etc and are often linked to quarterly campaign incentives/discounts/APRs on specific models or trim levels.Did people really only get a discount if they took the finance and people who paid 'cash' paid more ?

OddCat said:

To those who actually arranged car finance in a dealership, were these "you can have a discount but only if you take the finance" deals real ?

Did people really only get a discount if they took the finance and people who paid 'cash' paid more ?

This potential miss sell is about hidden commission agreements which were against the regulations at the time. Did people really only get a discount if they took the finance and people who paid 'cash' paid more ?

This in turn meant that potentially some dealers may have been economical with the truth as to what their best finance rate was at the time.

I cannot speak for others but over that period I took out 9 different agreements on 9 brand new cars.

Over that period I also bought other cars but on those no finance for whatever reason.

On some financed cars ( always “ part “) no discount was possible ,on others it was.

My negotiation style generally is first on the car itself / partex / price to change and then any finance conversations are dealt with separately.

I only take out Finance if the rate is acceptable and therefore I can use other money / investments to in effect offset the finance cost.

Doesn’t mean I was unhappy with any of those deals but that really isn’t the point.

OddCat said:

To those who actually arranged car finance in a dealership, were these "you can have a discount but only if you take the finance" deals real ?

Did people really only get a discount if they took the finance and people who paid 'cash' paid more ?

Yes, in the context of a finance contribution from the manufacturer (assuming new car).Did people really only get a discount if they took the finance and people who paid 'cash' paid more ?

So the manufacturer would put in say, £3,000 in to the finance package.

Which thus translates as a "discount" off the car when you take out the finance.

phpe said:

OddCat said:

To those who actually arranged car finance in a dealership, were these "you can have a discount but only if you take the finance" deals real ?

Did people really only get a discount if they took the finance and people who paid 'cash' paid more ?

On new cars, yes - finance deposit contributions are typically made by the captive finance provider such as VWFS, BMW FS, etc and are often linked to quarterly campaign incentives/discounts/APRs on specific models or trim levels.Did people really only get a discount if they took the finance and people who paid 'cash' paid more ?

Otherwise, people paying cash were disadvantaged in the sense that they were not told you'll have to take finance at 8% in order to get the discount - but you'll get, say, 3% of that back as a lump sum later. In which case some people might have chosen to do that.

OddCat said:

Well, hopefully, the FCA will have the good sense to instruct that these things must be netted out on the basis that it was all part of the same deal and you can't have the penny and the bun.

Otherwise, people paying cash were disadvantaged in the sense that they were not told you'll have to take finance at 8% in order to get the discount - but you'll get, say, 3% of that back as a lump sum later. In which case some people might have chosen to do that.

The FCA have been over all that previously, and chose to do nothing.Otherwise, people paying cash were disadvantaged in the sense that they were not told you'll have to take finance at 8% in order to get the discount - but you'll get, say, 3% of that back as a lump sum later. In which case some people might have chosen to do that.

OddCat said:

Well, hopefully, the FCA will have the good sense to instruct that these things must be netted out on the basis that it was all part of the same deal and you can't have the penny and the bun.

Otherwise, people paying cash were disadvantaged in the sense that they were not told you'll have to take finance at 8% in order to get the discount - but you'll get, say, 3% of that back as a lump sum later. In which case some people might have chosen to do that.

