PCP deal calculation help

Discussion

jw673 said:

If it's on the same basis as your most recent quote - I would guess at ~£530 PM.

re: S1 - I assume Audi either have finance offers (i.e. low %) on pre-reg cars, A1s/S1s, and/or pre-reg A1s/S1s - and that this doesn't currently apply to S3s.

Ouch - I was hoping for it to be around 400-ish tops. Don't think I'll proceed with that as it's rather high for PCP deals?re: S1 - I assume Audi either have finance offers (i.e. low %) on pre-reg cars, A1s/S1s, and/or pre-reg A1s/S1s - and that this doesn't currently apply to S3s.

Figures are funny as there was another used S3 quoted to me with £13,000 deposit but at £340/month... he didn't go into GFV and further details though.

Glad both the sales and business manager being very patient with my questions so far

mrdemon said:

It matters not what you put down, PCP you always loose,

Just work out what you pay a month over all which will be £560 and ask your self , am I happy to pay £560 a month to run the car.

Then look at a lease and see if you can do it cheaper than £560 a month, if so lease one.

I could not pay £560 a month to rent a hot hatch myself.

Don't think Audi does leasing and not very sure about personal leasing as I've heard it can be a pain.Just work out what you pay a month over all which will be £560 and ask your self , am I happy to pay £560 a month to run the car.

Then look at a lease and see if you can do it cheaper than £560 a month, if so lease one.

I could not pay £560 a month to rent a hot hatch myself.

Wills2 said:

They do, but often the retail arms of the dealers don't what to offer a PCH they prefer a PCP deal.

I've leased an Audi on a PCH contract from East Kent Audi.

Ah interesting to know I've leased an Audi on a PCH contract from East Kent Audi.

From my end I think the final decision it all depends on the figures based on £5k down, 36 months PCP as I definitely want some cash back and also want to keep monthly payments as low as possible. If I find the figures acceptable I will proceed otherwise I think I will respectfully decline & request deposit back.

I do feel bad not proceeding after all this but if I don't ask all the questions with them I wouldn't be in a position to make final decision - besides I did decline earlier but got call back that they've found a brand new car sitting in the docks...

I would like to extend my gratitude again to all posters who contributed - definitely learnt a lot in 2 days

Spooge said:

Paid a shade under 31k for my Stronic S3 in Sepang, with quite a few toys, sat nav, super sports seats, comfort pack etc.

You should not be paying list, even if you must have it before Christmas

That's cheap! Is that with Audi?You should not be paying list, even if you must have it before Christmas

I think I'll reply and say that after due consideration I will decline as the figures look to high to me...

crazy about cars said:

Ah interesting to know

From my end I think the final decision it all depends on the figures based on £5k down, 36 months PCP as I definitely want some cash back and also want to keep monthly payments as low as possible. If I find the figures acceptable I will proceed otherwise I think I will respectfully decline & request deposit back.

I do feel bad not proceeding after all this but if I don't ask all the questions with them I wouldn't be in a position to make final decision - besides I did decline earlier but got call back that they've found a brand new car sitting in the docks...

I would like to extend my gratitude again to all posters who contributed - definitely learnt a lot in 2 days

The over all price will be the same what ever figures you do all will be about £560 a month give or take.From my end I think the final decision it all depends on the figures based on £5k down, 36 months PCP as I definitely want some cash back and also want to keep monthly payments as low as possible. If I find the figures acceptable I will proceed otherwise I think I will respectfully decline & request deposit back.

I do feel bad not proceeding after all this but if I don't ask all the questions with them I wouldn't be in a position to make final decision - besides I did decline earlier but got call back that they've found a brand new car sitting in the docks...

I would like to extend my gratitude again to all posters who contributed - definitely learnt a lot in 2 days

They just want you to pay so are left with a gfv.

I think it's a bad way to buy a car and to me £560 to rent a car ESP just a hot hatch does not seem worth it.

What it does allow is you to get into a brand new car for £560. But in 3 years time you will be worse off and have to start all over again, which is ok if you are happy always paying £560 for the rest of your life on average cars.

I just ran my car for. £120 a month for 2 years and it's a £50k car !!

