Intelligent Money - your investment questions answered

Discussion

mikeiow said:

I can confirm that the Windstar yacht fits very nicely in Monte Carlo harbour: we were lucky enough to spend a few days on it some years back as a “work reward” trip which ended with us filling a large chunk of the harbour there and enjoying a black tie night at the Sporting Club: happy days

I’ll take the role of Chief Cook and Bottle Washer: it’s a tough job, but someone has to do it

I was tempted, but only capacity for 148 guests it is not big enough for our PHer Private Clients.I’ll take the role of Chief Cook and Bottle Washer: it’s a tough job, but someone has to do it

And I was so close!

kers !

kers !

JulianPH said:

mikeiow said:

I can confirm that the Windstar yacht fits very nicely in Monte Carlo harbour: we were lucky enough to spend a few days on it some years back as a “work reward” trip which ended with us filling a large chunk of the harbour there and enjoying a black tie night at the Sporting Club: happy days

I’ll take the role of Chief Cook and Bottle Washer: it’s a tough job, but someone has to do it

I was tempted, but only capacity for 148 guests it is not big enough for our PHer Private Clients.I’ll take the role of Chief Cook and Bottle Washer: it’s a tough job, but someone has to do it

And I was so close!

eta - ahhh, 100 pages up, the thread that delivers :hehe

Rewe said:

Hi everyone,

I'm a first time poster here and financial novice - please be kind!

I'm after some general advice. I'm thinking about taking early retirement from one field to start in a new one. As part of this, I would get about £85000 in a lump sum. My mortgage is about £110K currently. Would I (typically) be better off reducing my mortgage or investing in something? I am very risk averse. What are the general pros and cons or "gotchas"? Does being a higher/lower rate tax payer have any impact?

Thanks in advance?

Hi ReweI'm a first time poster here and financial novice - please be kind!

I'm after some general advice. I'm thinking about taking early retirement from one field to start in a new one. As part of this, I would get about £85000 in a lump sum. My mortgage is about £110K currently. Would I (typically) be better off reducing my mortgage or investing in something? I am very risk averse. What are the general pros and cons or "gotchas"? Does being a higher/lower rate tax payer have any impact?

Thanks in advance?

We are always kind!

As you are very risk adverse then reducing your mortgage, rather than investing in something, would always be the first option for you to take.

The "pro" here is total certainty and reduced debt/monthly outgoings.

The "con" is that with interest (and therefore mortgage) rates being so low, investment returns could provide massive outperformance over the mortgage reduction.

"Could" is the operative word here though. This is where the risk element comes in.

Paying off the mortgage gives you a guaranteed return/upside, as you have to pay this off at some time anyway and the earlier you do it the less it costs you in interest.

Investing "could" give you significantly his financial returns over time, but there is no guarantee of this.

So on face value, given you are very risk adverse, about to completely change your career field and have the ability to reduce your mortgage to just £25k, then this seems to be an incredibly sensible option.

There may be other factors involved though, such as you current pension/retirement provision. Your tax rate also has an important impact as a pension investment would entitle you to full income tax relief.

If you would like to chat through this with someone please feel free to contact Nik at nik.burrows@intelligentmoney.com or, of course, ask further here or send me a PM.

I hope that has been a helpful start.

Cheers

Julian

mikeiow said:

JulianPH said:

mikeiow said:

I can confirm that the Windstar yacht fits very nicely in Monte Carlo harbour: we were lucky enough to spend a few days on it some years back as a “work reward” trip which ended with us filling a large chunk of the harbour there and enjoying a black tie night at the Sporting Club: happy days

I’ll take the role of Chief Cook and Bottle Washer: it’s a tough job, but someone has to do it

I was tempted, but only capacity for 148 guests it is not big enough for our PHer Private Clients.I’ll take the role of Chief Cook and Bottle Washer: it’s a tough job, but someone has to do it

And I was so close!

eta - ahhh, 100 pages up, the thread that delivers :hehe

Congratulations Mike on being the one who pushed this thread over 100 pages!

Bonefish Blues said:

Look, I'm a reasonable guy. Surely we can agree terms and a sponsorship deal. How about 'Official IM Fishing Professional'. I mean, I'll wear advertising and everything. Literally a dozen people would see it. Possibly.

I'll get the merchandise made up straight away!Who needs the IM British GT Championship!

JulianPH said:

Rewe said:

Hi everyone,

I'm a first time poster here and financial novice - please be kind!

