PCP deal calculation help

Discussion

Fox- said:

CarlT said:

7.2% APR is cheaper than a bank loan at a guess...

Why guess - rates are clearly published and these rates are given to at least 51% of applicants.7.2% is far higher than a decent bank loan. Some are as low as 3.8%.

The cheapest loan i could find for £30,000 over three years was 5.9% APR

https://www.moneysupermarket.com/loans/quick-searc...

Fox- said:

daemon said:

BMW's PCP rate is 4.9% APR.

Have BMW started offering PCP's on Audi S3's then?Edited by daemon on Saturday 20th December 00:49

Edited by daemon on Saturday 20th December 01:20

daemon said:

Surely a matching APR would say otherwise?

For example, BMW are quoting 4.9% APR on their PCP deals, so presumably a 4.9% APR loan would have the same Annual Percentage Rate?

Interestingly, the cheapest APR i could get there with a quick check online for a £30,000 loan was 5.9% APR.

Funnily enough APR is affected by how the balance is re paid, payment holidays, breaks in payments, and end payments all stupidly show a lower APR, when in fact you are paying more interest. Thanks to the people who set APR up to continually confuse the end buyer.For example, BMW are quoting 4.9% APR on their PCP deals, so presumably a 4.9% APR loan would have the same Annual Percentage Rate?

Interestingly, the cheapest APR i could get there with a quick check online for a £30,000 loan was 5.9% APR.

Dr Jekyll said:

What I mean is:

Finance £20,000 on a PCP with £10,000 balloon. Start off owing £20,000, end up owing £10,000, so on average paying interest on just over £15,000.

Finance £20,000 over the same period on HP. Start off owing £20,000, end up owing zero, so on average paying interest on just over £10,000.

In a nutshell yes.Finance £20,000 on a PCP with £10,000 balloon. Start off owing £20,000, end up owing £10,000, so on average paying interest on just over £15,000.

Finance £20,000 over the same period on HP. Start off owing £20,000, end up owing zero, so on average paying interest on just over £10,000.

As has been said the balloon (end payment) does not reduce in balance with the time so the interest remains continually being calculated on that full amount, where your monthly payments drop so the interest on the amount that is being borrowed reduces with time.

Wills2 said:

crazy about cars said:

This was the final quote I've got. It's definitely better than the previous offer but I just don't feel comfortable enough paying over 400/month renting.

What discount are they giving you? And I would want that APR at 5% max. Just go back to them with what you are willing to/are happy with, they can only say no, and if so you walk.

daemon said:

I quoted it as an aside to show not all PCP deals have that high a rate and that 3.8% might not be achievable

I would imagine anyone with the financial resources etc to be buying brand new Audi's will have a sufficiently glowing credit record that the Representative APR will be easily achievable.Regarding the APR% it's been mentioned that 7-7.2% is normal for new cars while it's around 11% for used. Again I've been told the S3 I was offered is a new car not a pre-reg. Must be a cancelled order.

Has anyone managed to secure a better APR on Audi Finance? If you look at the screenshot closer the part around "Audi Finance" looks a bit funny as though it's been pasted over. Also did anyone notice "Add. charges" has been added to make the final price £33k? Is this normal?

Has anyone managed to secure a better APR on Audi Finance? If you look at the screenshot closer the part around "Audi Finance" looks a bit funny as though it's been pasted over. Also did anyone notice "Add. charges" has been added to make the final price £33k? Is this normal?

Edited by crazy about cars on Saturday 20th December 10:00

Edited by crazy about cars on Saturday 20th December 11:43

Fox- said:

daemon said:

I quoted it as an aside to show not all PCP deals have that high a rate and that 3.8% might not be achievable

I would imagine anyone with the financial resources etc to be buying brand new Audi's will have a sufficiently glowing credit record that the Representative APR will be easily achievable.I put that in with an "excellent" credit rating.

I think its the amount thats limiting the amount of competitive providers.

Happy for you to find a link to a 3.8% deal @ £30k.

It doesn't really matter if the loan is 3.8% 5.8 or 7.8% because the reason PCP will win most of the time is the person can't afford £900 a month end of!

Which brings us back nicely to "PCP gets some people into cars they can't afford to own!"

Or PCP gets lots of people into cars they can't afford to purchase but can rent for a while!

Which brings us back nicely to "PCP gets some people into cars they can't afford to own!"

Or PCP gets lots of people into cars they can't afford to purchase but can rent for a while!

Grandfondo said:

Which brings us back nicely to "PCP gets some people into cars they can't afford to own!"

"Some balloons are red!"Oh look, I made a statement that is factually correct but is vague enough that it provides absolutely no new or useful information. Looks like I've joined your club.

xRIEx said:

Grandfondo said:

Which brings us back nicely to "PCP gets some people into cars they can't afford to own!"

"Some balloons are red!"Oh look, I made a statement that is factually correct but is vague enough that it provides absolutely no new or useful information. Looks like I've joined your club.