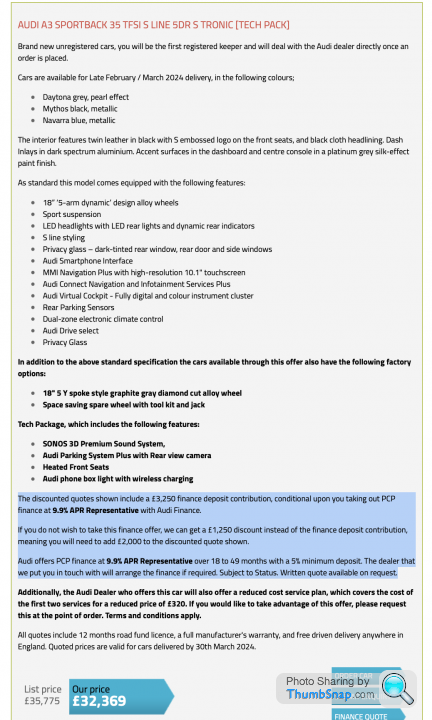

Here's an example of what I think is good practice - a new car buying service which breaks down the elements of the deal for the buyer to see.Otherwise, people paying cash were disadvantaged in the sense that they were not told you'll have to take finance at 8% in order to get the discount - but you'll get, say, 3% of that back as a lump sum later. In which case some people might have chosen to do that.

https://www.drivethedeal.com/SpecialOffers.aspx - let's pick a mid range A3 which is a fairly typical white goods aspirational car for the masses.

A savvy cash buyer can easily see the difference in discount between buying as a cash deal (£1250 off) and taking Audi Finance at 9.9% (£3250 off), and make their choice accordingly.

The key difference here (and the crux of the current investigation) is that Audi Finance will offer their published 9.9% rate to all eligible applicants...free from dealer interference bumping it up to say 13.9% to earn an undisclosed additional commission & the dealer not being transparent to the buyer about this aspect of the deal.

|https://thumbsnap.com/euRB3DJE[/url]

|https://thumbsnap.com/euRB3DJE[/url]Deep Thought said:

OddCat said:

Well, hopefully, the FCA will have the good sense to instruct that these things must be netted out on the basis that it was all part of the same deal and you can't have the penny and the bun.

Otherwise, people paying cash were disadvantaged in the sense that they were not told you'll have to take finance at 8% in order to get the discount - but you'll get, say, 3% of that back as a lump sum later. In which case some people might have chosen to do that.

The FCA have been over all that previously, and chose to do nothing.Otherwise, people paying cash were disadvantaged in the sense that they were not told you'll have to take finance at 8% in order to get the discount - but you'll get, say, 3% of that back as a lump sum later. In which case some people might have chosen to do that.

ashleyman said:

ashleyman said:

I’ve had a reply from MotoNovo. Nothing from VWFS or Santander yet.

Thank you for contacting us to find out if your Motor Finance Agreements had a discretionary commission arrangement. After an initial investigation we have concluded that your agreement(s) (1111111) for vehicle(s) (16REG) did involve a discretionary commission arrangement. We acknowledge and have recorded this as a complaint. We’ll provide you with a reference number via email as soon as possible. In the meantime, please use your agreement number as reference.

Santander have also just replied. DCA WAS in place on that one too. Thank you for contacting us to find out if your Motor Finance Agreements had a discretionary commission arrangement. After an initial investigation we have concluded that your agreement(s) (1111111) for vehicle(s) (16REG) did involve a discretionary commission arrangement. We acknowledge and have recorded this as a complaint. We’ll provide you with a reference number via email as soon as possible. In the meantime, please use your agreement number as reference.

With those being brand new on standard rates I can’t imagine there will be DCA but guess I’ll have to wait and see for sure.

The response to your enquiry will either advise that the commission model applicable to your agreement was fixed, and therefore not subject to any further action, or that the model was a Discretionary Commission Arrangement, in which case we will open a complaint on your behalf and our response will be an acknowledgement of your complaint.

OddCat said:

Deep Thought said:

OddCat said:

Well, hopefully, the FCA will have the good sense to instruct that these things must be netted out on the basis that it was all part of the same deal and you can't have the penny and the bun.

Otherwise, people paying cash were disadvantaged in the sense that they were not told you'll have to take finance at 8% in order to get the discount - but you'll get, say, 3% of that back as a lump sum later. In which case some people might have chosen to do that.

The FCA have been over all that previously, and chose to do nothing.Otherwise, people paying cash were disadvantaged in the sense that they were not told you'll have to take finance at 8% in order to get the discount - but you'll get, say, 3% of that back as a lump sum later. In which case some people might have chosen to do that.

Gassing Station | Finance | Top of Page | What's New | My Stuff