Main dealer has written car off

Discussion

TwigtheWonderkid said:

This has got f k all to do with gap insurance. All she wants is the market value today. She doesn't want the price she paid, or the cost of a brand new one. The whole problem is down to the fact that the garage's trade insurance only settles on trade value for cars in the care, custody or control of the garage, and she isn't in the trade. The garage don't seem to have twigged that they are responsible to bridge this shortfall, either by buying her a replacement car thru the trade (in which case there is no shortfall), or adding in money to bring her money up from trade price to market value.

k all to do with gap insurance. All she wants is the market value today. She doesn't want the price she paid, or the cost of a brand new one. The whole problem is down to the fact that the garage's trade insurance only settles on trade value for cars in the care, custody or control of the garage, and she isn't in the trade. The garage don't seem to have twigged that they are responsible to bridge this shortfall, either by buying her a replacement car thru the trade (in which case there is no shortfall), or adding in money to bring her money up from trade price to market value.

The OP mentioned GAP and you know full well the point of GAP - so if there's an insurance claim, why shouldn't GAP work?k all to do with gap insurance. All she wants is the market value today. She doesn't want the price she paid, or the cost of a brand new one. The whole problem is down to the fact that the garage's trade insurance only settles on trade value for cars in the care, custody or control of the garage, and she isn't in the trade. The garage don't seem to have twigged that they are responsible to bridge this shortfall, either by buying her a replacement car thru the trade (in which case there is no shortfall), or adding in money to bring her money up from trade price to market value. I don't get why the dealers solicitor, rather than their insurer, is dealing with this - unless their cover is 3rd party only. In which case it's down to the dealer to sort out. It seems incredible to me that if they're a dealer for that make of car, and they've got one the same, they wouldn't just replace it. I worked in a dealer that dropped a car off a 2 post lift - we gave the owner a new one.

Hi thanks for replies everyone.

I’m still trying to confirm all of the details. Sister

is very upset by it all and has shocked how the ‘solicitor’ spoke to her.

I might be putting 2 and 2 together and getting 5. So not pretending I fully understand. Here is what I suspect has happened.

Main dealer crash car

Main dealer have done a report on repair and concluded repair makes it a right off

Legal firm have decided £12k is reasonable compensation for car

Legal firm not interested in negotiating and got shirty and unpleasant when she phoned to discuss the below

Legal firm are aware of gap insurance and have decided they will make up the difference

‘Solicitor’ before hanging up and refusing to take any calls apparently said ‘you’re no worse off, claim on your own gap insurance it’s what it’s for’

Not sure if this will be deleted

I’m still trying to confirm all of the details. Sister

is very upset by it all and has shocked how the ‘solicitor’ spoke to her.

I might be putting 2 and 2 together and getting 5. So not pretending I fully understand. Here is what I suspect has happened.

Main dealer crash car

Main dealer have done a report on repair and concluded repair makes it a right off

Legal firm have decided £12k is reasonable compensation for car

Legal firm not interested in negotiating and got shirty and unpleasant when she phoned to discuss the below

Legal firm are aware of gap insurance and have decided they will make up the difference

‘Solicitor’ before hanging up and refusing to take any calls apparently said ‘you’re no worse off, claim on your own gap insurance it’s what it’s for’

Not sure if this will be deleted

Edited by Flumpo on Tuesday 17th March 22:46

Edited by Flumpo on Tuesday 17th March 22:48

Edited by Flumpo on Tuesday 17th March 23:04

IANAL but I'd be sending a letter (on the basis of TTW's script) to the Dealer stating I want a replacement vehicle so that I'm returned to the position I was in before their 'service' by Royal Mail 'signed for', and await their response. Then a following letter again by 'signed for' telling them if they don't settle in 14 days there will be court action. I'd be tempted to hang on to the car - what can they do? report it stolen? unfortunately, plod would possibly support them and say the issue with OP's car is a 'civil one' i wouldn't correspond with the insurance co or the solicitor, but IANAL.

How about asking the dealer under foi request full details of the accident, who was driving etc.

Then tell dealer principle you will be going after both the dealership and the driver for any other losses incurred.

It may just make them take notice if the person crashing the car was important enough.

