Proprietary Trading

Discussion

La Liga said:

oes a PAMM require any regulation from the trader?

It’s one of the areas of regulation that is open to interpretation as it’s a fair assumption to make from a broker’s perspective that somewhere in amongst the relationship between the trader and the individual will be some form of performance or activity related fee. Most brokers with a Pamm set up will usually allow a trader to have a few copy accounts but beyond that require some form of regulation to be involved. Ie they are happy to accept that most traders may have a few friends or family that would like some funds traded and it’s unlikely there would be any commercial arrangement that would be considered a regulated activity.

Trading for friends and family is really difficult. Your moral obligations can impact negatively on your trading mindset, they won’t ever understand that all traders will have periods of drawdown, they will always be paranoid about you stealing their money somehow and you can never charge fees anywhere high enough for the personal risk that you are taking.

The upside of these structures is that they keep the clients’ money in their own account and this really does cut down the levels of fraud, the most common of which being the trader masking losing open positions and closing only winning trades to fudge a crude performance figure, or over trading positions to generate more flow to hit a better commission tier at the brokerage (Go long 20 contracts and short 10 to obtain a net of long 10 but an additional flow of 20). And of course they give more general protection to the investor.

But, none of this over rides the downsides of trading for people you love and who are part of your life as the odds are heavily stacked that from the moment you start trading their money you are on a countdown to destroying the relationship that you treasure.

La Liga said:

Agreed trading for friends / family.

Thanks for the comprehensive reply via PAMM. Do you know what qualification / authorisation would an individual need to obtain to be on the safe side? The regulatory framework is a minefield!

I guess it would depend on where you were holding your account etc. I.e I’m not clued up on the rules in the US and Brokers there do tend to differ in how they regulated overseas clients anyway. Thanks for the comprehensive reply via PAMM. Do you know what qualification / authorisation would an individual need to obtain to be on the safe side? The regulatory framework is a minefield!

From the UK perspective it would be pretty hard to argue that an individual who is trading third party accounts which have some form of fee structure, ie a clear business structure as opposed to the POA route which is really just permissible for trading one’s wife’s account for CGT advantage but can be stretched a bit within the guidelines to be a general interpretation of ‘no more than 5 clear friends and/or family and no overt fees in evidence’ should not require regulation.

This means that the individual must create a recognised corporate wrapper under which they would be engaged. That wrapper needs to be regulated by the FCA and the relevant individuals must also be registered (ie have the appropriate exams etc).

Until recently a little fudge that many of us used was to set such structures up as Appointed Representatives or ARs. These were a cool little legacy of the SFA being merged in with the PIA(?) where the PIA had this AR structure to cover the practice of commissioned, independent, door to door financial product vending. Ie The Man From The Pru.

We used it to set similar structures for individual brokers or tiny firms as it was the only cost effective way for a small operation to function. Full regulation has always been costly.

The SFA’s view on the AR route was that it was permissible to use as a means to incubate a new firm but they wanted to see that firm grow and progress to a full application within a suitable time frame. Obviously many brokers abused this and today many of the umbrella firms have been shut down and the whole practice pretty much closed off.

This means full regulation really. And arguably a discretionary license. I think that means about £250k on the balance sheet and obviously more exams for the individuals.

This is why we use copy trading under a discretionary license to facilitate this business now. It has the upside that an individual can focus 100% on the trading and not any time on the regulation nor do they need any large capital investment. In addition, if they run a good account then we find the clients for them.

The downsides are that for certain types of trading (heavy scalping or sniping) it doesn’t really work as the spreads are wider to cover the increased costs of hedging, management, regulation and client acquisition. And as it displays a graphical representation of performance then it discourages around 95% of the people who want to trade client funds as they know they can’t get positive performance and their model lies in hiding that with blarney and trade masking to milk the punter for fees and comm for as long as possible.

As you can imagine, finding that 5% is somewhat difficult but overall the system works well. The majority of clients recognise that the typical good trader will only have a limited period of above market performance and will always have draw-down periods and so they move between traders continually reallocating and traders learn that draw-down episodes are part of the game of trading and absolutely normal. Plus, they learn that sometimes the market evolves into a cycle that they just can’t trade and so you step away or drop the activity and size substantially and keep that account protected while maybe setting up a second one to test new trade styles in the evolved market.

