FSAVC - Pension Matures - options

Discussion

Chums

the time has come that my FSAVC will pay out and as ever I'm confronted with several options some of which are excluded to me until I take financial advice!

Firstly we're not talking a 'big pot' but it's over the £30k threshold (just) requiring me to instruct a finnacial adviser, and it has a GAR.

I'm already in receipt of a very good pension so an 'additional' income of £155 gross per month for the rest of life (given it is not index linked) has limited appeal. Taking the max tax free lump sum (leaving £116 gross/month) makes sense to me given it would take c20yrs to accrue it through the monthly income extra if I didn't take it. I'm not confident of living another active 20yrs plus (despite good health) plus when/if I get the state pension in 12yrs that's more income to come.

GAR protects my payments for 5yrs but thereafter if I snuff it all is lost so its got me thinking. I like the idea of taking larger amounts every quarter/6 monthly but cannot with the 'standard' option. A fixed term annuity does not appear an option and I'm left with transfering the pot to a 'Retirement Account' which looks to be stock market invested in a 'cautious' fund. It would however let me take a min £500pm from it (subject to tax) as and when but presumably the fund is classed as my estate whilst the money is there? I'm already exposed to market funds so fluctuation doesn't necessarily bother me and buying in now given Brexit might not be a bad option.

Is this last option popular amongst those taking small free standing pensions and can someone advise the pitfalls or if I'm missing anything?

the time has come that my FSAVC will pay out and as ever I'm confronted with several options some of which are excluded to me until I take financial advice!

Firstly we're not talking a 'big pot' but it's over the £30k threshold (just) requiring me to instruct a finnacial adviser, and it has a GAR.

I'm already in receipt of a very good pension so an 'additional' income of £155 gross per month for the rest of life (given it is not index linked) has limited appeal. Taking the max tax free lump sum (leaving £116 gross/month) makes sense to me given it would take c20yrs to accrue it through the monthly income extra if I didn't take it. I'm not confident of living another active 20yrs plus (despite good health) plus when/if I get the state pension in 12yrs that's more income to come.

GAR protects my payments for 5yrs but thereafter if I snuff it all is lost so its got me thinking. I like the idea of taking larger amounts every quarter/6 monthly but cannot with the 'standard' option. A fixed term annuity does not appear an option and I'm left with transfering the pot to a 'Retirement Account' which looks to be stock market invested in a 'cautious' fund. It would however let me take a min £500pm from it (subject to tax) as and when but presumably the fund is classed as my estate whilst the money is there? I'm already exposed to market funds so fluctuation doesn't necessarily bother me and buying in now given Brexit might not be a bad option.

Is this last option popular amongst those taking small free standing pensions and can someone advise the pitfalls or if I'm missing anything?

Armitage.Shanks said:

Chums

the time has come that my FSAVC will pay out and as ever I'm confronted with several options some of which are excluded to me until I take financial advice!

Firstly we're not talking a 'big pot' but it's over the £30k threshold (just) requiring me to instruct a finnacial adviser, and it has a GAR.

I'm already in receipt of a very good pension so an 'additional' income of £155 gross per month for the rest of life (given it is not index linked) has limited appeal. Taking the max tax free lump sum (leaving £116 gross/month) makes sense to me given it would take c20yrs to accrue it through the monthly income extra if I didn't take it. I'm not confident of living another active 20yrs plus (despite good health) plus when/if I get the state pension in 12yrs that's more income to come.

GAR protects my payments for 5yrs but thereafter if I snuff it all is lost so its got me thinking. I like the idea of taking larger amounts every quarter/6 monthly but cannot with the 'standard' option. A fixed term annuity does not appear an option and I'm left with transfering the pot to a 'Retirement Account' which looks to be stock market invested in a 'cautious' fund. It would however let me take a min £500pm from it (subject to tax) as and when but presumably the fund is classed as my estate whilst the money is there? I'm already exposed to market funds so fluctuation doesn't necessarily bother me and buying in now given Brexit might not be a bad option.

Is this last option popular amongst those taking small free standing pensions and can someone advise the pitfalls or if I'm missing anything?

I would put this question to Nik on the Intelligent Money thread above. He knows pensions inside out.the time has come that my FSAVC will pay out and as ever I'm confronted with several options some of which are excluded to me until I take financial advice!