Dealer love PCP and buyers love having new cars, you are stuck stuck in that loop for ever and it's a s

t loop to be in.

t loop to be in. You have £13k, loan another £15k you will have £28k to buy a nice car at £260 a month !!! Paying 3.9%

Then just pick a nice 2 year old car which has lost a good % of money and ONLY keep it 12 months so it's in warranty while you have it, buy wise and the car might only drop 2 or 3k over that time.

Hopefully you will be paying the loan off faster than the car is dropping in value, so in 18months you should be able to buy a £32k car next not a £28k car.

Work your way up the ladder and you will soon be in £50k cars you pay cash for.

crazy about cars said:

That's cheap! Is that with Audi?

I think I'll reply and say that after due consideration I will decline as the figures look to high to me...

Yeah. I just got them to match the deal with drivethedeal.com. I think I'll reply and say that after due consideration I will decline as the figures look to high to me...

This was before the price increase in September and it was on a new car because I was happy to wait, and it was also end of quarter. Still, take the price specced up from dtd and stick the numbers in your pcp calculator.

N

jw673 said:

Whilst the dealer _may_ (I've no idea/is this ever possible?) be given some (tiny) room for manoeuvre on the GFV to please a customer - more likely than not the GFV will not change, irrespective of how you chop'n'change the payments. Changing annual mileage, or term, will change the GFV - age and mileage being one of the two main elements that determine a cars value (when comparing identical spec cars).

Also - the car already exists, so it isn't like you can select/deselect options for a factory order to see the GFV change on subsequent quotes. If you could – this would quite likely influence your choice as to what you wanted to spec. For example - you could decide if option X was “worth” (to you) the extra Y pounds per month.

That it is potentially loaded with options (£££) is also likely a "problem" - those options are unlikely to add much to the GFV, although are pushing up the price. I suspect you're going to end up paying for the whole (or at least, most of the) cost of them over the term; this being reflected in the depreciation/RRP->GFV. This isn't specific to how you're financing it - just a fact of life that options rarely retain much of their value at re-sale (save for a few things - leather, metallic paint, Sat Nav etc). I'm sure someone else has a better idea of how much value each of your specific options retains/what impact (if any) it is likely to have on the GFV.

Finally - how you change your payments doesn't change a) is it a good price/what discount can you achieve? and b) is the PX value reasonable?

The GFV is set by Volkswagen Finanicial Services and not the dealer. Therefore, you could only reduce it and not increase it. Options generally haven no impact whatsoever on the GFV a.Also - the car already exists, so it isn't like you can select/deselect options for a factory order to see the GFV change on subsequent quotes. If you could – this would quite likely influence your choice as to what you wanted to spec. For example - you could decide if option X was “worth” (to you) the extra Y pounds per month.

That it is potentially loaded with options (£££) is also likely a "problem" - those options are unlikely to add much to the GFV, although are pushing up the price. I suspect you're going to end up paying for the whole (or at least, most of the) cost of them over the term; this being reflected in the depreciation/RRP->GFV. This isn't specific to how you're financing it - just a fact of life that options rarely retain much of their value at re-sale (save for a few things - leather, metallic paint, Sat Nav etc). I'm sure someone else has a better idea of how much value each of your specific options retains/what impact (if any) it is likely to have on the GFV.

Finally - how you change your payments doesn't change a) is it a good price/what discount can you achieve? and b) is the PX value reasonable?

mrdemon said:

The over all price will be the same what ever figures you do all will be about £560 a month give or take.

They just want you to pay so are left with a gfv.

I think it's a bad way to buy a car and to me £560 to rent a car ESP just a hot hatch does not seem worth it.

What it does allow is you to get into a brand new car for £560. But in 3 years time you will be worse off and have to start all over again, which is ok if you are happy always paying £560 for the rest of your life on average cars.

I just ran my car for. £120 a month for 2 years and it's a £50k car !!

Dealer love PCP and buyers love having new cars, you are stuck stuck in that loop for ever and it's a st loop to be in.

You have £13k, loan another £15k you will have £28k to buy a nice car at £260 a month !!! Paying 3.9%

Then just pick a nice 2 year old car which has lost a good % of money and ONLY keep it 12 months so it's in warranty while you have it, buy wise and the car might only drop 2 or 3k over that time.