And of course, there’s no avoiding the s

t or bust traders who shoot for the moon. But even those can be scalped and copiers can grab a slice of the action while they are on a roll and then run for the hills before they implode. Which they always do.

t or bust traders who shoot for the moon. But even those can be scalped and copiers can grab a slice of the action while they are on a roll and then run for the hills before they implode. Which they always do. Interesting.

From my less knowledgeable point of view there doesn't appear to be a huge practical amount of difference between a PAMM and copy trading given the wide gap in what an individual's regulation is required to be. I did read somewhere that automated strategies (EAs etc) didn't require any regulation but that doesn't sound correct.

- Followers have their own account and control their own money.

- Followers choose to link their accounts with the primary trader's.

- The primary trader makes money the more people who link to / follow him.

I guess it depends on the pay structure i.e. is the primary trader being compensated with a share of the spread and makes more money the more they trade, or if are they receiving a % of 'AUM' like eToro.

I've tried eToro and looked at others, but as you point out they're not suitable for short-term 'scalpy' stuff. My average trade is about 9 minutes long so anything other than rapid executions (as opposed eToro's slippage) and tight spreads ruins my edge.

From my less knowledgeable point of view there doesn't appear to be a huge practical amount of difference between a PAMM and copy trading given the wide gap in what an individual's regulation is required to be. I did read somewhere that automated strategies (EAs etc) didn't require any regulation but that doesn't sound correct.

- Followers have their own account and control their own money.

- Followers choose to link their accounts with the primary trader's.

- The primary trader makes money the more people who link to / follow him.

I guess it depends on the pay structure i.e. is the primary trader being compensated with a share of the spread and makes more money the more they trade, or if are they receiving a % of 'AUM' like eToro.

I've tried eToro and looked at others, but as you point out they're not suitable for short-term 'scalpy' stuff. My average trade is about 9 minutes long so anything other than rapid executions (as opposed eToro's slippage) and tight spreads ruins my edge.

Crudely speaking, if you just want to trade a few accounts via a single execution point and are not charging those account holders anything for your activity then Pamm is better than copy trading. It’s cheaper and the execution is either DMA or an OTC that tracks DMA better due to being more A book than B. That said you still need to choose the broker carefully to ensure this is the case and that you will get that benefit. If you want to charge anything or run more than a few accounts the. Without the right regulation for Pamm, copy trading becaomes the only solution until you reach the point when you have enough under management to be able to cover the costs of regulation and still benefit from the lower execution costs of a Pamm structure. Or go and work at a house.

There has been a general review by the FCA re copy trading and it really needs to be done under a discretionary license going forward. EAs are arguably at the bottom end of the market place. They are easy to falsify and tend to target the smallest traders who have a tendency to believe that back testing is good indicator of future performance or that performance generated on a demo account will mean performance on a live account.

Scalping is always an issue and most OTC brokers use spreads to discourage such traders. 9 minutes is actually ok but there is a little quirk to OTC market making on the retail side that means if you allow the execution of very short term trades you also bring in the traders who know what this quirk is and how to spank it. And there is an army of them looking around for a niaive firm.

In addition, with copy trading you need the hedge more as one tiny trade is multiplied many times over so spikes your exposure. And you need enough time and spread to get the right hedging in place without locking in losses. An interesting aspect of copy trading is that you’d think that with all the extra volume you’d get a really good flow of long and short activity that would self hedge but it doesn’t work out that way. In reality what you see is pretty much all your copy accounts doing much the same long or short activity.

An extreme example being Bitcoin where everyone is just long and sitting. It’s horrible business. First of all you have to hedge it all but then the more you’re hedged the more your client default risk climbs (ie total wipe out in a pull back where the underlying travels well below your clients’ wipe-out point leaving you with the loss). Second, with cryptos, your risk of default at your ‘clearer’ is huge as these clearers are junk. You need wide spreads to be able to get your hedges away and wide spreads to cover the fact that there is potentially no liquidity when you come to unwind the hedge so have to pay more to find it. And then because traders are sitting on positions you’re taking all this risk and not generating any revenue.

If we could lay off scalpers with total efficiency it would be phenomenal business to have but due to the nature of retail OTCs we need to steer the most aggressive scalpers away. Which is a great shame.

There has been a general review by the FCA re copy trading and it really needs to be done under a discretionary license going forward. EAs are arguably at the bottom end of the market place. They are easy to falsify and tend to target the smallest traders who have a tendency to believe that back testing is good indicator of future performance or that performance generated on a demo account will mean performance on a live account.

