Average investing cost, subscriptions into Investment ISA.

Discussion

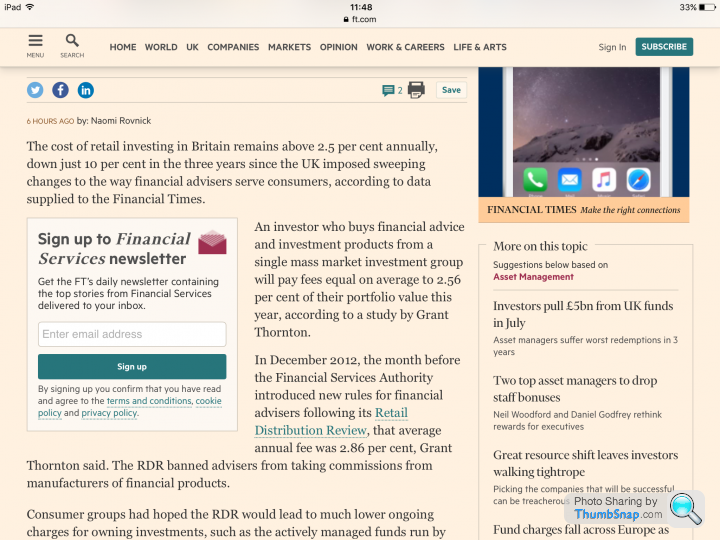

Money into the (investment) ISA wrapper increased by 20%, and the average cost of a retail investment is now a jaw dropping c.2.5% per annum. TWO POINT FIVE PERCENT???? Anyone who pays 2% (let alone 2.5) needs counselling.

Just thought you'd like to know - it's Friday after all, the sun is out and I've just decided to stack for the day and go mow the lawn. These links shouldn't be hiding behind paywalls.

https://www.gov.uk/government/statistics/individua...

https://www.ft.com/content/ba0ae18c-6a98-11e6-a0b1...

Just thought you'd like to know - it's Friday after all, the sun is out and I've just decided to stack for the day and go mow the lawn. These links shouldn't be hiding behind paywalls.

https://www.gov.uk/government/statistics/individua...

https://www.ft.com/content/ba0ae18c-6a98-11e6-a0b1...

Ginge R said:

Money into the (investment) ISA wrapper increased by 20%, and the average cost of a retail investment is now a jaw dropping c.2.5% per annum. TWO POINT FIVE PERCENT???? Anyone who pays 2% (let alone 2.5) needs counselling.

Just thought you'd like to know - it's Friday after all, the sun is out and I've just decided to stack for the day and go mow the lawn. These links shouldn't be hiding behind paywalls.

https://www.gov.uk/government/statistics/individua...

https://www.ft.com/content/ba0ae18c-6a98-11e6-a0b1...

Isn't the 'average' cost entirely meaningless, given the variety of different underlying exposures which you can have in an ISA?Just thought you'd like to know - it's Friday after all, the sun is out and I've just decided to stack for the day and go mow the lawn. These links shouldn't be hiding behind paywalls.

https://www.gov.uk/government/statistics/individua...

https://www.ft.com/content/ba0ae18c-6a98-11e6-a0b1...

Paying 0.5% would seem high for a UK equity tracker. Paying 2% for an active specialist emerging market equity fund might be quite reasonable.

sidicks said:

Isn't the 'average' cost entirely meaningless, given the variety of different underlying exposures which you can have in an ISA?

Paying 0.5% would seem high for a UK equity tracker. Paying 2% for an active specialist emerging market equity fund might be quite reasonable.

Wouldn't necessarily disagree. But there again, the 'average client' - whoever that might be, but that's who we're talking about - wouldn't be an aggregate 100% in emerging markets? By way of reference and balance: Paying 0.5% would seem high for a UK equity tracker. Paying 2% for an active specialist emerging market equity fund might be quite reasonable.

Ginge R said:

Wouldn't necessarily disagree. But there again, the 'average client' - whoever that might be, but that's who we're talking about - wouldn't be an aggregate 100% in emerging markets? By way of reference and balance:

I'm confused!The headline refers to ISAs (which are mainly invested in cash, according to the Government report) but the table you've attached seems to incorporate other products.

It also appears to combine initial costs and management fees.

Where does this 2.5% per annum figure come from?

Ginge R said:

Mate, just two separate items which I bundled together because they landed one after the other in my inbox.

