PCP deal calculation help

Discussion

jw673 said:

From the OP: £35,999 - £13,000 PX - GFV £13,798.75, 49M@£227.33

=~1.29% Flat/~2.58% APR, ~£493 Per Month over the term (incl. PX). If ignoring PX - ~£227 = ~£39 Interest & ~£188 Depreciation, per month.

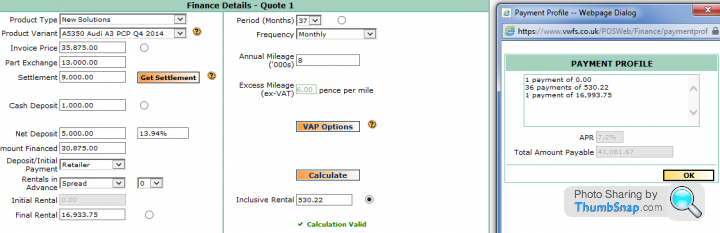

From the most recent post: £35,875 - £13,000 PX - GFV £16,933.75, 37M@£284.14

=~3.72% Flat/~7.62% APR, ~£635 Per Month over the term (incl. PX). If ignoring PX - ~£284 = ~£123 Interest & ~£161 Depreciation, per month.

The First Direct website isn't going to help as a PCP isn't a normal loan; it is in effect in two parts - a "normal" loan that covers the (expected) outstanding depreciation (Price-Deposit-GFV) and an interest only loan for the GFV. The above (*approximate*) figures are calculated on this basis.

crazy about cars - the initially posted deal, assuming it's quoted correctly(?), is actually the cheaper of the two - of which this is almost entirely down to the low %APR.

The above shows the other piece of the PCP puzzle - once you've ascertained you're getting the best price & PX, what's the best interest rate they're able to offer? This can make a *big* difference (see above) and is something the dealer may be able to change.

For example - the absolute bottom figure Audi finance may be willing to extend a loan to you, at a specific point in time/including any current finance offers/etc, may be 7%. Anything above this rate is free money from their perspective. If you're sold a deal that perfectly fits your laser-sharp focus on the "monthly", it may be that it's being offered at 7.5% APR - 0.5% for them to distribute as they wish (e.g. incentives based on deals sold above a given %APR rate). If the first (49M) example was at 7% vs. 7.5% APR - this would cost you an additional ~£360 over the term. I accept it isn't a vast amount of money - although better in your pocket than Audi's.

Note: as you'll be returning the vehicle I'm ignoring any consideration re: possible equity at the end of the term.

Yes, initial quote is correct but it's actually for an S1 - that was the first car I looked at and got offered PCP. I didn't even realised you can get PCP on used car but I was told it was a "pre registered" car.=~1.29% Flat/~2.58% APR, ~£493 Per Month over the term (incl. PX). If ignoring PX - ~£227 = ~£39 Interest & ~£188 Depreciation, per month.

From the most recent post: £35,875 - £13,000 PX - GFV £16,933.75, 37M@£284.14

=~3.72% Flat/~7.62% APR, ~£635 Per Month over the term (incl. PX). If ignoring PX - ~£284 = ~£123 Interest & ~£161 Depreciation, per month.

The First Direct website isn't going to help as a PCP isn't a normal loan; it is in effect in two parts - a "normal" loan that covers the (expected) outstanding depreciation (Price-Deposit-GFV) and an interest only loan for the GFV. The above (*approximate*) figures are calculated on this basis.

crazy about cars - the initially posted deal, assuming it's quoted correctly(?), is actually the cheaper of the two - of which this is almost entirely down to the low %APR.

The above shows the other piece of the PCP puzzle - once you've ascertained you're getting the best price & PX, what's the best interest rate they're able to offer? This can make a *big* difference (see above) and is something the dealer may be able to change.

For example - the absolute bottom figure Audi finance may be willing to extend a loan to you, at a specific point in time/including any current finance offers/etc, may be 7%. Anything above this rate is free money from their perspective. If you're sold a deal that perfectly fits your laser-sharp focus on the "monthly", it may be that it's being offered at 7.5% APR - 0.5% for them to distribute as they wish (e.g. incentives based on deals sold above a given %APR rate). If the first (49M) example was at 7% vs. 7.5% APR - this would cost you an additional ~£360 over the term. I accept it isn't a vast amount of money - although better in your pocket than Audi's.

Note: as you'll be returning the vehicle I'm ignoring any consideration re: possible equity at the end of the term.

