Hit and run, third party who's trader claiming vehicle sold

Discussion

Hi guys, I have been involved in an incident with another car who pulled out on me on a side road and I just want some advice from anyone who knows more about situations like what i'm going through at the moment as it feels like i'm going to explode as it doesn't look good currently!

I am fully comp.

I managed to get a picture of their vehicle registration and the damage to their vehicle before they drove off, police was informed, took a statement was given a reference number.

However the company I am instructing to deal with the claim have stated that the third party's insurers where the vehicle was insured with has stated that their client sold the vehicle prior to the incident and if this is the case - I may have to go through the MID.

I've established the following:

On the night of the incident, the vehicle was insured on the MID, the police on the night said it was insured, my insurers said it was insured.

A day or two after the incident, the vehicle was showing as no longer insured.

When I was contacted by my solicitors, I was told that the third party's insurers that their client had not reported any incident in relation to my vehicle.

This just stinks of trying to pull a fast one where the owner is trying wash his hands of the claim.

My solicitors have asked the third party insurance for an invoice to show vehicle was sold prior to the incident but i'm not optimistic, I mean it's not exactly difficult to write up an invoice showing a sale has taken place, they said they'll investigate any potential invoice that is put forward by the third party but I think I know how this will turn out.

They said because I don't know the name of the driver too this isn't great which I don't understand what difference does it make anyway!

What I don't understand, is the vehicle was shown as insured at the time, regardless if there was a sale at the time which I very much doubt - I've been told trade policy insurance is a bit different to standard motor insurance polices where it will be difficult to claim if the vehicle was sold, but the car was showing as insured so the third party's insurance should pay out and recoup their losses through the policy holder for their negligence of not cancelling their policy prior to the crash, it's just not right!!

I am fully comp.

I managed to get a picture of their vehicle registration and the damage to their vehicle before they drove off, police was informed, took a statement was given a reference number.

However the company I am instructing to deal with the claim have stated that the third party's insurers where the vehicle was insured with has stated that their client sold the vehicle prior to the incident and if this is the case - I may have to go through the MID.

I've established the following:

On the night of the incident, the vehicle was insured on the MID, the police on the night said it was insured, my insurers said it was insured.

A day or two after the incident, the vehicle was showing as no longer insured.

When I was contacted by my solicitors, I was told that the third party's insurers that their client had not reported any incident in relation to my vehicle.

This just stinks of trying to pull a fast one where the owner is trying wash his hands of the claim.

My solicitors have asked the third party insurance for an invoice to show vehicle was sold prior to the incident but i'm not optimistic, I mean it's not exactly difficult to write up an invoice showing a sale has taken place, they said they'll investigate any potential invoice that is put forward by the third party but I think I know how this will turn out.

They said because I don't know the name of the driver too this isn't great which I don't understand what difference does it make anyway!

What I don't understand, is the vehicle was shown as insured at the time, regardless if there was a sale at the time which I very much doubt - I've been told trade policy insurance is a bit different to standard motor insurance polices where it will be difficult to claim if the vehicle was sold, but the car was showing as insured so the third party's insurance should pay out and recoup their losses through the policy holder for their negligence of not cancelling their policy prior to the crash, it's just not right!!

Edited by captainhook on Friday 24th February 10:47

Josho said:

Wha car is it? How old etc?

Some dealers offer drive away insurance and this is the only reason I can think that a dealer would put iton their policy.

You need to find out who was insured and by who.

I wonder if it's a dealers own car and they are claiming it isn't.

Hi, the vehicle was not insured by a dealer i'm 100% sure of this, it was some little ***** that were in the car so it's under like a motor traders policy - the owner of the vehicle must of own a garage/workshop.Some dealers offer drive away insurance and this is the only reason I can think that a dealer would put iton their policy.

You need to find out who was insured and by who.

I wonder if it's a dealers own car and they are claiming it isn't.

it's an old car, Renault on a 04 plate, the insurance/broker is tradex

Well is seems like I know the outcome when my friend sent me this response when why does it matter if I don't know the name of the driver:

"It matters because there are several different schemes to compensate victims of uninsured/untraced drivers, which entitle you to different things depending on which one you can claim on.

If there was an insurance policy of any sort running on the car, and the driver was identified, then the Road Traffic Act requires the car's insurer to pay for damage caused to third partys, whether or not the person driving the car was covered by the policy. So if the trader had sold the car and not cancelled the policy, or even if the car was stolen, you'd be able to claim off the trader's policy - if you knew who the driver was.

However the above does NOT apply if the identity of the driver is unknown - because strictly speaking the insurer doesn't have to pay until you get a court judgement against the driver, and you can't file a court case against an anonymous shadow who disappeared into the night"

This is madness, it's not right, so because I don't know the driver, I can't claim off the third party's insurance, what an absolute farce. I'm not happy having to claim off my own policy, be out of pocket, lose my ncb and suffer from high premiums for an accident which is not my fault and has to be deemed by fault on a technicality of not knowing who the driver of no fault of my own, this scenario must be changed so this doesn't affect innocent drivers.

The claim handler has tried to chase up proof in the form of the invoice of the sale of vehicle of the car that was involved in incident however the phone of the insurers is keep ringing out so she said to mitigate losses as i'm using a hire car cost that by the end of week or early next week I may have to go down the MIB route and my insurance as I don't know the name of the driver involved and the third party insurers will just "keep denying liability" and i'm furious about that as I don't feel they are chasing hard enough to get the third party insurers to take note of this serious incident whereby I was hurt and my passenger was.

The third party insurers are Tradex.

You cannot just say the vehicle was sold at the time of the incident happened, whilst the vehicle was still showing as insured.

The key questions that have yet been answered are:

Why was the vehicle still insured at time of the incident if the car had been sold

How long ago was the vehicle sold

Why am I having to go through the possibility of claiming through my own insurance if the vehicle was insured at the time of the incident even though I don't know the drivers name.

Police have been helpless. officer took a statement 2 weeks ago, not responding to my emails, spoke to the police traffic dept saying no updates, there short of staff, WTH?

2 weeks after the time of the incident, I don't know if my vehicle is a write off, the claim handler is still waiting for the third party to do a without prejudice report on it and i'm just stressed right now.

Someone I know said their friend who sells and buys cars was involved with a similar incident and their policy was with tradex where they stated that they sold the car at the time of the incident but didn't have the details of who the car was sold to: Tradex sent investigators over and asked him a lot of questions, and in the end settled the claim with the third party, I can't understand why they can't do this and why my claim handler isn't pushing them to sort it out and take them down this route.

http://insurance.dwf.law/news-updates/2015/06/the-...

