Windscreen Claims WILL Affect Your NCD

Discussion

Glassman said:

LoonR1 said:

And to bring some closure I've quoted your opening post below. It's clear that you have chosen Hastings Direct as the prompt for this whole thread over 4 years ago. Here's the Hastings booklet

http://www.hastingsdirect.com/documents/Policy_doc...

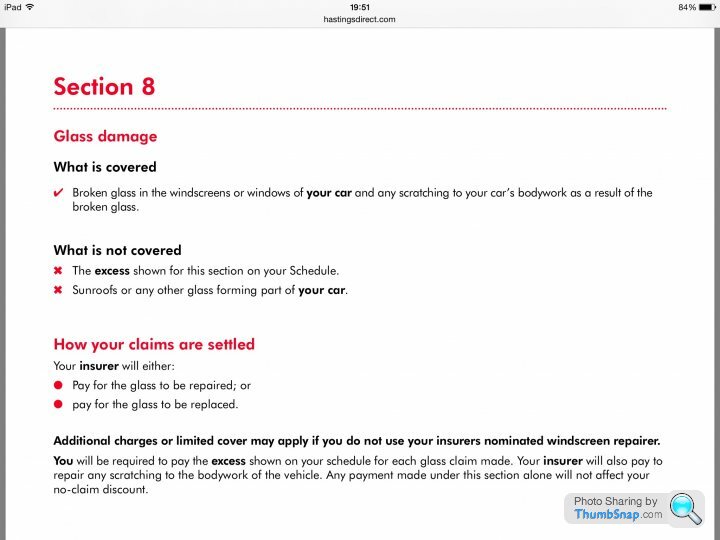

Section 8 page 25

http://www.hastingsdirect.com/about-us/news/100726.htmlhttp://www.hastingsdirect.com/documents/Policy_doc...

Section 8 page 25

Glassman said:

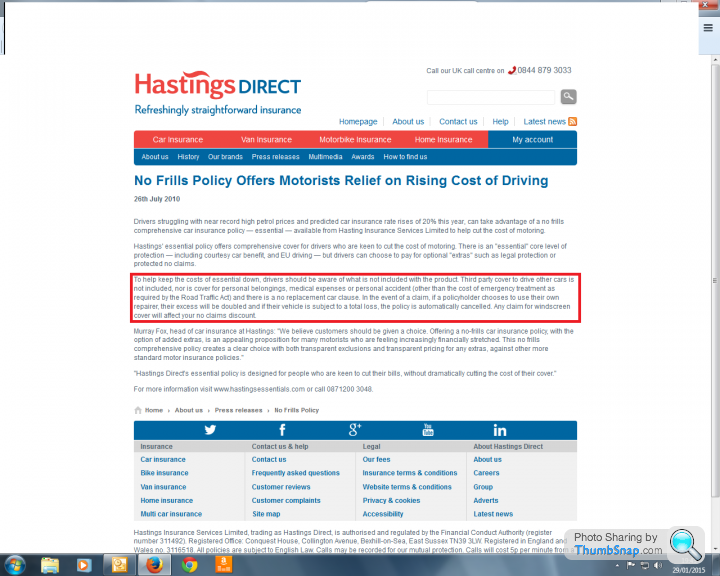

Hastings Direct are reported to be revising their policies to include a few interesting changes, one stands out quite clearly: "windscreen claims will affect no claims discounts and excesses will be doubled if policyholders choose their own repairer." This is to enable HD to offer drivers a 'no frills comprehensive car insurance policy to help cut motoring costs.

Furthermore, Equity Red Star, Fortis and NIG are to withdraw from personal lines, ie, private motor insurance (according to a broker in London). These are the type of policies that are bread and butter to a lot of brokers; with price online sales and price comparison websites it's a tough business for the motor insurance broker. But it's not just the guys in the broker world, with these changes to Key Facts and underwriters pulling out of motor insurance, is this the industry stepping sideways?

For the policyholder (with HD) this means (in the event of a windscreen claim) you will go with who we tell you to, or you get your wallet spanked.

