Pension growth strategy?

Discussion

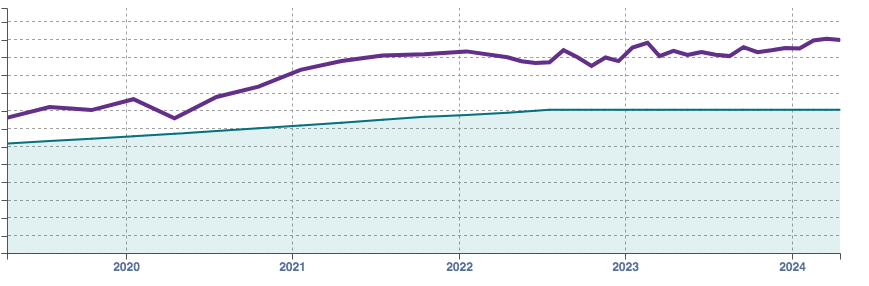

Looking for some pension investment advice. I'm in my mid forties, with a substantial pension fund (relatively speaking).

However I assume like many people my pension growth hasn't been performing as good as other years - for all the reasons that we know about in the news over the last 4 or so years. However, I feel like I need to learn a good pension stratgey especially as I am coming closer (20 years or so) away from retirement. I've pretty much stuck to a couple of volatile (high-ish risk) funds over the course of the last 10 or so years - as per the graph below. I combined a different pension into this one around August 2018 (so hence the spike around then).

Just under the last 3 or years, the pot has only increased by 7% roughly across the 3 years but I did however stop making contributions for around the last 2 years (since July 2022). I will re-start making significant contributions in the next month or so again.

I guess my basic question is: What are the best strategies people used to grow their pension pots? Do you switch funds regularly or just pump and dump and forget about it like I've have done over the last 10 or so years? My pension funds understanding is very limited - all I have used as my guiding principle is to use higher-risk funds given my current age profile and then look to de-risk as I get older and move them to less volatile funds in time. Sometimes I feel I should be monitoring fund performance on a weekly, monthly or quarterly basis and move them accordingly. Does any one do that in reality or do people take a longer term view? What is a good strategy? Split the pot into even more funds? My previous fund selection 10 years ago was based IIRC on previous years fund performance (but I can't really remember - might even have been a finger-in-the-air selection).

However I assume like many people my pension growth hasn't been performing as good as other years - for all the reasons that we know about in the news over the last 4 or so years. However, I feel like I need to learn a good pension stratgey especially as I am coming closer (20 years or so) away from retirement. I've pretty much stuck to a couple of volatile (high-ish risk) funds over the course of the last 10 or so years - as per the graph below. I combined a different pension into this one around August 2018 (so hence the spike around then).

Just under the last 3 or years, the pot has only increased by 7% roughly across the 3 years but I did however stop making contributions for around the last 2 years (since July 2022). I will re-start making significant contributions in the next month or so again.

I guess my basic question is: What are the best strategies people used to grow their pension pots? Do you switch funds regularly or just pump and dump and forget about it like I've have done over the last 10 or so years? My pension funds understanding is very limited - all I have used as my guiding principle is to use higher-risk funds given my current age profile and then look to de-risk as I get older and move them to less volatile funds in time. Sometimes I feel I should be monitoring fund performance on a weekly, monthly or quarterly basis and move them accordingly. Does any one do that in reality or do people take a longer term view? What is a good strategy? Split the pot into even more funds? My previous fund selection 10 years ago was based IIRC on previous years fund performance (but I can't really remember - might even have been a finger-in-the-air selection).

Edited by type-r on Wednesday 17th April 11:16

type-r said:

Looking for some pension investment advice. I'm in my mid forties, with a substantial pension fund (relatively speaking).

However I assume like many people my pension growth hasn't been performing as good as other years - for all the reasons that we know about in the news over the last 4 or so years. However, I feel like I need to learn a good pension stratgey especially as I am coming closer (20 years or so) away from retirement. I've pretty much stuck to a couple of volatile (high-ish risk) funds over the course of the last 10 or so years - as per the graph below. I combined a different pension into this one around August 2018 (so hence the spike around then).

Just under the last 3 or years, the pot has only increased by 7% roughly across the 3 years but I did however stop making contributions for around the last 2 years (since July 2022). I will re-start making significant contributions in the next month or so again.