I'm after some general advice. I'm thinking about taking early retirement from one field to start in a new one. As part of this, I would get about £85000 in a lump sum. My mortgage is about £110K currently. Would I (typically) be better off reducing my mortgage or investing in something? I am very risk averse. What are the general pros and cons or "gotchas"? Does being a higher/lower rate tax payer have any impact?

Thanks in advance?

Hi ReweI'm a first time poster here and financial novice - please be kind!

I'm after some general advice. I'm thinking about taking early retirement from one field to start in a new one. As part of this, I would get about £85000 in a lump sum. My mortgage is about £110K currently. Would I (typically) be better off reducing my mortgage or investing in something? I am very risk averse. What are the general pros and cons or "gotchas"? Does being a higher/lower rate tax payer have any impact?

Thanks in advance?

We are always kind!

As you are very risk adverse then reducing your mortgage, rather than investing in something, would always be the first option for you to take.

The "pro" here is total certainty and reduced debt/monthly outgoings.

The "con" is that with interest (and therefore mortgage) rates being so low, investment returns could provide massive outperformance over the mortgage reduction.

"Could" is the operative word here though. This is where the risk element comes in.

Paying off the mortgage gives you a guaranteed return/upside, as you have to pay this off at some time anyway and the earlier you do it the less it costs you in interest.

Investing "could" give you significantly his financial returns over time, but there is no guarantee of this.

So on face value, given you are very risk adverse, about to completely change your career field and have the ability to reduce your mortgage to just £25k, then this seems to be an incredibly sensible option.

There may be other factors involved though, such as you current pension/retirement provision. Your tax rate also has an important impact as a pension investment would entitle you to full income tax relief.

If you would like to chat through this with someone please feel free to contact Nik at nik.burrows@intelligentmoney.com or, of course, ask further here or send me a PM.

I hope that has been a helpful start.

Cheers

Julian

It seems obvious now that you have explained it.

I'll be paying it towards the mortgage. (Eventually) being mortgage free is going to feel good!

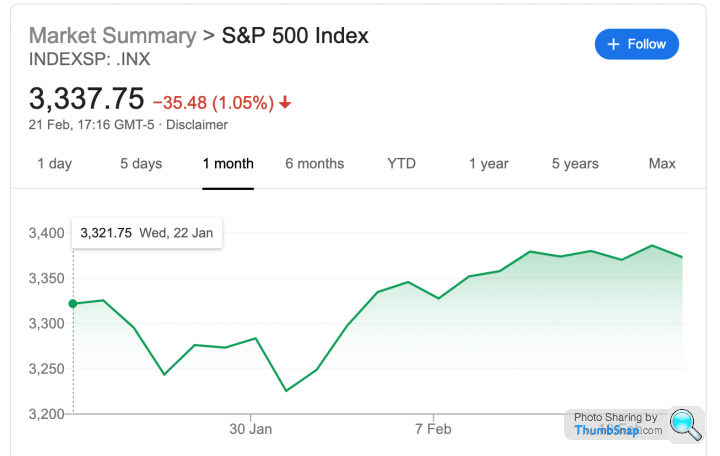

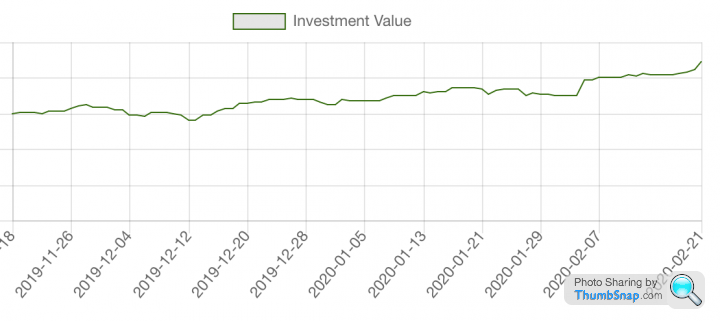

Following on from another thread talking about PH Equity (now up 14.48% over the last 3 months, more than double the S&P 500 at 6.9%) I wanted to highligh how it has done this with very little volatility.

