Portfolio Ideas

Discussion

Hi all,

I have been a lurker on these finance forums for a while and thought I would finally take the plunge, sign up and ask for some advice.

I am a first time investor, I have approx £500 a month to invest, with an outlook of never really needing the money. I may have been reading too many financial independence blogs, but my intention is to invest the £500 a month into a stocks and shares ISA and let it grow for 30 years or so (reinvesting dividends for all this period until I get to the stage where I want/need the money for my 'financial independence').

For background, I'm 28 work in London in a secure job with progression and already pay into a decent workplace pension. Have a house (with 80% LTV mortgage), gf but no kids, and probably none for a couple of years. Even when they come though it shouldn't affect my ability to invest the £500 a month.

I've put together the below portfolio and I am about to pull the trigger (investing £200 into each fund to start with and then £500 split across them monthly).

Aberdeen Latin American Equity I Acc

Aviva Inv UK Property 2 Acc

CF Woodford Equity Income Z Acc GBP

iShares Emerging Markets Equity Index (UK) H Acc

iShares Japan Equity Index (UK) H Acc

iShares Pacific ex Japan Equity Index (UK) H Acc

iShares UK Equity Index (UK) D Acc

Jupiter India I Acc

L&G European Index Trust C Acc

L&G US Index Trust C Acc

Vanguard Global Bond Index Hedged Acc GBP

Vanguard LifeStrategy 80% Equity A

My reasoning for the choices are I want to have as diverse a portfolio as possible, with exposure to basically the emerging markets and most of the developed markets. Fairly high risk tolerant given my time outlook and the fact I don't need the money. I also don't want to be too heavily invest in one fund for fear of a catastrophe hitting that fund in particular, hence I'm not chucking it all in the Lifestrategy 80.

All choices seem fairly low in expenses. Any obvious pitfalls I've fallen into / any advice for a beginner. My main concern is I have gone overkill on the number of funds.

I have been a lurker on these finance forums for a while and thought I would finally take the plunge, sign up and ask for some advice.

I am a first time investor, I have approx £500 a month to invest, with an outlook of never really needing the money. I may have been reading too many financial independence blogs, but my intention is to invest the £500 a month into a stocks and shares ISA and let it grow for 30 years or so (reinvesting dividends for all this period until I get to the stage where I want/need the money for my 'financial independence').

For background, I'm 28 work in London in a secure job with progression and already pay into a decent workplace pension. Have a house (with 80% LTV mortgage), gf but no kids, and probably none for a couple of years. Even when they come though it shouldn't affect my ability to invest the £500 a month.

I've put together the below portfolio and I am about to pull the trigger (investing £200 into each fund to start with and then £500 split across them monthly).

Aberdeen Latin American Equity I Acc

Aviva Inv UK Property 2 Acc

CF Woodford Equity Income Z Acc GBP

iShares Emerging Markets Equity Index (UK) H Acc

iShares Japan Equity Index (UK) H Acc

iShares Pacific ex Japan Equity Index (UK) H Acc

iShares UK Equity Index (UK) D Acc

Jupiter India I Acc

L&G European Index Trust C Acc

L&G US Index Trust C Acc

Vanguard Global Bond Index Hedged Acc GBP

Vanguard LifeStrategy 80% Equity A

My reasoning for the choices are I want to have as diverse a portfolio as possible, with exposure to basically the emerging markets and most of the developed markets. Fairly high risk tolerant given my time outlook and the fact I don't need the money. I also don't want to be too heavily invest in one fund for fear of a catastrophe hitting that fund in particular, hence I'm not chucking it all in the Lifestrategy 80.

All choices seem fairly low in expenses. Any obvious pitfalls I've fallen into / any advice for a beginner. My main concern is I have gone overkill on the number of funds.

Thoughts - written in a slight rush I'm afraid:

If you're looking at ~30 years, why not LS 100 rather than 80? - in fact why buy any bonds at all?

Similarly, over that long a time horizon I wouldn't bother with hedged funds - the hedging will cost you a little return each year, and probably exceed in cost any likely net exchange rate movement it's hedging against.

Why a UK property fund - there's no other property fund in there - what's special about the UK?

