What questions should a newbie ask an IFA?

Discussion

We have an IFA coming round this evening for a chat about what we can do with our finances.

I have already given them a breakdown of what is where in a spreadsheet and am looking to convert some of the cash to investments to get greater returns than having it in the bank.

Having never had experience of an IFA, what should I expect and what questions should I be asking to ensure they don't take the cash and put it all on black or something

Like do you give them a cheque and they invest it in the funds they pick or do they give you suggestions then you invest accordingly?

I have already given them a breakdown of what is where in a spreadsheet and am looking to convert some of the cash to investments to get greater returns than having it in the bank.

Having never had experience of an IFA, what should I expect and what questions should I be asking to ensure they don't take the cash and put it all on black or something

Like do you give them a cheque and they invest it in the funds they pick or do they give you suggestions then you invest accordingly?

What is classed as a decent wad, near 6 figures or something a bit less?

Looking on the unbiased page for their company, it does say one of the services they offer is financial planning/wealth management so they may cover what I am after.

Thanks for explaining the difference, I will see what they say this evening as it may not be what I am after as you say.

Looking on the unbiased page for their company, it does say one of the services they offer is financial planning/wealth management so they may cover what I am after.

Thanks for explaining the difference, I will see what they say this evening as it may not be what I am after as you say.

Edited by KTF on Monday 12th September 16:04

Q1: The guy coming round is a 'friend' in so far as I know him through the running club that I go to and he is coming over for an informal chat explaining what it is all about, what his company may be able to offer, etc. I am not expecting the double glazing salesman type pitch from him.

Q2: Yes, I will report back afterwards. I know how much interest I am getting from my various accounts so anything they offer will have to be better than that before I even break even. Not hard I assume but it is at least a figure.

Also why should I choose them vs the various robo options now available as I could just put the money into one of those instead rather than go via a middleman.

Q3: I realise there will be a fee involved but no idea what it will be or how it compares to other IFA/options so I see this as a fact finding exercise and I can then bounce the ideas off the people here - who have more knowledge about this than me from what I have read

Q2: Yes, I will report back afterwards. I know how much interest I am getting from my various accounts so anything they offer will have to be better than that before I even break even. Not hard I assume but it is at least a figure.

Also why should I choose them vs the various robo options now available as I could just put the money into one of those instead rather than go via a middleman.

Q3: I realise there will be a fee involved but no idea what it will be or how it compares to other IFA/options so I see this as a fact finding exercise and I can then bounce the ideas off the people here - who have more knowledge about this than me from what I have read

Ok, as a quick summary whilst I remember.

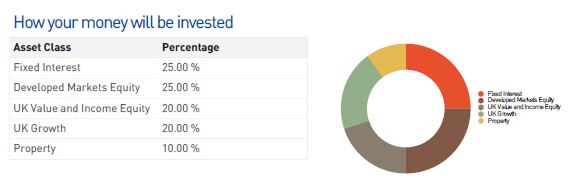

They do fact finding at the start to find out your attitude to risk, what you want to achieve, etc.

Then that is split into the various investment categories, pension, ISA, using this nucleus tool.

Then within each category you have a portfolio based on your risk.

The portfolios are whole of market and have various weighting - low risk is bonds, etc, high risk is oil exploration etc.

You can change them via the IFA but can see an overview any time via the tool.

In the tool you can click the investment category, click the portfolio to see the make up, drill down into the component parts, etc.

The portfolio composition is overseen by a company who can tweak the contents, monitor the returns, etc. to keep them current rather than the IFA try to keep tabs on 4000+ products all the time. Bit like the robo investment tools.

You can have custom built portfolios rather than the mass market robo ones but that costs more due to the work involved.

Management charge for an average risk client portfolio is 1.63%. This covers the IFA as the overseer of the whole process. The value add is them working out the tax efficient strategy then the portfolios in each bucket to use plus regular reviews. No money held by them, all paid in to the tool and invested in the funds.

At a high level the suggestion was to switch from the deposit accounts when the rates drop and regular savers when they mature and drip feed that into a stocks and shares ISA instead to maximise the tax efficiency. The type of ISA will depend on the attitude to risk.