I've came across this which shows the third party insurers could be still liable for the incident?

The third party insurers are Tradex.

You cannot just say the vehicle was sold at the time of the incident happened, whilst the vehicle was still showing as insured.

The key questions that have yet been answered are:

Why was the vehicle still insured at time of the incident if the car had been sold

How long ago was the vehicle sold

Why am I having to go through the possibility of claiming through my own insurance if the vehicle was insured at the time of the incident even though I don't know the drivers name.

Police have been helpless. officer took a statement 2 weeks ago, not responding to my emails, spoke to the police traffic dept saying no updates, there short of staff, WTH?

2 weeks after the time of the incident, I don't know if my vehicle is a write off, the claim handler is still waiting for the third party to do a without prejudice report on it and i'm just stressed right now.

Someone I know said their friend who sells and buys cars was involved with a similar incident and their policy was with tradex where they stated that they sold the car at the time of the incident but didn't have the details of who the car was sold to: Tradex sent investigators over and asked him a lot of questions, and in the end settled the claim with the third party, I can't understand why they can't do this and why my claim handler isn't pushing them to sort it out and take them down this route.

http://insurance.dwf.law/news-updates/2015/06/the-...

I've came across this which shows the third party insurers could be still liable for the incident?

What lesson can be learnt from this? I haven't done anything wrong. I took pictures of the car's damage and the vehicle registration, if the person wouldn't give me his name or address and drive off what could I I have done differently in this situation?

I could of taken the keys out of their car and wait until the police come and make the situation escalate in a bad way which I would of got a ticking off for and possibility at the same time the offenders could of fled the scene...

It's a disgrace that It's very likely I will have to claim on my own policy, the car was insured at the time of the incident, the third party has claimed they have sold the car and yet there is still no proof of any invoices presented to show this.

I've chased the police up and asked for updates they have said there isn't any what more can I do?! You can't say well if i'm not making an effort they won't. I don't have the resources to do all the legwork, the third party insurers won't speak to me, all the communication has to be the claim handler.

Maybe i should just switch to traders insurance, drive around like an idiot, if I crash, no problem! I'll just fled the scene and say the car is closed, leaving the other driver facing years of already high insurance premiums!!

I could of taken the keys out of their car and wait until the police come and make the situation escalate in a bad way which I would of got a ticking off for and possibility at the same time the offenders could of fled the scene...

It's a disgrace that It's very likely I will have to claim on my own policy, the car was insured at the time of the incident, the third party has claimed they have sold the car and yet there is still no proof of any invoices presented to show this.

I've chased the police up and asked for updates they have said there isn't any what more can I do?! You can't say well if i'm not making an effort they won't. I don't have the resources to do all the legwork, the third party insurers won't speak to me, all the communication has to be the claim handler.

Maybe i should just switch to traders insurance, drive around like an idiot, if I crash, no problem! I'll just fled the scene and say the car is closed, leaving the other driver facing years of already high insurance premiums!!

Well I went around said trader, turns out it's a gearbox specialist place.

Spoke to the owner, explained the situation, stated he's never seen that car before, yeah right! The car was under your policy mate so how can you not know of the car! He was smiling too saying: "no, no never seen it before, sorry"

Went back to the premises just now, (midnight) place was closed but their parking area wasn't and it had a few cars in there but no trace of the renault that hit me. - Bit stupid to think it would be there anyway. Will pop back later in the morning and show the workers a pic of car see if I can get a bit of luck.

Searched the local area, funnily enough spotted 10 of the same make and model of the car that hit me but not the offending vehicle I was itching to find.

TBH, it's a waste of time even bothering searching, it's central Birmingham, so many side roads and places the car be easily left to blend in.. - The chances of finding the car now after 2 weeks of the incident happening is very slim.

Will phone up the police to see if I can get some more information to see where was the last place the car was spotted on ANPR, that's if they will share the information. They said it can take up to 12 weeks to get a report on the car which is ridiculous, the incident hasn't even been passed to the traffic processing unit as of yet.

Phoned up the claims handler and said are you sure the address you've given me was the right place they said, just don't worry about it, you may feel we are not doing much about it but rest assured we are, let us do our jobs blah blah.

Just feel a bit hopless tbh, god knows where that car is. Will pop around tomorrow to ask the workers if they know anything about the car and then get a mate to pop around later to see if they can recommend a decent body shop repairer and then try that place out if they've got the car or had it in for any work.

Just want to nail these frauds, still haven't even sent over proof of invoice to show car's been sold. The owner knows the car, probably was his son or member of staff, will again try and see if I can spot anyone working there who was in the car at the time of incident.

Spoke to the owner, explained the situation, stated he's never seen that car before, yeah right! The car was under your policy mate so how can you not know of the car! He was smiling too saying: "no, no never seen it before, sorry"

Went back to the premises just now, (midnight) place was closed but their parking area wasn't and it had a few cars in there but no trace of the renault that hit me. - Bit stupid to think it would be there anyway. Will pop back later in the morning and show the workers a pic of car see if I can get a bit of luck.

Searched the local area, funnily enough spotted 10 of the same make and model of the car that hit me but not the offending vehicle I was itching to find.

TBH, it's a waste of time even bothering searching, it's central Birmingham, so many side roads and places the car be easily left to blend in.. - The chances of finding the car now after 2 weeks of the incident happening is very slim.

Will phone up the police to see if I can get some more information to see where was the last place the car was spotted on ANPR, that's if they will share the information. They said it can take up to 12 weeks to get a report on the car which is ridiculous, the incident hasn't even been passed to the traffic processing unit as of yet.

Phoned up the claims handler and said are you sure the address you've given me was the right place they said, just don't worry about it, you may feel we are not doing much about it but rest assured we are, let us do our jobs blah blah.

Just feel a bit hopless tbh, god knows where that car is. Will pop around tomorrow to ask the workers if they know anything about the car and then get a mate to pop around later to see if they can recommend a decent body shop repairer and then try that place out if they've got the car or had it in for any work.

Just want to nail these frauds, still haven't even sent over proof of invoice to show car's been sold. The owner knows the car, probably was his son or member of staff, will again try and see if I can spot anyone working there who was in the car at the time of incident.

Yeah It was silly going to the garage and asking about the car, of course he's going to deny it.

Going to the papers won't achieve nothing if It would make a difference then I would 100% be behind the idea.

