Retirement calculator

Discussion

Seems a decent calc to have a play on https://www.guiide.co.uk

Gives about the same result as one that I can use through work pension site.

I could easily retire now (60) but will carry on a few more years. Unless they pay me off, which is a possibility. May as well hang out for a years salary to go !

Don’t mind work now, thanks to the global pandemic. Every cloud.. Was 30 mile each way commute 4 days a week. Been to office twice this year!

Work 8-4, 37 days leave. Can do diy & run every day during that time @ more than twice average salary.

If I have to go in more than twice a week, or get any aggro, i’ll call it a day

I could easily retire now (60) but will carry on a few more years. Unless they pay me off, which is a possibility. May as well hang out for a years salary to go !

Don’t mind work now, thanks to the global pandemic. Every cloud.. Was 30 mile each way commute 4 days a week. Been to office twice this year!

Work 8-4, 37 days leave. Can do diy & run every day during that time @ more than twice average salary.

If I have to go in more than twice a week, or get any aggro, i’ll call it a day

UrbanAchiever said:

Looks good, but I fell at the first hurdle. Told it I want to retire at 53. Nope. Minimum retirement age is 55 for the calculator.

Will run the numbers for 55 but I'm not waiting that long!

Have a play around with https://engaging-data.com/will-money-last-retire-e... treating $ as £ IYSWIM.Will run the numbers for 55 but I'm not waiting that long!

xeny said:

UrbanAchiever said:

Looks good, but I fell at the first hurdle. Told it I want to retire at 53. Nope. Minimum retirement age is 55 for the calculator.

Will run the numbers for 55 but I'm not waiting that long!

Have a play around with https://engaging-data.com/will-money-last-retire-e... treating $ as £ IYSWIM.Will run the numbers for 55 but I'm not waiting that long!

That's a pretty bold statement.

Derek Chevalier said:

"If you look over all these historical cycles, we find that a 4% withdrawal rate will generally last through a long retirement"

That's a pretty bold statement.

The grammar is certainly not ideal and I don't agree about their idea of a long retirement.That's a pretty bold statement.

How about "If we look over these historical cycles, we find that a 4% withdrawal rate generally (96.6% of the time) lasted through a 30 year retirement" , which is my interpretation of the graph on https://engaging-data.com/visualizing-4-rule/ ?

xeny said:

Derek Chevalier said:

"If you look over all these historical cycles, we find that a 4% withdrawal rate will generally last through a long retirement"

That's a pretty bold statement.

The grammar is certainly not ideal and I don't agree about their idea of a long retirement.That's a pretty bold statement.

How about "If we look over these historical cycles, we find that a 4% withdrawal rate generally (96.6% of the time) lasted through a 30 year retirement" , which is my interpretation of the graph on https://engaging-data.com/visualizing-4-rule/ ?

But the bigger issue I have with these models is that they assume the money is invested in a certain way (broadly diversified portfolio) and with perfect investor behaviour.

In the real world, we all have our flaws and very few exhibit this perfect behaviour.

