PCP deal calculation help

Discussion

crazy about cars said:

To be honest I have no intentions of keeping it.

In which case/if you'll be returning it to Audi finance at the end of the PCP - over the term, including writing off the £13,000 PX as you're returning the car and (*if*) any equity is irrelevant, @~3.6% Flat/~7.37% APR it will have cost you ~£646 a month for the use of the vehicle (i.e. total/36). If ignoring the PX and just taking the £284 monthly - over the term this works out at an average of ~£119 in interest and ~£165 in depreciation, per month.

http://www.carfile.net/business/audi-a3-s3_tfsi_qu... shows discounts available on the S3 - I'm not sure why you're happy to pay what appears to be list price(?) for an in-stock car? This is what PCPs are good for - having the customer concentrate on the "monthly" as opposed to the basics, in your case: the price of the car and the value of the PX. How you best fund it once you've finalised those details are open to (endless, on PH) debate.

crazy about cars - see email re: PCP spreadsheet

Note: the above is based on 36 months

jw673 said:

In which case/if you'll be returning it to Audi finance at the end of the PCP - over the term, including writing off the £13,000 PX as you're returning the car and (*if*) any equity is irrelevant, @~3.6% Flat/~7.37% APR it will have cost you ~£646 a month for the use of the vehicle (i.e. total/36).

If ignoring the PX and just taking the £284 monthly - over the term this works out at an average of ~£119 in interest and ~£165 in depreciation, per month.

http://www.carfile.net/business/audi-a3-s3_tfsi_qu... shows discounts available on the S3 - I'm not sure why you're happy to pay what appears to be list price(?) for an in-stock car? This is what PCPs are good for - having the customer concentrate on the "monthly" as opposed to the basics, in your case: the price of the car and the value of the PX. How you best fund it once you've finalised those details are open to (endless, on PH) debate.

crazy about cars - see email re: PCP spreadsheet

Note: the above is based on 36 months

Thank you so much for your analysis so far jw673. I will check my PH email later.If ignoring the PX and just taking the £284 monthly - over the term this works out at an average of ~£119 in interest and ~£165 in depreciation, per month.

http://www.carfile.net/business/audi-a3-s3_tfsi_qu... shows discounts available on the S3 - I'm not sure why you're happy to pay what appears to be list price(?) for an in-stock car? This is what PCPs are good for - having the customer concentrate on the "monthly" as opposed to the basics, in your case: the price of the car and the value of the PX. How you best fund it once you've finalised those details are open to (endless, on PH) debate.

crazy about cars - see email re: PCP spreadsheet

Note: the above is based on 36 months

There are a few options on the car I'm looking at such as B&O, black optics pack, tech pack etc but to be fair I've not got a complete list of options which I've requested. The price including options as in screenshot is given as almost £36k.

I've also requested to see if it's possible to put down £5,000 deposit and have £8,000 cashback and will see how that will affect the monthly and GFV figures.

crazy about cars said:

Blimey that's a cracking deal! You are right it will cost around £400+/month with a £3k deposit. No discount given at all on the S3 but it does come with loaded with the right toys. Must've been a cancelled order.

Try Harder, I've heard of people getting 10% discount on them. I got 8% on mine when i ordered it in September 2013 with not much hesitation from the dealer.timbo999 said:

Under £2k interest to borrow £23k for 4 years??? Bite their hand off, that's cheaper than a Tesco loan for the same amount/period (and I can guarantee its nothing like 7%!!)...

I don't think your guarantees are worth much seeing as there are a few offering 4% or slightly under. crazy about cars said:

Thank you so much for your analysis so far jw673. I will check my PH email later.

There are a few options on the car I'm looking at such as B&O, black optics pack, tech pack etc but to be fair I've not got a complete list of options which I've requested. The price including options as in screenshot is given as almost £36k.

I've also requested to see if it's possible to put down £5,000 deposit and have £8,000 cashback and will see how that will affect the monthly and GFV figures.

Whilst the dealer _may_ (I've no idea/is this ever possible?) be given some (tiny) room for manoeuvre on the GFV to please a customer - more likely than not the GFV will not change, irrespective of how you chop'n'change the payments. Changing annual mileage, or term, will change the GFV - age and mileage being one of the two main elements that determine a cars value (when comparing identical spec cars).There are a few options on the car I'm looking at such as B&O, black optics pack, tech pack etc but to be fair I've not got a complete list of options which I've requested. The price including options as in screenshot is given as almost £36k.