Some balloons can't be paid so have to walk home!

crazy about cars said:

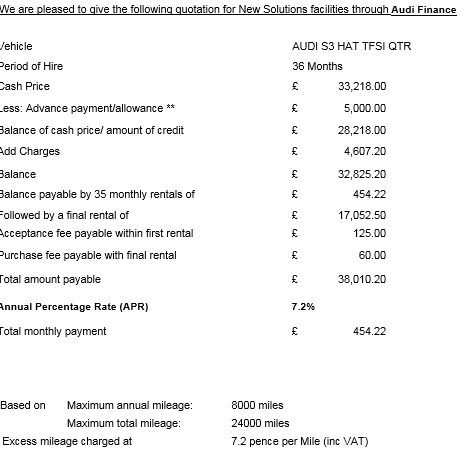

Regarding the APR% it's been mentioned that 7-7.2% is normal for new cars while it's around 11% for used. Again I've been told the S3 I was offered is a new car not a pre-reg. Must be a cancelled order.

Has anyone managed to secure a better APR on Audi Finance? If you look at the screenshot closer the part around "Audi Finance" looks a bit funny as though it's been pasted over. Also did anyone notice "Add. charges" has been added to make the final price £33k? Is this normal?

Audi Finance is part of Volkswagen Finanicial Services, so that maybe what is under the 'Audi Finance' line.Has anyone managed to secure a better APR on Audi Finance? If you look at the screenshot closer the part around "Audi Finance" looks a bit funny as though it's been pasted over. Also did anyone notice "Add. charges" has been added to make the final price £33k? Is this normal?

Edited by crazy about cars on Saturday 20th December 10:00

Edited by crazy about cars on Saturday 20th December 11:43

Add Charges - this is the charge for credit. IE. interest

The interest rate is generally fixed on new cars, there would have been no harm in asking though...

Well I know I shouldn't have but seen 2 used M135is with right colour and spec so I've asked for HP deals. It was over 780/month so I've asked for some PCP headline figures instead.

Car #1 retails at £31,500. 64 Reg

GFV £13,000 -ish (not confirmed)

5,000 deposit

36 month term/8,000 miles (No GAP)

Monthly payment = £580/month! Told him no straight away.

Car #2 retails at £27,500. 63 Reg although registered in Feb 2014

GFV £14,478

5,000 deposit

36 month term/8,000 miles (No GAP)

Monthly payment = £379. It was then pushed down to £350. Did some thinking but ultimately turned down.

350x36 + 5,000 = £488.88/month just for "renting" a used (albeit still very new) car. As a comparison I was paying around 420/month on a 20k car loan but I get to keep the car at the end not just walk away!

I like new cars and also like to change cars often and I definitely think PCP can work if I am careful. Just need to spot a nice deal on a new car and most importantly be patient!

P/S: Regarding the "can't afford to own" I would somewhat agree. I can get the equity to pay the balance outright but that would be crazy thing for me to do as I'm basically emptying the new house fund. So yes, I technically cannot afford to own a brand new car outright now.

Car #1 retails at £31,500. 64 Reg

GFV £13,000 -ish (not confirmed)

5,000 deposit

36 month term/8,000 miles (No GAP)

Monthly payment = £580/month! Told him no straight away.

Car #2 retails at £27,500. 63 Reg although registered in Feb 2014

GFV £14,478

5,000 deposit

36 month term/8,000 miles (No GAP)

Monthly payment = £379. It was then pushed down to £350. Did some thinking but ultimately turned down.

350x36 + 5,000 = £488.88/month just for "renting" a used (albeit still very new) car. As a comparison I was paying around 420/month on a 20k car loan but I get to keep the car at the end not just walk away!

I like new cars and also like to change cars often and I definitely think PCP can work if I am careful. Just need to spot a nice deal on a new car and most importantly be patient!

P/S: Regarding the "can't afford to own" I would somewhat agree. I can get the equity to pay the balance outright but that would be crazy thing for me to do as I'm basically emptying the new house fund. So yes, I technically cannot afford to own a brand new car outright now.

Edited by crazy about cars on Wednesday 24th December 12:13

crazy about cars said:

350x36 + 5,000 = £488.88/month just for "renting" a used (albeit still very new) car. As a comparison I was paying around 420/month on a 20k car loan but I get to keep the car at the end not just walk away!

I like new cars and also like to change cars often and I definitely think PCP can work if I am careful. Just need to spot a nice deal on a new car and most importantly be patient!

P/S: Regarding the "can't afford to own" I would somewhat agree. I can get the equity to pay the balance outright but that would be crazy thing for me to do as I'm basically emptying the new house fund. So yes, I technically cannot afford to own a brand new car outright now.

You seem to have this quite well weighed up. I guess the questions now are: how much are you prepared to pay per month for the use of a new car and is it likely that a deal will be offered at that price?I like new cars and also like to change cars often and I definitely think PCP can work if I am careful. Just need to spot a nice deal on a new car and most importantly be patient!

P/S: Regarding the "can't afford to own" I would somewhat agree. I can get the equity to pay the balance outright but that would be crazy thing for me to do as I'm basically emptying the new house fund. So yes, I technically cannot afford to own a brand new car outright now.