Hopefully you will be paying the loan off faster than the car is dropping in value, so in 18months you should be able to buy a £32k car next not a £28k car.

Work your way up the ladder and you will soon be in £50k cars you pay cash for.

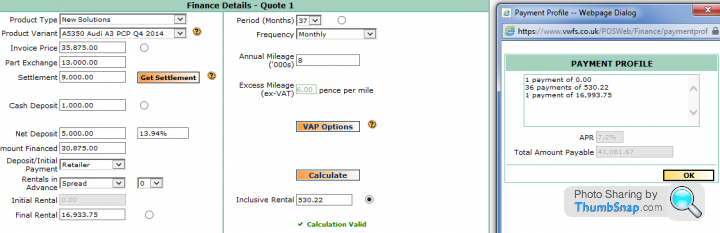

Agreed - I think if I do go ahead I will quickly regret the decision after few months (especially paying £530+/month!) Somehow I was totally blind to the "invoice price" in the screenshot. Does look that I'm paying top dollar plus a high-ish APR so no wonder they are so happy to come back with quotes quickly.They just want you to pay so are left with a gfv.

I think it's a bad way to buy a car and to me £560 to rent a car ESP just a hot hatch does not seem worth it.

What it does allow is you to get into a brand new car for £560. But in 3 years time you will be worse off and have to start all over again, which is ok if you are happy always paying £560 for the rest of your life on average cars.

I just ran my car for. £120 a month for 2 years and it's a £50k car !!

Dealer love PCP and buyers love having new cars, you are stuck stuck in that loop for ever and it's a s

t loop to be in. You have £13k, loan another £15k you will have £28k to buy a nice car at £260 a month !!! Paying 3.9%

Then just pick a nice 2 year old car which has lost a good % of money and ONLY keep it 12 months so it's in warranty while you have it, buy wise and the car might only drop 2 or 3k over that time.

Hopefully you will be paying the loan off faster than the car is dropping in value, so in 18months you should be able to buy a £32k car next not a £28k car.

Work your way up the ladder and you will soon be in £50k cars you pay cash for.

I just want a new car and I want it quickly but sometimes I need to see beyond (my frankly crap man) maths

Random leasing example for comparison (albeit not stock and at this price it'll be with zero options):

8K PA, 1x£2116.73 + 35x£352.79

http://www.gateway2lease.com/z_audi_s3_tfsiquattro...

Until you get an actual quote/confirmed pricing - take anything (pricing/availability/etc) posted on broker's websites with a pinch of salt. Nevertheless it provides you with an idea on lease pricing; it'll be nowhere near £5k + £530 PM (although, unlike Audi, they'll not take your PX).

Regardless of how it's being paid for - take each deal on its merits and certainly *do not* rush into anything.

8K PA, 1x£2116.73 + 35x£352.79

http://www.gateway2lease.com/z_audi_s3_tfsiquattro...

Until you get an actual quote/confirmed pricing - take anything (pricing/availability/etc) posted on broker's websites with a pinch of salt. Nevertheless it provides you with an idea on lease pricing; it'll be nowhere near £5k + £530 PM (although, unlike Audi, they'll not take your PX).

Regardless of how it's being paid for - take each deal on its merits and certainly *do not* rush into anything.

xRIEx said:

So if you pay £1,911.01 on borrowing £23k over 4 years, what is the interest rate then?

If you're having trouble, go to the First Direct website, it'll help you work out the answer.

I'm not having any trouble thanks - its you that doesn't seem to understand! (Hint its not 4% either!)If you're having trouble, go to the First Direct website, it'll help you work out the answer.

Edited by xRIEx on Sunday 14th December 09:37

Edited by xRIEx on Sunday 14th December 09:38

crazy about cars said:

As I've understood both PCP & leasing almost the same except for leasing you dont have the option to buy the car back. I understand how leasing can work for business but how would it work for personal use?

It works the same way apart from you cannot claim any of the VAT back. If we look at a PCP agreement you are essentially buying the car with a deferred amount (the GFV) being payable at the end, because of the structure of the agreement the finance house guarantee to buy the vehicle from you at the end of the terms for the GFV (all things been equal) or you can buy it yourself or re finance the GFV, trade in etc...