You've listed funds from most regions - why in that case buy a global fund like LifeStrategy - I'd suggest feeding what you've picked into Morningstar's x-ray tool and thinking about the resulting regional allocation with an even split - typically I start with a weighting that matches each market's share of the global capitalisation (so the US market is huge, similarly it's by default heavily weighted in a market cap matching portfolio).

You're going to be investing ~£6000 a year. Fairly quickly you'll be at the point where a fixed cost broker will be the economic choice. Think if you want to be potentially incurring 12 sets of transaction fees each month, or if you want to trim the number of funds (or accept cheaper transaction fees in return for higher annual fees). You could invest in the funds on a rota, but that would probably mean monthly manual intervention.

IMHO, the odds of Vanguard encountering a catastrophe and the rest surviving are pretty low - I'd suggest a bigger argument against buying Lifestrategy is it's overweighted towards the UK, which you may not want, but there are plenty of world equity trackers you could buy and then overweight emerging markets with a couple of other funds rather than the number you're looking at, which would potentially save you trading costs.

If you're looking at ~30 years, why not LS 100 rather than 80? - in fact why buy any bonds at all?

Similarly, over that long a time horizon I wouldn't bother with hedged funds - the hedging will cost you a little return each year, and probably exceed in cost any likely net exchange rate movement it's hedging against.

Why a UK property fund - there's no other property fund in there - what's special about the UK?

You've listed funds from most regions - why in that case buy a global fund like LifeStrategy - I'd suggest feeding what you've picked into Morningstar's x-ray tool and thinking about the resulting regional allocation with an even split - typically I start with a weighting that matches each market's share of the global capitalisation (so the US market is huge, similarly it's by default heavily weighted in a market cap matching portfolio).

You're going to be investing ~£6000 a year. Fairly quickly you'll be at the point where a fixed cost broker will be the economic choice. Think if you want to be potentially incurring 12 sets of transaction fees each month, or if you want to trim the number of funds (or accept cheaper transaction fees in return for higher annual fees). You could invest in the funds on a rota, but that would probably mean monthly manual intervention.

IMHO, the odds of Vanguard encountering a catastrophe and the rest surviving are pretty low - I'd suggest a bigger argument against buying Lifestrategy is it's overweighted towards the UK, which you may not want, but there are plenty of world equity trackers you could buy and then overweight emerging markets with a couple of other funds rather than the number you're looking at, which would potentially save you trading costs.

xeny said:

Thoughts - written in a slight rush I'm afraid:

If you're looking at ~30 years, why not LS 100 rather than 80? - in fact why buy any bonds at all?

Similarly, over that long a time horizon I wouldn't bother with hedged funds - the hedging will cost you a little return each year, and probably exceed in cost any likely net exchange rate movement it's hedging against.

Why a UK property fund - there's no other property fund in there - what's special about the UK?

You've listed funds from most regions - why in that case buy a global fund like LifeStrategy - I'd suggest feeding what you've picked into Morningstar's x-ray tool and thinking about the resulting regional allocation with an even split - typically I start with a weighting that matches each market's share of the global capitalisation (so the US market is huge, similarly it's by default heavily weighted in a market cap matching portfolio).

You're going to be investing ~£6000 a year. Fairly quickly you'll be at the point where a fixed cost broker will be the economic choice. Think if you want to be potentially incurring 12 sets of transaction fees each month, or if you want to trim the number of funds (or accept cheaper transaction fees in return for higher annual fees). You could invest in the funds on a rota, but that would probably mean monthly manual intervention.

IMHO, the odds of Vanguard encountering a catastrophe and the rest surviving are pretty low - I'd suggest a bigger argument against buying Lifestrategy is it's overweighted towards the UK, which you may not want, but there are plenty of world equity trackers you could buy and then overweight emerging markets with a couple of other funds rather than the number you're looking at, which would potentially save you trading costs.

Thanks for your response. On the Bonds, I included them to give myself a little bit of comfort given everything I have read about having a multi-asset portfolio. Also given the rising market we have had over the last few years, I am not sure I personally think (although what do I know) 100% stock investment is a good idea, even given the timeframe. If you're looking at ~30 years, why not LS 100 rather than 80? - in fact why buy any bonds at all?

Similarly, over that long a time horizon I wouldn't bother with hedged funds - the hedging will cost you a little return each year, and probably exceed in cost any likely net exchange rate movement it's hedging against.