Scalping is always an issue and most OTC brokers use spreads to discourage such traders. 9 minutes is actually ok but there is a little quirk to OTC market making on the retail side that means if you allow the execution of very short term trades you also bring in the traders who know what this quirk is and how to spank it. And there is an army of them looking around for a niaive firm.

In addition, with copy trading you need the hedge more as one tiny trade is multiplied many times over so spikes your exposure. And you need enough time and spread to get the right hedging in place without locking in losses. An interesting aspect of copy trading is that you’d think that with all the extra volume you’d get a really good flow of long and short activity that would self hedge but it doesn’t work out that way. In reality what you see is pretty much all your copy accounts doing much the same long or short activity.

An extreme example being Bitcoin where everyone is just long and sitting. It’s horrible business. First of all you have to hedge it all but then the more you’re hedged the more your client default risk climbs (ie total wipe out in a pull back where the underlying travels well below your clients’ wipe-out point leaving you with the loss). Second, with cryptos, your risk of default at your ‘clearer’ is huge as these clearers are junk. You need wide spreads to be able to get your hedges away and wide spreads to cover the fact that there is potentially no liquidity when you come to unwind the hedge so have to pay more to find it. And then because traders are sitting on positions you’re taking all this risk and not generating any revenue.

If we could lay off scalpers with total efficiency it would be phenomenal business to have but due to the nature of retail OTCs we need to steer the most aggressive scalpers away. Which is a great shame.

From a personal point of view the model of making additional income through simply trading my own account is attractive. Unfortunately, my current trading style is, and always has been, very short-term, so is subject to spreads / executions. For example, eToro has a 5 point spread on the DJIA, which is my most heavily traded market. I couldn't work with that. I need to really add longer-term to my skill set. Although I've been saying that for years.

The problem with copying, as you've mentioned, is a lot of the copiers have no idea about investment / realistic returns. Someone making 300% in a year on BTC is thought of as a god rather than someone doing 50% per year with much lower risk. When you have such of large pool of people trying to trade, it's inevitable a few will produce atypical returns over the short term.

I find the hedging side interesting. There are firms out there who claim to hedge all volume (Spreadbet / CFD). I don't know much about the back-end but I can't see how they can possibly do that. It sounds similar to firms who claim to only make money out of the spreads rather than net client losses. I've also thought about the hedging side of BTC from your end. How would a firm do it with 95%> of people have been long? Buy the actual coins? I know there are BTC Futures but what about the other coins?

Sounds a nightmare.

The problem with copying, as you've mentioned, is a lot of the copiers have no idea about investment / realistic returns. Someone making 300% in a year on BTC is thought of as a god rather than someone doing 50% per year with much lower risk. When you have such of large pool of people trying to trade, it's inevitable a few will produce atypical returns over the short term.

I find the hedging side interesting. There are firms out there who claim to hedge all volume (Spreadbet / CFD). I don't know much about the back-end but I can't see how they can possibly do that. It sounds similar to firms who claim to only make money out of the spreads rather than net client losses. I've also thought about the hedging side of BTC from your end. How would a firm do it with 95%> of people have been long? Buy the actual coins? I know there are BTC Futures but what about the other coins?

Sounds a nightmare.

Yup. You’ll give away a fair amount of performance in spread. I’m 3 points on the Dow. I’m actually a bit surprised at 5, to me that’s too much even for non scalpers.

What we find with copiers is that most arrive and pick the glamour traders who have big charts but when you look at how they are trading you can guarantee a wipe out event. After the client has learnt that the big performers always have big collapses they then look at the same traders who are plodding away with anything from 5-20% annual returns (you can gear up their trades to amplify performance so some traders trade in very small size with next to no leverage to let the follower decide how much risk to run). We always have a shortage of good traders.

Any firm who says they hedge 100% is generally talking bks. The likes of LMAX are few and far between. It’s all about running some risk on the flow. Besides, no firm has the balance sheet to hedge everything and you need to consider that your hedging costs are actually sometimes higher than the retail charges (due to spread competition from brokers who don’t hedge at all) and it’s all too common for clearers to raise margins on a broker who then can’t pass that on to the clients, so if you’re 100% hedged then you’d be screwed. The profits aren’t as big as people think though. Even IG’s L2 execution uses volume from the book ahead of DMA execution. Typically, in very Crude terms, you make about a £1 on the book for every £1 you make on spread and if you weren’t making that book revenue then given the cost of client acquisition in the UK and the small size of the average client then you wouldn’t be profitable.