The S3 on last post is a new car.

You are correct - I am not looking at any equity at the end as I have another family car which I plan to keep long term. I have been changing cars often and every time I lost money on P/X and sometimes on finance. For example I just paid off the finance on GTR and ended up PX it for E92 M3 just few months after! I've then sold the M3 for my current Fiat 595, granted I've got some cash back but I still lost out on the P/X as I've not got best price compared to selling privately.

So with PCP assuming I can afford the deposit next time plus monthly payments I should able to get a brand new car every 3 years while keeping "losses" low.

jw673 said:

If it's on the same basis as your most recent quote - I would guess at ~£530 PM.

re: S1 - I assume Audi either have finance offers (i.e. low %) on pre-reg cars, A1s/S1s, and/or pre-reg A1s/S1s - and that this doesn't currently apply to S3s.

Ouch - I was hoping for it to be around 400-ish tops. Don't think I'll proceed with that as it's rather high for PCP deals?re: S1 - I assume Audi either have finance offers (i.e. low %) on pre-reg cars, A1s/S1s, and/or pre-reg A1s/S1s - and that this doesn't currently apply to S3s.

Figures are funny as there was another used S3 quoted to me with £13,000 deposit but at £340/month... he didn't go into GFV and further details though.

Glad both the sales and business manager being very patient with my questions so far

mrdemon said:

It matters not what you put down, PCP you always loose,

Just work out what you pay a month over all which will be £560 and ask your self , am I happy to pay £560 a month to run the car.

Then look at a lease and see if you can do it cheaper than £560 a month, if so lease one.

I could not pay £560 a month to rent a hot hatch myself.

Don't think Audi does leasing and not very sure about personal leasing as I've heard it can be a pain.Just work out what you pay a month over all which will be £560 and ask your self , am I happy to pay £560 a month to run the car.

Then look at a lease and see if you can do it cheaper than £560 a month, if so lease one.

I could not pay £560 a month to rent a hot hatch myself.

Wills2 said:

They do, but often the retail arms of the dealers don't what to offer a PCH they prefer a PCP deal.

I've leased an Audi on a PCH contract from East Kent Audi.

Ah interesting to know I've leased an Audi on a PCH contract from East Kent Audi.

From my end I think the final decision it all depends on the figures based on £5k down, 36 months PCP as I definitely want some cash back and also want to keep monthly payments as low as possible. If I find the figures acceptable I will proceed otherwise I think I will respectfully decline & request deposit back.

I do feel bad not proceeding after all this but if I don't ask all the questions with them I wouldn't be in a position to make final decision - besides I did decline earlier but got call back that they've found a brand new car sitting in the docks...

I would like to extend my gratitude again to all posters who contributed - definitely learnt a lot in 2 days

Spooge said:

Paid a shade under 31k for my Stronic S3 in Sepang, with quite a few toys, sat nav, super sports seats, comfort pack etc.

You should not be paying list, even if you must have it before Christmas

That's cheap! Is that with Audi?You should not be paying list, even if you must have it before Christmas

I think I'll reply and say that after due consideration I will decline as the figures look to high to me...

mrdemon said:

The over all price will be the same what ever figures you do all will be about £560 a month give or take.

They just want you to pay so are left with a gfv.

I think it's a bad way to buy a car and to me £560 to rent a car ESP just a hot hatch does not seem worth it.

What it does allow is you to get into a brand new car for £560. But in 3 years time you will be worse off and have to start all over again, which is ok if you are happy always paying £560 for the rest of your life on average cars.

I just ran my car for. £120 a month for 2 years and it's a £50k car !!

Dealer love PCP and buyers love having new cars, you are stuck stuck in that loop for ever and it's a s t loop to be in.

t loop to be in.

You have £13k, loan another £15k you will have £28k to buy a nice car at £260 a month !!! Paying 3.9%

Then just pick a nice 2 year old car which has lost a good % of money and ONLY keep it 12 months so it's in warranty while you have it, buy wise and the car might only drop 2 or 3k over that time.

Hopefully you will be paying the loan off faster than the car is dropping in value, so in 18months you should be able to buy a £32k car next not a £28k car.

Work your way up the ladder and you will soon be in £50k cars you pay cash for.

Agreed - I think if I do go ahead I will quickly regret the decision after few months (especially paying £530+/month!) Somehow I was totally blind to the "invoice price" in the screenshot. Does look that I'm paying top dollar plus a high-ish APR so no wonder they are so happy to come back with quotes quickly.They just want you to pay so are left with a gfv.

