London Capital and Finance

Discussion

Ginge R said:

I hate to admit but it is a masterclass in weasily words that is worded to trip people up:

ISA - just a tax free wrapper to hold an asset class, no more, no less. I suspect associated by most as a way to hold cash tax free i.e. safe.

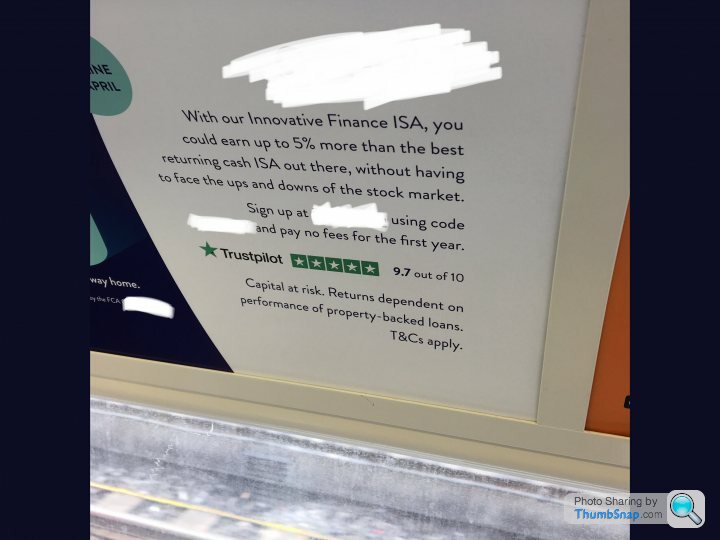

Comparison between "Innovative Finance ISA" and a "Cash ISA" re: "you could earn up to 5% more than the best returning cash ISA out there, without having to face the ups and downs of the stock market".

Bolded elements my own. Wording associates IF ISA with a Cash ISA - provides reassurance that capital is not at risk due to the vagaries of the stock market. Absolutely true. However, the advert clearly states that capital is at risk - just not via the stock market: "Returns dependent on performance of property-backed loans".

Throw in the excellent Trustpilot score, and I can see why many investors were fooled into thinking it was a safe investment. By nature, people ignore the small-print and only look at the headlines, without asking pertinent questions.

Edited by putonghua73 on Tuesday 26th March 12:38

harrycovert said:

Sold a BTL and I was thinking of investing some of the money in something other than bricks and mortar. Is there any point in checking the FCA website when companies like LC&F are registered.?

It’s always important to check. After that, if a firm is registered, it’s important to check what they are registered to do and whether the products they offer have FSCS cover. I also check the individuals and look at their history as this can help when forming an impression. Then a quick check at companies house to see how long the firm has been running and how well capitalised it is can help.

Nothing is fool proof but there are a series of easy and free online checks such as this that can help with a basic smell test.

harrycovert said:

Sold a BTL and I was thinking of investing some of the money in something other than bricks and mortar. Is there any point in checking the FCA website when companies like LC&F are registered.?

Unfortunately it does now seem that you have to search for what they are allowed to do. Being regulated is not enough and the FCA don't exactly make it any easier.For example, you may want to find out if someone is regulated for giving financial advice. The FCA call financial advisers a "CF30 Customer". That is not exactly helpful!

You may want someone to manage your money for you. You can pick from any number of firms that call themselves "Wealth Managers" and the like. Most have no FCA permissions whatsoever to actually manage (or even touch) your money.

You could end up with an appointed rep telling you what to do with your money - whilst they take no financial risk whatsoever (but a large chunk of your money).

My advice (not in the regulated sense) would be to explore people here who make sense. Derek Chevalier would be a good start. Nik from the IM sticky another.

Both are open and honest. They will also point you to alternative solutions.

Over the years on PH I have learned 5 things when it comes to money.