There was a very interesting and well written article on crypto hedging the other day: https://www.leaprate.com/experts/alex-nekritin/man...

What we find with copiers is that most arrive and pick the glamour traders who have big charts but when you look at how they are trading you can guarantee a wipe out event. After the client has learnt that the big performers always have big collapses they then look at the same traders who are plodding away with anything from 5-20% annual returns (you can gear up their trades to amplify performance so some traders trade in very small size with next to no leverage to let the follower decide how much risk to run). We always have a shortage of good traders.

Any firm who says they hedge 100% is generally talking b

ks. The likes of LMAX are few and far between. It’s all about running some risk on the flow. Besides, no firm has the balance sheet to hedge everything and you need to consider that your hedging costs are actually sometimes higher than the retail charges (due to spread competition from brokers who don’t hedge at all) and it’s all too common for clearers to raise margins on a broker who then can’t pass that on to the clients, so if you’re 100% hedged then you’d be screwed. The profits aren’t as big as people think though. Even IG’s L2 execution uses volume from the book ahead of DMA execution. Typically, in very Crude terms, you make about a £1 on the book for every £1 you make on spread and if you weren’t making that book revenue then given the cost of client acquisition in the UK and the small size of the average client then you wouldn’t be profitable. There was a very interesting and well written article on crypto hedging the other day: https://www.leaprate.com/experts/alex-nekritin/man...

Thanks, that article is interesting.

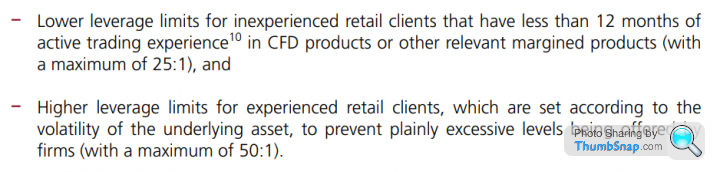

What are your views on the FCA’s proposed leverage caps of 25/1 and 50/1? Is that a starting point (an ‘anchor’) which is likely to rise due to the consultation? IG were very keen to have customers email the FCA. I also note that IG’s share price has pretty much recovered from that FCA proposal drop (albeit there could be a load of factors at play).

I know they’ve put it on pause since the ESMA are looking at similar issues. Why didn’t the FCA (I expect I’ll know your answer) know the ESMA were going to going to cover the same ground?

Is there any end in sight for an implementaton?

What are your views on the FCA’s proposed leverage caps of 25/1 and 50/1? Is that a starting point (an ‘anchor’) which is likely to rise due to the consultation? IG were very keen to have customers email the FCA. I also note that IG’s share price has pretty much recovered from that FCA proposal drop (albeit there could be a load of factors at play).

I know they’ve put it on pause since the ESMA are looking at similar issues. Why didn’t the FCA (I expect I’ll know your answer) know the ESMA were going to going to cover the same ground?

Is there any end in sight for an implementaton?

The FCA are due to publish early summer.

My general view is that if the FCA has done its job then we would never had had firms offering insane levels of leverage that only serve to ensure the average clients wiped out quicker. Couple loony leverage with manipulative bonuses that push the more niaive into massively over trading and it was great days for the pure B book churn and burn brokers.

IG’s reaction was slightly odd at the time. The FCA has been caught napping by the Govt and rushed out a response before getting it approved by IG. . They subsequently went around trying to hire a few burnt out punters in the hopes of finding some people who knew what a CFD was while apparently being requested by the powers that Be not to rush into any changes that would cost British jobs.

. They subsequently went around trying to hire a few burnt out punters in the hopes of finding some people who knew what a CFD was while apparently being requested by the powers that Be not to rush into any changes that would cost British jobs.

Bonus offers should be compliant to TCF, as should leverage. Both aspects have been willfully ignored by the regulator for years despite numerous protestations from the brokers. The risk they now face is that the retail consumer is no longer confined in any way by geographical borders so if they over tighten margins on UK firms the most vulnerable clients will simply open accounts offshore where the brokers will offer them silly margins and bonuses all day long. So the FCA has to weigh up this new dynamic, if they are aware of it as it’s only been being pointed out to them for about ten years now.