I guess my basic question is: What are the best strategies people used to grow their pension pots? Do you switch funds regularly or just pump and dump and forget about it like I've have done over the last 10 or so years? My pension funds understanding is very limited - all I have used as my guiding principle is to use higher-risk funds given my current age profile and then look to de-risk as I get older and move them to less volatile funds in time. Sometimes I feel I should be monitoring fund performance on a weekly, monthly or quarterly basis and move them accordingly. Does any one do that in reality or do people take a longer term view? What is a good strategy? Split the pot into even more funds? My previous fund selection 10 years ago was based IIRC on previous years fund performance (but I can't really remember - might even have been a finger-in-the-air selection).

Possibly in a similar position and I often have similar questions - Although my pots have increased by much more than 7% in that time. However I assume like many people my pension growth hasn't been performing as good as other years - for all the reasons that we know about in the news over the last 4 or so years. However, I feel like I need to learn a good pension stratgey especially as I am coming closer (20 years or so) away from retirement. I've pretty much stuck to a couple of volatile (high-ish risk) funds over the course of the last 10 or so years - as per the graph below. I combined a different pension into this one around August 2018 (so hence the spike around then).

Just under the last 3 or years, the pot has only increased by 7% roughly across the 3 years but I did however stop making contributions for around the last 2 years (since July 2022). I will re-start making significant contributions in the next month or so again.

I guess my basic question is: What are the best strategies people used to grow their pension pots? Do you switch funds regularly or just pump and dump and forget about it like I've have done over the last 10 or so years? My pension funds understanding is very limited - all I have used as my guiding principle is to use higher-risk funds given my current age profile and then look to de-risk as I get older and move them to less volatile funds in time. Sometimes I feel I should be monitoring fund performance on a weekly, monthly or quarterly basis and move them accordingly. Does any one do that in reality or do people take a longer term view? What is a good strategy? Split the pot into even more funds? My previous fund selection 10 years ago was based IIRC on previous years fund performance (but I can't really remember - might even have been a finger-in-the-air selection).

I have two main pots, and two smaller ones - In terms of the main pots - half is in a Standard Life fund that has done pretty well over time. I stopped paying in in 2016 and it has doubled since then. Every time I look to change the fund, I convince myself that it's fine where it is (those returns and the costs look ok to me)

My other main pot is in Vanguard and is a collection of other pots that I've moved together (where the annual costs were too high imho) plus my annual tax avoidance. It is split across an LS fund and the S&P and has done 26% in the last year plus contributions on top. I've then got the current job fund, and two others (one from my first job now worth 42K) and one that I'll move into Vanguard shortly.

In terms of monitoring, I check mine a couple of times a month and store all the instantaneous values in a spreadsheet. It's kind of meaningless as I'm still 10+ year's away and the only thing I've really learned is that pension pots move up and down way more than the annual statement might lead you to believe. It is not unusual for them to go down and back up several % in the same month.......

I try (and fail) to operate on a set and forget approach. I'm probably in about the right choices, paying about the right fees, and am continuing to (over) contribute so time will do it's thing.

If they double again in the next 10 years (which is not beyond the realms of possibility) then I should be about right......If anything, my new concern is whether I have over-rotated towards pension payments and should actually be looking to put less in somehow...

I'm not a pensions expert by anymeans - just a keen amateur, but am always interested in these kind of questions.,

type-r said:

Looking for some pension investment advice. I'm in my mid forties, with a substantial pension fund (relatively speaking).

However I assume like many people my pension growth hasn't been performing as good as other years - for all the reasons that we know about in the news over the last 4 or so years. However, I feel like I need to learn a good pension stratgey especially as I am coming closer (20 years or so) away from retirement. I've pretty much stuck to a couple of volatile (high-ish risk) funds over the course of the last 10 or so years - as per the graph below. I combined a different pension into this one around August 2018 (so hence the spike around then).

Just under the last 3 or years, the pot has only increased by 7% roughly across the 3 years but I did however stop making contributions for around the last 2 years (since July 2022). I will re-start making significant contributions in the next month or so again.

I guess my basic question is: What are the best strategies people used to grow their pension pots? Do you switch funds regularly or just pump and dump and forget about it like I've have done over the last 10 or so years? My pension funds understanding is very limited - all I have used as my guiding principle is to use higher-risk funds given my current age profile and then look to de-risk as I get older and move them to less volatile funds in time. Sometimes I feel I should be monitoring fund performance on a weekly, monthly or quarterly basis and move them accordingly. Does any one do that in reality or do people take a longer term view? What is a good strategy? Split the pot into even more funds? My previous fund selection 10 years ago was based IIRC on previous years fund performance (but I can't really remember - might even have been a finger-in-the-air selection).

