How many years no claims bonus do I say to insurers now?

Discussion

N111BJG said:

I just insured a second motorcycle & they offered to mirror the full NCD on my other bikes policy.

I suppose it might be because I'm old & the only rider of both bikes though.

Try adding your other half to the quote. My quotes were always cheaper with an additional driver (who had had no recent accidents)I suppose it might be because I'm old & the only rider of both bikes though.

sixor8 said:

Where is this 'maximum of 5 years' from?

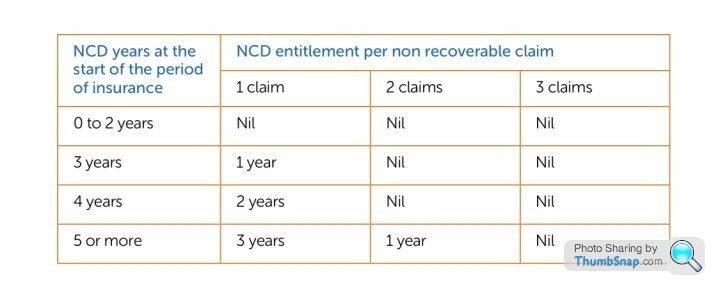

It was traditionally the maximum NCD that you could accrue, and the reason why losing 2 years from your "5 or more years" left you with 3 years.

Nowadays many insurers will credit you with more years, but they still retain the "claim with more than 5 years and you are left with three years" rule.

sixor8 said:

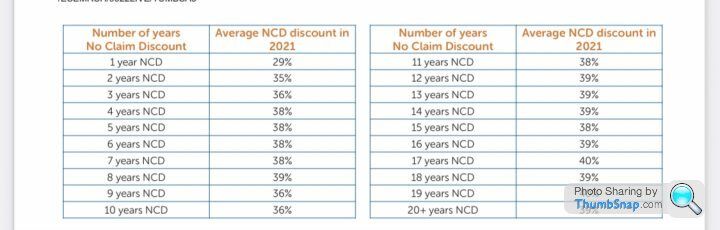

I actually have 17 and I keep policy renewals from other companies to prove it, because many firms only offer up to 9.

You may have pieces of paper to say that you have 17 years, but do you actually get a noticeably cheaper premium than if you had 9 or 5 years? I suspect you'll find that the only real difference having 17 years makes is that you get a slightly warmer, fuzzier glow when you look at your renewal letter, and the figures from Esure above tend to support that.

sixor8 said:

Absolute drivel that you'd have to declare claims from 16 years ago. They only recently increased asking about claims in the last 3 years, many now ask about the last 5.

Of course they only ask about accidents in the last 3-5 years, because they don't give a stuff about your claims history from decades ago, which in turn is why they don't really care whether you have 5, 9 or 20 years NCD. The point was that if you want an alternative reality where insurers do care about decades of driving history "reward you" for your claim free year back when Oasis were in the charts, the inevitable flip side would be that if you'd had an accident as a teenager, your still be getting penalised for it in middle age. Many would regards that as unfair too.

wong said:

N111BJG said:

I just insured a second motorcycle & they offered to mirror the full NCD on my other bikes policy.

I suppose it might be because I'm old & the only rider of both bikes though.

Try adding your other half to the quote. My quotes were always cheaper with an additional driver (who had had no recent accidents)I suppose it might be because I'm old & the only rider of both bikes though.

Pebbles167 said:

Evil.soup said:

Just to add to this, I recently insured a second car using zero no claims and it was effectively still quite cheap to insure. I do wonder how much difference the "discount" actually makes these days.

Bugger all is my opinion, once you're over 30 anyway. I insure different cars all the time, some with my 10 years no claims, others without. Makes next to no difference. Its always under £600 for something quick, and around £250 for something not so. When there is a difference I'm talking £20-40 a year most of the time.

Occasionally I get a car that it seems to make a fair difference on, but for most run of the mill stuff it doesn't.