Ah, ok.Ginge R said:

Did you read the FT piece?

Yep - funds that previously charged higher fees to pay commission now no longer do so, as the commission is charged separately.Ginge R said:

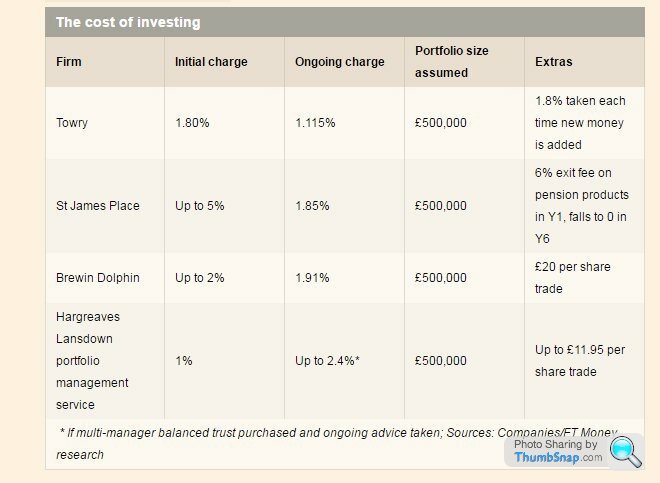

Here you go. Cheapest isn't always best, but by god, at 2.5%, I'd expect annual reviews hosted on the slopes of the Andes with my fevered brow and concern over cost wafted and gently calmed by svelte Peruvian virgins.

Yes, I saw that.My point was a) there wasn't any data to substantiate the number and b) the costs appear to relate to both investment management costs and advice costs.

I'm not sure that there is a need to pay for advice on an annual basis for a long term investment strategy, unless something fundamental has changed!

I was messaged earlier about this. On top of the fees mentioned, there's the SIPP which (it is claimed) tends to place most of its business in this direction, and the advice cost. Without pinning down the detail, that seems to me to be an annual cost of c.3.2 to 3.5%. They claim it's suitable for a three year strategy. I say 'strategy' of course.

https://www.nedbankprivatewealth.com/nedbank_wealt...

("Let's put 'private client' and 'wealth' on the masthead, think of a number, double it and add it to the cost").

edit: Gosh, here's a surprise - an 'independent' offshore recommendation.

https://www.aesinternational.com/reviews/offshore-...

https://www.nedbankprivatewealth.com/nedbank_wealt...

("Let's put 'private client' and 'wealth' on the masthead, think of a number, double it and add it to the cost").

edit: Gosh, here's a surprise - an 'independent' offshore recommendation.

https://www.aesinternational.com/reviews/offshore-...

Edited by Ginge R on Saturday 27th August 10:44

There are some very low charge operators out there who should also be mentioned. For instance, Cavendish Online offer one of the lowest cost pensions in the market with costs,

On typical funds:

Fund Charge 0.75%, FundsNetwork fee 0.25%, Cavendish Online fee 0.05% = Total Charge of 1.05% per year

On typical tracker funds:

Fund Charge 0.10%, FundsNetwork fee 0.25%, Cavendish Online fee 0.05% = Total Charge of 0.40% per year

Looks astounding value.

On typical funds:

Fund Charge 0.75%, FundsNetwork fee 0.25%, Cavendish Online fee 0.05% = Total Charge of 1.05% per year

On typical tracker funds:

Fund Charge 0.10%, FundsNetwork fee 0.25%, Cavendish Online fee 0.05% = Total Charge of 0.40% per year

Looks astounding value.

Ginge R said:

Money into the (investment) ISA wrapper increased by 20%, and the average cost of a retail investment is now a jaw dropping c.2.5% per annum. TWO POINT FIVE PERCENT???? Anyone who pays 2% (let alone 2.5) needs counselling.

Just thought you'd like to know - it's Friday after all, the sun is out and I've just decided to stack for the day and go mow the lawn. These links shouldn't be hiding behind paywalls.

https://www.gov.uk/government/statistics/individua...

https://www.ft.com/content/ba0ae18c-6a98-11e6-a0b1...

Surely it's all relative? Someone that manages their own portfolio for around 20bps pa may consider any advisory service expensive. Conversely, some want face to face advice and are willing to pay for it. Just thought you'd like to know - it's Friday after all, the sun is out and I've just decided to stack for the day and go mow the lawn. These links shouldn't be hiding behind paywalls.

https://www.gov.uk/government/statistics/individua...

https://www.ft.com/content/ba0ae18c-6a98-11e6-a0b1...