They do fact finding at the start to find out your attitude to risk, what you want to achieve, etc.

Then that is split into the various investment categories, pension, ISA, using this nucleus tool.

Then within each category you have a portfolio based on your risk.

The portfolios are whole of market and have various weighting - low risk is bonds, etc, high risk is oil exploration etc.

You can change them via the IFA but can see an overview any time via the tool.

In the tool you can click the investment category, click the portfolio to see the make up, drill down into the component parts, etc.

The portfolio composition is overseen by a company who can tweak the contents, monitor the returns, etc. to keep them current rather than the IFA try to keep tabs on 4000+ products all the time. Bit like the robo investment tools.

You can have custom built portfolios rather than the mass market robo ones but that costs more due to the work involved.

Management charge for an average risk client portfolio is 1.63%. This covers the IFA as the overseer of the whole process. The value add is them working out the tax efficient strategy then the portfolios in each bucket to use plus regular reviews. No money held by them, all paid in to the tool and invested in the funds.

At a high level the suggestion was to switch from the deposit accounts when the rates drop and regular savers when they mature and drip feed that into a stocks and shares ISA instead to maximise the tax efficiency. The type of ISA will depend on the attitude to risk.

Edited by KTF on Monday 12th September 22:11

The way it was explained was that the 1.63% was made up of the nucleus platform, the fund charge that sit in the pots within nucleus and their fee. It is split into 12 and taken monthly. The fee was an example as it varies depending on the fund mix in each risk category.

Their visit last night was primarily to have a chat about the overall process and explain how it all works. If I go with them then they would do the whole fact finding process to decide the risk rating, etc. The setup fee would be £500 which covers the due diligence, setting up the account on nucleus, etc. then the % charge each year.

Their visit last night was primarily to have a chat about the overall process and explain how it all works. If I go with them then they would do the whole fact finding process to decide the risk rating, etc. The setup fee would be £500 which covers the due diligence, setting up the account on nucleus, etc. then the % charge each year.

castroses said:

'Their visit...' ???

I thought it was just your friend from the running club?

If 'they' turned up as a team then that does sound very 'double glazing salesman' like.

I'd avoid.

It was the guy I know. Bad choice of words on my part. No double glazing salesman tactics just explaining to me the process involved and the options available. The nuts and bolts would be worked out if I went with them, filled in the risk questionnaire, financial questionnaire, etc.I thought it was just your friend from the running club?

If 'they' turned up as a team then that does sound very 'double glazing salesman' like.

I'd avoid.

garyhun said:

The IFA did a complete fact find on my wealth, income, debt etc and an analysis of my attitude to risk and then told me up front that to do an analysis of all my pensions and then a report suggesting any changes would be a fixed fee. He then said that as a follow-up if I wanted him to move the pensions according to the report (if any movement was needed) would be another fixed fee and then if I wanted annual reviews and ongoing management it would be a percentage of the value of my funds.

Right away I knew what all my upfront and ongoing costs would be and thus I am in a position to take some services and not others that I am happy to do myself and fully understand the financial exposure.

This would happen if I signed up with them as the formal process. Last night was an informal chat as shuch giving example fees as they did not know my full financial circumstance.Right away I knew what all my upfront and ongoing costs would be and thus I am in a position to take some services and not others that I am happy to do myself and fully understand the financial exposure.

The paperwork they left explained the stages involved - initial meeting, report produced inc all fees based on their recommendations, second meeting to go over the report.

Last night was like a pre-meeting as such. No specifics, just explaining what they do as I am not familiar with the options available.

JulianPH said:

I'll start with the good bit, because they are very good:

Nucleus is a very good platform and charges 0.35% a year (this reduces as your investment grows). If the total annual cost really is 1.63% then it sounds like the adviser is charging 0.5% and the cost of the underlying investments is 0.78% (which sounds about right).

A £500 flat fee to set everything up is also very good value indeed.

My only concerns are:

1) Why haven't they looked into any outstanding finance you have? For example, it usually makes sense to pay down finance on interest rates higher than you could reasonably expect to receive from your investments.