I've also requested to see if it's possible to put down £5,000 deposit and have £8,000 cashback and will see how that will affect the monthly and GFV figures.

Also - the car already exists, so it isn't like you can select/deselect options for a factory order to see the GFV change on subsequent quotes. If you could – this would quite likely influence your choice as to what you wanted to spec. For example - you could decide if option X was “worth” (to you) the extra Y pounds per month.

That it is potentially loaded with options (£££) is also likely a "problem" - those options are unlikely to add much to the GFV, although are pushing up the price. I suspect you're going to end up paying for the whole (or at least, most of the) cost of them over the term; this being reflected in the depreciation/RRP->GFV. This isn't specific to how you're financing it - just a fact of life that options rarely retain much of their value at re-sale (save for a few things - leather, metallic paint, Sat Nav etc). I'm sure someone else has a better idea of how much value each of your specific options retains/what impact (if any) it is likely to have on the GFV.

Finally - how you change your payments doesn't change a) is it a good price/what discount can you achieve? and b) is the PX value reasonable?

Thanks for all the advice chaps - really appreciate it.

I believe I've been blinded by the fact that I can have a new toy before Christmas without thinking of the longer term implications.

From what I can understand the car is worth £36,000 retail now and assuming at the end of 3 year I want to keep the car I pay around £4,000 (40k total) interest assuming I can fork out the balloon of 16k. If I don't I've lost £21,000 (13k as valued for my current car + 8k rental and that's not inclusive of the 3k I've lost in the 3 months of ownership).

Fired a few questions and will see what replies I get tomorrow but otherwise I do think it's a very costly Christmas present indeed. Just hope I would get my deposit back...

I believe I've been blinded by the fact that I can have a new toy before Christmas without thinking of the longer term implications.

From what I can understand the car is worth £36,000 retail now and assuming at the end of 3 year I want to keep the car I pay around £4,000 (40k total) interest assuming I can fork out the balloon of 16k. If I don't I've lost £21,000 (13k as valued for my current car + 8k rental and that's not inclusive of the 3k I've lost in the 3 months of ownership).

Fired a few questions and will see what replies I get tomorrow but otherwise I do think it's a very costly Christmas present indeed. Just hope I would get my deposit back...

xRIEx said:

I don't think your guarantees are worth much seeing as there are a few offering 4% or slightly under.

Er, yeah... I think you've misunderstood what I'm saying - If the interest charge is £2k on £23k over 4 years (as per the original post) then the interest rate cannot be 7% - its straight calculation you twerp. So I can guarantee it as it happens! Gawd there are some Muppets on here!timbo999 said:

xRIEx said:

I don't think your guarantees are worth much seeing as there are a few offering 4% or slightly under.

Er, yeah... I think you've misunderstood what I'm saying - If the interest charge is £2k on £23k over 4 years (as per the original post) then the interest rate cannot be 7% - its straight calculation you twerp. So I can guarantee it as it happens! Gawd there are some Muppets on here!If you're having trouble, go to the First Direct website, it'll help you work out the answer.

Edited by xRIEx on Sunday 14th December 09:37

Edited by xRIEx on Sunday 14th December 09:38

crazy about cars said:

Thanks for all the advice chaps - really appreciate it.

I believe I've been blinded by the fact that I can have a new toy before Christmas without thinking of the longer term implications.

From what I can understand the car is worth £36,000 retail now and assuming at the end of 3 year I want to keep the car I pay around £4,000 (40k total) interest assuming I can fork out the balloon of 16k. If I don't I've lost £21,000 (13k as valued for my current car + 8k rental and that's not inclusive of the 3k I've lost in the 3 months of ownership).

Fired a few questions and will see what replies I get tomorrow but otherwise I do think it's a very costly Christmas present indeed. Just hope I would get my deposit back...

PCP deals work best when they are manufacturer incentivised with cash in from them and when theres a relatively small deposit (say 10% tops). If that results in monthly payments you're happy with then great as you'll probably have a couple of thousand in equity at the end so you're only really down the monthly payments.I believe I've been blinded by the fact that I can have a new toy before Christmas without thinking of the longer term implications.