Firstly we're not talking a 'big pot' but it's over the £30k threshold (just) requiring me to instruct a finnacial adviser, and it has a GAR.

I'm already in receipt of a very good pension so an 'additional' income of £155 gross per month for the rest of life (given it is not index linked) has limited appeal. Taking the max tax free lump sum (leaving £116 gross/month) makes sense to me given it would take c20yrs to accrue it through the monthly income extra if I didn't take it. I'm not confident of living another active 20yrs plus (despite good health) plus when/if I get the state pension in 12yrs that's more income to come.

GAR protects my payments for 5yrs but thereafter if I snuff it all is lost so its got me thinking. I like the idea of taking larger amounts every quarter/6 monthly but cannot with the 'standard' option. A fixed term annuity does not appear an option and I'm left with transfering the pot to a 'Retirement Account' which looks to be stock market invested in a 'cautious' fund. It would however let me take a min £500pm from it (subject to tax) as and when but presumably the fund is classed as my estate whilst the money is there? I'm already exposed to market funds so fluctuation doesn't necessarily bother me and buying in now given Brexit might not be a bad option.

Is this last option popular amongst those taking small free standing pensions and can someone advise the pitfalls or if I'm missing anything?

As an (hopefully helpful) aside, pensions now fall outside of your estate for IHT purposes. You may also be be able to take tax free cash (PCLS, as it is now called) to reduced the value of your remaining pension so that it falls beneath the threshold now required for financial advice.

Nik is our new resident expert on these matters (Derek, Donkey and others can also be incredibly helpful with their knowledge and experience) so I would pop the question over to him and see what he says. You can always take it or leave it, but it costs you nothing!

Armitage.Shanks said:

Chums

the time has come that my FSAVC will pay out and as ever I'm confronted with several options some of which are excluded to me until I take financial advice!

Firstly we're not talking a 'big pot' but it's over the £30k threshold (just) requiring me to instruct a finnacial adviser, and it has a GAR.

I'm already in receipt of a very good pension so an 'additional' income of £155 gross per month for the rest of life (given it is not index linked) has limited appeal. Taking the max tax free lump sum (leaving £116 gross/month) makes sense to me given it would take c20yrs to accrue it through the monthly income extra if I didn't take it. I'm not confident of living another active 20yrs plus (despite good health) plus when/if I get the state pension in 12yrs that's more income to come.

GAR protects my payments for 5yrs but thereafter if I snuff it all is lost so its got me thinking. I like the idea of taking larger amounts every quarter/6 monthly but cannot with the 'standard' option. A fixed term annuity does not appear an option and I'm left with transfering the pot to a 'Retirement Account' which looks to be stock market invested in a 'cautious' fund. It would however let me take a min £500pm from it (subject to tax) as and when but presumably the fund is classed as my estate whilst the money is there? I'm already exposed to market funds so fluctuation doesn't necessarily bother me and buying in now given Brexit might not be a bad option.

Is this last option popular amongst those taking small free standing pensions and can someone advise the pitfalls or if I'm missing anything?

If I can give you some pointers, I’ll try. Firstly, a lot will depend what your retirement income needs are and the FCA is quite clear about points to be considered. Once you have started to identify your objectives, you first must consider how they can be achieved, the role played by safeguarded benefits (or potential safeguarded benefits, which you have touched upon - more below) in achieving them, and the consequential impact on those value of any course of action. the time has come that my FSAVC will pay out and as ever I'm confronted with several options some of which are excluded to me until I take financial advice!

Firstly we're not talking a 'big pot' but it's over the £30k threshold (just) requiring me to instruct a finnacial adviser, and it has a GAR.

I'm already in receipt of a very good pension so an 'additional' income of £155 gross per month for the rest of life (given it is not index linked) has limited appeal. Taking the max tax free lump sum (leaving £116 gross/month) makes sense to me given it would take c20yrs to accrue it through the monthly income extra if I didn't take it. I'm not confident of living another active 20yrs plus (despite good health) plus when/if I get the state pension in 12yrs that's more income to come.