The simple reality is that it’s already not really worth onboarding small clients any more as the cost of acquiring them plus the cost of maintaining them outweighs any profit they make so the smaller client is already well incentivised to send their money outside of the UK.

The harsh reality is that both the industry and the regulator need to recognise that a significant proportion of clients do not view the product as an investment tool but as a gaming tool and that everyone needs to mentally adapt to this somewhat significant change.

My general view is that if the FCA has done its job then we would never had had firms offering insane levels of leverage that only serve to ensure the average clients wiped out quicker. Couple loony leverage with manipulative bonuses that push the more niaive into massively over trading and it was great days for the pure B book churn and burn brokers.

IG’s reaction was slightly odd at the time. The FCA has been caught napping by the Govt and rushed out a response before getting it approved by IG.

. They subsequently went around trying to hire a few burnt out punters in the hopes of finding some people who knew what a CFD was while apparently being requested by the powers that Be not to rush into any changes that would cost British jobs. Bonus offers should be compliant to TCF, as should leverage. Both aspects have been willfully ignored by the regulator for years despite numerous protestations from the brokers. The risk they now face is that the retail consumer is no longer confined in any way by geographical borders so if they over tighten margins on UK firms the most vulnerable clients will simply open accounts offshore where the brokers will offer them silly margins and bonuses all day long. So the FCA has to weigh up this new dynamic, if they are aware of it as it’s only been being pointed out to them for about ten years now.

The simple reality is that it’s already not really worth onboarding small clients any more as the cost of acquiring them plus the cost of maintaining them outweighs any profit they make so the smaller client is already well incentivised to send their money outside of the UK.

The harsh reality is that both the industry and the regulator need to recognise that a significant proportion of clients do not view the product as an investment tool but as a gaming tool and that everyone needs to mentally adapt to this somewhat significant change.

DonkeyApple said:

IG’s reaction was slightly odd at the time. The FCA has been caught napping by the Govt and rushed out a response before getting it approved by IG. . They subsequently went around trying to hire a few burnt out punters in the hopes of finding some people who knew what a CFD was while apparently being requested by the powers that Be not to rush into any changes that would cost British jobs.

Coincidentally, IG have just sent another email inviting people to email the ESMA. . They subsequently went around trying to hire a few burnt out punters in the hopes of finding some people who knew what a CFD was while apparently being requested by the powers that Be not to rush into any changes that would cost British jobs.Doing it solely on £PP seems quite crude to me i.e. £20 PP with a 20 point stop vs £10 PP with a 40 point stop have dramatically different margain requirements even through the risk is the same. I appreciate the higher risk with higher leverage / tighter stops, but it seems disproportional.

Do you think they're doing the old anchoring trick i.e. starting deliberately low and then willing to move up during the 'consultation'?

I guess it’s the age old issue of few clients being able to relate £/p back to nominal value easily.

The ESMA rates are very low and you don’t need them that lownin order to protect the client. The industry worked for over 30 years on a pretty uniform set of industry margins that protected client and broker and these margins were essentially the margins that the clearers were offering for hedging. It’s only in the last decade with the meteoric rise of the pure bookmaker which was run as a marketing enterprise that they broke away from the historic margins (funnily enough there is a very good argument that this happened as a direct result of the regulators stopping brokers from being able to use client money as margin for that client’s trade at the clearers!!! Suddenly most firms couldn’t hedge even if they wanted to and so the rise of the pure bookmaker began). But the European mainland has never really had the kosher firms, Germany was a hotbed of criminal spankshops from the turn of the century with the retail CFD market and these were slowly surpassed by the arrival of the likes of Plus500 and Alpari with their high margin, low regulation models and the offshore firms that followed. I spent over a decade wholesaling in Europe and I can very safely say that there is barely an honest man involved in retail OTCs. Every deal expected a bung, everyone had offshore accounts, everyone was focussed purely on ripping their clients off.

Add to that the money management industry in the EU has always seen OTC trading as stealing client money from them that they should have been spanking for fees whether via their structured funds or ghastly products like covered warrants (turbos, sprinters, listed CFDs) and so they have always lobbied the authorities against retail OTCs and lobbying in the EU appears from my experience to involve lavish lunches, holidays and walking trips into Switzerland with bags of cash.