Furthermore, Equity Red Star, Fortis and NIG are to withdraw from personal lines, ie, private motor insurance (according to a broker in London). These are the type of policies that are bread and butter to a lot of brokers; with price online sales and price comparison websites it's a tough business for the motor insurance broker. But it's not just the guys in the broker world, with these changes to Key Facts and underwriters pulling out of motor insurance, is this the industry stepping sideways?

For the policyholder (with HD) this means (in the event of a windscreen claim) you will go with who we tell you to, or you get your wallet spanked.

Can we stop now as this is going in circles.

Can you please show me your staff salaries please, otherwise you're just proving to me that you pay below minimum wage.

sampsan said:

Glassman said:

sampsan said:

I used Autoglass, rang for a quote as was going to pay myself. That will be £175 sir, great please complete the work.

On the day of the works, fitter turned up with paperwork. He suggested that I could claim on my insurance and without thinking signed the forms and work was completed. Didn't think much more of it.

Some time later received a letter from my insurance company stating they had received a invoice from Autoglass and I was not covered for Windscreen therefore please find enclosed the invoice to pay directly.

No issues, my fault and should have checked the policy.

Then........ noticed the Autoglass invoice to the insurance company was not the £175 quoted but had risen to £480.

Following this had a major fall out with them where they denied the quote and refused to reduce the costs, this got silly with me telling them to come and remove the windscreen and take it away. Anyway eventually agreed on a reasonable amount but have never dealt with people so aggressive and unwilling to say anything apart from give me your money.

So lessons learnt.... they rip off insurance companies and always get a quote in writing.

Are you sure it was Autoglass, and not the Camorra? On the day of the works, fitter turned up with paperwork. He suggested that I could claim on my insurance and without thinking signed the forms and work was completed. Didn't think much more of it.

Some time later received a letter from my insurance company stating they had received a invoice from Autoglass and I was not covered for Windscreen therefore please find enclosed the invoice to pay directly.

No issues, my fault and should have checked the policy.

Then........ noticed the Autoglass invoice to the insurance company was not the £175 quoted but had risen to £480.

Following this had a major fall out with them where they denied the quote and refused to reduce the costs, this got silly with me telling them to come and remove the windscreen and take it away. Anyway eventually agreed on a reasonable amount but have never dealt with people so aggressive and unwilling to say anything apart from give me your money.

So lessons learnt.... they rip off insurance companies and always get a quote in writing.

LoonR1 said:

Can you please show me your staff salaries please, otherwise you're just proving to me that you pay below minimum wage.

About as related to the subject as the relationship between NCD and loading premiums following a glass claim. At the time of starting the thread, the statement in the OP was pretty bang on and true. You claim to debunk the claim the title of this thread, but a) you confirm there's at least one insurer who will frig a PH's NCD following a glass claim, and b) Hastings Direct state this which, at the time was true. No date confusion, and link with corresponding date/timestamp provided.

Others have stated that there may be a premium issue subsequent to a glass claim; again, Hastings (from the link you very kindly provided) state in Section 9:

"No-claim discount

"If you have protected no-claims discount, there is no guarantee that your premium will not increase".

Yet you're digging your heels in stating that the insurers are 'not bothered' by glass claims. In another post you say a 'claim' is a perceived risk, etc...

I'm just trying to understand which part(s) are correct. References are always good back up. What I pay, whether I pay; to whom I pay has no relevance whatsoever.

One. One insurer on one product out of hundreds. Even that insurer has three direct offerings and this was on one of those offerings. I don't think it even exists anymore

I can't show you underwriting criteria as its the competitive advantage that an insurer has and it's how they make money. They won't share this.

It's getting boring repeating this

Can I come into your business and get all the details of how you make money please. I'll takenit to your competitors and see how long survive.

I can't show you underwriting criteria as its the competitive advantage that an insurer has and it's how they make money. They won't share this.

It's getting boring repeating this

Can I come into your business and get all the details of how you make money please. I'll takenit to your competitors and see how long survive.