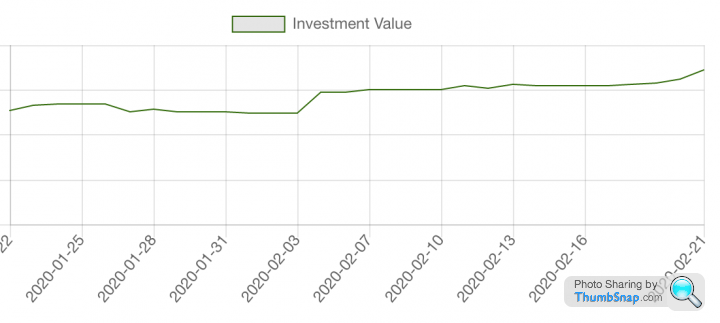

Compare the last month (I can't get my hands on 3 months for the S&P 500 right now). I have cropped out my investment amount for obvious reasons, but the periods are identical!:

S&P 500

PH Equity

When you strip out 98% of ther market you strip out a lot of the volatility, whilst doubling the performance (quite smoothly) in this case!

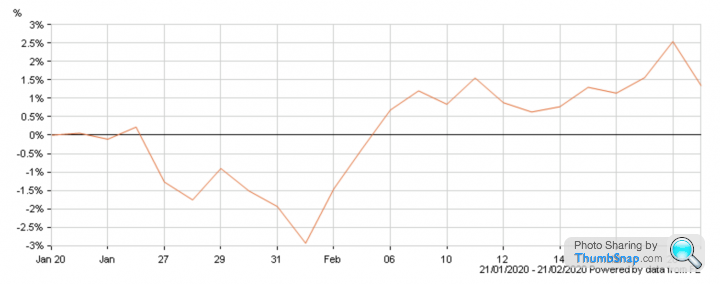

For further comparison here is Fundsmith Equity over the closest matching period I could fine (it is a few days out, but you can see the difference in volatility is huge):

Fundsmith Equity returned 1.4% over this period and PH Equity returned 8.53%.

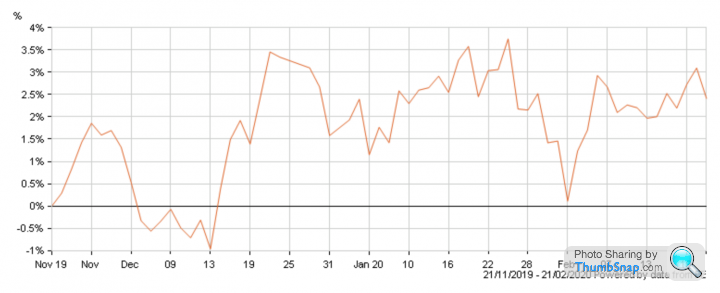

I can also show 3 months for both and had added Lindsell Train Global Equity to this mix:

Fundsmith Equity

Lindsell Train Global Equity

PH Equity

Over the last 3 months Fundsmith Equity returned 8.5%, Lindsell Train Global Equity returned 2.4% and PH Equity returned 14.48%.

So whilst the huge outperformance of PH Equity against Fundsmith and Lindsell Train is obvious, what I wanted to share was the stark difference between how we achieved this outperformance with vastly reduced volatility/risk and a smoother journey rahter than a roller coaster ride.

Julian

Compare the last month (I can't get my hands on 3 months for the S&P 500 right now). I have cropped out my investment amount for obvious reasons, but the periods are identical!:

S&P 500

PH Equity

When you strip out 98% of ther market you strip out a lot of the volatility, whilst doubling the performance (quite smoothly) in this case!

For further comparison here is Fundsmith Equity over the closest matching period I could fine (it is a few days out, but you can see the difference in volatility is huge):

Fundsmith Equity returned 1.4% over this period and PH Equity returned 8.53%.

I can also show 3 months for both and had added Lindsell Train Global Equity to this mix:

Fundsmith Equity

Lindsell Train Global Equity

PH Equity

Over the last 3 months Fundsmith Equity returned 8.5%, Lindsell Train Global Equity returned 2.4% and PH Equity returned 14.48%.

So whilst the huge outperformance of PH Equity against Fundsmith and Lindsell Train is obvious, what I wanted to share was the stark difference between how we achieved this outperformance with vastly reduced volatility/risk and a smoother journey rahter than a roller coaster ride.

Julian

irc said:

How does PH Equity compare with Fundsmith and S&P 500 over 3 and 5 years? 3 months seems quite a short time period to compare performance of long term investments.

