Poor people and credit

Discussion

DonkeyApple said:

berlintaxi said:

DonkeyApple said:

Firstly, there is no such thing as 0%. It's a marketing gimmick. You're still paying interest except it's front loaded in the deal.

Secondly, it's a good indicator that there is more to come off the price.

And thirdly, no one in their right mind is going to fanny about with credit paperwork. You're just going to give the money over and leave.

What a complet load of arrogant rubbish, do you realise how sad you come across as?Secondly, it's a good indicator that there is more to come off the price.

And thirdly, no one in their right mind is going to fanny about with credit paperwork. You're just going to give the money over and leave.

Nearly 300 posts per month, maybe you should try the real world for a change, you are completely out of touch with reality.

Edited by berlintaxi on Saturday 13th February 15:47

I couldn't spot anything that could be described as 'arrogant' either.

BrabusMog said:

DickyC said:

A high street dealer gave me a good discount on Mrs C's Rolex. I went in January when sales were slack.

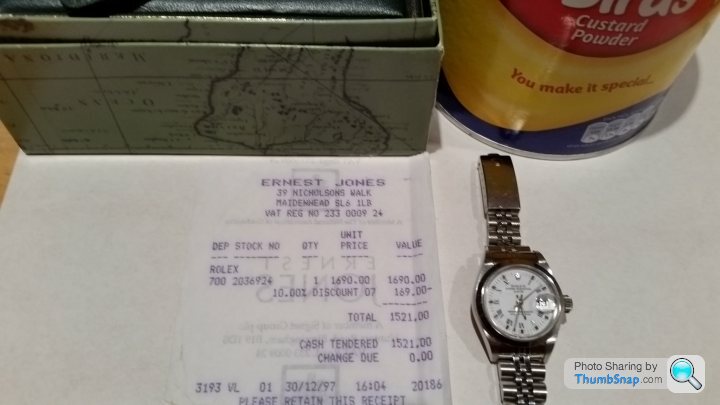

Custard, invoice, and watch, please. Not that I don't believe you, but none of my friends or family have ever got a disco off of the AD.

I had no idea it was so long ago! They did say no discount and took a bit of persuading. Mrs C wears it almost every day and it's like new.

DonkeyApple said:

Firstly, there is no such thing as 0%. It's a marketing gimmick. You're still paying interest except it's front loaded in the deal.

For that to be true - the cost of an item in a shop offering 0% interest would have to be higher than a shop that doesn't........how else would they pre-load the interest otherwise.If I can buy the same item in two different shops for the same price - but one offers 0% interest - would I not be mad not to take it?

Moonhawk said:

DonkeyApple said:

Firstly, there is no such thing as 0%. It's a marketing gimmick. You're still paying interest except it's front loaded in the deal.

For that to be true - the cost of an item in a shop offering 0% interest would have to be higher than a shop that doesn't........how else would they pre-load the interest otherwise.If I can buy the same item in two different shops for the same price - but one offers 0% interest - would I not be mad not to take it?

0% credit card balance transfer? Ever wondered why the "processing" fee is so high?

BrabusMog said:

Custard, invoice, and watch, please. Not that I don't believe you, but none of my friends or family have ever got a disco off of the AD.

Depends on the model, I would have thought. Stainless steel would be tricky, but I got a touch over 10% off my bi-metal sub at an AD in the UK.Moonhawk said:

DonkeyApple said:

Firstly, there is no such thing as 0%. It's a marketing gimmick. You're still paying interest except it's front loaded in the deal.

For that to be true - the cost of an item in a shop offering 0% interest would have to be higher than a shop that doesn't........how else would they pre-load the interest otherwise.If I can buy the same item in two different shops for the same price - but one offers 0% interest - would I not be mad not to take it?

They also aren't lending at 0 and just taking a small admin fee in exchange for the cost of their borrow on the debt (don't forget that finance houses borrow from banks and they borrow from money markets and there is interest mark-up all the way down the line until it reaches the retail consumer where the largest mark-up is applied to reflect the largest default risk).

There is a cost that is the whole funding charge over the lifetime of the debt, plus admin fee, less a small discount for paying 5 years (eg) interest up front.

One way or another, that is paid by the buyer. As the seller, gimmicks like 0% finance are good because they increase your turnover of stock as it allows more people to buy than would otherwise be possible (and that is the bit that is the entire basis for taking in consumer credit risk and the bit that the PH money gods try and tell the world isn't true and get very angry when someone dares to correct their deliberate deceits), it also helps shorten the length of time you are sitting on stock which is quite important as very often you are paying a lend on that stock yourself as you don't actually own it.

The point you make about two retailers having the same price etc is a valid one but the key is that as you know how the financing deal works and its cost and as you know the general way in which high cost retail units such as a jewellers run then you know that the finance cost is something you can play with as a buyer just like you always know the cost to the retail unit to process a purchase on a credit card. Obviously, there is no point in wasting time with chain stores as there is no one there who actually runs the business etc.

And here comes the nub, the reality of the situation, that some take great offence at. First of all, if you have £2k just sitting in your account that you have absolutely no need of and you wish to just swap for a nice bit of jewellery and as pointed out this money is earning nothing then you simply are not going to arse about in a shop buying a credit agreement as well as your bracelet to save just 1%. People simply do not behave like that. Even up in Yorkshire.

In addition you have to consider the rather simple fact that if an individual were one of the totally anomalous consumers who did go against all consumer and retail debt statistics and seek a 1% saving on goods that will plummet in value by what, 10-30% the moment a name is written in a piece of paper then such a person would generally seek out the far greater instance saving of finding an independent who will offer a discount greater than 1% for a cash transaction, or buy a bracelet that already has a name on its papers and thus make an even greater saving. But that type of consumer is not an impulse consumer and the marketing intent behind 0% deals is that they specifically target the impulse consumer.

It's a subject I find of interest as my family are jewellers. In the 70s-80s they were the largest sellers in the UK of Omega and some other brands. I myself am in retail credit and involved in lending. Just from that it is obvious that I am going to be pro consumer debt but it doesn't mean I am not free to dare to question the comical farce that is the 'I have the cash to dispose but I'm going to borrow instead' mantra of the modern Western male consumer. Equifax data alone highlights what a load of b

ks that is. The fact that a few people get angry each time someone dares to question the mantra and starts throwing abuse about (not you btw) really just reinforces the statement.

ks that is. The fact that a few people get angry each time someone dares to question the mantra and starts throwing abuse about (not you btw) really just reinforces the statement. Gassing Station | The Lounge | Top of Page | What's New | My Stuff