Are the wheels about to fall of car finance?

Discussion

gizlaroc said:

I have been one of the biggest advocates of financing cars, and still am, however, the PCP deals are bordering on a scam and mis selling imho, especially on used cars where the APR is sky high.

I just borrowed £30k from Hitachi Capital Finance for 2.89% at £537 a month.

BMW wanted me to borrow from them at only £527 a month.

He said that ''We Guarantee your car will be worth £13000 at the end of the term."

I kept saying "No, you guarantee that if I want to keep my car at the end of the term I will have to give you an additional £13,000 for the privilege."

Considering this guy was selling finance it was scary the fact he simply didn't get what I was saying.

Currently people are paying the equivalent in extra interest to the balloon at the end, and that is why I think car finance will be the new PPI, it is bordering on mis selling.

I think this is the problem in a nutshell. There is nothing wrong with the principals of PCP financing, the issue is the way that it is sold and the tricks that are used to disguise the true costs. I am not surprised that people are caught out with this. I just borrowed £30k from Hitachi Capital Finance for 2.89% at £537 a month.

BMW wanted me to borrow from them at only £527 a month.

He said that ''We Guarantee your car will be worth £13000 at the end of the term."

I kept saying "No, you guarantee that if I want to keep my car at the end of the term I will have to give you an additional £13,000 for the privilege."

Considering this guy was selling finance it was scary the fact he simply didn't get what I was saying.

Currently people are paying the equivalent in extra interest to the balloon at the end, and that is why I think car finance will be the new PPI, it is bordering on mis selling.

Cars are depreciating assets. If you buy them with cash, your equity erodes over time. If you buy them with finance you need to fund that depreciation. You need to be able to look at the cost of ownership over a given period and understand what you are paying in terms of that depreciation and interest. You also need to be able to compare the interest to what might be available elsewhere as an unsecured loan.

In terms of the interest, there is inevitably a cost to using other peoples money. If you don't have the cash then you need to decide if that is worth paying. If you do have the cash you need to decide if it is better to use it elsewhere (e.g. by leaving it in an offset mortgage account). Part of that is an understanding of liquidity. I don't necessarily want to have £40k tied up in a new car if I might need to get to that money in an emergency.

The problem is the hard sell from dealers. I understand this stuff well and I was very open with the last dealer I spoke to. Regardless, the business manager still came out and started talking to me about the cost per month, without agreeing the deposit and GMFV. They also quoted me interest using flat rates to disguise the punitive APR.

It is a minefield for someone who is not financially literate or experienced. But that is about sales NOT about finance itself.

I found this post interesting. I have recently been working with one of the largest vehicle financing organisations in the UK and conversation turned to this exact topic. I was told that they themselves had expected the bubble to burst at the end of last year and are surprised it's still continuing. Straight from the horses mouth as it were.

Elysium said:

I think this is the problem in a nutshell. There is nothing wrong with the principals of PCP financing, the issue is the way that it is sold and the tricks that are used to disguise the true costs. I am not surprised that people are caught out with this.

Cars are depreciating assets. If you buy them with cash, your equity erodes over time. If you buy them with finance you need to fund that depreciation. You need to be able to look at the cost of ownership over a given period and understand what you are paying in terms of that depreciation and interest. You also need to be able to compare the interest to what might be available elsewhere as an unsecured loan.

In terms of the interest, there is inevitably a cost to using other peoples money.

Good points ! That's why a lease, for all its faults, is far less opaque than PCP although some still struggle to add/multiply a few simple numbers.Cars are depreciating assets. If you buy them with cash, your equity erodes over time. If you buy them with finance you need to fund that depreciation. You need to be able to look at the cost of ownership over a given period and understand what you are paying in terms of that depreciation and interest. You also need to be able to compare the interest to what might be available elsewhere as an unsecured loan.

In terms of the interest, there is inevitably a cost to using other peoples money.

I would disagree with the inevitability of the cost of using other people's money. Occasionally a lease deal will be significantly less than depreciation (for a number of reasons that I can't be bothered explaining again) but as this is the only route to that situation, you're effectively saving money by choosing to use other people's money.

CS Garth said:

The canniest thing car markers have done in recent times is to make people view a car like a phone and completely obfuscate the actual price they are paying. So long as the wheels go round and a car has equity or parity in it then the corks keep popping, the minute negative equity creeps in (ie values soften) then the problems start. As with any credit boom.