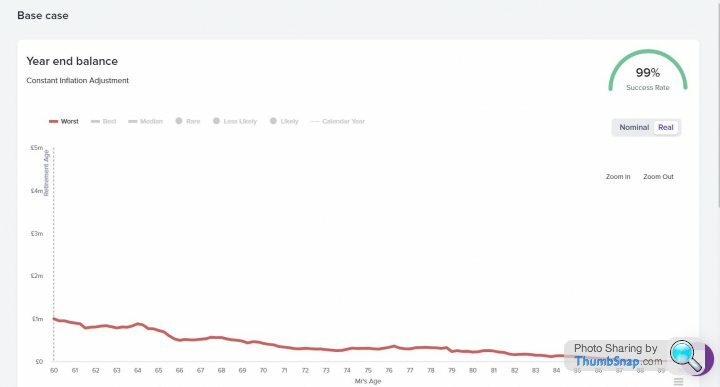

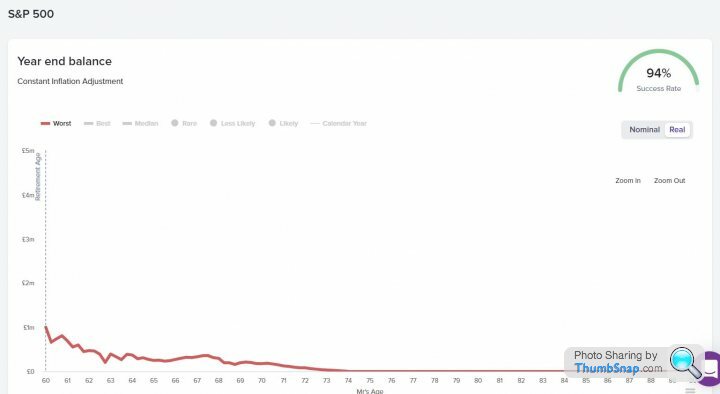

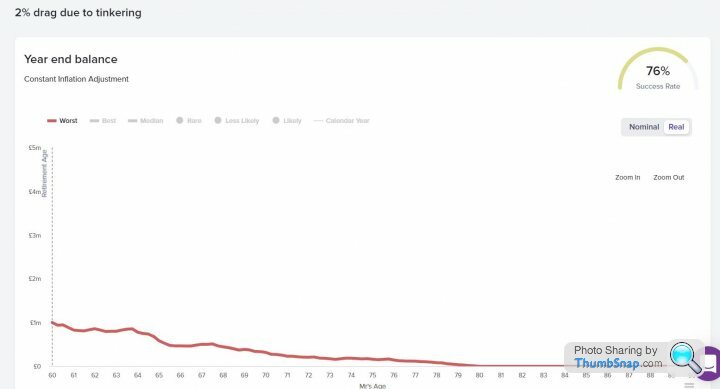

The S&P example shows what has happened with an undiversified portfolio (money gone after ~13 years in the worst case) while #3 shows the impact of investment vs investor returns (2% fees vs 0.3% in base case).

1. Perfect behaviour with a diversified portfolio

2. Perfect behaviour but not diversified (S&P only)

3. Diversified, but buying high and selling low (1.7% pa drag)

Truth be told it is just as terrifying as all the other calculators.

I'm 32 and I've just started getting serious with my pensions nopw I've finished off my student loan, I'd like a comfortable retirement and I'm currently putting in £16k via salary sacrifice (inc company contribution) plus I will add about £6k to my SIPP so a further £10k in tax relief. It looks like at 65 I will be ok but ideally I don't want to be in professional services at 60+ so it looks like I need to work harder and get more out of the tax relief.

Albeit at 60 I'd like to be in good enough health to try something else for 5-10 years or go part-time and spent time with the grand kids if I have any at the time.

Thanks for posting OP. It is really useful to se a pension calculator which includes inflation and aren't on a day-one basis.

I'm 32 and I've just started getting serious with my pensions nopw I've finished off my student loan, I'd like a comfortable retirement and I'm currently putting in £16k via salary sacrifice (inc company contribution) plus I will add about £6k to my SIPP so a further £10k in tax relief. It looks like at 65 I will be ok but ideally I don't want to be in professional services at 60+ so it looks like I need to work harder and get more out of the tax relief.

Albeit at 60 I'd like to be in good enough health to try something else for 5-10 years or go part-time and spent time with the grand kids if I have any at the time.

Thanks for posting OP. It is really useful to se a pension calculator which includes inflation and aren't on a day-one basis.

We are also definitely heading for a crisis with pensions that auto-enrolment is not doing enough to sort out. The average salary of £31,000 PA| has an auto enrolment contribution of approximately £2,500 PA.

People are going to live a very miserable later life or work indefinitely at this rate.

People are going to live a very miserable later life or work indefinitely at this rate.

Brett748 said:

We are also definitely heading for a crisis with pensions that auto-enrolment is not doing enough to sort out. The average salary of £31,000 PA| has an auto enrolment contribution of approximately £2,500 PA.

People are going to live a very miserable later life or work indefinitely at this rate.

I’m assuming that autoenrolment is going to be slowly ratcheted up. If it ends up at say, 6% employer, 6% employee that’s a big improvement on where we are now. People are going to live a very miserable later life or work indefinitely at this rate.

Brett748 said:

We are also definitely heading for a crisis with pensions that auto-enrolment is not doing enough to sort out. The average salary of £31,000 PA| has an auto enrolment contribution of approximately £2,500 PA.

People are going to live a very miserable later life or work indefinitely at this rate.

Many will be left relying on inheritance and help from older relatives People are going to live a very miserable later life or work indefinitely at this rate.

Brett748 said:

Truth be told it is just as terrifying as all the other calculators.

You want to see what mine always look like, massive shortfall forever. The OP's calculator gives me a "Even if you increase your total contribution [by 300% (I'll not share the £)] per month you would be expected to run out of money in retirement". The thrills of not starting planning till 50 (and life getting in the way for the previous 30 years).

beanoir78 said:

The big unknown for me with any of these calculators, or even not using them is how much I would like or need as a pension.

Same here. I just stash money away and hope for the best tbh. One day i'm going to think f k it and pack it all in and see whats what then.

k it and pack it all in and see whats what then.A more useful calculator to me would be where you tell it what you have today, and no further contributions but you can update it as you make contributions (maybe linked to your bank a/c) and then a sliding scale of some meaningful indicator from utterly f

ked, fked, poverty mate, not quite poverty, ok-if-you-don't-live-long, better, bestGassing Station | Finance | Top of Page | What's New | My Stuff