- If you need an accountant then use Eric

- If you need a mortgage then use Sarnie

- If you need financial advice use Derek

- If you are unsure, listen to DonkeyApple

- If you want a sense check, ask Nik on the IM sticky

I hope this is helpful

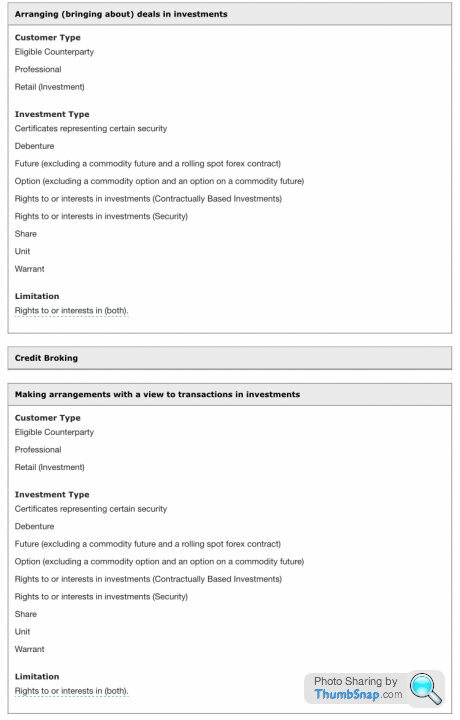

An example

Here is a screen shot from the fca detailing the permissions held.

Now

The company (loose term, wolf in sheep’s clothing may be more accurate), is/should be a money lender, that’s should have been it’s principal activity.

Note there are no credit broking permissions (its principle activity)?

There are no suits of armour with any investment, but if you do it with a proper advisor, through a proper firm, into properly managed funds you’ve got a chance, if a fund/advisory company goes sideways.

If you choose to chase an out of this world return, against illiquid security vs your investment, you really need to think about how much you can afford to lose, some of these investments may work, but the reality is they are not for the retail investor and even for an experienced high net worth investor would/should create challenges as to why to invest.

Credibility and ‘having some wool on your back’ are key for advisors these days (investment and or debt).

Here is a screen shot from the fca detailing the permissions held.

Now

The company (loose term, wolf in sheep’s clothing may be more accurate), is/should be a money lender, that’s should have been it’s principal activity.

Note there are no credit broking permissions (its principle activity)?

There are no suits of armour with any investment, but if you do it with a proper advisor, through a proper firm, into properly managed funds you’ve got a chance, if a fund/advisory company goes sideways.

If you choose to chase an out of this world return, against illiquid security vs your investment, you really need to think about how much you can afford to lose, some of these investments may work, but the reality is they are not for the retail investor and even for an experienced high net worth investor would/should create challenges as to why to invest.

Credibility and ‘having some wool on your back’ are key for advisors these days (investment and or debt).

harrycovert said:

Sold a BTL and I was thinking of investing some of the money in something other than bricks and mortar. Is there any point in checking the FCA website when companies like LC&F are registered.?

Such a good point. The register is in the process of being updated, but it’s going to be a long and tortured process. It’s nigh on impossible to do proper due diligence when you don’t know what you don’t know. To be fair, that’s why you rely on the likes of advisers and even the most provincial SIPP providers to have properly verifiable and credible procedures in place do it for you (fingers crossed) if you do decide to invest. What the real world calls advice, we call a personal recommendation. Please don’t think it’s advice - I’m acutely conscious is not ever giving a ‘value judgement’. What I would say is this. Unless you have a pro, like a SIPP provider, an adviser or the like, doing due diligence, think about sticking with brands that you know and are comfortable with. I’m not taking on clients, so I have no skin in the game - but if you would like to have a natter about the more general aspects, please don’t hesitate to drop me a line.

millen said:

Recent development, I think:

https://www.investmentweek.co.uk/investment-week/n...

Ohh treasury select committee, so its been sent up the the BEIS then, let's hope they do a fact find/hearing on BBC Parliament channel.https://www.investmentweek.co.uk/investment-week/n...

Yep! Interesting times...

New Model Adviser also covered this in some depth in advance of the posted link (The Investment Week coverage seems to be a duplication of NMA's original report):

https://citywire.co.uk/new-model-adviser/news/fca-...

The basics are:

Edited to add the New Model Adviser is part of Citywire - sorry if that caused any confusion!

New Model Adviser also covered this in some depth in advance of the posted link (The Investment Week coverage seems to be a duplication of NMA's original report):

https://citywire.co.uk/new-model-adviser/news/fca-...

The basics are:

Citywire said:

The Financial Conduct Authority (FCA) will be subject to an independent investigation over its supervision of failed mini-bond firm London Capital & Finance (LC&F).

In a meeting on Thursday, the FCA board decided that an independent person should investigate the regulator’s supervision of LC&F. This investigation will also look at whether the existing regulatory system adequately protects retail purchasers of mini-bonds from ‘unacceptable levels of harm’.

This follows the chair of the Treasury Select Committee Nicky Morgan writing to the Treasury to ask for an investigation into the FCA’s handling of LC&F and to see if it should bring mini-bonds under its regulatory perimeter.