Particularly influencing the young, wrapping up insurance sometimes into the deal, fewer youngsters (and their families) hands on with cars which increases the risk cost of a used car etc. Edited by CS Garth on Monday 27th March 11:09

It's a constant part of consumerism these days (always was but seems even more marketed/pushed now), that something is new/improved and therefore the great all singing and dancing thing 12 months ago is now obsolete and almost embarrassing to have! Nothing old is worth caring for, image is almost everything and (may be I'm old!) but this seems really bad in the youth (£200+ must have football boots anyone?)

I'm not sure the wheels will fall off yet, it suits everyone in the main so it seems, manufacturers and us and a slow in sales will probably see more incentives/deals and perhaps the odd uncompetitive/'struggling more than others' manufacturer will go at some point?

gizlaroc said:

I have been one of the biggest advocates of financing cars, and still am, however, the PCP deals are bordering on a scam and mis selling imho, especially on used cars where the APR is sky high.

I just borrowed £30k from Hitachi Capital Finance for 2.89% at £537 a month.

BMW wanted me to borrow from them at only £527 a month.

He said that ''We Guarantee your car will be worth £13000 at the end of the term."

I kept saying "No, you guarantee that if I want to keep my car at the end of the term I will have to give you an additional £13,000 for the privilege."

Considering this guy was selling finance it was scary the fact he simply didn't get what I was saying.

Currently people are paying the equivalent in extra interest to the balloon at the end, and that is why I think car finance will be the new PPI, it is bordering on mis selling.

I have no doubt PCP is no longer 'bordering' on being a scam, in a lot of instances it is being flat out missold.I just borrowed £30k from Hitachi Capital Finance for 2.89% at £537 a month.

BMW wanted me to borrow from them at only £527 a month.

He said that ''We Guarantee your car will be worth £13000 at the end of the term."

I kept saying "No, you guarantee that if I want to keep my car at the end of the term I will have to give you an additional £13,000 for the privilege."

Considering this guy was selling finance it was scary the fact he simply didn't get what I was saying.

Currently people are paying the equivalent in extra interest to the balloon at the end, and that is why I think car finance will be the new PPI, it is bordering on mis selling.

I have had two dealers, one a Honda and another a Renault, try to tell me on a PCP the final payment is not subject to interest. When they're charging >5%+ on a £30k that's quite a statement! I'm not one to defend those who fail to do their own due diligence, but I think it's scandalous what car salesman get away with spinning.

I like the idea of PCP, and like all successful products has some very useful attributes. However, it complicates the picture massively for the consumer to make an informed decision.

Scootersp said:

CS Garth said:

The canniest thing car markers have done in recent times is to make people view a car like a phone and completely obfuscate the actual price they are paying. So long as the wheels go round and a car has equity or parity in it then the corks keep popping, the minute negative equity creeps in (ie values soften) then the problems start. As with any credit boom.

Particularly influencing the young, wrapping up insurance sometimes into the deal, fewer youngsters (and their families) hands on with cars which increases the risk cost of a used car etc. Edited by CS Garth on Monday 27th March 11:09

It's a constant part of consumerism these days (always was but seems even more marketed/pushed now), that something is new/improved and therefore the great all singing and dancing thing 12 months ago is now obsolete and almost embarrassing to have! Nothing old is worth caring for, image is almost everything and (may be I'm old!) but this seems really bad in the youth (£200+ must have football boots anyone?)

I'm not sure the wheels will fall off yet, it suits everyone in the main so it seems, manufacturers and us and a slow in sales will probably see more incentives/deals and perhaps the odd uncompetitive/'struggling more than others' manufacturer will go at some point?

Low wages and cheap, near-unlimited finance mean everyone is drifting toward an era where they share or rent a house, vehicle and phone.

daemon said:

I dont know of too many PCP car owners who view them as just "renting" the car. Any we've had in the past we've never treated it as anything other than "our" car.

Likewise if i was buying a 2-3 year old car, i'd be very jumpy about buying from a car supermarket - i'd rather pay the bit extra (and often not that much extra) and get one from a franchised dealer with an approved used warranty.

Also being a cash buyer of a new car (if you can find them any more?) doesnt guarantee its going to be treated any better - it "might - particularly if its a performance car - but likewise "mechanical sympathy" is rare these days.

Thats the game of chess we all play in the second hand market, risk buying a used year car enjoy another 5/7 years from it with a potential bills of £2000 - £4000 along the way with a few days faffing, or change your car when the warranty runs out every 3 years at a cost of £20,000 - £30,000 each time (if looking at more expensive metal) suddenly the used car doesn't look so expensive to run, cos changing twice in that same period could be as much as £60,000! (yes worst extreme). Same story adding up those big lease payments over 6 years. Likewise if i was buying a 2-3 year old car, i'd be very jumpy about buying from a car supermarket - i'd rather pay the bit extra (and often not that much extra) and get one from a franchised dealer with an approved used warranty.