GAR protects my payments for 5yrs but thereafter if I snuff it all is lost so its got me thinking. I like the idea of taking larger amounts every quarter/6 monthly but cannot with the 'standard' option. A fixed term annuity does not appear an option and I'm left with transfering the pot to a 'Retirement Account' which looks to be stock market invested in a 'cautious' fund. It would however let me take a min £500pm from it (subject to tax) as and when but presumably the fund is classed as my estate whilst the money is there? I'm already exposed to market funds so fluctuation doesn't necessarily bother me and buying in now given Brexit might not be a bad option.

Is this last option popular amongst those taking small free standing pensions and can someone advise the pitfalls or if I'm missing anything?

Any half decent adviser will do a proper cash flow analysis anyway, and will refer to the importance of ‘reliable income’ versus ‘essential outgoings’. Core reliable income may include your state pension, any DB benefits, annuities, various guaranteed third way products and, possibly, good quality rental income (although this is not as secure as others).

You say there are some guaranteed annuity rates under your policy, can you do a partial transfer (many people who say you have to transfer 100% are a bit muddled!)? Does it contain any other protected rights, are you able to take your retirement savings before Normal Retirement Age if you are incapable of carrying out your normal occupation, and what are the costs?

JulianPH said:

You may also be be able to take tax free cash (PCLS, as it is now called) to reduced the) value of your remaining pension so that it falls beneath the threshold now required for financial advice.

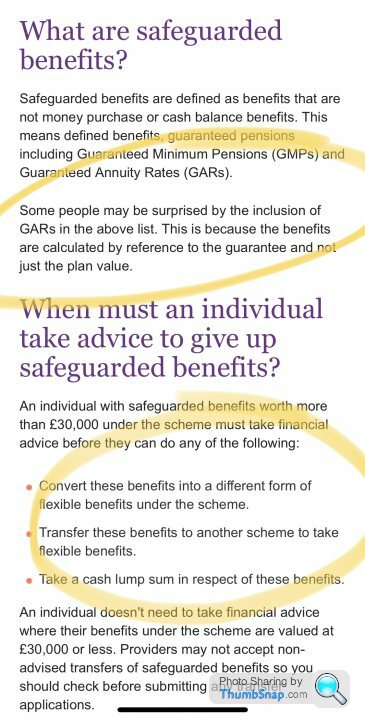

If there are *safeguarded benefits* linked to OP’s FSAVC then he’ll have to take advice as the value of his fund is over £30,000. Safeguarded benefits are defined as “benefits that are not money purchase or cash balance benefits". This means defined benefits of course, and guaranteed pensions including Guaranteed Minimum Pensions (GMP) and Guaranteed Annuity Rates (GAR). OP has declared GAR so he must also take suitably regulated financial advice. This means that advice must be taken if ‘just’ tax free cash is required, so taking PCLS in order to reduce fund size simply to avoid the need to take suitably regulated financial advice is not permissible. He must also do so if he wants to convert his fund into a different form of flexibility, or transfer his fund to another scheme to take flexible benefits.

The smoke and mirrors are strong in this thread.

If you need paid advice - get paid advice. It may not be big money but IMO the usual answer is to take your 25% tax free and then see how long you can live. If you're a 40% taxpayer that's just the way it is. No point sobbing about being well off.

As for the " not index linked" you could always transfer it somewhere else but index linking inevitably costs real cash money somewhere down the line. Which do you want, "money" or "money plus insurance"? Guess which is (on average) more expensive? Unsurprisingly it's the one with the "plus" in the sentence....

If you need paid advice - get paid advice. It may not be big money but IMO the usual answer is to take your 25% tax free and then see how long you can live.

If you're a 40% taxpayer that's just the way it is. No point sobbing about being well off.As for the " not index linked" you could always transfer it somewhere else but index linking inevitably costs real cash money somewhere down the line. Which do you want, "money" or "money plus insurance"? Guess which is (on average) more expensive? Unsurprisingly it's the one with the "plus" in the sentence....

rockin said:

The smoke and mirrors are strong in this thread.

If you need paid advice - get paid advice. It may not be big money but IMO the usual answer is to take your 25% tax free and then see how long you can live. If you're a 40% taxpayer that's just the way it is. No point sobbing about being well off.

As for the " not index linked" you could always transfer it somewhere else but index linking inevitably costs real cash money somewhere down the line. Which do you want, "money" or "money plus insurance"? Guess which is (on average) more expensive? Unsurprisingly it's the one with the "plus" in the sentence....