The last few years have been very strong for global equities, with 10.7% annualised returns over the last 5 years and 7.8% annualised over 3 years.However I assume like many people my pension growth hasn't been performing as good as other years - for all the reasons that we know about in the news over the last 4 or so years. However, I feel like I need to learn a good pension stratgey especially as I am coming closer (20 years or so) away from retirement. I've pretty much stuck to a couple of volatile (high-ish risk) funds over the course of the last 10 or so years - as per the graph below. I combined a different pension into this one around August 2018 (so hence the spike around then).

Just under the last 3 or years, the pot has only increased by 7% roughly across the 3 years but I did however stop making contributions for around the last 2 years (since July 2022). I will re-start making significant contributions in the next month or so again.

I guess my basic question is: What are the best strategies people used to grow their pension pots? Do you switch funds regularly or just pump and dump and forget about it like I've have done over the last 10 or so years? My pension funds understanding is very limited - all I have used as my guiding principle is to use higher-risk funds given my current age profile and then look to de-risk as I get older and move them to less volatile funds in time. Sometimes I feel I should be monitoring fund performance on a weekly, monthly or quarterly basis and move them accordingly. Does any one do that in reality or do people take a longer term view? What is a good strategy? Split the pot into even more funds? My previous fund selection 10 years ago was based IIRC on previous years fund performance (but I can't really remember - might even have been a finger-in-the-air selection).

Edited by type-r on Wednesday 17th April 11:16

If your pension has performed poorly, it's likely you've unfortunately chosen poor funds to invest in. As such good work identifying this and asking the question.

SL Jupiter Merlin Growth is a fund of funds - there is a fund manager who is choosing some active funds to invest in. You're paying both the fund manager and the managers of the funds he/she is investing in. It just so happens that out of the entire investment universe of 5000 odd funds, the manager of the Jupiter fund of funds has 25% of their fund allocated to Jupiter funds. Completely coincidental I am sure, and certainly no bias involved ;-)

The fund is appallingly expensive. As in taking the piss and laughing at anyone investing in it expensive. The total expense is 2.82% per annum. I am sure the managers will say "yes but we are making great selection of funds and earning our fees". In return I'd ask them why their 100% equity fund has returned 14.9% over 3 years and 35.9% over 5 years when global equities which you can buy via a global tracker at a fee of 0.13% have returned 25.3% and 66.5% over the same timeframe.

If I can just put those fees into context for you (as this is a bugbear of mine). Let's say global equities return 8% a year. Using the global tracker at a 0.13% fee, a £100k starting amount and 25 years of growth. Your pot increases by £584k, you keep £564k of those gains, you end up with £664k.

Now using Jupiter Merlin's fees and the same amount/timeframe. Your pot increases by £584k, you keep £253k of that gain, Jupiter Merlin keep £331k of it. You end up with £353k.

So the first and easiest way to improve the performance of your pension is to ditch this horrendously expensive massively underperforming pile of s

t.

t. The other fund you have is a punt on a single region, Asia Pacific. It's quite a random punt to make. The fund has returned -4.17% p/annum over 3 years, and just over 2% per annum over 5. Fees aren't horrendous, but it's a 3rd quartile performer compared to other funds in its sector. ABRDN are a poor investment house (see their share price, news about poorly performing funds, redundancies etc for more detail) so generally I'd avoid any active funds managed by them.

Summary is current holdings are a mix of 1 that's global equities but massively underperforming whilst charging you a diabolical amount in return and 1 that's a punt on a specific region, and that region has been in the doldrums whilst the fund selected has been one of the poorer performers.

If you accept that you don't have a reliable method of selecting in advance which active funds and which regions are going to perform well (and the folk at Jupiter who do this for a day job, who have a team of researchers, analysts, economists and quant experts helping them don't or they wouldn't be performing so badly) then my advice would be to buy a cheap global tracker or a cheap multi asset fund, keep your fees low and let time/the market do it's thing.

^^ this

and if you want to gauge the impact of fees work out what you're paying in total and plug them in here.

https://larrybates.ca/t-rex-score/

and if you want to gauge the impact of fees work out what you're paying in total and plug them in here.

https://larrybates.ca/t-rex-score/

The S&P500 graph on this link is highly informative. Once you have the page in front of you click on "Max" to see the long term trend.

https://www.google.com/finance/quote/.INX:INDEXSP?...