About 2/3rds of my revenue is derived from European clients. Much of this is copy trading where our margins are already much lower than with self directed trading accounts so the impact there will be hard but not terminal.

Maybe Brexit will mean the FCA don’t enact the same guidelines as Europe and our UK business will remain as is but I can’t see the EU permitting us to sit 20 miles away and hoover up their retail clients.

As a result we’re looking at Asia going forward for growth. More people who have more money and they are a people looking to the future not looking to the past and imploding like Europe seems to be. I’m far too small an enterprise to afford the time to get involved in fighting in a depressing market place that wants to die, sometimes I feel like the only person in my industry who is not clinically depressed.

The ESMA rates are very low and you don’t need them that lownin order to protect the client. The industry worked for over 30 years on a pretty uniform set of industry margins that protected client and broker and these margins were essentially the margins that the clearers were offering for hedging. It’s only in the last decade with the meteoric rise of the pure bookmaker which was run as a marketing enterprise that they broke away from the historic margins (funnily enough there is a very good argument that this happened as a direct result of the regulators stopping brokers from being able to use client money as margin for that client’s trade at the clearers!!! Suddenly most firms couldn’t hedge even if they wanted to and so the rise of the pure bookmaker began). But the European mainland has never really had the kosher firms, Germany was a hotbed of criminal spankshops from the turn of the century with the retail CFD market and these were slowly surpassed by the arrival of the likes of Plus500 and Alpari with their high margin, low regulation models and the offshore firms that followed. I spent over a decade wholesaling in Europe and I can very safely say that there is barely an honest man involved in retail OTCs. Every deal expected a bung, everyone had offshore accounts, everyone was focussed purely on ripping their clients off.

Add to that the money management industry in the EU has always seen OTC trading as stealing client money from them that they should have been spanking for fees whether via their structured funds or ghastly products like covered warrants (turbos, sprinters, listed CFDs) and so they have always lobbied the authorities against retail OTCs and lobbying in the EU appears from my experience to involve lavish lunches, holidays and walking trips into Switzerland with bags of cash.

About 2/3rds of my revenue is derived from European clients. Much of this is copy trading where our margins are already much lower than with self directed trading accounts so the impact there will be hard but not terminal.

Maybe Brexit will mean the FCA don’t enact the same guidelines as Europe and our UK business will remain as is but I can’t see the EU permitting us to sit 20 miles away and hoover up their retail clients.

As a result we’re looking at Asia going forward for growth. More people who have more money and they are a people looking to the future not looking to the past and imploding like Europe seems to be. I’m far too small an enterprise to afford the time to get involved in fighting in a depressing market place that wants to die, sometimes I feel like the only person in my industry who is not clinically depressed.

From a client's perspective I hope it doesn't diminish competition, even if it's just the big boys fighting for each client.

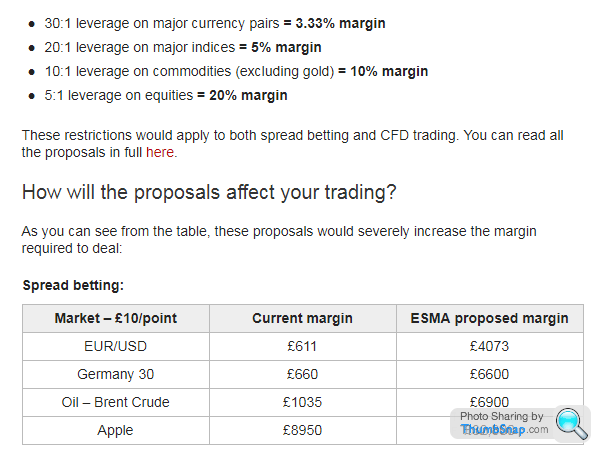

I'm not sure why the proposed margin / leverage for FX is higher than indices. I'd have thought the former has much greater potential for large unexpected, account-damaging moves than the latter. What was the last time something like that happened on an index? DJIA 2010 'flash crash'? I guess there are more considerations than that.

If the margin / leverage is uniform across Europe, maybe that'll encourage people simply to put more into their accounts who otherwise wouldn't. Or go to some dodgy broker somewhere outside the regulator's reach...

I was thinking, could a broker based somewhere potentially trustworthy like Australia attract UK / EU clients and place hardware this side?