After the cost of obligatory advice, I wonder what you’d be left with. Never underestimate the value of five years worth of GAR. If you need paid advice - get paid advice. It may not be big money but IMO the usual answer is to take your 25% tax free and then see how long you can live.

If you're a 40% taxpayer that's just the way it is. No point sobbing about being well off.As for the " not index linked" you could always transfer it somewhere else but index linking inevitably costs real cash money somewhere down the line. Which do you want, "money" or "money plus insurance"? Guess which is (on average) more expensive? Unsurprisingly it's the one with the "plus" in the sentence....

https://citywire.co.uk/new-model-adviser/news/roya...

When I had a finanical review over 12 months ago I mentioned this FSAVC and the advice was if you don't need it leave it where it is and treat it as either paid up or keep paying in. That said the idea of a tax free bung now is appealing and whilst I've got the GAR it is only for 5yrs where presumably the remainder is written off when I snuff it at the +5yr point?

Whilst I could get some 'protection' by getting an annuity that give spouse cover, index linking etc. this defrays the monthly return making it about enough for a tank of petrol or some beer money.

If we were talking an additional 'income' of £250pm that would be a different ball-game, but tax paid I'm looking more like £80pm fixed for life. The issue of being forced to pay for financial 'advice' on how to decide an option given the amount doesn't sit right being as it's just over the £30k mandatory advice limit.

Whilst I could get some 'protection' by getting an annuity that give spouse cover, index linking etc. this defrays the monthly return making it about enough for a tank of petrol or some beer money.

If we were talking an additional 'income' of £250pm that would be a different ball-game, but tax paid I'm looking more like £80pm fixed for life. The issue of being forced to pay for financial 'advice' on how to decide an option given the amount doesn't sit right being as it's just over the £30k mandatory advice limit.

85Carrera said:

JulianPH said:

I would put this question to Nik on the Intelligent Money thread above. He knows pensions inside out.

Don’t you think it might have been appropriate to also let the OP know that you have a financial interest in Intelligent Money?Just by way of background:

1) We are not financial advisers and (like every other provider) could not accept a DB transfer over £30k without the member obtaining independent financial advice.

2) I was simply offering the OP access to a qualified and experienced person (and his G60 BD transfer qualified colleague, Paul) to get a free and impartial overview of his options assist in deciding whether it was worthwhile paying for advice (which he may find difficult to obtain on a small pot).

So I was simply trying to be helpful without seeking any financial reward, something I have been doing here for years.

Ginge R said:

If there are *safeguarded benefits* linked to OP’s FSAVC then he’ll have to take advice... OP has declared GAR so he must also take suitably regulated financial advice. This means that advice must be taken if ‘just’ tax free cash is required

This is a factually incorrect and a highly misleading statement regarding the requirement to pay for financial advice (ironically, made by a financial adviser).The OP has never stated that he is considering delaying taking benefits and so there is no requirement whatsoever for him to pay for financial advice in order to receive the tax free cash (PCLS) from safeguarded benefits - regardless of the amount of money involved.

He is also free to purchase an index linked annuity from another provider (should he wish) without, again, having to pay for financial advice.

Should he decide that he wishes to seek financial advice, or feels that he needs advice to help him make the right decision, he can obviously chose to do so but stating he has a requirement to pay for the services of you and your colleagues, when he does not, is part and parcel of people's mistrust of financial advisers.

As a financial adviser yourself, I would have hoped you were better informed. People make important (and expensive) decisions based upon what you say to them.

Those options above I don't need advice apparantly. However if I want to move the money into the company's own 'Retirement Fund' relying on cautious stock investments, value can rise/fall etc. allowing cash (taxed) access whenever I like I need to seek financial advice. This to me seems the better option as I'm not locked into an annuity which writes off the pot in lieu of a monthly pension.

Dear Julian,

Before 6 April 2015 firms without the pension transfer permission could have advised on plans with GARs. These firms now need to have the pension transfer permission. An adviser firm now needs to have the extended 'advising on pension transfers and pension opt-outs' permission to advise on transfers and conversions of safeguarded benefits to flexible benefits.