There are two leaning points,

1. The long term trend is unquestionably upwards. Hooray!

2. There are times when it suddenly drops 20% in a heartbeat. Ouch. You can clearly see this with the financial crisis of 2008, Covid in 2020 and Putin's invasion of Ukraine in 2022.

So you need to "believe" in the long terms trend to avoid scaring the living daylights out of yourself - which would usually result in making bad decisions, like selling at the bottom and being too scared to get back in until you've missed the rebound.

The bottom line is often as simple as - don't try to be clever, keep costs down and make sure those contributions go in every month regardless of sentiment.

https://www.google.com/finance/quote/.INX:INDEXSP?...

There are two leaning points,

1. The long term trend is unquestionably upwards. Hooray!

2. There are times when it suddenly drops 20% in a heartbeat. Ouch. You can clearly see this with the financial crisis of 2008, Covid in 2020 and Putin's invasion of Ukraine in 2022.

So you need to "believe" in the long terms trend to avoid scaring the living daylights out of yourself - which would usually result in making bad decisions, like selling at the bottom and being too scared to get back in until you've missed the rebound.

The bottom line is often as simple as - don't try to be clever, keep costs down and make sure those contributions go in every month regardless of sentiment.

Fat80b's post above sums up my approach and experiences...I am early 40's and another 'amateur' who tinkers a bit with the aim to maximise growth over the next 15-20 years.

All my pensions are/were DC, amalgamated the old ones into a SIPP and invested the whole lot into a single Developed Markets Equity ETF....the urge to tinker is strong e.g: add EM, Smallcap etc but resisted so far. Work pension split across 4 Equity funds including the Sharia HSBC one...(not based on any cultural/religious reasons but the work pension options are naff hence have to go with what's available).

I tend to stagger my risk somewhat e.g investment wrapper I cant access till 60 in S&P500, pensions in 100% global equity (70% US then!) and S&SISA roughly 75/25 equities/bonds......no idea if my 'strategy' will go t*ts up or not but there it is! Oh and maximise employee pension matching (if applicable).

All my pensions are/were DC, amalgamated the old ones into a SIPP and invested the whole lot into a single Developed Markets Equity ETF....the urge to tinker is strong e.g: add EM, Smallcap etc but resisted so far. Work pension split across 4 Equity funds including the Sharia HSBC one...(not based on any cultural/religious reasons but the work pension options are naff hence have to go with what's available).

I tend to stagger my risk somewhat e.g investment wrapper I cant access till 60 in S&P500, pensions in 100% global equity (70% US then!) and S&SISA roughly 75/25 equities/bonds......no idea if my 'strategy' will go t*ts up or not but there it is! Oh and maximise employee pension matching (if applicable).

I take Warren Buffets advice and invest into S&P 500 via my SIPP each month. I also hold some Lifestrategy 100 and FTSE trackers.

I find it worthwhile to keep an eye out for opportunities in individual companies, but to only plan with amounts you’re happy to lose (gambling). I made 200% on Tesla and then sold out, 40% on Hyundai, etc.

I’d say c.90% of my SIPP is S&P500, FTSE and Lifestrategy funds.

I find it worthwhile to keep an eye out for opportunities in individual companies, but to only plan with amounts you’re happy to lose (gambling). I made 200% on Tesla and then sold out, 40% on Hyundai, etc.

I’d say c.90% of my SIPP is S&P500, FTSE and Lifestrategy funds.

Sunday Drive said:

I take Warren Buffets advice and invest into S&P 500 via my SIPP each month. I also hold some Lifestrategy 100 and FTSE trackers.

I find it worthwhile to keep an eye out for opportunities in individual companies, but to only plan with amounts you’re happy to lose (gambling). I made 200% on Tesla and then sold out, 40% on Hyundai, etc.

I’d say c.90% of my SIPP is S&P500, FTSE and Lifestrategy funds.

No losses ? I find it worthwhile to keep an eye out for opportunities in individual companies, but to only plan with amounts you’re happy to lose (gambling). I made 200% on Tesla and then sold out, 40% on Hyundai, etc.

I’d say c.90% of my SIPP is S&P500, FTSE and Lifestrategy funds.

Vanguard FTSE Global all cap is where everything I invest sits in terms of pension. Same for my wife.

Fairly happy with the simplicity/coverage/fee/platform, most of our investments in ISA/GIA in very similar tbh - bar my ongoing punt with Fundsmith which I will probably bin one day now there’s a 4 figure fee each year.