From what I can understand the car is worth £36,000 retail now and assuming at the end of 3 year I want to keep the car I pay around £4,000 (40k total) interest assuming I can fork out the balloon of 16k. If I don't I've lost £21,000 (13k as valued for my current car + 8k rental and that's not inclusive of the 3k I've lost in the 3 months of ownership).

Fired a few questions and will see what replies I get tomorrow but otherwise I do think it's a very costly Christmas present indeed. Just hope I would get my deposit back...

I think you're very much right to work away from this one.

I cannot see the sense in putting 13k cash into a 35k car to not own it at the end, and then on top of that not getting any discount on a manual S3 (surely that market will prefer the DSG)

I wouldn't put down anymore than 10% and I'd be looking for 5% APR and a discount.

You can get an S3 for 2.5k down and £360 a month on PCH.....

http://www.contracthire-audi.co.uk/audi_s-rs_contr...

Thanks again all for the helpful advise.

I've asked for a revised figure based on deposit of £5k (£8k refunded), 8,000 miles/year 3 year PCP . Will see how the monthly payments are. Worse case I was told that my £1,000 deposit will be refunded, otherwise the car will be PDI'ed, registered and delivered to me before Christmas.

Regarding the specs it's as below (only thing missing from my wish list is sunroof but to be honest it's not a deal breaker):

S3 3 door 6 speed manual in Panther black

Bang & Olufsen

Black styling package

Technology package with Audi connect

Comfort package

Privacy glass

Red brake calipers

Black inlays

I've asked for a revised figure based on deposit of £5k (£8k refunded), 8,000 miles/year 3 year PCP . Will see how the monthly payments are. Worse case I was told that my £1,000 deposit will be refunded, otherwise the car will be PDI'ed, registered and delivered to me before Christmas.

Regarding the specs it's as below (only thing missing from my wish list is sunroof but to be honest it's not a deal breaker):

S3 3 door 6 speed manual in Panther black

Bang & Olufsen

Black styling package

Technology package with Audi connect

Comfort package

Privacy glass

Red brake calipers

Black inlays

From the OP: £35,999 - £13,000 PX - GFV £13,798.75, 49M@£227.33

=~1.29% Flat/~2.58% APR, ~£493 Per Month over the term (incl. PX). If ignoring PX - ~£227 = ~£39 Interest & ~£188 Depreciation, per month.

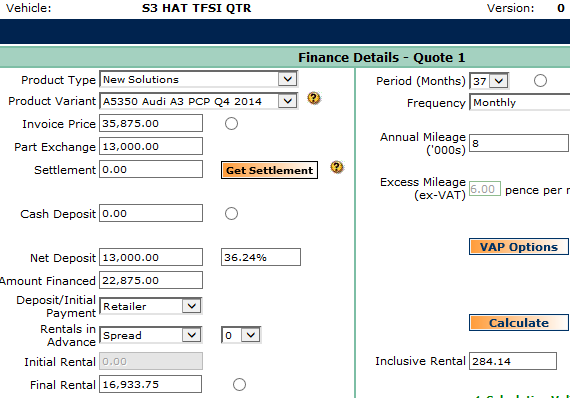

From the post@18:56: £35,875 - £13,000 PX - GFV £16,933.75, 37M@£284.14

=~3.72% Flat/~7.62% APR, ~£635 Per Month over the term (incl. PX). If ignoring PX - ~£284 = ~£123 Interest & ~£161 Depreciation, per month.

The First Direct website isn't going to help as a PCP isn't a normal loan; it is in effect in two parts - a "normal" loan that covers the (expected) outstanding depreciation (Price-Deposit-GFV) and an interest only loan for the GFV. The above (*approximate*) figures are calculated on this basis.

crazy about cars - the initially posted deal, assuming it's quoted correctly(?), is actually the cheaper of the two - of which this is almost entirely down to the low %APR.

The above shows the other piece of the PCP puzzle - once you've ascertained you're getting the best price & PX, what's the best interest rate they're able to offer? This can make a *big* difference (see above) and is something the dealer may be able to change.

