No news isn't always good news.

Discussion

Bleugh. As the end of tax year looms, as blood pressure increases as ISAs and pension business gets put on the books, some news from Co-funds and Aegon.

In the past day or so, Co-funds has sharpened its SIPP pencil to stick one on other providers and Aegon has slashed prices of its retirement products too. Mainly in response to the budget, mainly with one eye on the Dutch situation, anyone with a decent sized pension fund really should take a look at the new deal.

In a loud and clear Garlick TVR exhaust-esque (yes, I saw the insomniac's Tweet this morning) response to that budget, changes to the Aegon One Retirement proposition are kicking in. The will be a rationalised investment range of around 100 funds (tbc) and a lowering of the drawdown access limit from £50k to £20k - that will affect someone on here who was told he needed £50,000 (I think).

Aegon's press release contains a bit of a gem too, it seems that there is a commitment to move to a fixed charge model in 2015. If they push that one through, it's big news. Aegon now look incredibly competitive at the higher end of the pension fund market as the fixed price kicks in. Co-funds has removed the setup and annual charge on its Suffolk Life-provided Pension Account too.

Does any of this apply to you? Possibly, possibly not - take an informed view yourself or seek advice you trust. I think though, that the announcement from Aegon is potentially massive news, especially for the saver who has saved well. So I'll be junking more files this week (files that replaced the files that got junked after the budget!). Great.

In the past day or so, Co-funds has sharpened its SIPP pencil to stick one on other providers and Aegon has slashed prices of its retirement products too. Mainly in response to the budget, mainly with one eye on the Dutch situation, anyone with a decent sized pension fund really should take a look at the new deal.

In a loud and clear Garlick TVR exhaust-esque (yes, I saw the insomniac's Tweet this morning) response to that budget, changes to the Aegon One Retirement proposition are kicking in. The will be a rationalised investment range of around 100 funds (tbc) and a lowering of the drawdown access limit from £50k to £20k - that will affect someone on here who was told he needed £50,000 (I think).

Aegon's press release contains a bit of a gem too, it seems that there is a commitment to move to a fixed charge model in 2015. If they push that one through, it's big news. Aegon now look incredibly competitive at the higher end of the pension fund market as the fixed price kicks in. Co-funds has removed the setup and annual charge on its Suffolk Life-provided Pension Account too.

Does any of this apply to you? Possibly, possibly not - take an informed view yourself or seek advice you trust. I think though, that the announcement from Aegon is potentially massive news, especially for the saver who has saved well. So I'll be junking more files this week (files that replaced the files that got junked after the budget!). Great.

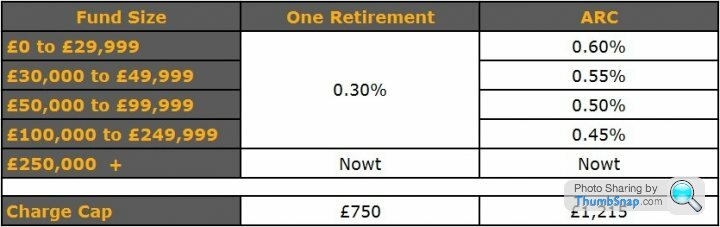

Sure - in summary, Aegon has announced revised charging structures on its ARC platform and its One Retirement pension, which one are you? From 3 May there is a now a price cap ceiling at £250k. This is a table I have pinched which shows the new charging structure.

I'm not sure yet how the impact will be rolled out to existing clients, but it should mean quite useful savings across the board. If you have a large fund, the benefits seem obvious. Working with other wrappers and funds on the ARC platform, large funds now stand to make seriously impressive gains. The biggest news is Aegon's seeming intention to charge according to a fixed fee.

I'm not sure yet how the impact will be rolled out to existing clients, but it should mean quite useful savings across the board. If you have a large fund, the benefits seem obvious. Working with other wrappers and funds on the ARC platform, large funds now stand to make seriously impressive gains. The biggest news is Aegon's seeming intention to charge according to a fixed fee.

If you asked someone at work, even if you phoned the call centre at Aegon, they probably wouldn't know. Wait a week or so and then e-mail your pension point of contact. Just copy and paste something like this.

I have an Aegon pension contract. Given the recent announcement by Aegon, can you tell me how the restructuring of the charges that relate to their retirement contracts will apply to my occupational pension (number #**********).

I have an Aegon pension contract. Given the recent announcement by Aegon, can you tell me how the restructuring of the charges that relate to their retirement contracts will apply to my occupational pension (number #**********).

Well, I suggested the risk was one of legislation and legislation.

Just as we did away with annuities and allowed everyone to declare open season on their pension savings, Australia is now consulting on whether to implement some form of *compulsory* annuitisation in a bid to allow retirees to mitigate the longevity risks associated with drawdown versus expensive/poor fund performance (cheapest isn't always best, but neither is expensive always best!).

Australia is looking at encouraging/forcing savers to purchase retirement income products: ‘Risk management is a major weakness of the drawdown phase. Although individual are concerned about outliving their savings, few retirees use income stream products with longevity risk protection, and there is a limited choice of these products.’

Why is this significant?

Because just the other month George Osborne stated that ‘no one will need to buy an annuity!' and because in the past, we have tended to keep a beady eye on what Australians are doing with their financial planning. Most advisers believe the audacity of Osborne's move was based on political motivation. If Labour gets in (cue noises about nationalising the rail network again already, etc) what's the bet that this will be on the agenda again?

http://www.ftadviser.com/2014/07/17/pensions/perso...

(Apologies, you might need a free trial log in to read that)

Just as we did away with annuities and allowed everyone to declare open season on their pension savings, Australia is now consulting on whether to implement some form of *compulsory* annuitisation in a bid to allow retirees to mitigate the longevity risks associated with drawdown versus expensive/poor fund performance (cheapest isn't always best, but neither is expensive always best!).

Australia is looking at encouraging/forcing savers to purchase retirement income products: ‘Risk management is a major weakness of the drawdown phase. Although individual are concerned about outliving their savings, few retirees use income stream products with longevity risk protection, and there is a limited choice of these products.’

Why is this significant?

Because just the other month George Osborne stated that ‘no one will need to buy an annuity!' and because in the past, we have tended to keep a beady eye on what Australians are doing with their financial planning. Most advisers believe the audacity of Osborne's move was based on political motivation. If Labour gets in (cue noises about nationalising the rail network again already, etc) what's the bet that this will be on the agenda again?

http://www.ftadviser.com/2014/07/17/pensions/perso...

(Apologies, you might need a free trial log in to read that)

Some more platform/wrap news that allows a little light into the (still) murky world of costs and charges. Hargreaves Lansdown launches a non advised model portfolio service for 2% or so.

http://www.investmentweek.co.uk/investment-week/ne...

http://www.investmentweek.co.uk/investment-week/ne...

Considering EIS wrapper?

Never let the tax tail wag the investment dog. I posted the other day that I was disinclined to use Octopus and at the risk of saying I told you so, I do feel that sometimes, grasp of the validity of the underlying investments gets subordinated to commercial opportunities - more so these days, as VCT/EIS gets more mainstream. If appropriate, still choose carefully.

http://m.citywire.co.uk/money/lower-risk-film-fund...

Never let the tax tail wag the investment dog. I posted the other day that I was disinclined to use Octopus and at the risk of saying I told you so, I do feel that sometimes, grasp of the validity of the underlying investments gets subordinated to commercial opportunities - more so these days, as VCT/EIS gets more mainstream. If appropriate, still choose carefully.

http://m.citywire.co.uk/money/lower-risk-film-fund...

Gassing Station | Finance | Top of Page | What's New | My Stuff