Fairly happy with the simplicity/coverage/fee/platform, most of our investments in ISA/GIA in very similar tbh - bar my ongoing punt with Fundsmith which I will probably bin one day now there’s a 4 figure fee each year.

Edited by okgo on Wednesday 17th April 19:00

I have no idea what I'm doing, so of course, I fiddled with mine. My current work one is with Aviva and it was all in their standard fund so I moved 25% to one riskier fund and 25% to another.

22-23 they all lost money but the 2 riskier funds less than the original standard one so I was happy.

23-24 the standard fund went up 14% and the 2 funds I chose went up 29% and 25%. So I'm still happy and now consider myself a wheeling dealing pension man.

22-23 they all lost money but the 2 riskier funds less than the original standard one so I was happy.

23-24 the standard fund went up 14% and the 2 funds I chose went up 29% and 25%. So I'm still happy and now consider myself a wheeling dealing pension man.

Some great posts and advice on here, thank you. I haven't got a clue about SIPPs, to global trackers, to S&P etc It's an acronymn minefield lol. Looks like I have some homework to do!

Thanks for the links to education and also letting me know how sh!t my fund selections are! I definitely needed to hear that. Also the ridiculous fees I never knew I was shelling out. Time to clean up my act and get proper pension savvy.

I definitely needed to hear that. Also the ridiculous fees I never knew I was shelling out. Time to clean up my act and get proper pension savvy.

Thanks for the links to education and also letting me know how sh!t my fund selections are!

I definitely needed to hear that. Also the ridiculous fees I never knew I was shelling out. Time to clean up my act and get proper pension savvy.As above, I think the fees are one of the most important things that most people miss.

The fact that the gov schemes are both a) expensive and b) offer rubbish choice is a future scandal waiting to be discovered……it’s like the post office scandal. Everyone knows it, it just hasn’t made the front page yet!

My SL pot is at 0.35% which I consider ok.

I had one with Nest which offers a rubbish selection of funds and charged a fee on the way in and an ongoing charge. I binned them as soon as I could

I had another at 0.65% and my current scheme charges 1.02% which is criminal.

I generally consider that if it’s less than 0.5% and funds are good then I’ll leave it where it is, if it’s more than that, then I’ll move it to my vanguard pot.

The fact that the gov schemes are both a) expensive and b) offer rubbish choice is a future scandal waiting to be discovered……it’s like the post office scandal. Everyone knows it, it just hasn’t made the front page yet!

My SL pot is at 0.35% which I consider ok.

I had one with Nest which offers a rubbish selection of funds and charged a fee on the way in and an ongoing charge. I binned them as soon as I could

I had another at 0.65% and my current scheme charges 1.02% which is criminal.

I generally consider that if it’s less than 0.5% and funds are good then I’ll leave it where it is, if it’s more than that, then I’ll move it to my vanguard pot.

type-r said:

Some great posts and advice on here, thank you. I haven't got a clue about SIPPs, to global trackers, to S&P etc It's an acronymn minefield lol. Looks like I have some homework to do!

Thanks for the links to education and also letting me know how sh!t my fund selections are! I definitely needed to hear that. Also the ridiculous fees I never knew I was shelling out. Time to clean up my act and get proper pension savvy.

Don't spend too much time on it.Thanks for the links to education and also letting me know how sh!t my fund selections are!

I definitely needed to hear that. Also the ridiculous fees I never knew I was shelling out. Time to clean up my act and get proper pension savvy.Investing is one of those weird areas where in an ideal world you learn just enough to be doing sensible things, you start to do them, and then you'd just keep doing them and act like you're dead

bhstewie said:

hstewie said: Investing is one of those weird areas where in an ideal world you learn just enough to be doing sensible things, you start to do them, and then you'd just keep doing them and act like you're dead

Was it Fidelity that did a study and found their best performing investors over 10yrs were dead, so their investments had been left un-molested for years?James6112 said:

No losses ?

Investors never have losses! You never hear Adam mentioning losses do you? If you're an investor - as we all are here - you only count gains. That's because the rest will come back eventually so it's more gain, just delayed a bit

Sheepshanks said:

Was it Fidelity that did a study and found their best performing investors over 10yrs were dead, so their investments had been left un-molested for years?

There's only one problem with that strategy...Om a slightly serious note, what happens to investments if the owner dies and nobody turns up to sort them out?

Gassing Station | Finance | Top of Page | What's New | My Stuff