Why a UK property fund - there's no other property fund in there - what's special about the UK?

You've listed funds from most regions - why in that case buy a global fund like LifeStrategy - I'd suggest feeding what you've picked into Morningstar's x-ray tool and thinking about the resulting regional allocation with an even split - typically I start with a weighting that matches each market's share of the global capitalisation (so the US market is huge, similarly it's by default heavily weighted in a market cap matching portfolio).

You're going to be investing ~£6000 a year. Fairly quickly you'll be at the point where a fixed cost broker will be the economic choice. Think if you want to be potentially incurring 12 sets of transaction fees each month, or if you want to trim the number of funds (or accept cheaper transaction fees in return for higher annual fees). You could invest in the funds on a rota, but that would probably mean monthly manual intervention.

IMHO, the odds of Vanguard encountering a catastrophe and the rest surviving are pretty low - I'd suggest a bigger argument against buying Lifestrategy is it's overweighted towards the UK, which you may not want, but there are plenty of world equity trackers you could buy and then overweight emerging markets with a couple of other funds rather than the number you're looking at, which would potentially save you trading costs.

Hedged funds, I have to admit I simply hadn't realised I could get these funds (or similar) not hedged. UK property fund was there to get me over my craving for a buy to let, although I realise the fund is invested in commercial property rather than residential. I don't think I can get exposure to the UK residential market through funds from everything I have read, although I could have just missed something.

I don't think transaction fees are a concern, as I would be using Hargreaves Lansdown, and the regular saving on there doesn't have any charges I understand. I know they are not the cheapest platform but I am drawn in by the handy website.

Current country split for the above portfolio is as follows from Trustnet.

Regions Total(%)

UK 18.6

USA 16.4

Japan 6.0

Brazil 5.6

India 4.8

Australia 2.8

France 2.8

Germany 2.6

China 2.6

Other Holdings 38.0

Sector split is below:

Sectors Total(%)

Financials 19.3

Industrials 11.0

Gold 8.1

Consumer Goods 7.6

Health Care 7.4

Government Bonds 4.8

Technology 4.1

Consumer Services 4.0

Consumer Staples 3.1

Other Holdings 30.5

Will look into lowering the number of funds as you suggested as I had feared I had gone a bit overboard.

alienwarerandy said:

I am a first time investor, I have approx £500 a month to invest, with an outlook of never really needing the money. I may have been reading too many financial independence blogs, but my intention is to invest the £500 a month into a stocks and shares ISA and let it grow for 30 years or so (reinvesting dividends for all this period until I get to the stage where I want/need the money for my 'financial independence').

I've put together the below portfolio and I am about to pull the trigger (investing £200 into each fund to start with and then £500 split across them monthly).

All choices seem fairly low in expenses. Any obvious pitfalls I've fallen into / any advice for a beginner. My main concern is I have gone overkill on the number of funds.

I've put together the below portfolio and I am about to pull the trigger (investing £200 into each fund to start with and then £500 split across them monthly).

All choices seem fairly low in expenses. Any obvious pitfalls I've fallen into / any advice for a beginner. My main concern is I have gone overkill on the number of funds.

Well done for deciding to invest for your future. We are often told now that fewer people are saving for their future. I won't say too much here, but I just wonder whether some could save, but prefer to have short-life consumer goods instead.

I managed to do what you describe, but have never bought funds. Instead I cut out the middle men, many of whom have not performed as well for their clients as might be imagined.

Ref. your plan for diversification.

12 funds. I don't know, but say they might run holdings in 50 companies. That would be 600 companies.

Over 30 years, I gradually built up to having holdings in between 25 and 30 businesses. That is generally accepted as adequate diversification. If a complete failure does occur, it only involves one thirtieth.

Another commonly overlooked aspect, is that many FTSE 100 companies are really international trading businesses. Some even do very little business in the UK and might be trading in 200 different countries. So even with just one if those companies, you might have diversification into a great number of different currencies and economic markets.

Over 30 years, I suppose I have saved thousands of pounds in fees, and remember the quoted fee is not all that you will be paying.

If your employer happens to operate any employee share schemes, that is the first thing to consider. It can be compared to betting on a horse, after it has crossed the finish line. You do need the luck of being with a successful company, but otherwise 'max it out' because it is a no brainer.