Also being a cash buyer of a new car (if you can find them any more?) doesnt guarantee its going to be treated any better - it "might - particularly if its a performance car - but likewise "mechanical sympathy" is rare these days.

Edited by johnnnnnnyy on Monday 27th March 13:40

I've bought all but one of my cars with cash and it's becoming increasingly like jumping through flaming hoops to do so at a main dealership.

My last one (£7k nearly new) was painful. Think I spent an hour once I'd already said I'd buy the car and agreed a price having to listen to finance deals (all of which got a blunt no from me). It then seemed like it was genuinely an issue for them to accept that much money in one hit.

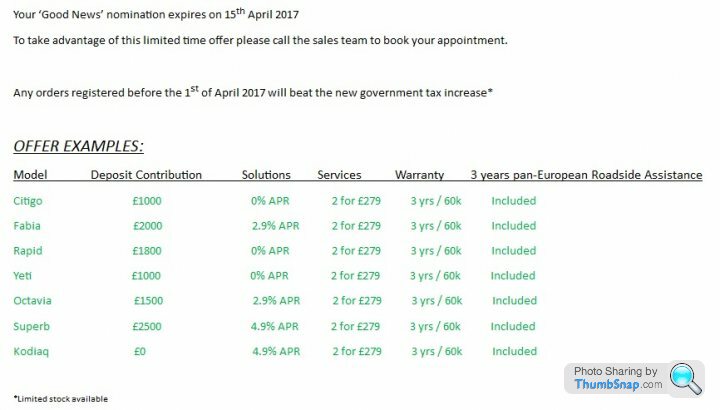

The car was exactly what I wanted so I put up with it all. Ironically ever since they've been sending me leaflets every few months with their latest finance offers, often they don't even include an actual price. This one arrived last week...

My last one (£7k nearly new) was painful. Think I spent an hour once I'd already said I'd buy the car and agreed a price having to listen to finance deals (all of which got a blunt no from me). It then seemed like it was genuinely an issue for them to accept that much money in one hit.

The car was exactly what I wanted so I put up with it all. Ironically ever since they've been sending me leaflets every few months with their latest finance offers, often they don't even include an actual price. This one arrived last week...

johnnnnnnyy said:

Thats the game of chess we all play in the second hand market, risk buying a used year car enjoy another 5/7 years from it with a potential bills of £2000 - £4000 along the way with a few days faffing, or change your car when the warranty runs out every 3 years at a cost of £20,000 - £30,000 each time (if looking at more expensive metal) suddenly the used car doesn't look so expensive to run, cos changing twice in that same period could be as much as £60,000! (yes worst extreme). Same story adding up those big lease payments over 6 years.

If something is losing £20-30k in five years then the price is going to be something in the region of £50k new.If you buy a three-year-old car that was £50k new (let's say, a Jag XJ for £24k) then it'll lose the thick end of £20k in depreciation over the next six years. Let's call it £18k - £6k trade-in would be decent for this car at 9 years old: https://www.cargiant.co.uk/car/jaguar/xj/YT14EOH

Let's take the mid-point of your estimate on the repair bills - £3k.

So your cost of ownership over three years, against something that might lose £60k in six years if bought new - is £21k. That makes your overall cost of a used car £350 per month all in. That gives you a £286/month lease budget on a 9+35. While it won't get you a brand new XJ, it would get you a brand new E Class. I don't think someone who leases is crazy for choosing the convenience of a brand new E-Class that never gets over three years old vs. what will eventually be an eight-year-old Jag.

ukaskew said:

I've bought all but one of my cars with cash and it's becoming increasingly like jumping through flaming hoops to do so at a main dealership.

My last one (£7k nearly new) was painful. Think I spent an hour once I'd already said I'd buy the car and agreed a price having to listen to finance deals (all of which got a blunt no from me). It then seemed like it was genuinely an issue for them to accept that much money in one hit.

The car was exactly what I wanted so I put up with it all. Ironically ever since they've been sending me leaflets every few months with their latest finance offers, often they don't even include an actual price. This one arrived last week...

Even so, where's the monthly payment on those 'deals'?My last one (£7k nearly new) was painful. Think I spent an hour once I'd already said I'd buy the car and agreed a price having to listen to finance deals (all of which got a blunt no from me). It then seemed like it was genuinely an issue for them to accept that much money in one hit.