Thanks, the vehicle registration is BG04RRV silver Renault Megane.

So now the car is in the process of being inspected on Monday through my own Insurance co, will have to pay excess (£500)

After telling them that I don't want to use their crappy approved bodyshop repairer (that's if the car isn't categorised) I was told if I went down the route of using my own choice of repairer, I would be liable for the courtesy car costs? WTH? The claims company is their own in house one and they said on the phone that I wouldn't be liable for any costs as long as I was cooperative with their enquiries and the claim wasn't fraudulent....

I'm hoping my car is a write off anyway, don't have faith in it ever be the same. 2010 Audi S3, 34,000 miles, fully loaded, 8 very short owners. If this one was a cat albeit slightly double miles then I'm hoping mine is and I can buy it back for pennies. (rolls eyes) https://www.copart.co.uk/lot/22725387/?resultIndex...

Here's the damage.

[url]

[url]

|http://thumbsnap.com/rId6TUWh[/url]

|http://thumbsnap.com/rId6TUWh[/url]

Going to the papers won't achieve nothing if It would make a difference then I would 100% be behind the idea.

Thanks, the vehicle registration is BG04RRV silver Renault Megane.

So now the car is in the process of being inspected on Monday through my own Insurance co, will have to pay excess (£500)

After telling them that I don't want to use their crappy approved bodyshop repairer (that's if the car isn't categorised) I was told if I went down the route of using my own choice of repairer, I would be liable for the courtesy car costs? WTH? The claims company is their own in house one and they said on the phone that I wouldn't be liable for any costs as long as I was cooperative with their enquiries and the claim wasn't fraudulent....

I'm hoping my car is a write off anyway, don't have faith in it ever be the same. 2010 Audi S3, 34,000 miles, fully loaded, 8 very short owners. If this one was a cat albeit slightly double miles then I'm hoping mine is and I can buy it back for pennies. (rolls eyes) https://www.copart.co.uk/lot/22725387/?resultIndex...

Here's the damage.

[url]|http://thumbsnap.com/rId6TUWh[/url]Pip1968 said:

I would put a few pictures of the TP's vehilce up and not yours. The focus is the missing car not your damage! Then put something in the county section of PH maybe under 'spotted' ie Have you seen this vehicle? If you are on Facebook put something on there. Use it like some do for publicity for crowd funding. Maybe someone will be able to help. If you want to go further an advert in the local rag 'Reward for where abouts of this vehicle'.

They are scum but seemingly everywhere.

I had something similar about fifteen years ago. Hit at a roundabout by a van and had to pay out as the driver did not put a claim in. A year or so later the legal people took the company to court and got my excess back. Company were trying to say that the driver was responsble for his own insurance.

Pip

A good point, will get one up and running shortly. I did actually put a post up on a very local car community page offering a £1000 reward for information leading to the whereabouts to the car and the person who owns it and judging by a few responses and a few people tagging someone I knew, - it was clear a few people on the group did know the person but wouldn't share me their details, one of them being a childhood friend who I now no longer speak to as he knows the person but wouldn't give me any details.They are scum but seemingly everywhere.

I had something similar about fifteen years ago. Hit at a roundabout by a van and had to pay out as the driver did not put a claim in. A year or so later the legal people took the company to court and got my excess back. Company were trying to say that the driver was responsble for his own insurance.

Pip

When I threatened to inform the police that he maybe withholding information for a crime that's been committed the majority of the page turned against me calling me a all sorts for names under the sun for bringing the "feds" in the picture and a"snitch" shortly afterwards, I was blocked.

Funny thing is though, those same people if the tables were turned and were in the same position, or if there car was stolen, they would be putting up information on all these car pages and would be going to the police. Bunch of idiots.

I've been in involved in an accident with a hit and run driver. (Got their registration, however policyholder who is a motor trader claiming vehicle was sold which is a lie) Anyway I've got to go through my own insurance co and the MIB to reclaim the eventual losses...

I've got to pay my excess and the insurance co is taking the car to a bodyshop which is crap based on the reviews posted online. I want to take it to Audi to get it repaired if it's repairable (touchwood the costs are too high and they write it off)

However my insurance co are stating if I take it elsewhere of my choice then the max they'll pay per hour is £27 and anything above that, I would be liable for the amount. Is that right, are they allowed to say this? The dozen other decent bodyshops i contacted who charged 45+ an hour stated that the bodyshop will do a rubbish substandard job and it will come out looking like previous damage has been inflicted on the car which I don't want as when I come to sell if panels look out of place and places look like it's been painted over then it's going to be difficult if prospective buyers notice these areas..

I've told them that i'm not happy and if the car had to go to the bodyshop of their choice and it was a crap job, I will give them a chance to rectify the problem, and if it's crap again I will demand that the work is taken elsewhere and stripped and done again,

Also, it's likely the bodyshop will use pattern parts, can i demand that they use genuine oem parts, the car isn't a banger, It's a 16k car and I don't want corners to be cut.

Lastly, i'm wating on the engineers report and the cost of the repair if it's repairable, can I ask my insurance co for cash in lieu payment of damages - I know people have mentioned that asking this could raise suspicions but the claim is 100% genuine, police were involved, the policy of third party was traced back to a motor trader who claims the car was sold when the accident happened.. They did tell me though when i asked them that usually a cash in lieu payment is usually only made if parts are hard to obtain for repair.

I've got to pay my excess and the insurance co is taking the car to a bodyshop which is crap based on the reviews posted online. I want to take it to Audi to get it repaired if it's repairable (touchwood the costs are too high and they write it off)

However my insurance co are stating if I take it elsewhere of my choice then the max they'll pay per hour is £27 and anything above that, I would be liable for the amount. Is that right, are they allowed to say this? The dozen other decent bodyshops i contacted who charged 45+ an hour stated that the bodyshop will do a rubbish substandard job and it will come out looking like previous damage has been inflicted on the car which I don't want as when I come to sell if panels look out of place and places look like it's been painted over then it's going to be difficult if prospective buyers notice these areas..

I've told them that i'm not happy and if the car had to go to the bodyshop of their choice and it was a crap job, I will give them a chance to rectify the problem, and if it's crap again I will demand that the work is taken elsewhere and stripped and done again,

Also, it's likely the bodyshop will use pattern parts, can i demand that they use genuine oem parts, the car isn't a banger, It's a 16k car and I don't want corners to be cut.

