Average investing cost, subscriptions into Investment ISA.

Discussion

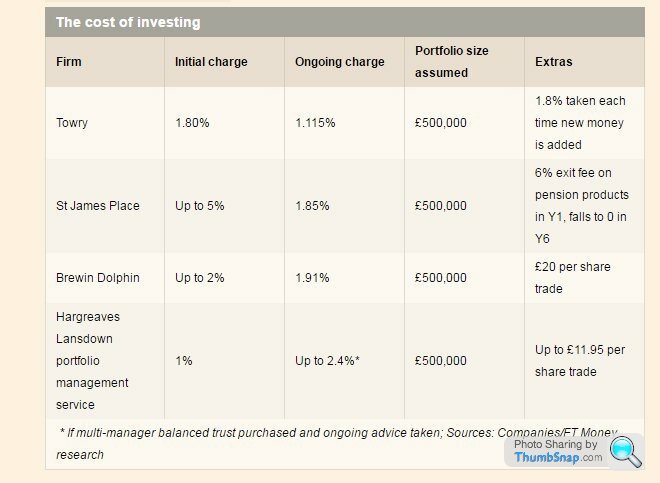

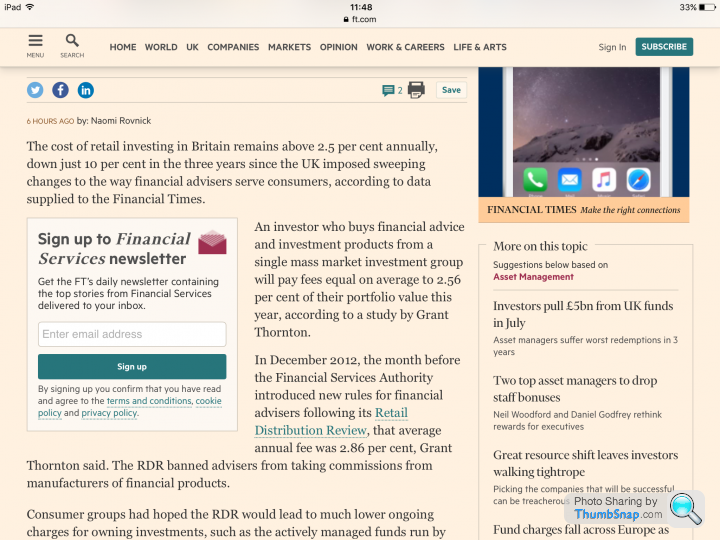

Money into the (investment) ISA wrapper increased by 20%, and the average cost of a retail investment is now a jaw dropping c.2.5% per annum. TWO POINT FIVE PERCENT???? Anyone who pays 2% (let alone 2.5) needs counselling.

Just thought you'd like to know - it's Friday after all, the sun is out and I've just decided to stack for the day and go mow the lawn. These links shouldn't be hiding behind paywalls.

https://www.gov.uk/government/statistics/individua...

https://www.ft.com/content/ba0ae18c-6a98-11e6-a0b1...

Just thought you'd like to know - it's Friday after all, the sun is out and I've just decided to stack for the day and go mow the lawn. These links shouldn't be hiding behind paywalls.

https://www.gov.uk/government/statistics/individua...

https://www.ft.com/content/ba0ae18c-6a98-11e6-a0b1...

sidicks said:

Isn't the 'average' cost entirely meaningless, given the variety of different underlying exposures which you can have in an ISA?

Paying 0.5% would seem high for a UK equity tracker. Paying 2% for an active specialist emerging market equity fund might be quite reasonable.

Wouldn't necessarily disagree. But there again, the 'average client' - whoever that might be, but that's who we're talking about - wouldn't be an aggregate 100% in emerging markets? By way of reference and balance: Paying 0.5% would seem high for a UK equity tracker. Paying 2% for an active specialist emerging market equity fund might be quite reasonable.

I was messaged earlier about this. On top of the fees mentioned, there's the SIPP which (it is claimed) tends to place most of its business in this direction, and the advice cost. Without pinning down the detail, that seems to me to be an annual cost of c.3.2 to 3.5%. They claim it's suitable for a three year strategy. I say 'strategy' of course.

https://www.nedbankprivatewealth.com/nedbank_wealt...

("Let's put 'private client' and 'wealth' on the masthead, think of a number, double it and add it to the cost").

edit: Gosh, here's a surprise - an 'independent' offshore recommendation.

https://www.aesinternational.com/reviews/offshore-...

https://www.nedbankprivatewealth.com/nedbank_wealt...