The car was exactly what I wanted so I put up with it all. Ironically ever since they've been sending me leaflets every few months with their latest finance offers, often they don't even include an actual price. This one arrived last week...

CYMR0 said:

If something is losing £20-30k in five years then the price is going to be something in the region of £50k new.

If you buy a three-year-old car that was £50k new (let's say, a Jag XJ for £24k) then it'll lose the thick end of £20k in depreciation over the next six years. Let's call it £18k - £6k trade-in would be decent for this car at 9 years old: https://www.cargiant.co.uk/car/jaguar/xj/YT14EOH

Let's take the mid-point of your estimate on the repair bills - £3k.

So your cost of ownership over three years, against something that might lose £60k in six years if bought new - is £21k. That makes your overall cost of a used car £350 per month all in. That gives you a £286/month lease budget on a 9+35. While it won't get you a brand new XJ, it would get you a brand new E Class. I don't think someone who leases is crazy for choosing the convenience of a brand new E-Class that never gets over three years old vs. what will eventually be an eight-year-old Jag.

While I agree with your sentiment, you've equated 6 years of the second hand Jag with 3 years of leasing the new Merc. If you buy a three-year-old car that was £50k new (let's say, a Jag XJ for £24k) then it'll lose the thick end of £20k in depreciation over the next six years. Let's call it £18k - £6k trade-in would be decent for this car at 9 years old: https://www.cargiant.co.uk/car/jaguar/xj/YT14EOH

Let's take the mid-point of your estimate on the repair bills - £3k.

So your cost of ownership over three years, against something that might lose £60k in six years if bought new - is £21k. That makes your overall cost of a used car £350 per month all in. That gives you a £286/month lease budget on a 9+35. While it won't get you a brand new XJ, it would get you a brand new E Class. I don't think someone who leases is crazy for choosing the convenience of a brand new E-Class that never gets over three years old vs. what will eventually be an eight-year-old Jag.

Venturist said:

CYMR0 said:

If something is losing £20-30k in five years then the price is going to be something in the region of £50k new.

If you buy a three-year-old car that was £50k new (let's say, a Jag XJ for £24k) then it'll lose the thick end of £20k in depreciation over the next six years. Let's call it £18k - £6k trade-in would be decent for this car at 9 years old: https://www.cargiant.co.uk/car/jaguar/xj/YT14EOH

Let's take the mid-point of your estimate on the repair bills - £3k.

So your cost of ownership over three years, against something that might lose £60k in six years if bought new - is £21k. That makes your overall cost of a used car £350 per month all in. That gives you a £286/month lease budget on a 9+35. While it won't get you a brand new XJ, it would get you a brand new E Class. I don't think someone who leases is crazy for choosing the convenience of a brand new E-Class that never gets over three years old vs. what will eventually be an eight-year-old Jag.

While I agree with your sentiment, you've equated 6 years of the second hand Jag with 3 years of leasing the new Merc. If you buy a three-year-old car that was £50k new (let's say, a Jag XJ for £24k) then it'll lose the thick end of £20k in depreciation over the next six years. Let's call it £18k - £6k trade-in would be decent for this car at 9 years old: https://www.cargiant.co.uk/car/jaguar/xj/YT14EOH

Let's take the mid-point of your estimate on the repair bills - £3k.

So your cost of ownership over three years, against something that might lose £60k in six years if bought new - is £21k. That makes your overall cost of a used car £350 per month all in. That gives you a £286/month lease budget on a 9+35. While it won't get you a brand new XJ, it would get you a brand new E Class. I don't think someone who leases is crazy for choosing the convenience of a brand new E-Class that never gets over three years old vs. what will eventually be an eight-year-old Jag.

Get rid of the Jag after five years (versus six) and £3k of bills and the cost is comparable to leasing an E-Class. Keep it nine years with no major problems and you're comfortably ahead.

Edited by CYMR0 on Monday 27th March 14:06

Edited by CYMR0 on Monday 27th March 14:10

ukaskew said:

I've bought all but one of my cars with cash and it's becoming increasingly like jumping through flaming hoops to do so at a dealership.

My last one (£7k nearly new) was painful. Think I spent an hour once I'd already said I'd buy the car and agreed a price having to listen to finance deals (all of which got a blunt no from me). It then seemed like it was genuinely an issue for them to accept that much money in one hit.

The car was exactly what I wanted so I put up with it all. Ironically ever since they've been sending me leaflets every few months with their latest finance offers, often they don't even include an actual price. This one arrived last week...