For example - the absolute bottom figure Audi finance may be willing to extend a loan to you, at a specific point in time/including any current finance offers/etc, may be 7%. Anything above this rate is free money from their perspective. If you're sold a deal that perfectly fits your laser-sharp focus on the "monthly", it may be that it's being offered at 7.5% APR - 0.5% for them to distribute as they wish (e.g. incentives based on deals sold above a given %APR rate). If the first (49M) example was at 7% vs. 7.5% APR - this would cost you an additional ~£360 over the term. I accept it isn't a vast amount of money - although better in your pocket than Audi's.

Note: as you'll be returning the vehicle I'm ignoring any consideration re: possible equity at the end of the term.

=~1.29% Flat/~2.58% APR, ~£493 Per Month over the term (incl. PX). If ignoring PX - ~£227 = ~£39 Interest & ~£188 Depreciation, per month.

From the post@18:56: £35,875 - £13,000 PX - GFV £16,933.75, 37M@£284.14

=~3.72% Flat/~7.62% APR, ~£635 Per Month over the term (incl. PX). If ignoring PX - ~£284 = ~£123 Interest & ~£161 Depreciation, per month.

The First Direct website isn't going to help as a PCP isn't a normal loan; it is in effect in two parts - a "normal" loan that covers the (expected) outstanding depreciation (Price-Deposit-GFV) and an interest only loan for the GFV. The above (*approximate*) figures are calculated on this basis.

crazy about cars - the initially posted deal, assuming it's quoted correctly(?), is actually the cheaper of the two - of which this is almost entirely down to the low %APR.

The above shows the other piece of the PCP puzzle - once you've ascertained you're getting the best price & PX, what's the best interest rate they're able to offer? This can make a *big* difference (see above) and is something the dealer may be able to change.

For example - the absolute bottom figure Audi finance may be willing to extend a loan to you, at a specific point in time/including any current finance offers/etc, may be 7%. Anything above this rate is free money from their perspective. If you're sold a deal that perfectly fits your laser-sharp focus on the "monthly", it may be that it's being offered at 7.5% APR - 0.5% for them to distribute as they wish (e.g. incentives based on deals sold above a given %APR rate). If the first (49M) example was at 7% vs. 7.5% APR - this would cost you an additional ~£360 over the term. I accept it isn't a vast amount of money - although better in your pocket than Audi's.

Note: as you'll be returning the vehicle I'm ignoring any consideration re: possible equity at the end of the term.

Edited by jw673 on Sunday 14th December 11:54

Wills2 said:

I cannot see the sense in putting 13k cash into a 35k car to not own it at the end, and then on top of that not getting any discount on a manual S3 (surely that market will prefer the DSG)

I wouldn't put down anymore than 10% and I'd be looking for 5% APR and a discount.

You can get an S3 for 2.5k down and £360 a month on PCH.....

http://www.contracthire-audi.co.uk/audi_s-rs_contr...

Manual is my personal preference as I had a 6 speed MKII TT which was fun. The new engine is rated at 300PS so it will be even better I wouldn't put down anymore than 10% and I'd be looking for 5% APR and a discount.

You can get an S3 for 2.5k down and £360 a month on PCH.....

http://www.contracthire-audi.co.uk/audi_s-rs_contr...

I'm happy to know that Audi Finance offers S3 for just £2.5k deposit and 360/month! My long term plan (assuming I can afford) is to continue getting a new car every 3 years on PCP with Audi. To me that's new car every 3 years with minimal cost to change and cost to run over the duration. Makes sense?

jw673 said:

From the OP: £35,999 - £13,000 PX - GFV £13,798.75, 49M@£227.33

=~1.29% Flat/~2.58% APR, ~£493 Per Month over the term (incl. PX). If ignoring PX - ~£227 = ~£39 Interest & ~£188 Depreciation, per month.

From the most recent post: £35,875 - £13,000 PX - GFV £16,933.75, 37M@£284.14

=~3.72% Flat/~7.62% APR, ~£635 Per Month over the term (incl. PX). If ignoring PX - ~£284 = ~£123 Interest & ~£161 Depreciation, per month.

The First Direct website isn't going to help as a PCP isn't a normal loan; it is in effect in two parts - a "normal" loan that covers the (expected) outstanding depreciation (Price-Deposit-GFV) and an interest only loan for the GFV. The above (*approximate*) figures are calculated on this basis.

crazy about cars - the initially posted deal, assuming it's quoted correctly(?), is actually the cheaper of the two - of which this is almost entirely down to the low %APR.