2) I never like it when costs are not broken down (as I attempted to do above) as it is not very transparent.

3) Do you need to be paying for the platform? Often it is the adviser that gets the most benefit of their clients all being on a platform. However, sometimes the functionality is handy for clients and some platforms get better deals of fund pricing/access. As I said Nucleus is one of the best platforms.

4) What is your adviser doing for the ongoing fee? Once set up correctly this should only need changing every few years in line with changes in your own circumstances.

5) Are you being told to leave a certain amount in cash for unseen emergencies? You should.

In a nutshell, if all stacks up this seems pretty good but there is a growing trend with advisers to move away from platforms and put clients in a low cost discretionary managed portfolio directly with the investment manager. That said, there is usually no cost savings as this is matched by the trend for advisers to swallow up the saving by charging 1% a year for their advice!

As I have already mentioned, advisers do not manage your money - the investment/fund manager does this for you. The adviser simply guides you through some third party risk profiling software and maps you to a portfolios within that risk/reward level. Apart from repeating this every few years that is really it.

Where they add real value is ensuring you are using all your tax allowances,, giving you advice on many other aspects (better mortgage rates, full insurance protection (where needed - wife, kids, etc.) IHT planning and ensuring you are actually putting aside enough money to cover everything, including the income you require in retirement.

If you are going to get all of this then great, this sounds like a good deal. Just be weary of the type of adviser who believes he is some sort of investment genius and ignores all these other things (if they were an investment genius they would be an investment manage/fund manager earning a fortune, not a financial adviser). If you manage to find the former and avoid the latter you are onto a good thing!

Thanks for the advice. To answer some of your points raised.Nucleus is a very good platform and charges 0.35% a year (this reduces as your investment grows). If the total annual cost really is 1.63% then it sounds like the adviser is charging 0.5% and the cost of the underlying investments is 0.78% (which sounds about right).

A £500 flat fee to set everything up is also very good value indeed.

My only concerns are:

1) Why haven't they looked into any outstanding finance you have? For example, it usually makes sense to pay down finance on interest rates higher than you could reasonably expect to receive from your investments.

2) I never like it when costs are not broken down (as I attempted to do above) as it is not very transparent.

3) Do you need to be paying for the platform? Often it is the adviser that gets the most benefit of their clients all being on a platform. However, sometimes the functionality is handy for clients and some platforms get better deals of fund pricing/access. As I said Nucleus is one of the best platforms.

4) What is your adviser doing for the ongoing fee? Once set up correctly this should only need changing every few years in line with changes in your own circumstances.

5) Are you being told to leave a certain amount in cash for unseen emergencies? You should.

In a nutshell, if all stacks up this seems pretty good but there is a growing trend with advisers to move away from platforms and put clients in a low cost discretionary managed portfolio directly with the investment manager. That said, there is usually no cost savings as this is matched by the trend for advisers to swallow up the saving by charging 1% a year for their advice!

As I have already mentioned, advisers do not manage your money - the investment/fund manager does this for you. The adviser simply guides you through some third party risk profiling software and maps you to a portfolios within that risk/reward level. Apart from repeating this every few years that is really it.

Where they add real value is ensuring you are using all your tax allowances,, giving you advice on many other aspects (better mortgage rates, full insurance protection (where needed - wife, kids, etc.) IHT planning and ensuring you are actually putting aside enough money to cover everything, including the income you require in retirement.

If you are going to get all of this then great, this sounds like a good deal. Just be weary of the type of adviser who believes he is some sort of investment genius and ignores all these other things (if they were an investment genius they would be an investment manage/fund manager earning a fortune, not a financial adviser). If you manage to find the former and avoid the latter you are onto a good thing!

1. In short, I don't have any. But this would be covered by the questionnaire I would fill in as part of their process where it asks for income, debt, outgoings that sort of thing.

2. They drew the whole process out last night on a bit of paper and broke down the costs into each chunk - nucleus, the funds and their fee. I cant remember the exact breakdown but it was along the lines of your guess above.