Maybe I am just getting old!

I would discuss the nature of the claim with the insurers on the phone.

The likelihood of you having a second claim in short order is far lower than, say, someone who has crashed his car into another car, as you weren't driving the trampoline at the time of the accident.

I had a complete write off of a £4,500 car about 12 years ago. The insurers paid out in full, and my premium didn't increase one penny on renewal. The reason was I didn't crash into anyone, I slid into a deep ditch avoiding a 60 mph x 2 head on collision with an oblivious texter coming the other way. My car rolled gently onto its roof in the ditch, but was otherwise fine, until the recovery buffoon decided that it was a smart move to pull the car out of the ditch end over end.

I do wonder if your renewal premium would be lower if you explained the full facts of the claim to a real person, and nicely told them you would have to look elsewhere if they couldn't reduce it.

The likelihood of you having a second claim in short order is far lower than, say, someone who has crashed his car into another car, as you weren't driving the trampoline at the time of the accident.

I had a complete write off of a £4,500 car about 12 years ago. The insurers paid out in full, and my premium didn't increase one penny on renewal. The reason was I didn't crash into anyone, I slid into a deep ditch avoiding a 60 mph x 2 head on collision with an oblivious texter coming the other way. My car rolled gently onto its roof in the ditch, but was otherwise fine, until the recovery buffoon decided that it was a smart move to pull the car out of the ditch end over end.

I do wonder if your renewal premium would be lower if you explained the full facts of the claim to a real person, and nicely told them you would have to look elsewhere if they couldn't reduce it.

QBee said:

I would discuss the nature of the claim with the insurers on the phone.

The likelihood of you having a second claim in short order is far lower than, say, someone who has crashed his car into another car, as you weren't driving the trampoline at the time of the accident.

I had a complete write off of a £4,500 car about 12 years ago. The insurers paid out in full, and my premium didn't increase one penny on renewal. The reason was I didn't crash into anyone, I slid into a deep ditch avoiding a 60 mph x 2 head on collision with an oblivious texter coming the other way. My car rolled gently onto its roof in the ditch, but was otherwise fine, until the recovery buffoon decided that it was a smart move to pull the car out of the ditch end over end.

I do wonder if your renewal premium would be lower if you explained the full facts of the claim to a real person, and nicely told them you would have to look elsewhere if they couldn't reduce it.

Tried this yesterday, esure said that because I have had a claim in the last 5 years then the price is fixed and they aren’t open to the usual haggling, company policy apparently.The likelihood of you having a second claim in short order is far lower than, say, someone who has crashed his car into another car, as you weren't driving the trampoline at the time of the accident.

I had a complete write off of a £4,500 car about 12 years ago. The insurers paid out in full, and my premium didn't increase one penny on renewal. The reason was I didn't crash into anyone, I slid into a deep ditch avoiding a 60 mph x 2 head on collision with an oblivious texter coming the other way. My car rolled gently onto its roof in the ditch, but was otherwise fine, until the recovery buffoon decided that it was a smart move to pull the car out of the ditch end over end.

I do wonder if your renewal premium would be lower if you explained the full facts of the claim to a real person, and nicely told them you would have to look elsewhere if they couldn't reduce it.

It’s still the cheapest quote I have managed to find though and I was generally happy with how they handled the accident which was far better than how Tesco handled the damage to our van (on wife’s insurance) from the same incident.

It was an expensive day!

£150 to replace a few slates on the roof at mates rates

£100 trampoline put in the bin

£500 excess on the van insurance

£200 excess on the car insurance

£170 increase on my own insurance policy

Unknown increase on my wife’s van policy that is due next month. The one good point with her though is that she didn’t have any no claims on the van as it was on her car policy, she now doesn’t have a car so she can use the NCB on the van this time round. Premium will go up though as it was cheap last year.

Edited by ED209 on Tuesday 28th June 08:33

Gassing Station | Speed, Plod & the Law | Top of Page | What's New | My Stuff