I agree the gap insurance is irrelevant at this stage unless the dealer has such insurance and can claim on that.

If they know she has gap insurance as they sold it to her, rather than her telling them about it, have they breached dpr regs? How do they know she’s not cancelled it after buying it?

Whatever, she should end up with a like for Like car. If she gets 12k from insurance and adds 3k to it to get same spec car, then sue the dealer and or driver for the 3k.

She could even buy it from same dealer then sue them for the 3k. Would be ironic.

Then tell dealer principle you will be going after both the dealership and the driver for any other losses incurred.

It may just make them take notice if the person crashing the car was important enough.

I agree the gap insurance is irrelevant at this stage unless the dealer has such insurance and can claim on that.

If they know she has gap insurance as they sold it to her, rather than her telling them about it, have they breached dpr regs? How do they know she’s not cancelled it after buying it?

Whatever, she should end up with a like for Like car. If she gets 12k from insurance and adds 3k to it to get same spec car, then sue the dealer and or driver for the 3k.

She could even buy it from same dealer then sue them for the 3k. Would be ironic.

FOI only applies to public bodies.

It’s all very well threatening legal action etc and that’s fine if you’ve got a spare car and don’t need the money - likely the OP’s sister just needs it sorting.

OP hasn’t answered on GAP, but if she does have a GAP policy you’re supposed to tell them immediately the car is written off. I presume they kick the arse of whoever is paying out in order to minimise their own payment.

The dealer may be low-balling as they think GAP will pick up the difference (which is apparently what they’ve said). It occurs to me the dealer might be dropping into ‘oh, you didn’t buy GAP like we told you to?” mode though.

It’s all very well threatening legal action etc and that’s fine if you’ve got a spare car and don’t need the money - likely the OP’s sister just needs it sorting.

OP hasn’t answered on GAP, but if she does have a GAP policy you’re supposed to tell them immediately the car is written off. I presume they kick the arse of whoever is paying out in order to minimise their own payment.

The dealer may be low-balling as they think GAP will pick up the difference (which is apparently what they’ve said). It occurs to me the dealer might be dropping into ‘oh, you didn’t buy GAP like we told you to?” mode though.

Sheepshanks said:

The OP mentioned GAP and you know full well the point of GAP - so if there's an insurance claim, why shouldn't GAP work?

I don't get why the dealers solicitor, rather than their insurer, is dealing with this - unless their cover is 3rd party only. In which case it's down to the dealer to sort out. It seems incredible to me that if they're a dealer for that make of car, and they've got one the same, they wouldn't just replace it. I worked in a dealer that dropped a car off a 2 post lift - we gave the owner a new one.

Many GAP policies are subject to them paying the difference between the genuine market value. If the "Insurers" settle the write off value at below what they reasonably deem to be the genuine market value they will generally only pay the difference between the market value and not make up the difference of it being undervalued.I don't get why the dealers solicitor, rather than their insurer, is dealing with this - unless their cover is 3rd party only. In which case it's down to the dealer to sort out. It seems incredible to me that if they're a dealer for that make of car, and they've got one the same, they wouldn't just replace it. I worked in a dealer that dropped a car off a 2 post lift - we gave the owner a new one.

Many GAP policies will give advice on the market value and settling the claim, so contacting the GAP Insurer would be sensible

Miserablegit said:

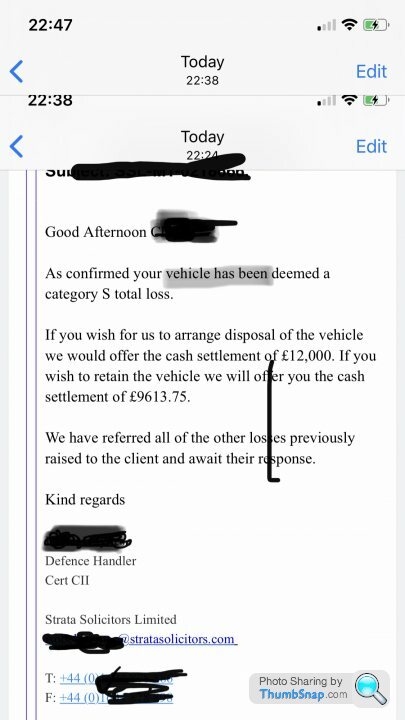

Looking at their website it seems there is only one qualified solicitor there and the rest are claims handlers from the insurance industry. This is reinforced by the letter that was posted earlier.