Ozzie Osmond said:

There are some very low charge operators out there who should also be mentioned. For instance, Cavendish Online offer one of the lowest cost pensions in the market with costs,

On typical funds:

Fund Charge 0.75%, FundsNetwork fee 0.25%, Cavendish Online fee 0.05% = Total Charge of 1.05% per year

On typical tracker funds:

Fund Charge 0.10%, FundsNetwork fee 0.25%, Cavendish Online fee 0.05% = Total Charge of 0.40% per year

Looks astounding value.

How do we think this compares with Old Mutual Wealth, Ginge R? https://www.cavendishonline.co.uk/investments/On typical funds:

Fund Charge 0.75%, FundsNetwork fee 0.25%, Cavendish Online fee 0.05% = Total Charge of 1.05% per year

On typical tracker funds:

Fund Charge 0.10%, FundsNetwork fee 0.25%, Cavendish Online fee 0.05% = Total Charge of 0.40% per year

Looks astounding value.

Simpo Two said:

Ozzie Osmond said:

There are some very low charge operators out there who should also be mentioned. For instance, Cavendish Online offer one of the lowest cost pensions in the market with costs,

On typical funds:

Fund Charge 0.75%, FundsNetwork fee 0.25%, Cavendish Online fee 0.05% = Total Charge of 1.05% per year

On typical tracker funds:

Fund Charge 0.10%, FundsNetwork fee 0.25%, Cavendish Online fee 0.05% = Total Charge of 0.40% per year

Looks astounding value.

How do we think this compares with Old Mutual Wealth, Ginge R? https://www.cavendishonline.co.uk/investments/On typical funds:

Fund Charge 0.75%, FundsNetwork fee 0.25%, Cavendish Online fee 0.05% = Total Charge of 1.05% per year

On typical tracker funds:

Fund Charge 0.10%, FundsNetwork fee 0.25%, Cavendish Online fee 0.05% = Total Charge of 0.40% per year

Looks astounding value.

Let's assume we're focusing on costs. £100,000-£500,000 held on Old Mutual will cost you 0.30%, with Cavendish, it's 0.25%. So, if you add the standing Cavendish charge of 0.20% (which wasn't mentioned by Oz), you're on parity as near as damnit with other platforms. Thereafter, other factors which you may wish to consider, apply. If we strike out fund costs and charges, Cavendish has a series of other sundry charges which creep things up a little - Old Mutual, to its credit, doesn't. So, c.0.49-0.54% to hold assets on both. But, it's all relative.

I've costed that for a singleton Vanguard fund, not all clients suit identical solutions. By comparison, the investment managers I use for 'Fiver' charge 0.46-0.52% which includes discretionary management via a wide variety of funds within a portfolio (and that's the ongoing fund and platform price I will also charge for my pension). I should point out, Fiver also charges a 0.34% annual advisory charge, so at c.0.8% pa, I'm more expensive in that sense, for an 'intelligent' advised service, than both Old Mutual and Cavendish are for a non advised 'iron bomb' one.

Like I said, I'm assuming your reference is costs and charges. Distilling whether or not *any* proposition is right, on a messageboard, is impossible. I fielded an angry call from someone last week who wasn't suitable for Fiver, because I suggested, instead, she use a different service. In a similar vein, and to demonstrate, Aegon bought Cofunds for £140million the other week, ostensibly to provide an 'integrated pension service'. That would make it, possibly, ideal for non advised drawdown clients (worth the premium to some?)? We'll see.

Ginge R said:

Let's assume we're focusing on costs. £100,000-£500,000 held on Old Mutual will cost you 0.30%, with Cavendish, it's 0.25%. So, if you add the standing Cavendish charge of 0.20% (which wasn't mentioned by Oz), you're on parity as near as damnit with other platforms. Thereafter, other factors which you may wish to consider, apply. If we strike out fund costs and charges, Cavendish has a series of other sundry charges which creep things up a little - Old Mutual, to its credit, doesn't. So, c.0.49-0.54% to hold assets on both. But, it's all relative.

I was under the impression that OMW was 0.35% for 500K+; am I wrong or has it changed? I went to check but am no further forward: https://www.oldmutualwealth.co.uk/Library/charges/...Gassing Station | Finance | Top of Page | What's New | My Stuff