TA14 said:

You seem to have this quite well weighed up. I guess the questions now are: how much are you prepared to pay per month for the use of a new car and is it likely that a deal will be offered at that price?

I would be looking at German hot hatches like S3, M135i or Golf R. The term would have to be 36 month/8000 miles. I would like to stick to max of £5,000 as deposit. I'll be happy to pay around 250/month. If on HP I am willing to pay up to 450/month and put in larger deposit. From my experience so far that doesn't seem possible on PCP but let's see what the new year brings. Some people mentioned leasing which is something I need to look into as Audi/BMW/Merc doesn't really push personal leasing.

I've "lost" a lot when changing cars in the past as I've almost never negotiated on discounts, however all those cars were either bought outright or on HP so I own the car in the end someway or another. Hence on PCP I would hope to do all the research and be comfortable with what I'm going into.

I think in your position I would look at an older M135i - they are all low miles and warranted anyway so why not save a pile of money?

http://usedcars.bmw.co.uk/1-Series/3.0-M135i/Bosto...

This one has the M Performance Exhuast and you could probably get that price down to nearer £20k. Drop your £6k deposit down, borrow £15k from Santander or similar at 4ish % APR and over 48 months you are paying £339.

You can almost always haggle 2 years warranty into the dealer then circa £40ish a month for the remaining 2 years.

Then either:

a) At the end of the 48 months you own an M135i outright. Judging by the values of the old shape 135i or 130i hatchbacks it's going to be worth at least 10k. Yours to do with as you wish.

b) Want a shorter term? With a £6k deposit the car is likely always going to be worth more than the loan and the loan isn't secured on the car, so simply flog it and pay the loan off.

http://usedcars.bmw.co.uk/1-Series/3.0-M135i/Bosto...

This one has the M Performance Exhuast and you could probably get that price down to nearer £20k. Drop your £6k deposit down, borrow £15k from Santander or similar at 4ish % APR and over 48 months you are paying £339.

You can almost always haggle 2 years warranty into the dealer then circa £40ish a month for the remaining 2 years.

Then either:

a) At the end of the 48 months you own an M135i outright. Judging by the values of the old shape 135i or 130i hatchbacks it's going to be worth at least 10k. Yours to do with as you wish.

b) Want a shorter term? With a £6k deposit the car is likely always going to be worth more than the loan and the loan isn't secured on the car, so simply flog it and pay the loan off.

4%-ish APR is good, very good indeed for a £20,000 loan! I really need to do my research on loans as in my position it gives me more choices and also very competitive rates to PCP. However a 2014 (63 reg) M135i is only £5k more so that might sound like a better proposition. M Performance exhaust + debadged is good and I love that colour however I would prefer H&K system.

Fox- said:

I think in your position I would look at an older M135i - they are all low miles and warranted anyway so why not save a pile of money?

http://usedcars.bmw.co.uk/1-Series/3.0-M135i/Bosto...

This one has the M Performance Exhuast and you could probably get that price down to nearer £20k. Drop your £6k deposit down, borrow £15k from Santander or similar at 4ish % APR and over 48 months you are paying £339.

You can almost always haggle 2 years warranty into the dealer then circa £40ish a month for the remaining 2 years.

Then either:

a) At the end of the 48 months you own an M135i outright. Judging by the values of the old shape 135i or 130i hatchbacks it's going to be worth at least 10k. Yours to do with as you wish.

b) Want a shorter term? With a £6k deposit the car is likely always going to be worth more than the loan and the loan isn't secured on the car, so simply flog it and pay the loan off.

http://usedcars.bmw.co.uk/1-Series/3.0-M135i/Bosto...

This one has the M Performance Exhuast and you could probably get that price down to nearer £20k. Drop your £6k deposit down, borrow £15k from Santander or similar at 4ish % APR and over 48 months you are paying £339.

You can almost always haggle 2 years warranty into the dealer then circa £40ish a month for the remaining 2 years.

Then either:

a) At the end of the 48 months you own an M135i outright. Judging by the values of the old shape 135i or 130i hatchbacks it's going to be worth at least 10k. Yours to do with as you wish.

b) Want a shorter term? With a £6k deposit the car is likely always going to be worth more than the loan and the loan isn't secured on the car, so simply flog it and pay the loan off.

Fox- said:

Is it?

I don't see what £5k gets you that makes it worth spending to get a 63 plate instead of a 62 plate.

Length of warranty as I'll most probably keep it for 3 years at least. In the example you have given there's 1 year left on manufacturers and AUC warranty is not applicable when there's balance of manufacturers left. Regarding discounts you'd be surprised at how reluctant BMW is at giving them on used cars. Having nearly £3k off is neigh on impossible I think.I don't see what £5k gets you that makes it worth spending to get a 63 plate instead of a 62 plate.

3 years down the line I would guess that car would be worth very close to £10-12k which is less than the value I've borrowed (£15k + interest).

The more I think of it there's really no win-win situation for a buyer unless there's been a great deal like what they used to do for the new Golf Rs.

Gassing Station | General Gassing | Top of Page | What's New | My Stuff