With a PCH you are running an operating lease for the given period and will have to hand the car back at the end of term regardless.

One thing to note is the difference between a PCH and PCP as it appears on your credit file in that the total amount borrowed including the GFV shows on your credit file but with a PCH only the payments remaining show.

Something to think about of you're thinking of moving home/buying a house as the banks look at this now.

Wills2 said:

It works the same way apart from you cannot claim any of the VAT back.

If we look at a PCP agreement you are essentially buying the car with a deferred amount (the GFV) being payable at the end, because of the structure of the agreement the finance house guarantee to buy the vehicle from you at the end of the terms for the GFV (all things been equal) or you can buy it yourself or re finance the GFV, trade in etc...

With a PCH you are running an operating lease for the given period and will have to hand the car back at the end of term regardless.

One thing to note is the difference between a PCH and PCP as it appears on your credit file in that the total amount borrowed including the GFV shows on your credit file but with a PCH only the payments remaining show.

Something to think about of you're thinking of moving home/buying a house as the banks look at this now.

Thanks Wills that's definitely helpful. I'm looking to purchase a property in 3-5 years so this is good for thought. If we look at a PCP agreement you are essentially buying the car with a deferred amount (the GFV) being payable at the end, because of the structure of the agreement the finance house guarantee to buy the vehicle from you at the end of the terms for the GFV (all things been equal) or you can buy it yourself or re finance the GFV, trade in etc...

With a PCH you are running an operating lease for the given period and will have to hand the car back at the end of term regardless.

One thing to note is the difference between a PCH and PCP as it appears on your credit file in that the total amount borrowed including the GFV shows on your credit file but with a PCH only the payments remaining show.

Something to think about of you're thinking of moving home/buying a house as the banks look at this now.

Looks like best thing for me to do if I plan to borrow for a new car is to look for PCH lease deals and sell my current car privately.

Edited by crazy about cars on Sunday 14th December 15:37

timbo999 said:

xRIEx said:

So if you pay £1,911.01 on borrowing £23k over 4 years, what is the interest rate then?

If you're having trouble, go to the First Direct website, it'll help you work out the answer.

I'm not having any trouble thanks - its you that doesn't seem to understand! (Hint its not 4% either!)If you're having trouble, go to the First Direct website, it'll help you work out the answer.

Edited by xRIEx on Sunday 14th December 09:37

Edited by xRIEx on Sunday 14th December 09:38

xRIEx said:

In that case you'd better tell FD that they've got their figures wrong, or shop them to the FCA/PRA for non-compliant advertising.

Trust me ('cos I can do arithmetic) the APR on the figures in the original post (below) is 2.6% as someone posted before. I suspect you have forgotten that its got a balloon payment of £13k odd so its not a straight repayment loan.'Car retail value : £35,999

P/X value : £13,000 (to be used as deposit)

PCP 49 months £227.33 per month with an optional final future value of £13798.75p'

Edited by timbo999 on Sunday 14th December 20:08

What's the issue with putting in a high deposit on a PCP?

I curently have a 3 year PCP with Audi and when working out the different cost options at the outset, the overall cost was lower with a larger deposit, since the amount being borrowed is less, therefore accruing less interest over the term.

Ultimately, the total cost will be a combination of deposit + 36 payments. Therefore in simple terms (and ignoring the cost of interest in this example), the overall cost would surely be the same with either a low deposit + high monthly payment or a high deposit + low monthly payments. At the end of the day, the same amount get paid off.

In my situation, I went for a large deposit and smaller monthly payments becuase I preferred a lower monthly liability.

I curently have a 3 year PCP with Audi and when working out the different cost options at the outset, the overall cost was lower with a larger deposit, since the amount being borrowed is less, therefore accruing less interest over the term.

Ultimately, the total cost will be a combination of deposit + 36 payments. Therefore in simple terms (and ignoring the cost of interest in this example), the overall cost would surely be the same with either a low deposit + high monthly payment or a high deposit + low monthly payments. At the end of the day, the same amount get paid off.

In my situation, I went for a large deposit and smaller monthly payments becuase I preferred a lower monthly liability.

Gassing Station | General Gassing | Top of Page | What's New | My Stuff