I'm not sure why the proposed margin / leverage for FX is higher than indices. I'd have thought the former has much greater potential for large unexpected, account-damaging moves than the latter. What was the last time something like that happened on an index? DJIA 2010 'flash crash'? I guess there are more considerations than that.

If the margin / leverage is uniform across Europe, maybe that'll encourage people simply to put more into their accounts who otherwise wouldn't. Or go to some dodgy broker somewhere outside the regulator's reach...

I was thinking, could a broker based somewhere potentially trustworthy like Australia attract UK / EU clients and place hardware this side?

Liquidity really. The order books for equity futures are really quite thin so once you’ve lifted what’s showing at best then you can gap down very rapidly trying to get a fill. FX is much more liquid.

The retail market though never traded FX until MT4 came along as a means to make a market and wipe out clients and that was when shops sprang up to preach about FX.

The retail market though never traded FX until MT4 came along as a means to make a market and wipe out clients and that was when shops sprang up to preach about FX.

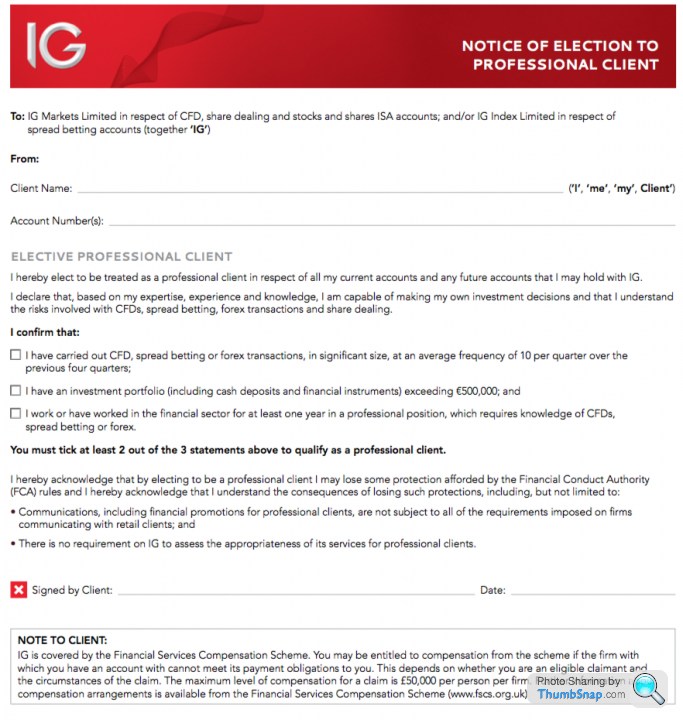

I keep getting the impression from IG that they feel that "big", "experienced" traders will be exempt from new regulations and can keep existing leverage

Although many people have also said they expect Binary to be banned all together - which I find illogical because its actually quite a fun product to trade against an existing position but I guess a lot of retail investors have blown up trading binaries in isolation

Although many people have also said they expect Binary to be banned all together - which I find illogical because its actually quite a fun product to trade against an existing position but I guess a lot of retail investors have blown up trading binaries in isolation

DonkeyApple said:

Liquidity really. The order books for equity futures are really quite thin so once you’ve lifted what’s showing at best then you can gap down very rapidly trying to get a fill. FX is much more liquid.

I assume index futures are also thinner in that case. traxx said:

I keep getting the impression from IG that they feel that "big", "experienced" traders will be exempt from new regulations and can keep existing leverage

Although many people have also said they expect Binary to be banned all together - which I find illogical because its actually quite a fun product to trade against an existing position but I guess a lot of retail investors have blown up trading binaries in isolation.

I think it's like this. Although many people have also said they expect Binary to be banned all together - which I find illogical because its actually quite a fun product to trade against an existing position but I guess a lot of retail investors have blown up trading binaries in isolation.

The FCA have proposed two tiers of traders. Inexperienced and experienced. The latter would be allowed greater leverage than the former. IG are referring to the latter as 'professionals'.

The ESMA have proposed banning binary products but not banning them for 'professionals'.

I assume IG are thinking that if they can get traders to prove they are 'professionals' then they will be able to offer both higher leverage and binary products.

I note when asking people to declare themselves as 'professionals' they have written (I don't have it to hand) that they don't need to follow best execution rules or something similar. Hopefully DA can expand on that.

The upside of classifying a client as ‘professional’ is that they both opt out of the FSCS and you can use their funds to hedge their positions, or other clients’ positions. You also de seg those funds.