This in itself sort of proves that it's good for them above all else. The crucial thing for them is the constant cycle, if thousands of people got to an end of term on their car such that no decision had to be made, they just were in a position to carry on using it and suddenly have zero monthly payment (like a used car bank loan situation) then many thousands of these would actually be quite happy with the car and keep using it and then be quite pleasantly surprised at the extra cash they've got left over. My last one (£7k nearly new) was painful. Think I spent an hour once I'd already said I'd buy the car and agreed a price having to listen to finance deals (all of which got a blunt no from me). It then seemed like it was genuinely an issue for them to accept that much money in one hit.

The car was exactly what I wanted so I put up with it all. Ironically ever since they've been sending me leaflets every few months with their latest finance offers, often they don't even include an actual price. This one arrived last week...

The current situations, mean as the end of term looms a decision needs to be made, back to square one with an end of lease or faced with a massive balloon payment and 4-5 years more of the same 'per months' to own a 3+ year old car (you are probably bored with!) seems bad compared to getting into a new one for the same 'per month' cost. Then you are on the hook, used to the nice new(er) car every few years and it feels fine, probably is fine to most and at the end of the day it's all personal choice, but it's hard to 'downgrade' in any part of life so once that nice new lease is over, even if you feel it cost you more than you'd like, is a well used car going to appeal? to many not only would it not appeal it's now become 'simply not an option' in their heads. To lot's of people it's non issue and their personal finances are such it's convenient above all else. The dealers have certainly managed to get more of a percentage of those not quite so secure financially and where certainly in the past these people would have been (for better or worse)in far older used cars.

I am not an accountant or someone with a special interested in finance matters.

However, isn't this the way the economy has been driven for a while now? Credit and the associated costs with it?

I remember seeing a piece on the news late last year with the presenter stood in a furniture shop. She was pointing to the 'buy now, pay later' and 'x%' credit deals saying this is how the government want the economy run. Or have I got that wrong?

The only thing I have on finance is the house. I'm not really interested in taking finance out on anything else if I can avoid it.

However, isn't this the way the economy has been driven for a while now? Credit and the associated costs with it?

I remember seeing a piece on the news late last year with the presenter stood in a furniture shop. She was pointing to the 'buy now, pay later' and 'x%' credit deals saying this is how the government want the economy run. Or have I got that wrong?

The only thing I have on finance is the house. I'm not really interested in taking finance out on anything else if I can avoid it.

CYMR0 said:

3. The thing is... I can go and buy a base model Golf for £14,500 right now, brand new. Admittedly it will be sackcloth spec and couldn't pull the skin off a rice pudding, but the build cost won't be that different from a slightly nicer Match - certainly not £2k less.

I didn't know they were that low - can you point me towards one, please? We've got a mk6 in the family that was £13K which seemed amazing at the time (2011). Match model was nudging £20K.CYMR0 said:

So, even in this pretty dire scenario for the manufacturer they've given me 1/3 off an excessive list price and still made more money than they would on a poverty spec model. The finance company might be recording a loss, but as it's manufacturer owned, that loss is more than offset by the margin (not profit after overhead) on the car.

The pure manufacturing cost of making a car is pretty low and PCP was particularly designed to keep factories running at full capacity - it's a disaster if they're only making 50 cars an hour on a line geared up to make 60.I think the thing to bear in mind would be where would you be if you lost your job/income. With a PCP you'd have to hand it back, and luckily you might not be in debt.

If you had a loan, you would own the car. You could sell it to cover the finance and more than likely be able to buy a cheap used car to get back on the road.

Your image would suffer though (but only in your mind).

If you had a loan, you would own the car. You could sell it to cover the finance and more than likely be able to buy a cheap used car to get back on the road.

Your image would suffer though (but only in your mind).

Sheepshanks said:

CYMR0 said:

3. The thing is... I can go and buy a base model Golf for £14,500 right now, brand new. Admittedly it will be sackcloth spec and couldn't pull the skin off a rice pudding, but the build cost won't be that different from a slightly nicer Match - certainly not £2k less.

I didn't know they were that low - can you point me towards one, please? We've got a mk6 in the family that was £13K which seemed amazing at the time (2011). Match model was nudging £20K.Audemars said:

Most people can not negotiate a decent mobile phone deal. How do you expect them to negotiate one for a big ticket item such as a car.

Despite all the leasing/PCP going on, used car prices across the board are about 50% overpriced.

There is definitely a bubble.

Used cars in the UK are among the cheapest in the world. Take a look at the used car market in the US.Despite all the leasing/PCP going on, used car prices across the board are about 50% overpriced.

There is definitely a bubble.

Gassing Station | General Gassing | Top of Page | What's New | My Stuff