Resisting the instinct to tinker?

Discussion

Other than willpower and common sense has anyone struggled to sit back and do nothing with what's supposed to be a long term investment?

Part of the question comes from looking at likes of Fidelity who offer everything under the sun (almost) v. say Vanguard who only offer Vanguard products.

I could see having access to so many options being a great thing, but also a potential recipe for disaster if you don't know what you're doing?

Kid in a sweet shop anyone?

Part of the question comes from looking at likes of Fidelity who offer everything under the sun (almost) v. say Vanguard who only offer Vanguard products.

I could see having access to so many options being a great thing, but also a potential recipe for disaster if you don't know what you're doing?

Kid in a sweet shop anyone?

I try not to tinker, but I do constantly monitor my percentages of each sector, country and region.

So....towards the end of '17 I cut the upper cream off asian and emerging market funds as they were up 40%.

Yesterday I seriously cut my exposure to US banks (30% cut) .

It is often difficult sell some shares in the best performing funds.

But if you don't your diversification will become too heavy in some places, light in others and more susceptible to corrections.

I go back 6 months later and check my changes to see if my decisions were good,

ETA I do changes in a way not to cause tax events if possible.

So....towards the end of '17 I cut the upper cream off asian and emerging market funds as they were up 40%.

Yesterday I seriously cut my exposure to US banks (30% cut) .

It is often difficult sell some shares in the best performing funds.

But if you don't your diversification will become too heavy in some places, light in others and more susceptible to corrections.

I go back 6 months later and check my changes to see if my decisions were good,

ETA I do changes in a way not to cause tax events if possible.

Edited by jeff m2 on Thursday 18th January 14:13

I have a portfolio where many of the same shares have been held for 20 years. I agree with you that you certainly need something to stop the desire to continually change holdings. Frequent changes to holdings can sometimes be more like gambling than investing. Hoping for luck that the decision was correct, rather than sticking with a business, which is steadily increasing profits and raising dividends. Changes will also add to your overheads costs.

You could try my system if you want. The principle is to know precisely the overall progress that you are making, when compared to whatever market average that you choose.

If you tend to run mostly with, or ahead of your chosen benchmark, then don't change anything.

If you cannot keep up, then it is telling you that you are holding some of the wrong investments. It then would become awkward, but fortunately I have not had to deal with that.

What I hold is private, but I can tell you they are mostly very large FTSE 100 constituents, international, non-cyclical businesses.

You only need a spreadsheet to operate this system, and if you are very keen, perhaps do an end of week valuation. Restart your figures every 1st January.

This system is very helpful when markets are in decline, because if you can see you are down by 10% for example, but your benchmark is down 20%, then all is still going OK and hopefully you should be well placed for an upturn. It is the old percentage problem. A 50% drop requires a 100% rise, just to get back to where you were.

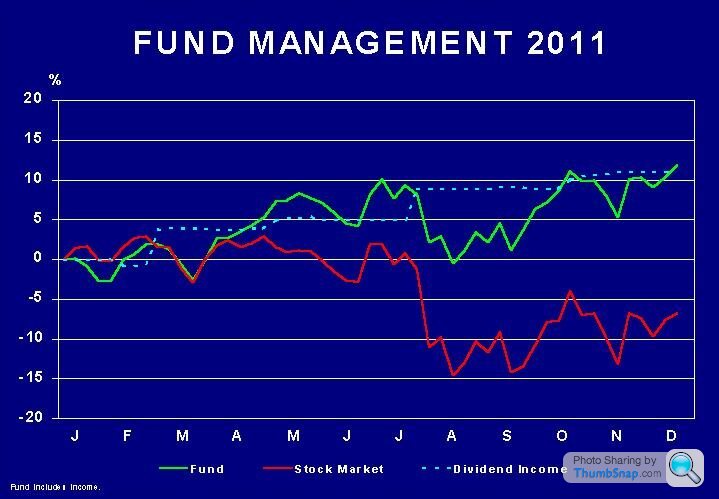

A chart helps greatly to monitor progress. This is an example of one of my annual charts. Note how it consists of only 3 lines. It is all too easy to complicate this subject.

If you wonder about the two sharp uplifts to total dividends, it is because many companies have a 31st December end of financial year, so their dividend increase announcements (final and interim) occur in spring and late summer.

Best of luck to you.

Edited by Jon39 on Thursday 18th January 20:01

b hstewie said:

hstewie said:

hstewie said: Other than willpower and common sense has anyone struggled to sit back and do nothing with what's supposed to be a long term investment?

Part of the question comes from looking at likes of Fidelity who offer everything under the sun (almost) v. say Vanguard who only offer Vanguard products.

I could see having access to so many options being a great thing, but also a potential recipe for disaster if you don't know what you're doing?

Kid in a sweet shop anyone?