Lastly, i'm wating on the engineers report and the cost of the repair if it's repairable, can I ask my insurance co for cash in lieu payment of damages - I know people have mentioned that asking this could raise suspicions but the claim is 100% genuine, police were involved, the policy of third party was traced back to a motor trader who claims the car was sold when the accident happened.. They did tell me though when i asked them that usually a cash in lieu payment is usually only made if parts are hard to obtain for repair.

Too early to say, could be other issues that they find when inspecting the car but it's seems unlikely to be a write off.

I will check my policy what it states, what I do know is that I won't be charged extra for taking it elsewhere, I'll just lose the benefit of a courtesy car.

Does anyone know how the insurance co/assessors come to determining value the car? Parkers/glass guide? Do they take into consideration amount of previous owners? I've just done a valuation check on motoring.co.uk and autotrader and both sites are coming back with a 14.5 - 15k figure.

I'm was not aware you can ask your potential insurers when taking out a policy that you could ask to only use dealers only for repair in an event of a claim that results in a repair, if this was something I was made aware of when taking out the policy I would of 100% have done this.

Would an option be if the assessors report comes back as say 7k, could I ask for a cash in lieu payment minus the labour charge but exclusive of the vat on the parts to fix the car myself?

I will check my policy what it states, what I do know is that I won't be charged extra for taking it elsewhere, I'll just lose the benefit of a courtesy car.

Does anyone know how the insurance co/assessors come to determining value the car? Parkers/glass guide? Do they take into consideration amount of previous owners? I've just done a valuation check on motoring.co.uk and autotrader and both sites are coming back with a 14.5 - 15k figure.

I'm was not aware you can ask your potential insurers when taking out a policy that you could ask to only use dealers only for repair in an event of a claim that results in a repair, if this was something I was made aware of when taking out the policy I would of 100% have done this.

Would an option be if the assessors report comes back as say 7k, could I ask for a cash in lieu payment minus the labour charge but exclusive of the vat on the parts to fix the car myself?

Thank you all for your help, yes I've been looking online and it seems that the insurance co is just trying to fob me off in regards to taking the car to a bodyshop of my choice, I have a legal right, yes I lose my rights to a hire car and no protection in regards to warranty/guarantee of repair but that's clear across the board. I won't get charged extra for taking it to a place of my own choice either, my excess is £500 as standard nothing else. The other handler I had spoken to from my insurers was probably just trying to scare me in saying I would be liable for the current courtesy car costs.

I will demand that the car goes to a bodyshop of my choice, Audi or someone reputable who will use, proper genuine oem parts and actually take care when carrying out repairs.

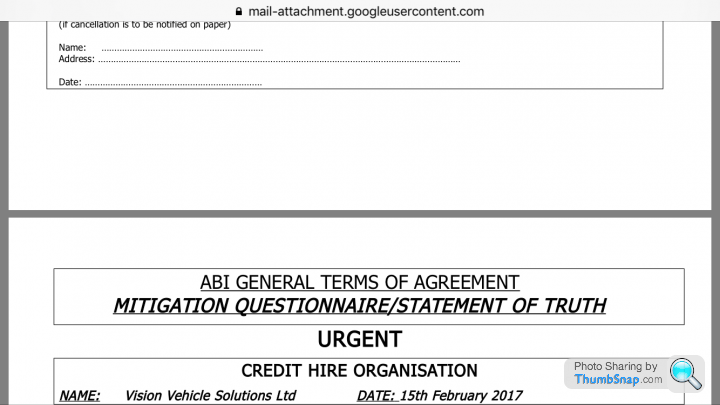

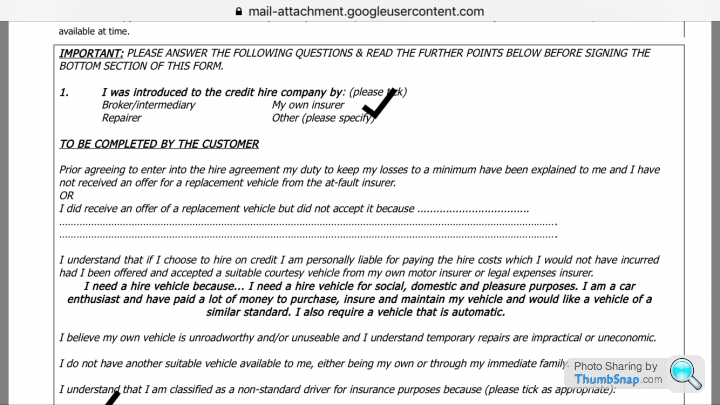

Yes identifiable vehicle which at the time showed as insured by my insurers, the police and the claims company my own insurers referred me to. Claims company have sent me out document to sign to send off to the MIB, I'm claiming off my insurers and they will recover their costs from the MIB.

I will demand that the car goes to a bodyshop of my choice, Audi or someone reputable who will use, proper genuine oem parts and actually take care when carrying out repairs.

source said:

The right to use your own repairer is covered under the consumer rights directive 1993, The Association of British Insurer's (A.B.I.) What was the Office of Fair Trade (OFT) the Financial Service Authority(FSA) which is now the FCA and the Vehicle Body Repair Association (VBRA/RMI) all agreed that the consumer has the right to choose!

The Consumer rights act 2015 now supercedes it.

Motor Vehicle block exemption regulations ec1400/2002

EU law ensures, for competitive purposes, that every car owner has the right to freely choose any repair shop to provide services and repairs for their vehicle (see the Block Exemption for motor vehicles and the Market Court (2012:13)). Manufacturers are obligated to provide the information necessary for any independent repair shop to be able to perform these repairs and services.

Application part 8 of the Enterprise act for unfair trading regulations 2008

The Consumer Protection for unfair trading regulations 2008 and application 8 of 2002 enterprise act, prohibits unfair commercial practices including agressive "Steerage techniques" and misleading actions, these are action which may materially distort your economic behaviour.

“materially distort the economic behaviour” means in relation to an average consumer, appreciably to impair the average consumer’s ability to make an informed decision thereby causing him to take a transactional decision that he would not have taken otherwise;

2015 Insurance Act also stipulates prior to a contract occuring, the insurer has to make the insured aware that the contract fulfills the demands and needs of the consumer,and any adverse term or condition is brought to the attention of the consumer. This should have no material detriment to the consumer. To advise after the contract has occured any restriction's in the consumers choice, or advise that you seek to reduce your contractural liabilities is a breach of the act.

http://www.motorclaimguru.co.uk/your-rights-as-a-c...