I think it's a bad way to buy a car and to me £560 to rent a car ESP just a hot hatch does not seem worth it.

What it does allow is you to get into a brand new car for £560. But in 3 years time you will be worse off and have to start all over again, which is ok if you are happy always paying £560 for the rest of your life on average cars.

I just ran my car for. £120 a month for 2 years and it's a £50k car !!

Dealer love PCP and buyers love having new cars, you are stuck stuck in that loop for ever and it's a s

t loop to be in. You have £13k, loan another £15k you will have £28k to buy a nice car at £260 a month !!! Paying 3.9%

Then just pick a nice 2 year old car which has lost a good % of money and ONLY keep it 12 months so it's in warranty while you have it, buy wise and the car might only drop 2 or 3k over that time.

Hopefully you will be paying the loan off faster than the car is dropping in value, so in 18months you should be able to buy a £32k car next not a £28k car.

Work your way up the ladder and you will soon be in £50k cars you pay cash for.

I just want a new car and I want it quickly but sometimes I need to see beyond (my frankly crap man) maths

Wills2 said:

It works the same way apart from you cannot claim any of the VAT back.

If we look at a PCP agreement you are essentially buying the car with a deferred amount (the GFV) being payable at the end, because of the structure of the agreement the finance house guarantee to buy the vehicle from you at the end of the terms for the GFV (all things been equal) or you can buy it yourself or re finance the GFV, trade in etc...

With a PCH you are running an operating lease for the given period and will have to hand the car back at the end of term regardless.

One thing to note is the difference between a PCH and PCP as it appears on your credit file in that the total amount borrowed including the GFV shows on your credit file but with a PCH only the payments remaining show.

Something to think about of you're thinking of moving home/buying a house as the banks look at this now.

Thanks Wills that's definitely helpful. I'm looking to purchase a property in 3-5 years so this is good for thought. If we look at a PCP agreement you are essentially buying the car with a deferred amount (the GFV) being payable at the end, because of the structure of the agreement the finance house guarantee to buy the vehicle from you at the end of the terms for the GFV (all things been equal) or you can buy it yourself or re finance the GFV, trade in etc...

With a PCH you are running an operating lease for the given period and will have to hand the car back at the end of term regardless.

One thing to note is the difference between a PCH and PCP as it appears on your credit file in that the total amount borrowed including the GFV shows on your credit file but with a PCH only the payments remaining show.

Something to think about of you're thinking of moving home/buying a house as the banks look at this now.

Looks like best thing for me to do if I plan to borrow for a new car is to look for PCH lease deals and sell my current car privately.

Edited by crazy about cars on Sunday 14th December 15:37

Mandat said:

What's the issue with putting in a high deposit on a PCP?

I curently have a 3 year PCP with Audi and when working out the different cost options at the outset, the overall cost was lower with a larger deposit, since the amount being borrowed is less, therefore accruing less interest over the term.

Ultimately, the total cost will be a combination of deposit + 36 payments. Therefore in simple terms (and ignoring the cost of interest in this example), the overall cost would surely be the same with either a low deposit + high monthly payment or a high deposit + low monthly payments. At the end of the day, the same amount get paid off.

In my situation, I went for a large deposit and smaller monthly payments becuase I preferred a lower monthly liability.

I think the GFV also plays a part in the calculation - depending if you will be keeping the car.I curently have a 3 year PCP with Audi and when working out the different cost options at the outset, the overall cost was lower with a larger deposit, since the amount being borrowed is less, therefore accruing less interest over the term.

Ultimately, the total cost will be a combination of deposit + 36 payments. Therefore in simple terms (and ignoring the cost of interest in this example), the overall cost would surely be the same with either a low deposit + high monthly payment or a high deposit + low monthly payments. At the end of the day, the same amount get paid off.

In my situation, I went for a large deposit and smaller monthly payments becuase I preferred a lower monthly liability.

For me the final cost of purchase of around £41k just doesn't make it worthwhile in the end. It just doesn't seem the best way for me to get a new motor.

Plot thickens - my deposit is still not refunded but had a voicemail from Sales Manager asking me to call him back. Kept calling me "mate" now too

In conference most of today and tomorrow so can't really take calls so have requested him to email me if possible with further details.

So let's just say the invoice price is lowered to around £31,000 with same terms would it be a good deal?

In conference most of today and tomorrow so can't really take calls so have requested him to email me if possible with further details.