3. As a client I would get 'read only' access to the platform - log in get a grand total with a +/-, ability to drill down into the various holdings, etc. Any changes (for example moving to a different risk rating) would be done by the IFA after a discussion as to why it is needed. It seems to be part of their model as they said they use it to send out correspondence, updates, etc rather than via paper all the time so I dont think it can be opted out.

4. This is the only niggle at the moment as it does seem like they are being the interface for a robo platform which, in theory, I could do myself via fiveraday. As you suggest, once it is up and running, it should look after itself with only minor tweaks needed for life events and the like.

I have multiple pensions so they said they can look at that aspect as well with a view of leaving where they are or combining them plus check that I am investing with a view to minimising tax, etc. I am a while away from retirement/inheritance type events but they could also begin to put the building blocks for that in place.

5. Yes, they said a certain amount should be held back in cash as an emergency and if there were any things planned in the short term - new kitchen or whatever - then this should be held in cash as well because the investments should be a 5-10+ year thing in order to get a reasonable return.

They cover all areas of your finances and look at the full picture. Its not like the so called investment geniuses you see that are busy making a lot of noise and selling their conferences to explain how you can become like them.

JulianPH said:

rsbmw said:

My opinion is that the service sounds pretty good, and reasonably priced, especially if you don't have the appetite or aptitude for doing it yourself. It does essentially sound like robo investment, with a few other products bundled into an online portal and a guy to walk you through setting it all up / occasional reviews. Frankly this is probably a good fit for the majority.

On reflection, after my rather in depth comment above, I would agree with you 100%. You could easily end up paying the same amount doing it yourself with Hargreaves Lansdown (0.45% platform charge, fund costs and their SIPP fees for any pension element) and having to do it all yourself. This does seem to be very good value.I've also read other comments now and can see that this was a pre-meeting chat and all the stuff I was concerned with should be covered at the fact finding hearing.

I have had a go at picking stocks and shares myself and discovered I am no expert so happy for someone else who should be a bit more knowledgeable to have a go instead. Plus they should know how to limit the tax exposure on top.

He also said that because it is a third party picking and choosing the funds then there is no emotional aspect involved - holding on to something when it tanks because you think you may recover your money in the future.

Whilst they were a small company, they are part of a larger network of advisors who all use the same platform so the fund charges are institutional rates compared to doing it yourself which allows them to compete with the online options.

Edited by KTF on Tuesday 13th September 10:10

Ozzie Osmond said:

Simpo Two said:

So you're paying on two levels - the 'company'/platform and the IFA. Who has discretion to adjust the portfolio? Why pay both of them? I have learned the hard way, twice, that 'daily monitoring' sounds great but means nothing of the sort. It means 'I'll surf the net/get some new clients while the 1.63%s roll in'.

If the dog is not going to do anything, don't pay him - do nothing yourself and save the money!

Just to repeat - this is the aspect you need to watch out for.If the dog is not going to do anything, don't pay him - do nothing yourself and save the money!

Also, the financial services sector is notorious for "friends" selling stuff to their mates. There's a risk you'll then be reluctant to be critical or to change anything because of the friendship - and he can go on pocketing a nice slice of pie for very little activity/value. Sometimes it's best to keep friends separate from your business.

I approached him rather than he approached me. There was no hard sell, just an explanation of what is involved. As I had no idea about the fees being offered, I came here for some advice and it seems that they are within the expected ballpark and they are not trying to pull a fast one.

rsbmw said:

I think following your meeting and some of the thoughts on the thread you seem pretty well informed. The decision is whether you're happy to pay a bit of a premium for a platform and someone else doing the legwork, or whether you would be happy doing more of this yourself to save (or make more) money. My personal opinion is that a platform fee from the likes of this, fiveraday etc can be worth its weight in gold for the actively managed portfolio, where the alternative is randomly picking funds from a list (which is what I would do!). The IFA portion, probably not so much but could work out to be great value for someone who is simply not confident with this stuff.