It is about time.In a meeting on Thursday, the FCA board decided that an independent person should investigate the regulator’s supervision of LC&F. This investigation will also look at whether the existing regulatory system adequately protects retail purchasers of mini-bonds from ‘unacceptable levels of harm’.

This follows the chair of the Treasury Select Committee Nicky Morgan writing to the Treasury to ask for an investigation into the FCA’s handling of LC&F and to see if it should bring mini-bonds under its regulatory perimeter.

Edited to add the New Model Adviser is part of Citywire - sorry if that caused any confusion!

Edited by JulianPH on Tuesday 2nd April 15:50

Another update:

https://www.professionaladviser.com/professional-a...

Due to the financial promotion of the 'bonds' being a regulated activity (signed off by a regulated firm) there could be FSCS compensation available.

https://www.professionaladviser.com/professional-a...

Due to the financial promotion of the 'bonds' being a regulated activity (signed off by a regulated firm) there could be FSCS compensation available.

More on the LCF big cheese salesman https://www.standard.co.uk/business/administrators...

996driver said:

Looks like LCF have found a loophole to avoid submitting their accounts to Companies House. It appears if you reduce your financial reporting period by 1 day then the filing date is extended by 3 months. So by doing this you can avoid the scrutiny that comes from having your compnay accounts publicly accessible. You might wonder why they would want to do so

There is so more to read here with some extensive discussion of the risks

https://forums.moneysavingexpert.com/showthread.ph...

and here

https://damn-lies-and-statistics.blogspot.com/2017...

Looks like Blackmore, another mini bond that was being promoted by Surge Financial has pulled the same act. There is so more to read here with some extensive discussion of the risks

https://forums.moneysavingexpert.com/showthread.ph...

and here

https://damn-lies-and-statistics.blogspot.com/2017...

Blackmore Bonds

https://www.telegraph.co.uk/investing/bonds/mini-b...

I also notice that Dolphin has apparently delayed paying out on a bond maturity, as if a name change wasn’t dubious enough.

As another firm paying over 20% of the investors’ capital away upfront to cold callers and the recent delay does seem to suggest that they have been using new money to pay out old and that new money has stopped flowing.

https://www.telegraph.co.uk/investing/bonds/mini-b...

I also notice that Dolphin has apparently delayed paying out on a bond maturity, as if a name change wasn’t dubious enough.

As another firm paying over 20% of the investors’ capital away upfront to cold callers and the recent delay does seem to suggest that they have been using new money to pay out old and that new money has stopped flowing.

Ginge R said:

Good luck! Fingers crossed.

...

An example of a mini bond is one for Mexican fast food chain Chilango, which offered a free burrito every week over the fixed 4-year term of the investment, to anyone who invested over £10,000. Madness.

...

"Chilango bond holders to be offered either 10p in the pound to cash out their investment, or shares in the company."...

An example of a mini bond is one for Mexican fast food chain Chilango, which offered a free burrito every week over the fixed 4-year term of the investment, to anyone who invested over £10,000. Madness.

...

https://twitter.com/langtoncapital/status/12046665...

---

Chilango has confirmed a proposed CVA that would see it exit four leases and cut rents by 40% at some of its remaining sites.

https://twitter.com/langtoncapital/status/12046664...

I am working on sourcing a bond issue at the moment and I’ve found is that even with the correct mechanism and an appropriate fund raising solution the serious issue is reputational risk. It just doesn’t seem possible to put an issue together without a name on the boilerplate that doesn’t appear to have been involved in minibonds, pension, crypto’s, AIM or any of the latest games the FCA actively non regulates.

While I’ve always known the type of person who has been involved in these what I didn’t quite appreciate is that it doesn’t look like you can put a deal together without their names appearing and for me that makes it really difficult to do a deal as you know that how ever hard you work to put an honest issue together it can be blown away by an expose on one of these people or their latest company.

It is far more endemic that I even believed and I already thought it was well over 50% filth and junk on all of this stuff.

While I’ve always known the type of person who has been involved in these what I didn’t quite appreciate is that it doesn’t look like you can put a deal together without their names appearing and for me that makes it really difficult to do a deal as you know that how ever hard you work to put an honest issue together it can be blown away by an expose on one of these people or their latest company.

It is far more endemic that I even believed and I already thought it was well over 50% filth and junk on all of this stuff.

Gassing Station | Finance | Top of Page | What's New | My Stuff