They say good investing is supposed to be as exciting as watching paint dry.Part of the question comes from looking at likes of Fidelity who offer everything under the sun (almost) v. say Vanguard who only offer Vanguard products.

I could see having access to so many options being a great thing, but also a potential recipe for disaster if you don't know what you're doing?

Kid in a sweet shop anyone?

My experience is that excitement and good return very rarely correlate (I've only be at it a couple of years). Give yourself 5% to play with, let someone else look after the rest.

Whatever you do don't read the LSE boards for AIM stocks, it's red rag to a bull.

Jon39 said:

I have a portfolio where many of the same shares have been held for 20 years. I agree with you that you certainly need something to stop the desire to continually change holdings. Frequent changes to holdings can sometimes be more like gambling than investing. Hoping for luck that the decision was correct, rather than sticking with a business, which is steadily increasing profits and raising dividends. Changes will also add to your overheads costs.

You could try my system if you want. The principle is to know precisely the overall progress that you are making, when compared to whatever market average that you choose.

If you tend to run mostly with, or ahead of your chosen benchmark, then don't change anything.

Jon39 said:

If you cannot keep up, then it is telling you that you are holding some of the wrong investments. It then would become awkward, but fortunately I have not had to deal with that.

Only because you’ve chosen to compare against the wrong benchmark!Jon39 said:

A chart helps greatly to monitor progress. This is an example of one of my annual charts. Note how it consists of only 3 lines. [b]It is all too easy to complicate this subject.[/n]

If you wonder about the two sharp uplifts to total dividends, it is because many companies have a 31st December end of financial year, so their dividend increase announcements (final and interim) occur in spring and late summer.

It’s also all too easy to oversimplify this subject and to use an incorrect benchmark which provides a misleading picture of what is actually going on!If you wonder about the two sharp uplifts to total dividends, it is because many companies have a 31st December end of financial year, so their dividend increase announcements (final and interim) occur in spring and late summer.

bhstewie said:

hstewie said: Other than willpower and common sense has anyone struggled to sit back and do nothing with what's supposed to be a long term investment?

Equity investment should be a long term decision - however that doesn’t mean that your investment shouldn’t be monitored on a regular basis.You do need to differentiate between monitoring the outcome of your investment decision and your choice of implementing that decision i.e. which equity / investment markets / sectors you have chosen and how you have effected that decision (active v passive and which manager in the case of an active strategy).

Plenty of ‘casual’ investors underestimate the risks they are running (due to having poorly diversified portfolios) or use inappropriate benchmarks which don’t reflect the opportunity set they have access to compared to that benchmark.

Personally I’d suggest that market / sector allocation is kept as broad as possible (or left to the professionals), with minimal changes from year to year unless you have really strong views. Don’t underestimate the impact of trading costs!

For most people, who don’t have the time or inclination, a passive global equity approach would see them achieve decent long terms returns without undue volatility or risk.

For those that must ‘tinker’, I’d still suggest keeping a significant proportion as above, and just tinker with a proportion of your holding!

sidicks said:

Personally I’d suggest that market / sector allocation is kept as broad as possible (or left to the professionals), with minimal changes from year to year unless you have really strong views. Don’t underestimate the impact of trading costs!

Appreciate this is a YMMV one depending what they're doing but assuming no "human" interaction i.e. done online but tons of choices from total DIY to some level of active management even of reasonably passive funds what do you consider reasonable charges?Psychologically <= 1% doesn't sound much but equally it's still double those @ 0.4-0.5%

bhstewie said:

hstewie said: Appreciate this is a YMMV one depending what they're doing but assuming no "human" interaction i.e. done online but tons of choices from total DIY to some level of active management even of reasonably passive funds what do you consider reasonable charges?

Psychologically <= 1% doesn't sound much but equally it's still double those @ 0.4-0.5%

You need to differentiate the platform fee (“admin”) from the fund fee (“investment management”).Psychologically <= 1% doesn't sound much but equally it's still double those @ 0.4-0.5%

For passive strategies I’d expect fees below 0.5% depending on asset classes / sectors.

sidicks said:

Only because you’ve chosen to compare against the wrong benchmark!

Where could the Total Return index have been found in 1988?

Those were very different days, when you had to wait for the next days newspaper, to even see share prices.

It might have been in the FT, but few private individuals bought that every day.

Anyway, you clearly have far superior knowledge of this subject than me, so consequently you must made a Billion using your investment skills, not just a paltry M.

As a help to the OP, why don't you write about your expert investment techniques, and answer the original question of how to 'resist the instinct to tinker' ?

Jon39 said:

Where could the Total Return index have been found in 1988?

Those were very different days, when you had to wait for the next days newspaper, to even see share prices.

It might have been in the FT, but few private individuals bought that every day.