Do you know that generally with bonds, the capital value moves inversely to interest rates? If you think interest rates will be moving down, then bonds should be good. I never forecast the future, but with interest rates near to zero, the lowest since I believe 1694, what do you think?

Edited by Jon39 on Thursday 19th October 22:49

Jon39 said:

Well done for deciding to invest for your future. We are often told now that fewer people are saving for their future. I won't say too much here, but I just wonder whether some could save, but prefer to have short-life consumer goods instead.

I managed to do what you describe, but have never bought funds. Instead I cut out the middle men, many of whom have not performed as well for their clients as might be imagined.

Ref. your plan for diversification.

12 funds. I don't know, but say they might run holdings in 50 companies. That would be 600 companies.

Over 30 years, I gradually built up to having holdings in between 25 and 30 businesses. That is generally accepted as adequate diversification. If a complete failure does occur, it only involves one thirtieth.

Another commonly overlooked aspect, is that many FTSE 100 companies are really international trading businesses. Some even do very little business in the UK and might be trading in 200 different countries. So even with just one if those companies, you might have diversification into a great number of different currencies and economic markets.

Over 30 years, I suppose I have saved thousands of pounds in fees, and remember the quoted fee is not all that you will be paying.

If your employer happens to operate any employee share schemes, that is the first thing to consider. It can be compared to betting on a horse, after it has crossed the finish line. You do need the luck of being with a successful company, but otherwise 'max it out' because it is a no brainer.

Do you know that generally with bonds, the capital value moves inversely to interest rates? If you think interest rates will be moving down, then bonds should be good. I never forecast the future, but with interest rates near to zero, the lowest since I believe 1694, what do you think?

Edited by Jon39 on Thursday 19th October 22:49

(i) I understand bonds generally do well when stocks do poorly, so given we are at all time high market levels, I thought including them as a small percentage of my portfolio over the long term would be beneficial, even if in the short term they take a bit of a battering if interest rates rise; and

(ii) from what I can see bonds have done reasonably over the last five years. The Vanguard Global Bond Index is up 16% cumulatively over the last 5 years, so I thought would potentially lower the risk of the portfolio over the long run rather than being 100% in stocks.

I do also want to build up a separate portfolio of direct equity holdings in certain companies, but wanted to get this portfolio up and running first as an almost set and forget (I will keep an eye on it every few months or so). Of the 30 businesses you have built up stakes in, are these all generally blue chip stocks in the FTSE 100, or have you also dabbled with a few more mid caps?

IMO you would be very unwise to buy shares in individual companies. At your level of investment you could choose 3 or 4 mainstream funds and put equal contributions into each of them.

Just cover a few main equity sectors such as UK, Global, Emerging and add a Bond fund if you think it will add a bit of protection.

Don't overthink it!

Just cover a few main equity sectors such as UK, Global, Emerging and add a Bond fund if you think it will add a bit of protection.

Don't overthink it!

alienwarerandy said:

Thanks for the advice.

(i) I understand bonds generally do well when stocks do poorly, so given we are at all time high market levels, ...

(ii) from what I can see bonds have done reasonably over the last five years.

I do also want to build up a separate portfolio of direct equity holdings in certain companies, but wanted to get this portfolio up and running first as an almost set and forget (I will keep an eye on it every few months or so). Of the 30 businesses you have built up stakes in, are these all generally blue chip stocks in the FTSE 100, or have you also dabbled with a few more mid caps?

(i) I understand bonds generally do well when stocks do poorly, so given we are at all time high market levels, ...

(ii) from what I can see bonds have done reasonably over the last five years.

I do also want to build up a separate portfolio of direct equity holdings in certain companies, but wanted to get this portfolio up and running first as an almost set and forget (I will keep an eye on it every few months or so). Of the 30 businesses you have built up stakes in, are these all generally blue chip stocks in the FTSE 100, or have you also dabbled with a few more mid caps?

It was a long and gradual process for me to learn and gain experience of this subject. First purchase long ago was a tiny £180 in one company, and now am fortunate to have two months each year, when total dividends reach five figures. To pass on that knowledge is impossible really. If anyone wants to be succesful with equity investment, they need to be interested to learn, and gradually gain experience themselves . You need the right mental approach as well. Rocky times will occur, portfolio values will fall and not everyone can cope with that. Lost sleep means don't get involved.