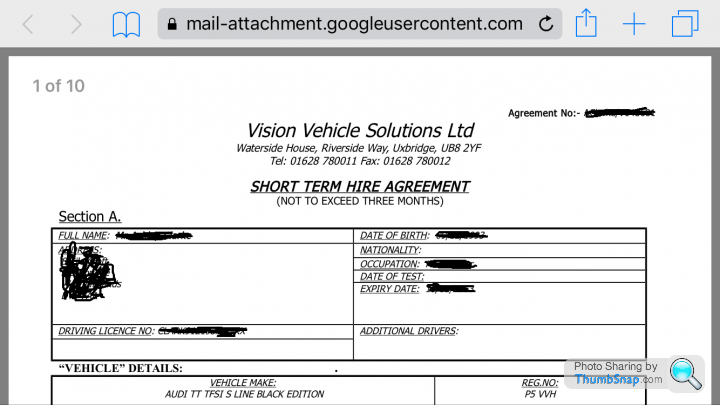

Also i'm not actually sure if i'm in a hire car or not? My insurers are markerststudy and the claims management company is vision vehicles, markerstudy bought them out in 2013 so now part of the markerstudy group.The Consumer rights act 2015 now supercedes it.

Motor Vehicle block exemption regulations ec1400/2002

EU law ensures, for competitive purposes, that every car owner has the right to freely choose any repair shop to provide services and repairs for their vehicle (see the Block Exemption for motor vehicles and the Market Court (2012:13)). Manufacturers are obligated to provide the information necessary for any independent repair shop to be able to perform these repairs and services.

Application part 8 of the Enterprise act for unfair trading regulations 2008

The Consumer Protection for unfair trading regulations 2008 and application 8 of 2002 enterprise act, prohibits unfair commercial practices including agressive "Steerage techniques" and misleading actions, these are action which may materially distort your economic behaviour.

“materially distort the economic behaviour” means in relation to an average consumer, appreciably to impair the average consumer’s ability to make an informed decision thereby causing him to take a transactional decision that he would not have taken otherwise;

2015 Insurance Act also stipulates prior to a contract occuring, the insurer has to make the insured aware that the contract fulfills the demands and needs of the consumer,and any adverse term or condition is brought to the attention of the consumer. This should have no material detriment to the consumer. To advise after the contract has occured any restriction's in the consumers choice, or advise that you seek to reduce your contractural liabilities is a breach of the act.

http://www.motorclaimguru.co.uk/your-rights-as-a-c...

Yes identifiable vehicle which at the time showed as insured by my insurers, the police and the claims company my own insurers referred me to. Claims company have sent me out document to sign to send off to the MIB, I'm claiming off my insurers and they will recover their costs from the MIB.

Edited by captainhook on Monday 6th March 21:08

Edited by captainhook on Monday 6th March 21:11

anniesdad said:

OP, yes it's a credit hire car supplied by Vision Vehicle Solutions. Markerstudy bought the company a few years ago as you say, if you can't beat 'em...

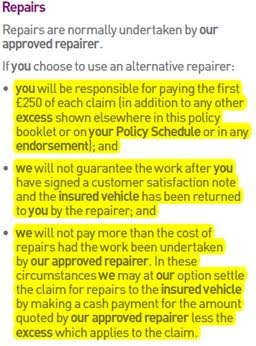

It's not a courtesy car that you are driving. The expectation is that the third party and/or their insurers will pay for the vehicle that you are hiring. VVS should explain to you about your right to hire a car and your liability in doing so.

You could call your local Audi approved repairer and ask them if they have a courtesy car that they would be prepared to supply to you? Sounds like you've got a third party that is looking to wriggle out of this on a probable fabricated technicality, their insurers will be only too happy to oblige. Did you say you have a lawyer representing you?

Understood, I hate dealing with claim management companies because it's clear that the vast majority have their own interest at heart and don't proactively try and get things wrapped up in relation to establishing liability with TP insurers as quickly as they can do in most cases. Only reason I went with them is because I needed a CC as mine was completely unroadworthy and insurers recommended to use them as they are in house, to keep costs down and mitigate losses..It's not a courtesy car that you are driving. The expectation is that the third party and/or their insurers will pay for the vehicle that you are hiring. VVS should explain to you about your right to hire a car and your liability in doing so.

You could call your local Audi approved repairer and ask them if they have a courtesy car that they would be prepared to supply to you? Sounds like you've got a third party that is looking to wriggle out of this on a probable fabricated technicality, their insurers will be only too happy to oblige. Did you say you have a lawyer representing you?

However I would never use them again, very early on it was established that TP claimed the vehicle was sold at time of incident, they couldn't tell me when TP had sold the vehicle or give me any information on when they could get proof from the TP insurers inform of an invoice of any type to show the vehicle had been sold and every time I called, (reasonable time period between calls too) I've been greeted with an attitude that portrayed that I was an nuisance which was clear by the tone of the operator and the claims handler who had come over very sarcastic at times like they knew it all and I didn't. They've been hopeless and since the 14th Feb when the started working on the claim, they could of easy established from the TP if the vehicle was indeed sold with proof, something they haven't even established, in the form of invoice proof. I've asked them for the actual information on what they hold on the TP and their insurers as I've phoned Tradex a dozen times and have stated no such vehicle as been insurered through them and they have been unwilling to give me the info to do my own lines of enquiry.

I'm not using a solicitor unfortunately. Vision are the ones dealing with the claim on behalf of markerstudy.

Tomorrow, first thing, I will ask them to divert the car to a local Audi approved centre to let them carry out the estimate of the car and I will state that I will not compromise on the repairs and I refuse to use their shoddy bodyshop.

KungFuPanda said:

I'm surprised a credit hire company gave you a car despite the potential insurance and indemnity issues.

Cowboys? No suprised really the way they've handled my claim. I don't know what goes on behind the scenes but I certainty don't think they handled they way they could of.. anniesdad said:

No comment other than to say that it is very much in the interest of the AMC to wrap up liability early on. A solicitor may see things somewhat differently however...

They should divulge the information they do have to you, however they are somewhat reliant upon the third party insurers exchanging information.

VVS should still provide you with a hire vehicle until the repairs are completed.

They should divulge the information they do have to you, however they are somewhat reliant upon the third party insurers exchanging information.

VVS should still provide you with a hire vehicle until the repairs are completed.

anniesdad said:

OP, as an aside, you have the name of the company that bought the motor trade policy off Tradex. They are the only organisation other than their insurance broker that can change the covered vehicles on the policy. You have on one hand an insurer saying that their policyholder sold the vehicle prior to the accident and on the other the company owner saying he doesn't know what car you are talking about. I believe, you have enough to commence legal proceedings should you choose to do so, as it makes an interesting story for a judge to hear...