2. Despite the flaws identified in your process, you are still claiming that you’ve not needed to change your strategy ‘because you’ve outperformed the benchmark’, when you really haven’t!

Jon39 said:

Anyway, you clearly have far superior knowledge of this subject than me, so consequently you must made a Billion using your investment skills, not just a paltry M.

I also know how to play football, but that doesn’t mean I’m about to join the Premier League!

I do at least understand the need for a relevant and appropriate benchmark. So that puts me one step ahead already!

The OP is asking for help - I don’t believe that you pretending that you’ve performed better than you actually have is going to help him!

Jon39 said:

As a help to the OP, why don't you write about your expert investment techniques, and answer the original question of how to 'resist the instinct to tinker' ?

I have already done so.Edited by sidicks on Friday 19th January 10:08

bhstewie said:

hstewie said: All in?

See examples here:http://www.hl.co.uk/funds/index-tracker-funds/weal...

Much cheaper than 0.5%

sidicks said:

Jon39 said:

... Anyway, you clearly have far superior knowledge of this subject than me, so consequently you must made a Billion using your investment skills, not just a paltry M.

I also know how to play football, but that doesn’t mean I’m about to join the Premier League!

I do at least understand the need for a relevant and appropriate benchmark.

So that puts me one step ahead already.

Mr. Sidicks,

You seem to be mesmerized by benchmarks, and have continually suggested that I need to change my investment system.

I thought the main reason to invest, was to try achieve the best capital increase possible, together with the best possible increase in income flow.

Whether one beats a benchmark is interesting and can be a useful aid, but certainly not the most important aspect to me.

To have been able to access weekly total return indicies in 1988, you would almost have needed to be working in the City. That information is now readily available, and you criticise me for not going through 30 years of data, to recalculate all the numbers.

It would make no difference to the returns already obtained, so what would be the benefit?

With your enthusiasm for benchmark wizardry, please tell me from the following performance figures, whether the FTSE All-Share Index Total Return has beaten me over the 30 year period. I am not bothered at all, but you might enjoy telling me that a 30 year tracker fund (after fees) would have left me in the dust. Probably unlikely though, but I await your calculations with interest.

To 29th December 2017

1 year = + 8.28%

2 years = +31.41%

3 years = + 39.62%

5 years = +65.62%

10 years = +163.49%

30 years = + 4553.36%

sidicks said:

Thank you and yes, that's the fund cost but with HL for example there is their 0.45% management fee so then you're up into 0.6-0.7% all in.Jon39 said:

Mr. Sidicks,

No need for the formality, Sidicks is fine!Jon39 said:

You seem to be mesmerized by benchmarks, and have continually suggested that I need to change my investment system.

Not really true.If you want to measure performance then you need to choose an appropriate benchmark against which to asses that performance which takes account of a) your opportunity set and b) your particularly strategy. Your approach does not appear to do either.

The fact that you come on here to ‘boast’ about your performance against the benchmark means that it doesn’t seem unreasonable to highlight the massive flaws in your approach.

Jon39 said:

I thought the main reason to invest, was to try achieve the best capital increase possible, together with the best possible increase in income flow.

Different people will have different objectives, but total return is one important metric (relative to the benchmark), as is risk-adjusted return (relative to the benchmark) . Your approach doesn’t accurately reflect either.Jon39 said:

Whether one beats a benchmark is interesting and can be a useful aid, but certainly not the most important aspect to me.

Which is entirely fine, but then why do you choose to post about that performance against a (inappropriate) benchmark on here?Jon39 said:

To have been able to access weekly total return indicies in 1988, you would almost have needed to be working in the City. That information is now readily available, and you criticise me for not going through 30 years of data, to recalculate all the numbers.

It would make no difference to the returns already obtained, so what would be the benefit?

You don’t need weekly data for the comparison you are seeking to make. You already have the annual performance figures for your portfolio against which you could compare the annualised performance for the appropriate benchmark. Simple.It would make no difference to the returns already obtained, so what would be the benefit?

Jon39 said:

With your enthusiasm for benchmark wizardry, please tell me from the following performance figures, whether the FTSE All-Share Index Total Return has beaten me over the 30 year period.

I am trying not to mislead the OP with inappropriate comparisons and false claims, that is all. Jon39 said:

I am not bothered at all, but you might enjoy telling me that a 30 year tracker fund (after fees) would have left me in the dust. Probably unlikely though, but I await your calculations with interest.

You are ‘not bothered’ but you keep boasting about your track record - go figure!As above, an appropriate comparison would take into account risk and volatility, but you won’t reveal anything about your portfolio, making such a comparison impossible to make.

You’ve also not provided any information inflows and outflows to the portfolio over the period, so again a comparison is impossible to make.

Edited by sidicks on Friday 19th January 12:43

Gassing Station | Finance | Top of Page | What's New | My Stuff