Ref (i) & (ii) Bonds, particularly government stocks, are fixed contracts if held to the maturity date. Inflation is usually the killer. I did buy some a long time ago, when interest rates were about 15% and inflation was falling. Interest rates did fall and I sold with a 30% gain, but have never bought any since.

Yes, my favourites are FTSE 100, non cyclical, defensive, international companies. Plenty of diversification and spread of risk. To achieve rising share prices, you need growing profits, so business selection is crucial. The majority of my holdings have remained the same for 20 years. If overall you are generally beating the market average, then leave everything alone. In the early days, I did the usual newbie penny share type trading, but soon realised that winning the lottery is more likely, that hoping to find the next Apple.

Remember, when markets are falling, if your total fund falls by a smaller percentage, you are still making good progress.

Forget about sell when the share price rises or falls so many percent. If you feel the business is growing, hang on. Just because a firm might have begun say 100 years ago, does not mean it is going to cease being a good business.

If you have good businesses, don't panic during a market crash, get ready to buy more at lower prices. Many people buy high, then panic sell at lower levels. Common sense and logic can help, e.g. avoiding being sucked into the 1999 dot com bubble, and realising the debt crisis of 2007 was going to go pop, although it was impossible to know when that would happen.

Best of luck.

Edited by Jon39 on Friday 20th October 13:27

Jon39 said:

If you have good businesses, don't panic during a market crash, get ready to buy more at lower prices. Many people buy high, then panic sell at lower levels. Common sense and logic can help, e.g. avoiding being sucked into the 1999 dot com bubble, and realising the debt crisis of 2007 was going to go pop, although it was impossible to know when that would happen.

If you had to go with your gut feeling - when do you *think* the next market crash or recession will or could happen? Are you seeing any signs yet that are making you cautious or tempting you to turn into cash?

Cheers

Phooey said:

Hi Jon, always interesting to read your posts in the finance room

If you had to go with your gut feeling - when do you *think* the next market crash or recession will or could happen? Are you seeing any signs yet that are making you cautious or tempting you to turn into cash?

Cheers

If you had to go with your gut feeling - when do you *think* the next market crash or recession will or could happen? Are you seeing any signs yet that are making you cautious or tempting you to turn into cash?

Cheers

Hello Phooey,

Thank you for your kind words.

Having read some of my 'stuff', you might have been disappointed whenever I mention, I never make forecasts.

Stock markets are so variable, that it seems to me, impossible to predict what will happen next.

Try printing out some pundits forecasts, and then look again in a years time. Some firms have such revered names, that what they say is often assumed to be correct. That they must be able to see into the future. A year ago Goldman Sachs made a client Sell recommendation on a FTSE 100 company. For all I knew they might have been correct, but the share price then climbed considerably. That would have cost their clients dearly. Some while later, they quietly issued a Buy recommendation on the same company, as if their previous forecast did not exist. And these people are supposed to be experts. It is happening all the time.

The two instances that I mentioned, 1999 and 2007, were so obvious, that they were rare exceptions to my own rule, of never forecasting. I don't know your age, but leading up to 1999, many start-up technology companies were being floated. Some of those businesses had enormous valuations, but most had never made a profit. The investment community went wild with excitement, as if these new firms were going to take over the world. One or two did, but it was all such a big gamble. The big traditional firms went out of fashion while all that was going on, so the market beat me during that period, but after the bubble burst, the traditionals roared back into favour. People lost a lot of money, because they did not seem to think enough, about those businesses and their valuations. They just followed 'the herd' and bought.

I am sure you will know all about 2007. Consumers and governments were borrowing as much as they could. Lenders were fighting each other for market share. TV programmes showed how easy it was, to get any size mortgage that you wanted. The 'liar loans'. Those in authority did nothing about it, because everything was going so well. It was obvious to many, that there would eventually be trouble, but of course as usual, it was impossible to predict the timing of the end of the that debt boom. Afterwards people kept saying, no one saw that coming, and blamed it all on others.

You therefore know my answer to your question. Debt is clearly a big worry once again, but what will happen, I don't know.