("Let's put 'private client' and 'wealth' on the masthead, think of a number, double it and add it to the cost").

edit: Gosh, here's a surprise - an 'independent' offshore recommendation.

https://www.aesinternational.com/reviews/offshore-...

Edited by Ginge R on Saturday 27th August 10:44

Simpo Two said:

Ozzie Osmond said:

There are some very low charge operators out there who should also be mentioned. For instance, Cavendish Online offer one of the lowest cost pensions in the market with costs,

On typical funds:

Fund Charge 0.75%, FundsNetwork fee 0.25%, Cavendish Online fee 0.05% = Total Charge of 1.05% per year

On typical tracker funds:

Fund Charge 0.10%, FundsNetwork fee 0.25%, Cavendish Online fee 0.05% = Total Charge of 0.40% per year

Looks astounding value.

How do we think this compares with Old Mutual Wealth, Ginge R? https://www.cavendishonline.co.uk/investments/On typical funds:

Fund Charge 0.75%, FundsNetwork fee 0.25%, Cavendish Online fee 0.05% = Total Charge of 1.05% per year

On typical tracker funds:

Fund Charge 0.10%, FundsNetwork fee 0.25%, Cavendish Online fee 0.05% = Total Charge of 0.40% per year

Looks astounding value.

Let's assume we're focusing on costs. £100,000-£500,000 held on Old Mutual will cost you 0.30%, with Cavendish, it's 0.25%. So, if you add the standing Cavendish charge of 0.20% (which wasn't mentioned by Oz), you're on parity as near as damnit with other platforms. Thereafter, other factors which you may wish to consider, apply. If we strike out fund costs and charges, Cavendish has a series of other sundry charges which creep things up a little - Old Mutual, to its credit, doesn't. So, c.0.49-0.54% to hold assets on both. But, it's all relative.

I've costed that for a singleton Vanguard fund, not all clients suit identical solutions. By comparison, the investment managers I use for 'Fiver' charge 0.46-0.52% which includes discretionary management via a wide variety of funds within a portfolio (and that's the ongoing fund and platform price I will also charge for my pension). I should point out, Fiver also charges a 0.34% annual advisory charge, so at c.0.8% pa, I'm more expensive in that sense, for an 'intelligent' advised service, than both Old Mutual and Cavendish are for a non advised 'iron bomb' one.

Like I said, I'm assuming your reference is costs and charges. Distilling whether or not *any* proposition is right, on a messageboard, is impossible. I fielded an angry call from someone last week who wasn't suitable for Fiver, because I suggested, instead, she use a different service. In a similar vein, and to demonstrate, Aegon bought Cofunds for £140million the other week, ostensibly to provide an 'integrated pension service'. That would make it, possibly, ideal for non advised drawdown clients (worth the premium to some?)? We'll see.

No, over £500,000 the charge is 0.25%. But your post reminded me, when I wrote that earlier, I had forgotten - Old Mutual operates a banding system. This would make Cavendish slightly more cheaper in come cases. If all you want to do is invest a large amount of money and forget about it completely over an extended period of time, it might make more sense. But if that was the case, you'd probably go direct to Vanguard anyway. And extending that logic, if you wanted to take income, move it around or do any number of the things that most people want to do with their money, the prism through which you interpret cost and value would probably change again.

I always consider all of them, and whether or not they are appropriate. Suitability and relevance depends on many things; whether the portfolio is mature, is there a single cogent and cohesive financial strategy (from which wealth management and all subsequent manner of enabling objectives and tactics flow and stand the test of time)?, what are the number of wrappers, the requirements, activity, servicing standards, client requirement for simplicity, and last but not least, costs (etc). Fair to say, since OMW was, effectively, put up for sale (and since CoFunds was bought), platforms are going through yet another state of flux, they are trying to save money and that is having an impact.

Simpo Two said:

You have a gift for writing impressive-looking essays without conclusion. What I actually asked was whether you still recommend OMW, because 18 months ago it was, I was assured against my better judgement, the best thing since sliced bread.

You originally asked if I still used it, and the answer is yes. I have migrated some clients away from it recently though, but not for reasons which always reflect on the proposition. If subsequently, client circumstances change, markedly, so might the recommendation.If I feel that a client is suitable for Platform A over Platform B for any given reason (in answer to your point, above) I will always recommend it. Whether or not I have or haven't recently ("still') is immaterial, that will depend on any recent clients and their unique needs, and not dogma.

Gassing Station | Finance | Top of Page | What's New | My Stuff