However you do have some support here. I can understand why you might be angsty and wanting to get this resolved tomorrow. I can tell you that won't happen and despite your supposition that this can get sorted just with a couple of phone calls the sad reality is that it won't. VVS are acting for you, they know what they are doing. Your insurers less so, as they frankly have given you some pretty shoddy advice by the sounds of it. Just hang in there and do what you suggest, demand the car be repaired by your chosen repairer. If they maintain that you will be partially liable for the damage other than the £500 excess then ask them to point to the relevant clause in the policy that confirms this (you can read the policy wording yourself in the mean time so as to understand your cover better). If they do have such a clause, I'm sure that at renewal time you'll be going elsewhere if this sorry business hasn't convinced you to do that already.

Super, well i'll told them under no circumstances that I want my vehicle repaired with those shoddy cowboys which they now agree that that isn't a problem and haven't mentioned about taking the courtesy car away from me, as of yet..However you do have some support here. I can understand why you might be angsty and wanting to get this resolved tomorrow. I can tell you that won't happen and despite your supposition that this can get sorted just with a couple of phone calls the sad reality is that it won't. VVS are acting for you, they know what they are doing. Your insurers less so, as they frankly have given you some pretty shoddy advice by the sounds of it. Just hang in there and do what you suggest, demand the car be repaired by your chosen repairer. If they maintain that you will be partially liable for the damage other than the £500 excess then ask them to point to the relevant clause in the policy that confirms this (you can read the policy wording yourself in the mean time so as to understand your cover better). If they do have such a clause, I'm sure that at renewal time you'll be going elsewhere if this sorry business hasn't convinced you to do that already.

In regards to legal proceedings, I very much want to do so against the TP and their insurers, however will I need to instruct a solicitor to do so? Even though VVS are 'dealing with my claim?' I will need VVS to also co-operate and send as much details they have in regards to the info they hold on the TP and their insurers if I were to instruct a solicitor to act on my behalf through the courts as right now, the info VVS are giving me in relation to the TP insurers are wrong - they are claiming no such vehicle has ever been insurerd with them.

In regards to taking it elsewhere and paying any differences it's now been cleared up:

Edited by captainhook on Tuesday 7th March 12:06

No you are right, VVS aren't a cowboy company but I strongly standby my opinion that the service you receive when it comes to handling claims in similar scenario bows down to who is dealing with your claim. The police have been PATHETIC, I have limited resources to get liability, what the TP insurers should of done is investigate if the car was indeed actually sold and obtain proof from the policyholder to back up their claim to state the vehicle was sold, they haven't so I bloody hope they get hit with a big bill when liability from on there side is established.