It’s a difficult area as in the one hand with genuine professional traders it’s a good thing that they become segregated from retail client pooled accounts, it’s important that their funds are used at the clearers to hedge their positions. You can offer insurance policies to protect them from broker default as they will not be covered by the FSCS although their balances are usually well in excess anyway.

The massive problem is that because there are benefits to moving a client to professional then it is open to abuse and many firms have tried all sorts of wheezes to get clients to elect up. They’ve offered interest on deposits, preferential rates, bonuses etc. None of which benefit the client.

If the proposal is to define margin restrictions via professional/non professional then to me, at first glance, it’s a disaster waiting to happen as thousands of retail clients will elect up when they never should and throw away their basic protections. Any new margining criteria should not be structured around this existing pair of client criteria. It is not fair to the clients nor safe for them. It would be another case of the regulator creating risk out of thin air.

My current thinking is that the most suitable solution is for any client who wants higher margin to prove through tests, declarations and evidence of track record that they understand any associated risks but not to link a change to any loss of client protection.

It’s a difficult area as in the one hand with genuine professional traders it’s a good thing that they become segregated from retail client pooled accounts, it’s important that their funds are used at the clearers to hedge their positions. You can offer insurance policies to protect them from broker default as they will not be covered by the FSCS although their balances are usually well in excess anyway.

The massive problem is that because there are benefits to moving a client to professional then it is open to abuse and many firms have tried all sorts of wheezes to get clients to elect up. They’ve offered interest on deposits, preferential rates, bonuses etc. None of which benefit the client.

If the proposal is to define margin restrictions via professional/non professional then to me, at first glance, it’s a disaster waiting to happen as thousands of retail clients will elect up when they never should and throw away their basic protections. Any new margining criteria should not be structured around this existing pair of client criteria. It is not fair to the clients nor safe for them. It would be another case of the regulator creating risk out of thin air.

My current thinking is that the most suitable solution is for any client who wants higher margin to prove through tests, declarations and evidence of track record that they understand any associated risks but not to link a change to any loss of client protection.

This the FCA wording from 1.16 where I think the two tiers are from: https://www.fca.org.uk/publication/consultation/cp...

The FCA are talking about 'experienced retail clients'. Is that what IG are calling 'professional' in the form posted by traxx? Perhaps not as the FCA's proposed requirements are lower.

IG also produced a document (I think it was launched in the platform) which spoke of some 'best execution' rules which they don't need to follow when classing someone as a professional. Do you know anything about that DA?

Would there be any greater spread betting tax implications when classing oneself as a professional?

The FCA are talking about 'experienced retail clients'. Is that what IG are calling 'professional' in the form posted by traxx? Perhaps not as the FCA's proposed requirements are lower.

IG also produced a document (I think it was launched in the platform) which spoke of some 'best execution' rules which they don't need to follow when classing someone as a professional. Do you know anything about that DA?

Would there be any greater spread betting tax implications when classing oneself as a professional?

Yup, the IG form is a separate matter related to electing yourself up to be classed as professional. As a professional the retail best ex policy would no longer apply to you. Not that this would have any impact in normal trading but I suspect it becomes an opportunity for the broker during an event like the CHF decoupling a couple of years back?

The tax aspect I don’t think impacts. The revenue have their own set of criteria for their term ‘professional’ and they are orientated around how you earn your living. Ie if the majority of your income is from trading then strictly speaking you become liable for income tax on your trading gains. I can’t recall it ever being enforced by the revenue. More the other way around where someone will claim to be a professional trader, obtain the classification and then get an offshore OTC broker to create a falsified massive trading loss that the individual then uses to claim back X number of years of income tax. There was some such wheeze going on a few years ago along those lines.

The tax aspect I don’t think impacts. The revenue have their own set of criteria for their term ‘professional’ and they are orientated around how you earn your living. Ie if the majority of your income is from trading then strictly speaking you become liable for income tax on your trading gains. I can’t recall it ever being enforced by the revenue. More the other way around where someone will claim to be a professional trader, obtain the classification and then get an offshore OTC broker to create a falsified massive trading loss that the individual then uses to claim back X number of years of income tax. There was some such wheeze going on a few years ago along those lines.

Edited by DonkeyApple on Monday 22 January 01:17

Gassing Station | Finance | Top of Page | What's New | My Stuff