One. One insurer on one product out of hundreds. Even that insurer has three direct offerings and this was on one of those offerings. I don't think it even exists anymore

I can't show you underwriting criteria as its the competitive advantage that an insurer has and it's how they make money. They won't share this.

It's getting boring repeating this

Can I come into your business and get all the details of how you make money please. I'll takenit to your competitors and see how long survive.

I can't show you underwriting criteria as its the competitive advantage that an insurer has and it's how they make money. They won't share this.

It's getting boring repeating this

Can I come into your business and get all the details of how you make money please. I'll takenit to your competitors and see how long survive.

Glassman said:

Yet you're digging your heels in stating that the insurers are 'not bothered' by glass claims. In another post you say a 'claim' is a perceived risk, etc...

Maybe the insurance industry doesn't like the fact their NCB con is being rumbled. Said it before but will say it again because it's appropriate. The insurance industry has pulled a blinder with NCB, scaring people out of claiming for something they have paid for because they might loose some NCB discount. People wake up, NCB is a discount on your base premium which is as open to manipulation as any other variable without open justification

Edited by crossy67 on Thursday 29th January 20:44

LoonR1 said:

Can I come into your business and get all the details of how you make money please. I'll takenit to your competitors and see how long survive.

Will a glass claim affect NCD? Not with all insurers. OK then, will my premium rise as a result of a glass claim. IOW, is there a claw-back, or are the insurers hiding behind the NCD thing but will still hike up the premium under a different guise etc etc? It's this bit that most people think is true and some are presenting themselves as case examples. You say this is b

ks. A simple bit of evidence will suffice. Nothing to do with margins, profit, inside leg measurements or anything else. What's so secretive about it? Does a windscreen claim mean mine premium will go up as a result. You say no. Others say yes. They have the premium (and their insurer's words to back it up). You go all stush about it.

ks. A simple bit of evidence will suffice. Nothing to do with margins, profit, inside leg measurements or anything else. What's so secretive about it? Does a windscreen claim mean mine premium will go up as a result. You say no. Others say yes. They have the premium (and their insurer's words to back it up). You go all stush about it. It's so secretive because it's part of their underwriting factors. They don't share this data. It's not because they see it as a way to scam people it's because they use this to set their premiums.

However, glass claims are a mimor costs in the bigger scheme

Never going to convince you and you're never going to want to be convinced. you don't seem to want to share those details I asked for either. Why not?

However, glass claims are a mimor costs in the bigger scheme

Never going to convince you and you're never going to want to be convinced. you don't seem to want to share those details I asked for either. Why not?

crossy67 said:

Maybe the insurance industry doesn't like the fact their NCB con is being rumbled. Said it before but will say it again because it's appropriate. The insurance industry has pulled a blinder with NCB, scaring people out of claiming for something they have paid for because they might loose some NCB discount. People wake up, NCB is a discount on your base premium which is as open to manipulation as any other variable without open justification

Tinfoil. Get your tinfoil here. Edited by crossy67 on Thursday 29th January 20:44

Glassman said:

LoonR1 said:

you don't seem to want to share those details I asked for either. Why not?

Because it's unrelated? No parallels can be drawn from it, and it's not something that would help motorists. I've heard that you pay less than minimum wage.

See how consistently repeating stuff that is irrelevant can be frustrating n

It was better off locked, the conversation will just go around in circles.

Window claims generally don't affect NCD bar one or two insurers.

They may affect premiums but there are so many other factors that it's not easily quantified and to do so would require insurers to release company sensitive data which we won't.

The question has been answered.

Leave it locked I say.

Window claims generally don't affect NCD bar one or two insurers.

They may affect premiums but there are so many other factors that it's not easily quantified and to do so would require insurers to release company sensitive data which we won't.

The question has been answered.

Leave it locked I say.

Glassman said:

Loon, would you say that not declaring a windscreen claim would be deemed as non disclosure of a material fact?

Sorry answering because I think this has been debated before If I was asked "have I claimed for a windscreen in the last 5 years" I'd answer it - but I've never been asked in 30 years

Gassing Station | General Gassing | Top of Page | What's New | My Stuff