It is likely they have been engaged by the dealership’s insurers.

It looks to me as though they're being employed by the dealer as they appear to offer their services to in effect businesses who are self Insuring. It is likely they have been engaged by the dealership’s insurers.

A motor trade Insurer would generally use their in house claims staff to handle a claim as it's cheaper for them and they already have the relevant experience. This is not a complicated claim for an Insurer to deal with

http://www.stratasolicitors.com/motorclaims.php

My father in law used to be a dealer principal at a main dealer 20 years ago, I remember him saying their excess was £10k and they’d rarely ever claim on insurance and there were always knocks, bumps, scrapes, thefts etc as you’d imagine when you’ve a crowded car park, test drives, lots of staff etc. theyd just deal with - insurance was fir a really bad day (he’s passed away now so I can’t confirm the details exactly).. I imagine the excess would now be higher. I’m a little surprised therefore this is actually an insurance claim and not just the dealer getting their lawyers to deal with it as cheaply as possible on their behalf.

Not sure it adds much to the debate but if the dealer is effectively paying the bill, and if they’ve a car you’d accept, it may well be worth a conversation with the dealer. Go in being reasonable, with a ‘st happens, employees.. sigh.. , let’s just get this sorted, neither of us want this dragging on’ attitude, you might get a more receptive audience.

Not sure it adds much to the debate but if the dealer is effectively paying the bill, and if they’ve a car you’d accept, it may well be worth a conversation with the dealer. Go in being reasonable, with a ‘s

t happens, employees.. sigh.. , let’s just get this sorted, neither of us want this dragging on’ attitude, you might get a more receptive audience. Graveworm said:

Anyone who has an accident or damages a car would put things in the hands of their insurers. They would say pass all correspondence via us. The beef is with the insurer. If they won't move then it's time for ombudsman or court.

Is that true ?The business was engaged to provide a service and has failed to return the vehicle back.

They are insured to cover their loss, but the OP's 'contract' is with the company who have failed to meet the service expected.

They should use their insurance to cover their loss then make up the difference.

Take them to court to cover your loss.

Piersman2 said:

elanfan said:

Why has the OP not claimed on her own insurance company and leave them to go after the garage?

This, I was wondering the same as I read the thread.

Besides, the sister won't want a claim on her insurance record.

I don’t have any further details from last night but a few quick responses:

Sister has spoken to her insurance, they have categorically said she isn’t covered with them for this. They are not going to get involved. - I will suggest she phoned them again and asks specifically about motor legal insurance.

The gap situation is being made slightly complicated. She has phoned them 3 times but the people she gets through to are ‘computer says no’ types. They are unable to start the claim until they have the insurance details of the driver. Solicitor won’t give out these details and says gdpr. Solicitor now refusing to discuss anything or take calls.

It takes over an hour to get through to the gap people who are only open 9-5. Added to that she works for a company who support working from home software. Unsurprisingly they are incredibly busy at the moment. Her boss isn’t happy about her making hour long phone calls during his busiest period ever.

I will ask if she is in the aa, I doubt it but I would think she has some scheme through Mercedes.

Thanks for replies.

Sister has spoken to her insurance, they have categorically said she isn’t covered with them for this. They are not going to get involved. - I will suggest she phoned them again and asks specifically about motor legal insurance.

The gap situation is being made slightly complicated. She has phoned them 3 times but the people she gets through to are ‘computer says no’ types. They are unable to start the claim until they have the insurance details of the driver. Solicitor won’t give out these details and says gdpr. Solicitor now refusing to discuss anything or take calls.

It takes over an hour to get through to the gap people who are only open 9-5. Added to that she works for a company who support working from home software. Unsurprisingly they are incredibly busy at the moment. Her boss isn’t happy about her making hour long phone calls during his busiest period ever.

I will ask if she is in the aa, I doubt it but I would think she has some scheme through Mercedes.

Thanks for replies.

Gassing Station | Speed, Plod & the Law | Top of Page | What's New | My Stuff