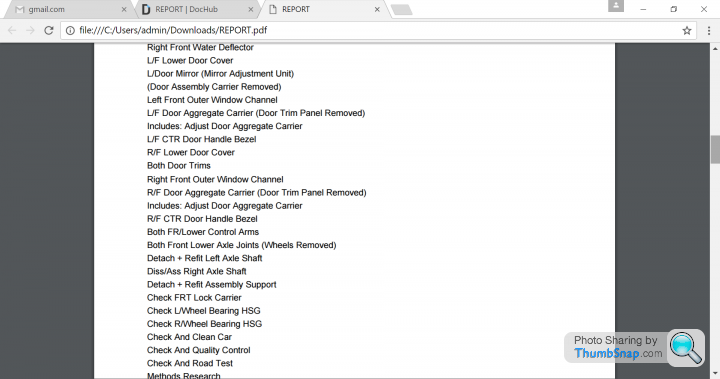

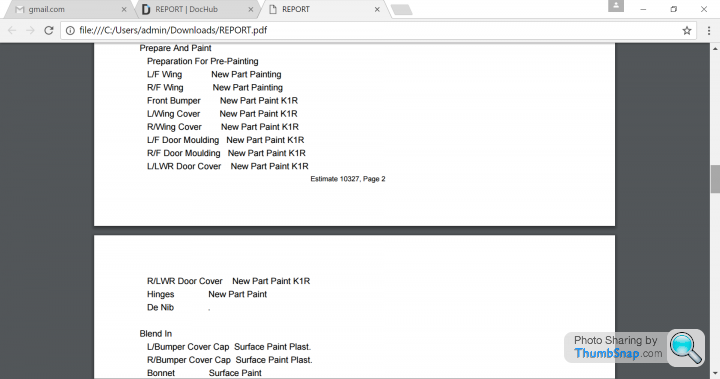

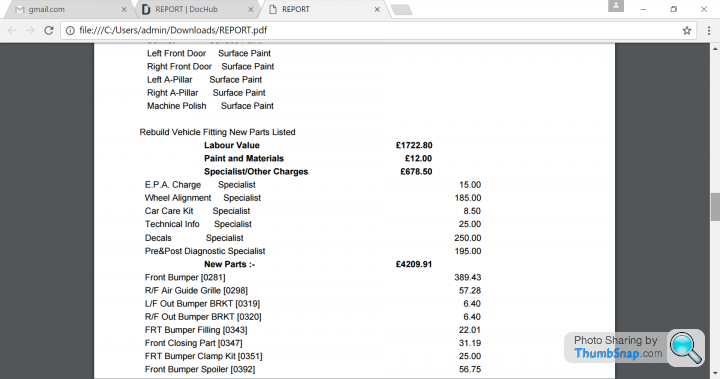

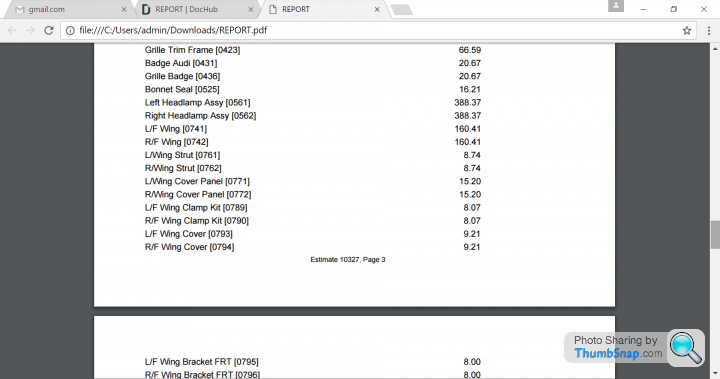

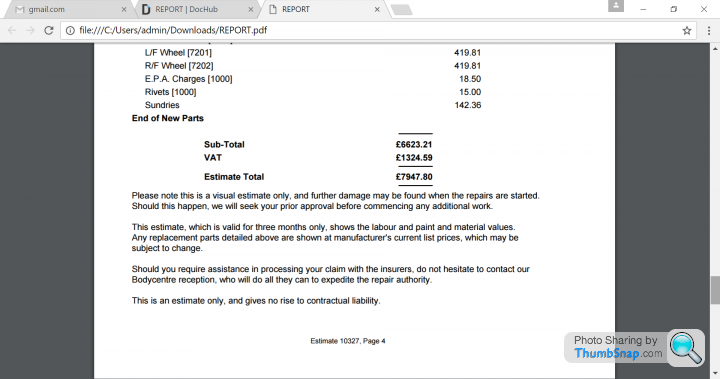

Anyway the car has been to my Audi approved repairer and the repair bill has been valued at 8k, and costs may rise once they start stripping parts and unearth more damage.. the bodyshop assessor said it's 50-50 in terms of a write off - I no longer want the car.

My insurer say they use glass and cap to value the car so with it being a 60% margin for a write off it may seem unlikely..

My 2010 S3 with 35000 on the clock is valued at £14850 - £15500 on the cap website (private sale) so at 14,850 if the 60% write off figure was applied with 14,850 being the lowest price from engineers car value point of view the repair costs would have to exceed £8910 to deem a write off.

The car on the glass guide website is valued at: 14,320 at a private guide price, so at s 60% margin using glass the repair bill will have to exceed 8610 to deem a write off..

I'm just hoping they bloody write it off and if they don't I will push for a few options.

CASH in lieu payment of the damage cost to fix it myself.

Write it off and buy it back so they can obtain their salvage costs back.

Anyway the car has been to my Audi approved repairer and the repair bill has been valued at 8k, and costs may rise once they start stripping parts and unearth more damage.. the bodyshop assessor said it's 50-50 in terms of a write off - I no longer want the car.

My insurer say they use glass and cap to value the car so with it being a 60% margin for a write off it may seem unlikely..

My 2010 S3 with 35000 on the clock is valued at £14850 - £15500 on the cap website (private sale) so at 14,850 if the 60% write off figure was applied with 14,850 being the lowest price from engineers car value point of view the repair costs would have to exceed £8910 to deem a write off.

The car on the glass guide website is valued at: 14,320 at a private guide price, so at s 60% margin using glass the repair bill will have to exceed 8610 to deem a write off..

I'm just hoping they bloody write it off and if they don't I will push for a few options.

CASH in lieu payment of the damage cost to fix it myself.

Write it off and buy it back so they can obtain their salvage costs back.

Edited by captainhook on Tuesday 14th March 21:37

Edited by captainhook on Tuesday 14th March 21:37

Surprise surprise... (NOT!) Markerstudy are claiming that the repair costs are over inflated and have instructed a company called Hoopers to come and inspect the car - I've told them that I want to be present when they are there as I have concerns about the car if it's going to be repaired - namely the airbag light and traction control light. The airbag light im not happy with - I carry kids in the car regularly and if the airbags aren't been replaced then I want to write the car off.

I don't believe the bodyshop have fully inspected the car anyway - I've asked has the car been on the ramp and they said no - so a proper full inspection needs to be carried out because it's clear if it's going to be repaired and further faults are found, markerstudy will be funny in authorizing the aidditonal costs.

Not good, not good at all. Over a month I've been in a hire car and only things have been moving this week. Disgraceful.

Nice of them to do underwriting check on me too - Another way of them trying to wriggle out in paying out the costs. I refuse to use to use their own independent approved bodyshop, they will not use genuine Audi parts, they will not do the job properly and they will treat the car as a number..

Will never use markerstudy EVER AGAIN.

I've seen the repair cost and the repair estimate and no parts have been added that doesn't reflect the damage done. The parts must be REPLACED not repaired where cowboys they wanted me to go would of done.

I don't believe the bodyshop have fully inspected the car anyway - I've asked has the car been on the ramp and they said no - so a proper full inspection needs to be carried out because it's clear if it's going to be repaired and further faults are found, markerstudy will be funny in authorizing the aidditonal costs.

Not good, not good at all. Over a month I've been in a hire car and only things have been moving this week. Disgraceful.

Nice of them to do underwriting check on me too - Another way of them trying to wriggle out in paying out the costs. I refuse to use to use their own independent approved bodyshop, they will not use genuine Audi parts, they will not do the job properly and they will treat the car as a number..

Will never use markerstudy EVER AGAIN.

I've seen the repair cost and the repair estimate and no parts have been added that doesn't reflect the damage done. The parts must be REPLACED not repaired where cowboys they wanted me to go would of done.

KungFuPanda said:

Are Markerstudy your own insurer?

Yes markerstudy are my own insurance co.It's not as if I paid for the cheapest policy ether I've paid them 2400 for the year. Wish I done my research on them on comparethemarket there's hundreds of the same complaints about them.

It has to be sorted Monday the latest, it's making me too stress.

matjk said:

Im no expert, but that looks like a very minor scrape and just cosmetic damage, whats the deal with the ABS and Airbags, surely the airbags didn't go off. And are those brake calipers just painted to look like lambo ones or are they a modification, might give the insurance company wiggle room, just something to bear in mind.

It does look like very minor comestic damage but the damage done reflects what needs to be done, yeah sure, the car probably could get repaired by their approved repairer for a little less than that BUT, they won't use the same genuine oem parts, I don't want pattern parts on a £16k car, the work they will do will also be below standard, I want to take it to someone I trust first time round and these guys I don't mess around - they deal with 6 figure value cars on a daily basis carrying out full conversions to a high standards. It's an Audi car and needs Audi parts and repaired to Audi standards otherwise the value will drop on a shoddy repair.TBF, they did say what the assesor is probably thinking is looking at the pics - He can't believe the repair costs will cost that much which is fair enough, it doesn't look like a 8k+ job but it is, so i understand why they have instructed Hoopers to view the car.

Those brake calipers are a modification, they did tell me the claim went before an underwriters for review for the mods and they are "please to tell me that the checks can back find in regards to declared mods" - So obviously they were looking for ways not to pay out - I'm glad I declared everything..