If I were to do it myself I would fill in the questionnaire on (for example) fiveraday, see what it comes up with then set it going with a month feed from a cash account. Whether this would be the best option or not (out of both the platforms available and the funds available on the platform) I don't know which is where (I hope) the IFA would come in to fine tune the options. I realise there is a premium for this service but it is not that much more than the robo options charge when I compare the fees online.

The sorting out the pension(s) aspect would be stage 2 as that isn't something I am going to fiddle with without speaking to an advisor first.

I think from the various comments here, what I am being offered is 'fair' value.

I agree with the comments that it will be cheaper to use a robo option as I would just be converting cash to S&S at this point but (for a small sum in the grand scheme of things) it may be worth having an IFA on hand if you need advice on other matters or want to look at other options, etc.

If it was a mortgage then that would be different as its a one off thing on an infrequent basis.

I agree with the comments that it will be cheaper to use a robo option as I would just be converting cash to S&S at this point but (for a small sum in the grand scheme of things) it may be worth having an IFA on hand if you need advice on other matters or want to look at other options, etc.

JulianPH said:

If the OP wants I can make an introduction - but I obviously have to declare here that I have a connection. It might be an idea to see a different approach (my adviser operates over the phone and internet, rather than does house visits), but I think what he is being offered is good value and he may prefer a 'face-to-face' adviser.

Assuming they all use a similar platform and will offer the same products then it comes down to the difference in fees. I think for the time being I would prefer to go with someone I 'know' rather than someone in another part of the country.If it was a mortgage then that would be different as its a one off thing on an infrequent basis.

I feel a spreadsheet coming on to work this all out but at a high level I see it like this (feel free to correct any errors).

Aim: Move from cash into tax efficient stocks and shares wrapper instead. As a layman I assume this would then be limited to my annual ISA allowance each year. I have already used this years ISA allowance in a cash ISA so there is a charge for transferring that over to the S&S platform.

So, laying out the two options I see at the moment:

Option 1 (IFA)

Setup cost = £500

180 day interest penalty for moving this years ISA allowance (£15,240) = X

Annual charge of 1.63%/365 x number of days between setup and the next tax year.

Option 2 (fiveraday for example)

180 day interest penalty for moving this years ISA allowance (£15,240) = X

Annual charge of 0.8/365 x number of days between setup and the next tax year.

So for 'year 1' going for option 2 makes you +£500 & 0.83% up on option 1 assuming they are invested in similar portfolios that return similar results.

So, from a financial point of view, unless the IFA can do something recover that 'loss' in 7 months it doesn't sense to go with that option (I realise the figures involved are low but still).

For year 2, option 1 would also have grow by more than 0.83% (maybe more if the loss from year 1 is not recovered yet) before it again started to make sense.

Also for year 1, the deposit would be a lump sum rather than drip fed which increases the exposure to the market tanking the day after its invested (unlikely as that may be).

Now maybe the IFA would have more ideas on what could be done compared to me opening an account with fiveraday and putting it in the suggested portfolio or maybe the product they sell is essentially the same so there would be no big difference between the results you get out?

Aim: Move from cash into tax efficient stocks and shares wrapper instead. As a layman I assume this would then be limited to my annual ISA allowance each year. I have already used this years ISA allowance in a cash ISA so there is a charge for transferring that over to the S&S platform.

So, laying out the two options I see at the moment:

Option 1 (IFA)

Setup cost = £500

180 day interest penalty for moving this years ISA allowance (£15,240) = X

Annual charge of 1.63%/365 x number of days between setup and the next tax year.

Option 2 (fiveraday for example)

180 day interest penalty for moving this years ISA allowance (£15,240) = X

Annual charge of 0.8/365 x number of days between setup and the next tax year.

So for 'year 1' going for option 2 makes you +£500 & 0.83% up on option 1 assuming they are invested in similar portfolios that return similar results.

So, from a financial point of view, unless the IFA can do something recover that 'loss' in 7 months it doesn't sense to go with that option (I realise the figures involved are low but still).

For year 2, option 1 would also have grow by more than 0.83% (maybe more if the loss from year 1 is not recovered yet) before it again started to make sense.