So let's just say the invoice price is lowered to around £31,000 with same terms would it be a good deal?

daemon said:

You're still in the realms of large deposit, large residual which means you're going to have taken a large bath by the end of the term, for what is really a glorified hot hatch.

True dat. I just don't understand why if this is sold to me as a new car I don't seem to be receiving the same deals.So what would you be paying for same car? What deposit, what monthly, what APR and what GFV?

Grandfondo said:

The GFV is set by Audi finance so that won't change really even with discount the deposit is up to you but will affect the monthly payments!

Get a cheap loan and at least you will know where you stand and at the end of the term at least you will have an asset if you can ever call a car that!

Thanks! Due to my choice of cars I've never really considered them an appreciating asset Get a cheap loan and at least you will know where you stand and at the end of the term at least you will have an asset if you can ever call a car that!

However with the competitive loan rates I do see why it's not really worth going for PCP deals in certain cases.

£5k down, £280/month 38 months PCP with £15,000 GFV sound like good deal?

jw673 said:

I think with an APR of ~0.5% the car would have to be discounted to ~£30,000 (note: it's unlikely be the same 36K-pre-discount car as before - the GFV has dropped quite a bit, with only an additional 1 month on the term). Or discounted to ~£26,300@~7.2% APR.

Have you made the £5K/£280PM/38M/£15K GFV figures up? or has it been indicated to you by the dealer that they're realistic/achievable?

At ~£31,000, on the same terms as before, I'd would guess at ~£380 PM (averaged incl. £5k deposit =~£513 PM, of which ~£133 PM is interest).

Whilst it may not be 100% accurate - if you tweak the spreadsheet for the slightly longer terms (37/38 vs 36) you can play with the figures.

Yes, those are the figures I've made up - I want to see what people would think is a good deal.Have you made the £5K/£280PM/38M/£15K GFV figures up? or has it been indicated to you by the dealer that they're realistic/achievable?

At ~£31,000, on the same terms as before, I'd would guess at ~£380 PM (averaged incl. £5k deposit =~£513 PM, of which ~£133 PM is interest).

Whilst it may not be 100% accurate - if you tweak the spreadsheet for the slightly longer terms (37/38 vs 36) you can play with the figures.

From the latest quote I think they only figure that could be lowered would be the invoice price. 7.2% APR seem to remain the same throughout my different quotes.

Hi all,

It seems that they are really desperate to shift. Still no refund I've been asked to go back to them with a figure of how much discount I want.

What should I say?

Invoice price reduced to £31,500

Deposit £5,000

36 months 8,000 miles

£380/month?

I guess the GFV and APR will remain the same.

P/S: I have no intention of owning this car I already own outright another. I just want the best way to run a new car for 3 years.

I've looked at lease deals and most are pretty restrictive when it comes to options but it is cheaper. Not to say I won't consider PCH but at the moment I would appreciate some advice based on my current situation with Audi's PCP quote.

It seems that they are really desperate to shift. Still no refund I've been asked to go back to them with a figure of how much discount I want.

What should I say?

Invoice price reduced to £31,500

Deposit £5,000

36 months 8,000 miles

£380/month?

I guess the GFV and APR will remain the same.

P/S: I have no intention of owning this car I already own outright another. I just want the best way to run a new car for 3 years.

I've looked at lease deals and most are pretty restrictive when it comes to options but it is cheaper. Not to say I won't consider PCH but at the moment I would appreciate some advice based on my current situation with Audi's PCP quote.

Edited by crazy about cars on Tuesday 16th December 18:36

daemon said:

Broadspeed are only offering around 6% discount so i'd be surprised if a dealer was able to do 15%.

Not sure otherwise. I cant say i feel the love for the deal at all, but maybe others will be more positive

Perhaps I should rephrase my question as, based on the spec what should the invoice price be? Not sure otherwise. I cant say i feel the love for the deal at all, but maybe others will be more positive

At the moment I am comfortable putting in £5,000 deposit and £380/month for 3 years. I might but car outright but what I will do is negotiate to go onto another PCP deal.

The last quote at list price I believe the final cost of purchase at 7.2% apr was £42,000 which I'm definitely not comfortable with.

I reckon if discounted to £31,000 I should be able to hit the target above.

The last quote at list price I believe the final cost of purchase at 7.2% apr was £42,000 which I'm definitely not comfortable with.

I reckon if discounted to £31,000 I should be able to hit the target above.

Gassing Station | General Gassing | Top of Page | What's New | My Stuff