The airbags didn't go off, however the airbag light kept appearing on and off, intermittently, the ESP is on permanently now once they do further checks they may fight the abs pump or whatever it's called needs replacing, which is about another £1000 on top. I won't be happy having the car back with either the ESP light on, and the airbags replaced, it's a safety hazard and there's no guarantee the airbag deploys when I get the car back and i'm driving, now they either replace those too, or write the car off. I'm stuffed either way as for the next 5 years, I will be paying through the nose for something not my fault.

I've got the report here, there's nothing on here that would say the claim costs are inflated, far from it..

I may come across slightly OTT but the insurers are just trying to get the done on the cheap and i'm not having it, I pay my premiums and in the event of a claim - I expect them to provide the services they are should be providing, promptly and professionally, they aren't do this are are trying to get the car repaired on the cheap, I'm not having it. I want the car back in the position it was prior to the incident, if they don't want to do that then write it off. The report costs are not inflated whatsoever.

matjk said:

Of course the insurance will want to do it as cheaply as possible. Also garages have a habit of changing absolutely eveything when they get wind it's a insurance job, for example there's lots of left hand side and right hand side bits being changes but the photo looks like just one side , obviously we can't see all the damage in the photos but that's the sort of thing the insurance company are going to question. Hope you get it all sorted to your satisfaction, I would be fuming as it wasn't your fault and now your going to be out of pocket. Looks like a nice car too, I like the S3

Damage is on two sides, passenger side wing was crumpled from the impact as both cars collided I was pushed into barrier and went up a curb. - They are also disputing the cars front wheel curb marks too stating it wasn't from the crash but the car was not curbed before incident and no one drives my car, it's just not right, I will be on their case everyday until they get fed up of me.Thanks, it was a nice car, the damage isn't major but now it's all happened, I've just lost interest in it and faith in it, It will never be the same again, - I just hope it's all resolved come the end of next week.

Andehh said:

Sorry to hear OP, any updates?

Hi yes, the insurance stated the repair costs were inflated and said that one of the wheels damaged wasn't caused by the incident and they disputed that a passenger side area of the car was not from the incident.. To be fair if I was looking at the pictures from a computer I would also think that estimate cannot be right, which was what my insurers claim handler was telling me their assessors was having difficulties grasping after the bodyshop sent them images and repair costs amount..An assessor from hoopers, fairly nice chap to be fair came to view the car at the bodyshop, quite quickly came to the conclusion that the all the replacement parts the audi approved repairer put on the estimate was needed and the passenger side area and wheel was in fact damaged from the accident.

The repair costs came just under £8,000 so not a write off, however I'm getting increasingly frustrated with the bodyshop it's now at. I've tried to get through to the chap at the Audi approved bodyshop countless times to ask if i'm going to liable for the difference in their hourly labour rate and he has failed to return my calls after messages upon messages have been left by the first line of contact (receptionists) - My insurance company said they they would only pay the 27PHR labour rate charge that their approved repairer would charge, any difference in the labour rate, I would be liable for that amount, which would be around £700+ pounds, I refuse to pay any more out of my pocket for an accident that was not my fault plus having to pay my excess of £500.

I'm in a difficult situation now, I don't want to use an insurers approved repairer, they will use pattern parts and not do the job properly, if they can guarantee they will purchase genuine audi approved parts and show me invoices to prove they have done so, I will just bite the bullet and end up using them if the bodyshop i've taken the car to, says i'm going to be liable for the difference in labour rate charges.

I've asked my insurance co to just let me sort the car out myself however they are being funny about it saying they would only offer a cash in lieu if parts for the car was not available or it was a classic - I don't understand the difference really them paying the bodyshop or them paying me - though I understand a cash in lieu settlement of damages can raise flags with any insurance company suspecting possible fraud but it's a 100% legit claim and i'll be using the settlement to repair the car, bit silly really, would of had the car on the road by now.

Edited by captainhook on Monday 20th March 22:16

Marketstudy are claiming they are still "awaiting the report" from the the independent assessor, they should have it by the morning so will give them a call back then.

Honestly what a nightmare company to deal with, I honestly wished I've done my research on them before taking out the policy, I would have never have gone near them if I knew the true extent of how bad they are when it comes to claiming - denying claims on technicalities, taking months to sort out simple repairs, the list goes on. How can the likes of FOS, the insurance regulator and so on allow companies like them to get away with it? I wonder what is the percentage of claims they refuse to pay out on for minor technicalities. They should be given strong words to clean up their acts or face sanctions or for the better, complete closure.

I feel like jumping off a cliff, i'm bitter with the idiot who drove off with without stopping and exchanging details, thus making me deal with these chancers and sorry excuse of an insurance company, I've done caring now, they are refusing to pay the difference in the labor rate of my Audi approved repairer which means I will have make up the labor rate difference - My only hope is over the coming days - the audi approved bodyshop and my insurers can come to an agreement on the labor rate so I can use them and not pay a penny to fix the damage. If not, i'll just use their approved repairers, if i'm not happy with the work, get my own independent assessor and if he agrees, take the car elsewhere, bill the insurers for the work to be rectified and threaten to go down the FOS route if they don't play ball.

Honestly what a nightmare company to deal with, I honestly wished I've done my research on them before taking out the policy, I would have never have gone near them if I knew the true extent of how bad they are when it comes to claiming - denying claims on technicalities, taking months to sort out simple repairs, the list goes on. How can the likes of FOS, the insurance regulator and so on allow companies like them to get away with it? I wonder what is the percentage of claims they refuse to pay out on for minor technicalities. They should be given strong words to clean up their acts or face sanctions or for the better, complete closure.

I feel like jumping off a cliff, i'm bitter with the idiot who drove off with without stopping and exchanging details, thus making me deal with these chancers and sorry excuse of an insurance company, I've done caring now, they are refusing to pay the difference in the labor rate of my Audi approved repairer which means I will have make up the labor rate difference - My only hope is over the coming days - the audi approved bodyshop and my insurers can come to an agreement on the labor rate so I can use them and not pay a penny to fix the damage. If not, i'll just use their approved repairers, if i'm not happy with the work, get my own independent assessor and if he agrees, take the car elsewhere, bill the insurers for the work to be rectified and threaten to go down the FOS route if they don't play ball.

PH XKR said:

No way on this green earth is that claim worth the write off figure you are so hopeful of achieving.

Yep, I've come to that conclusion awhile ago.andymc said:

get it fixed and trade it in mate

Will do, not going to stress over it any longer, will just push it this week so either the insurers approved repairer or the audi bodyshop bare minimum puts in the order for the required parts then once sorted, trade it in.Gassing Station | Speed, Plod & the Law | Top of Page | What's New | My Stuff