The above shows the other piece of the PCP puzzle - once you've ascertained you're getting the best price & PX, what's the best interest rate they're able to offer? This can make a *big* difference (see above) and is something the dealer may be able to change.

For example - the absolute bottom figure Audi finance may be willing to extend a loan to you, at a specific point in time/including any current finance offers/etc, may be 7%. Anything above this rate is free money from their perspective. If you're sold a deal that perfectly fits your laser-sharp focus on the "monthly", it may be that it's being offered at 7.5% APR - 0.5% for them to distribute as they wish (e.g. incentives based on deals sold above a given %APR rate). If the first (49M) example was at 7% vs. 7.5% APR - this would cost you an additional ~£360 over the term. I accept it isn't a vast amount of money - although better in your pocket than Audi's.

Note: as you'll be returning the vehicle I'm ignoring any consideration re: possible equity at the end of the term.

Yes, initial quote is correct but it's actually for an S1 - that was the first car I looked at and got offered PCP. I didn't even realised you can get PCP on used car but I was told it was a "pre registered" car.=~1.29% Flat/~2.58% APR, ~£493 Per Month over the term (incl. PX). If ignoring PX - ~£227 = ~£39 Interest & ~£188 Depreciation, per month.

From the most recent post: £35,875 - £13,000 PX - GFV £16,933.75, 37M@£284.14

=~3.72% Flat/~7.62% APR, ~£635 Per Month over the term (incl. PX). If ignoring PX - ~£284 = ~£123 Interest & ~£161 Depreciation, per month.

The First Direct website isn't going to help as a PCP isn't a normal loan; it is in effect in two parts - a "normal" loan that covers the (expected) outstanding depreciation (Price-Deposit-GFV) and an interest only loan for the GFV. The above (*approximate*) figures are calculated on this basis.

crazy about cars - the initially posted deal, assuming it's quoted correctly(?), is actually the cheaper of the two - of which this is almost entirely down to the low %APR.

The above shows the other piece of the PCP puzzle - once you've ascertained you're getting the best price & PX, what's the best interest rate they're able to offer? This can make a *big* difference (see above) and is something the dealer may be able to change.

For example - the absolute bottom figure Audi finance may be willing to extend a loan to you, at a specific point in time/including any current finance offers/etc, may be 7%. Anything above this rate is free money from their perspective. If you're sold a deal that perfectly fits your laser-sharp focus on the "monthly", it may be that it's being offered at 7.5% APR - 0.5% for them to distribute as they wish (e.g. incentives based on deals sold above a given %APR rate). If the first (49M) example was at 7% vs. 7.5% APR - this would cost you an additional ~£360 over the term. I accept it isn't a vast amount of money - although better in your pocket than Audi's.

Note: as you'll be returning the vehicle I'm ignoring any consideration re: possible equity at the end of the term.

The S3 on last post is a new car.

You are correct - I am not looking at any equity at the end as I have another family car which I plan to keep long term. I have been changing cars often and every time I lost money on P/X and sometimes on finance. For example I just paid off the finance on GTR and ended up PX it for E92 M3 just few months after! I've then sold the M3 for my current Fiat 595, granted I've got some cash back but I still lost out on the P/X as I've not got best price compared to selling privately.

So with PCP assuming I can afford the deposit next time plus monthly payments I should able to get a brand new car every 3 years while keeping "losses" low.

crazy about cars said:

I've asked for a revised figure based on deposit of £5k (£8k refunded), 8,000 miles/year 3 year PCP .

If it's on the same basis as your most recent quote - I would guess at ~£530 PM.re: S1 - I assume Audi either have finance offers (i.e. low %) on pre-reg cars, A1s/S1s, and/or pre-reg A1s/S1s - and that this doesn't currently apply to S3s.

It matters not what you put down, PCP you always loose,

Just work out what you pay a month over all which will be £560 and ask your self , am I happy to pay £560 a month to run the car.

Then look at a lease and see if you can do it cheaper than £560 a month, if so lease one.

I could not pay £560 a month to rent a hot hatch myself.

Just work out what you pay a month over all which will be £560 and ask your self , am I happy to pay £560 a month to run the car.

Then look at a lease and see if you can do it cheaper than £560 a month, if so lease one.

I could not pay £560 a month to rent a hot hatch myself.

Gassing Station | General Gassing | Top of Page | What's New | My Stuff