I won't be selling holdings. Hopefully my defensives will continue trading reasonably. Being out of the market can result in missing upward movements. Trying to time markets is a gamble. I might be over confident about this, but so far, during each year when the Index has fallen, my portfolio has either not fallen at all, or has fallen by lesser percentage than the market. Maybe next time, whenever that is, might be different, but in this 'game' one has to remain confident. It is all about how good the businesses are, that you hold.

Edited by Jon39 on Saturday 21st October 12:51

Thanks Jon - all sounds like wise words. As for me - I'm just over 40 and contribute monthly (ISA) via a local IFA company - Adventurous portfolio. On a couple of occasions very recently I've heard people mention they have "gone into cash"... just got me thinking if I should too

My IFA says basically the same as you - don't try and time the market and risk missing out on the upward movements - especially as I'm in it for another 10+ years

Cheers mate

My IFA says basically the same as you - don't try and time the market and risk missing out on the upward movements - especially as I'm in it for another 10+ years

Cheers mate

A final point following your reply.

My system of continuing to hold through recessions, does rely on holding quite a few defensive type companies, ie. their products continue to be in fairly constant demand.

If someone holds cyclicals, miners, house builders etc., then they would usually be expected to have greater share price falls and probably dividend cuts, when economic times become difficult. Therefore if you think 'troubles' might be coming, you may want to check what your money is actually invested in.

Adventurous portfolio is presumably a fund. They love their titles, but what it means, is not clear.

The fund world now seem to compare their performance with strange mythical 'benchmarks'.

Suggest you just compare the annual result each year, against the percentage change of the FTSE All-Share Index, to keep things simple. If you are beating the broad market average (Index) then you can be pleased. I did my weekly figures this evening, and if I remember correctly, the Index is at present + 6.58% since 1 Jan 2017.

Jon39 said:

Suggest you just compare the annual result each year, against the percentage change of the FTSE All-Share Index, to keep things simple. If you are beating the broad market average (Index) then you can be pleased. I did my weekly figures this evening, and if I remember correctly, the Index is at present + 6.58% since 1 Jan 2017.

Sounds like good advice Jon - thank you for doing the maths

...Just logged into my Standard Life Wrap > Performance > Summary, and my "Return" is +11.54% - 1st Jan 2017 to 21st Oct 2017. From what I can see that is AFTER fees ("Account Transfers"). I'm not entirely sure what "Simple Return" means but that is the default view. Other option is IRR and that is showing +11.94%.

Suppose I can't moan while its up.. but them Advisor / Platform / Wrap / OAC etc etc etc fees mount up. I'm in the wrong job

Phooey said:

Sounds like good advice Jon - thank you for doing the maths

...Just logged into my Standard Life Wrap > Performance > Summary, and my "Return" is +11.54% - 1st Jan 2017 to 21st Oct 2017. From what I can see that is AFTER fees ("Account Transfers"). I'm not entirely sure what "Simple Return" means but that is the default view. Other option is IRR and that is showing +11.94%.

...Just logged into my Standard Life Wrap > Performance > Summary, and my "Return" is +11.54% - 1st Jan 2017 to 21st Oct 2017. From what I can see that is AFTER fees ("Account Transfers"). I'm not entirely sure what "Simple Return" means but that is the default view. Other option is IRR and that is showing +11.94%.

You can be very happy with those two percentage increases. Roughly double the market average.

I don't know what simple return means, neither am I familiar with your abbreviation IRR, but the fund world seems to like complication.

My philosophy is to keep everything as simple as I possible.

Keeping calendar year percentage records and then comparing with the FTSE All-Share index, is certainly the simplest and clearest way to follow progress.

I sometimes hear people talk about a particular successful share trade they are pleased with, but it is then ridiculous that they don't seem to have any idea, about how they are doing overall.

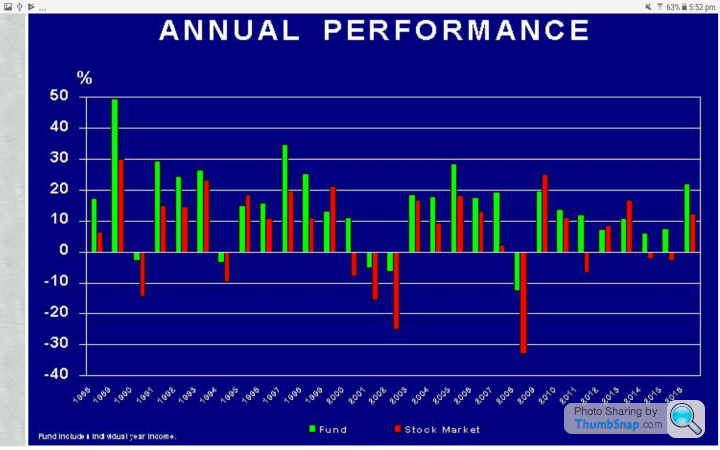

If a basic spreadsheet is used to record the percentage figures, then a couple of charts can automatically be produced, which really show at a glance, what has been happening. This is my latest complete year chart. You can spot the referendum effect.