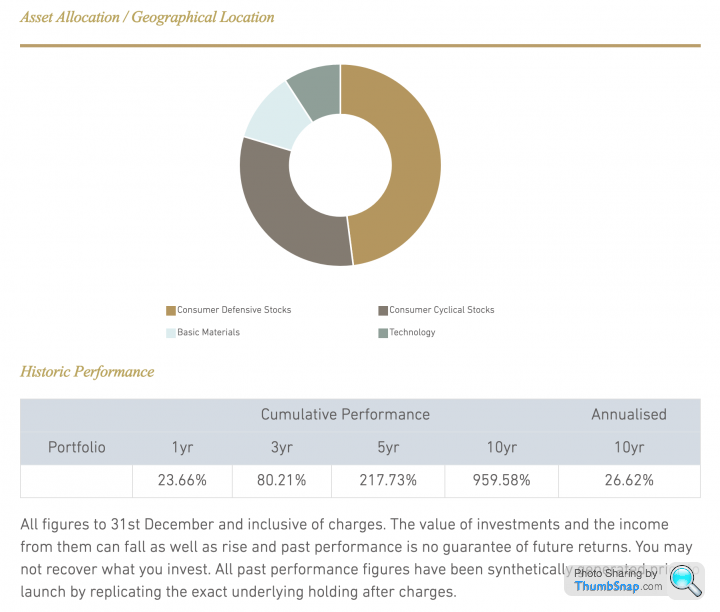

I completely agree that 3 months is a short time period, but this is the time it has been available for retail investors. Prior to that I ran it purely for family investments.I can show you the performance over longer period though as this is on our website:

- Fundsmith did c. 60% over 3 years and Lindsell Train did c. 65%. PH Equity was 80%.

- Over 5 years Fundsmith did c. 140% and Lindsell Train did c. 135%. PH Equity was 217%.

- 10 years sees Fundsmith at c. 390%, Linsell Train (only 9 year figure available)at 374% and PH Equity at 959%.

I must stress that whilst these are the real figures for PH Equity, we have to label them as "synthetic" as retail investors could not access the portfolio back then.

As I said in my post above the outperformance speacks for itself, but my real focus was on the vastly reduced volatility/risk we took in getting this outperformance.

Cheers

Julian

Edited for typo

Edited by JulianPH on Saturday 22 February 14:55

Just to add, sorry, I carried on with the Fundsmith/Lindsell Train comparisons, when you actually asked about Fundsmith/S&P 500.

S&P 500 is up 158% over 5 years.

Fundsmith has fallen short of this (see above).

PH Equity was 217.73%.

Also, PH Equity doesn't have platform charges to reduce these returns (as Fundsmith does) and has a lower annual management charge too (0.67% all inclusive OCF).

To be more precise with my numbers I've just been on the Fundsmith website and 3 year returns are 58.56% (PH Equity 80.21%), 5 years for Fundsmith is 138.11% (PH Equity 217.73%) and Fundsmith over 10 years is 392.86% (PH Equity 959.58%).

S&P 500 is up 158% over 5 years.

Fundsmith has fallen short of this (see above).

PH Equity was 217.73%.

Also, PH Equity doesn't have platform charges to reduce these returns (as Fundsmith does) and has a lower annual management charge too (0.67% all inclusive OCF).

To be more precise with my numbers I've just been on the Fundsmith website and 3 year returns are 58.56% (PH Equity 80.21%), 5 years for Fundsmith is 138.11% (PH Equity 217.73%) and Fundsmith over 10 years is 392.86% (PH Equity 959.58%).

irc said:

Thanks. Impressive numbers.

Cheers! What is more impressive (to me) is these were achieved with very low volatility/risk (hence my earlier post).

Getting impressive numbers is not simple, but if you take enough risk you can do this short term.

Doing this consistently over multiple time periods (over the long term) without taking those risks is the problem!

I remember having dinner with Terry one evening (Langar Hall, on him) not long after he had launched. He initially impressed me, but then went on to contradict himself and his investment philosophy.

This was obviously a long time ago though.

He has certainly delivered very well, but a tracker would have outperformed him over the last 5 years - at a fraction on the price.

So my own take on this is that whilst performance is incredibly important, the risk and volatility you take in extracting this performance is equally as important.

I am not knocking him in any way, just highlighting that (within these specific segments of the markets) he is behind market returns whilst I am more than double above them.

You have had fantastic returns historically though, but may perhaps want (or not) to evaluate your furture strategy using the hindsight you have.

Cheers

Julian

PS I think his fund is very good BTW and am sure it will come back to beating the markets.

Edited for typos

Edited by JulianPH on Sunday 23 February 15:04

Gassing Station | Finance | Top of Page | What's New | My Stuff