Also for year 1, the deposit would be a lump sum rather than drip fed which increases the exposure to the market tanking the day after its invested (unlikely as that may be).

Now maybe the IFA would have more ideas on what could be done compared to me opening an account with fiveraday and putting it in the suggested portfolio or maybe the product they sell is essentially the same so there would be no big difference between the results you get out?

Ginge R said:

Is the penalty worth moving? If you don't have a good buffer fund for when the roof falls off, why not consider leaving it where it is and start afresh? Cheapest isn't always best, but you really have to justify expense, and more importantly, needless expense.

This was another thought as I could just do nothing until nearer April and get it all set up to start drip feeding in from the start of the tax year.The penalty is 180 days interest on the amount withdrawn (£15240) and the rate is 2.05% so that is around £150 to add to the 'losses' (if my sums are correct). Not a large number but a number all the same. There would then be the lost interest on the remaining balance to factor in for the rest of the term (the remainder would mature March 2018).

rsbmw said:

I don't think you'll see a huge difference between platforms in terms of returns, for the reasons Ginge mentions above. If it's purely S&S ISA, Nucleus makes less sense as you're paying for but not using the rest of the product/service. If you start getting your pensions involved, then the IFA and the rest of Nucleus makes more sense.

To cut costs further you could even look at tracker funds purchased through the lowest cost broker you can find. Splitting across several well established ones should see you suitably diversified and reasonable returns. This is the type of thing that would be worth that one-off fee to the IFA though.

On the pensions side of things I was more interested in seeing if it was worth combining them and/or moving the current amounts to difference portfolios within the existing plans, etc. This is the area that I have least knowledge about and see it as a separate piece of work. I have no idea what benefit (if any) there would be in bringing them in under the Nucleus umbrella.To cut costs further you could even look at tracker funds purchased through the lowest cost broker you can find. Splitting across several well established ones should see you suitably diversified and reasonable returns. This is the type of thing that would be worth that one-off fee to the IFA though.

Yes, you could reduce costs a bit further by picking the trackers yourself (or via the IFA) but then that would need an element of active management compared to going for the robo option that manages it on your behalf? Also my track record of picking trackers and shares myself is less than brilliant

It is a guaranteed 2% on the whole amount in the account but you lose 180 days of 2% interest on the amount withdrawn. The remainder still gets 2% so the interest gained overall for the year will be less than 2% but more than 1% due to the remaining balance.

From what I understand, the most tax efficient way would be to use the S&S ISA allowance and as I have already paid on to a cash ISA this year the only option would be to transfer a chunk of that over (hence the penalty).

As the ISA allowance is 15k this year, 20k next year, the transfer of cash to S&S would have to be drip fed in over a number of years (unless someone knows of another way?) so yes, the £500 would be a year 1 loss (amongst other fees, etc) that would have to be recovered before you recover your costs and start showing a profit.

From April next year the payments to the S&S ISA would be from new money as the existing ISA would not need to be touched so yes, starting from April is starting to look like a better option...

From what I understand, the most tax efficient way would be to use the S&S ISA allowance and as I have already paid on to a cash ISA this year the only option would be to transfer a chunk of that over (hence the penalty).

As the ISA allowance is 15k this year, 20k next year, the transfer of cash to S&S would have to be drip fed in over a number of years (unless someone knows of another way?) so yes, the £500 would be a year 1 loss (amongst other fees, etc) that would have to be recovered before you recover your costs and start showing a profit.

From April next year the payments to the S&S ISA would be from new money as the existing ISA would not need to be touched so yes, starting from April is starting to look like a better option...

JulianPH said:

ISA transfers have no effect on the annual allowance. They are already an ISA so not classed as a further contribution. You can transfer whenever you like with no impact on your allowance.

I would do as others suggest and wait until there is no penalty.

I have already paid the full amount into my cash ISA this year, in May, so my allowance is used up until 2017 which is why I would have to do a transfer.I would do as others suggest and wait until there is no penalty.

I agree that it seems wasteful to transfer out and incur the penalty.

Gassing Station | Finance | Top of Page | What's New | My Stuff