Edited by Jon39 on Saturday 21st October 20:24

Google says IRR is "Internal Rate of Return":

http://www.investinganswers.com/financial-dictiona...

I'm not quite sure I _understand_ the article though :-/

http://www.investinganswers.com/financial-dictiona...

I'm not quite sure I _understand_ the article though :-/

xeny said:

I'm not quite sure I _understand_ the article though

' formula for IRR is: = P0 + P1/(1+IRR) + P2/(1+IRR)2 + P3/(1+IRR)3 + . . . +Pn/(1+IRR)n where P0, P1, . . . Pn equals the cash flows in periods 1, 2, . . . n, respectively; and IRR equals the project's internal rate of r'

I am not surprised.

If one were cynical, it might be suggested, that trying to obtain other peoples money to invest, is a very different activity from managing the investment of your own money.

I seem to recall one of Mr Warren Buffett's quotes. Something about, beware of being approached by boffins bearing complicated formulas.

Edited by Jon39 on Saturday 21st October 20:56

Jon39 said:

' formula for IRR is: = P0 + P1/(1+IRR) + P2/(1+IRR)2 + P3/(1+IRR)3 + . . . +Pn/(1+IRR)n where P0, P1, . . . Pn equals the cash flows in periods 1, 2, . . . n, respectively; and IRR equals the project's internal rate of r'

I am not surprised.

If one were cynical, it might be suggested, that trying to obtain other peoples money to invest, is a very different activity from managing the investment of your own money.

I seem to recall one of Mr Warren Buffett's quotes. Something about, beware of being approached by boffins with complicated formulas.

sidicks said:

IRR isn't complicated, it's just the actual return achieved taking into account the timing of cashflows.

Thank you.

Would that therefore involve the timing of incoming and outgoing flows of customer cash, and all their share transaction cash movements.

My investment cash flow, usually only consists of the regular flow of incoming dividends. Virtually no other cash movements, unless a rights issue, or takeover occurs. Presumably that is why I have never needed to know about IRR.

Jon39 said:

Thank you.

Would that therefore involve the timing of incoming and outgoing flows of customer cash, and all their share transaction cash movements.

My investment cash flow, usually only consists of the regular flow of incoming dividends. Virtually no other cash movements, unless a rights issue, or takeover occurs. Presumably that is why I have never needed to know about IRR.

sidicks said:

What do you do with your dividends and how due you account for them in your return calculation?

Dividends after receipt, remain within the fund total as cash, until the year end.

The fund percentage change (shown in the above chart) therefore includes those cash dividends as they build up during the year (mentioned in the chart footnote).

At the start of the following year, the monitoring percentages reset again to zero, therefore showing zero cash dividends on the 1st January. Doing the monitoring that way, enables me to have a picture of each year individually.

Before you say it, I do know there is a small cheat involved, because the basic FTSE All-Share Index does not include dividends received. All part of my aim for simplicity and trying to avoid complication. However, that has not made any difference, to the overall market outperformance of the portfolio.

Edited by Jon39 on Saturday 21st October 23:07

Jon39 said:

Dividends after receipt, remain within the fund total as cash, until the year end.

The fund percentage change (shown in the above chart) therefore includes those cash dividends as they build up during the year (mentioned in the chart footnote).

At the start of the following year, the monitoring percentages reset again to zero, therefore showing zero cash dividends on the 1st January. Doing the monitoring that way, enables me to have a picture of each year individually.

Before you say it, I do know there is a small cheat involved, because the basic FTSE All-Share Index does not include dividends received. However, all part of my aim for simplicity and trying to avoid complications.

Gassing Station | Finance | Top of Page | What's New | My Stuff