PCP deal calculation help

Discussion

I'm lost as well. What was the specific question?

I'm lost as well. What was the specific question?

Dr Jekyll said:

The implication is that it's the interest on the PCP balloon that's unsurprisingly more than the interest on the decreasing HP balance.

Ok, so he's talking about a scenario that won't exist - the overall cost to buy the car - rather than the overall cost of the car whilst he has it.TA14 said:

Dr Jekyll said:

The implication is that it's the interest on the PCP balloon that's unsurprisingly more than the interest on the decreasing HP balance.

Ok, so he's talking about a scenario that won't exist - the overall cost to buy the car - rather than the overall cost of the car whilst he has it.HP would effectively mean paying off the residual as he went along, so less interest incurred.

Dr Jekyll said:

HP would effectively mean paying off the residual as he went along, so less interest incurred.

Surely a matching APR would say otherwise?For example, BMW are quoting 4.9% APR on their PCP deals, so presumably a 4.9% APR loan would have the same Annual Percentage Rate?

Interestingly, the cheapest APR i could get there with a quick check online for a £30,000 loan was 5.9% APR.

daemon said:

Dr Jekyll said:

HP would effectively mean paying off the residual as he went along, so less interest incurred.

Surely a matching APR would say otherwise?For example, BMW are quoting 4.9% APR on their PCP deals, so presumably a 4.9% APR loan would have the same Annual Percentage Rate?

Finance £20,000 on a PCP with £10,000 balloon. Start off owing £20,000, end up owing £10,000, so on average paying interest on just over £15,000.

Finance £20,000 over the same period on HP. Start off owing £20,000, end up owing zero, so on average paying interest on just over £10,000.

TA14 said:

Ok, so he's talking about a scenario that won't exist - the overall cost to buy the car - rather than the overall cost of the car whilst he has it.

Sorry, I'm still not with you as to what your question is?To clarify what I think you are getting at, is that I am paying interest on the whole of the GFV sum for the full term of the loan. Conversely, with a HP arrangement, the pricipal amount would be decreasing month on month with every payment, therefore the interest accrued on the HP loan would be less than the interest accrued on the PCP loan.

crazy about cars said:

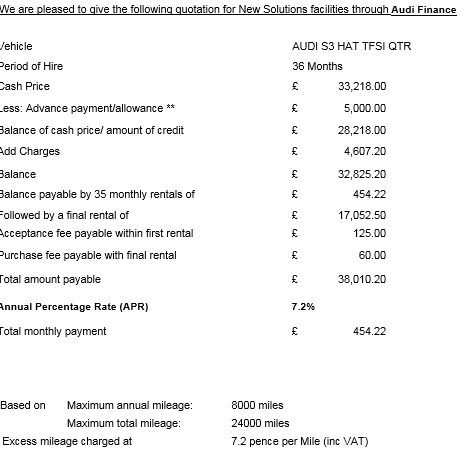

This was the final quote I've got. It's definitely better than the previous offer but I just don't feel comfortable enough paying over 400/month renting.

The notion of "renting" the car is a red herring, and a lot of people incorrectly get hung up on that point.Imagine that you buy a new car with cash and sell it in 3 years time. You will lose £x based on the car's depreciation and you will have no car once you sell it. Even though you initially bought the car outright with cash, you have effectively rented the car for £x/36 per month.

IMO, to work out if the deal is good for you, compare the total cost of ownership with the different payment methods (cash, HP, PCP, lease, etc) over the term that you want, to see which offers you most value for money, flexibility, etc.

Mandat said:

The notion of "renting" the car is a red herring, and a lot of people incorrectly get hung up on that point.

Imagine that you buy a new car with cash and sell it in 3 years time. You will lose £x based on the car's depreciation and you will have no car once you sell it. Even though you initially bought the car outright with cash, you have effectively rented the car for £x/36 per month.

IMO, to work out if the deal is good for you, compare the total cost of ownership with the different payment methods (cash, HP, PCP, lease, etc) over the term that you want, to see which offers you most value for money, flexibility, etc.

Agreed. If only Audi could discount closer to 4k I'd definitely go ahead. I can afford it but I just don't feel comfortable committing if that makes sense. If it's 450/month but I'll own the car (no GFV) then it's a different story.Imagine that you buy a new car with cash and sell it in 3 years time. You will lose £x based on the car's depreciation and you will have no car once you sell it. Even though you initially bought the car outright with cash, you have effectively rented the car for £x/36 per month.

IMO, to work out if the deal is good for you, compare the total cost of ownership with the different payment methods (cash, HP, PCP, lease, etc) over the term that you want, to see which offers you most value for money, flexibility, etc.

crazy about cars said:

This was the final quote I've got. It's definitely better than the previous offer but I just don't feel comfortable enough paying over 400/month renting.

You'd be nuts to do a deal like this IMO especially given recent Golf R lease deals.Also I know new vs secondhand isn't comparable but there was an approved used rs4 convertible in sprint blue recently with 20kish miles for just over £20k with two years audi warranty.... I'd rather be driving that.

Total cost of ownership will be faaaaaaaaar cheaper and faaaaaar more enjoyable with pretty much all the benefits of new car warranty.

Froomee said:

crazy about cars said:

This was the final quote I've got. It's definitely better than the previous offer but I just don't feel comfortable enough paying over 400/month renting.

You'd be nuts to do a deal like this IMO especially given recent Golf R lease deals.Also I know new vs secondhand isn't comparable but there was an approved used rs4 convertible in sprint blue recently with 20kish miles for just over £20k with two years audi warranty.... I'd rather be driving that.

Total cost of ownership will be faaaaaaaaar cheaper and faaaaaar more enjoyable with pretty much all the benefits of new car warranty.

crazy about cars said:

Mandat said:

The notion of "renting" the car is a red herring, and a lot of people incorrectly get hung up on that point.

Imagine that you buy a new car with cash and sell it in 3 years time. You will lose £x based on the car's depreciation and you will have no car once you sell it. Even though you initially bought the car outright with cash, you have effectively rented the car for £x/36 per month.

IMO, to work out if the deal is good for you, compare the total cost of ownership with the different payment methods (cash, HP, PCP, lease, etc) over the term that you want, to see which offers you most value for money, flexibility, etc.

Agreed. If only Audi could discount closer to 4k I'd definitely go ahead. I can afford it but I just don't feel comfortable committing if that makes sense. If it's 450/month but I'll own the car (no GFV) then it's a different story.Imagine that you buy a new car with cash and sell it in 3 years time. You will lose £x based on the car's depreciation and you will have no car once you sell it. Even though you initially bought the car outright with cash, you have effectively rented the car for £x/36 per month.

IMO, to work out if the deal is good for you, compare the total cost of ownership with the different payment methods (cash, HP, PCP, lease, etc) over the term that you want, to see which offers you most value for money, flexibility, etc.

crazy about cars said:

CarlT said:

You would if you paid £450 or so a month...

Not in the PCP scenario. crazy about cars said:

This was the final quote I've got. It's definitely better than the previous offer but I just don't feel comfortable enough paying over 400/month renting.

What discount are they giving you? And I would want that APR at 5% max. Just go back to them with what you are willing to/are happy with, they can only say no, and if so you walk.

Gassing Station | General Gassing | Top of Page | What's New | My Stuff