My post, which you have selectively drawn from, is explicit. I did not refer to an index linked annuity because that is not what AS was thinking of doing. If, as he stated, he wants “to convert his fund into a different form of flexibility, or transfer his fund to another scheme to take flexible benefits” then suitably qualified regulated financial advice *is* required.

The purchase *of an annuity* with safeguarded benefits is not considered to be a conversion. This means a client with a GAR can use these benefits to purchase a different shape of annuity without the need for advice where these benefits are worth more than £30,000. However, this is what AS states he wishes to avoid.

You suggested that taking tax free cash immediately before doing so, in order to avoid taking advice by diminishing the transfer value to sub £30,000 was a viable option. I said it wasn’t. My perspective remain extant.

FCA CP15/7 refers:

“We have considered whether advice on transfers from personal pension arrangements containing GMPs and other safeguarded benefits should be exempt from the requirement for a Pension Transfer Specialist. At this time, we will not exclude such activity from the requirement for a Pension Transfer Specialist. This is because the benefits may replicate or otherwise correspond to benefits under a DB scheme and may be more complex to assess.”

I have attached a screenshot each from Old Mutual and Royal London which may be useful. I hope you are well. Your name cropped up in the convivial of company this evening. I chatted with Tom the other day about some mutual clients of ours, who contacted me after a radio programme recently. He was most professional, please pass on my appreciation to him.

Before 6 April 2015 firms without the pension transfer permission could have advised on plans with GARs. These firms now need to have the pension transfer permission. An adviser firm now needs to have the extended 'advising on pension transfers and pension opt-outs' permission to advise on transfers and conversions of safeguarded benefits to flexible benefits.

My post, which you have selectively drawn from, is explicit. I did not refer to an index linked annuity because that is not what AS was thinking of doing. If, as he stated, he wants “to convert his fund into a different form of flexibility, or transfer his fund to another scheme to take flexible benefits” then suitably qualified regulated financial advice *is* required.

The purchase *of an annuity* with safeguarded benefits is not considered to be a conversion. This means a client with a GAR can use these benefits to purchase a different shape of annuity without the need for advice where these benefits are worth more than £30,000. However, this is what AS states he wishes to avoid.

You suggested that taking tax free cash immediately before doing so, in order to avoid taking advice by diminishing the transfer value to sub £30,000 was a viable option. I said it wasn’t. My perspective remain extant.

FCA CP15/7 refers:

“We have considered whether advice on transfers from personal pension arrangements containing GMPs and other safeguarded benefits should be exempt from the requirement for a Pension Transfer Specialist. At this time, we will not exclude such activity from the requirement for a Pension Transfer Specialist. This is because the benefits may replicate or otherwise correspond to benefits under a DB scheme and may be more complex to assess.”

I have attached a screenshot each from Old Mutual and Royal London which may be useful. I hope you are well. Your name cropped up in the convivial of company this evening. I chatted with Tom the other day about some mutual clients of ours, who contacted me after a radio programme recently. He was most professional, please pass on my appreciation to him.

JulianPH said:

This is a factually incorrect and a highly misleading statement regarding the requirement to pay for financial advice (ironically, made by a financial adviser).

The OP has never stated that he is considering delaying taking benefits and so there is no requirement whatsoever for him to pay for financial advice in order to receive the tax free cash (PCLS) from safeguarded benefits - regardless of the amount of money involved.

He is also free to purchase an index linked annuity from another provider (should he wish) without, again, having to pay for financial advice.

Should he decide that he wishes to seek financial advice, or feels that he needs advice to help him make the right decision, he can obviously chose to do so but stating he has a requirement to pay for the services of you and your colleagues, when he does not, is part and parcel of people's mistrust of financial advisers.

As a financial adviser yourself, I would have hoped you were better informed. People make important (and expensive) decisions based upon what you say to them.

The OP has never stated that he is considering delaying taking benefits and so there is no requirement whatsoever for him to pay for financial advice in order to receive the tax free cash (PCLS) from safeguarded benefits - regardless of the amount of money involved.

He is also free to purchase an index linked annuity from another provider (should he wish) without, again, having to pay for financial advice.

Should he decide that he wishes to seek financial advice, or feels that he needs advice to help him make the right decision, he can obviously chose to do so but stating he has a requirement to pay for the services of you and your colleagues, when he does not, is part and parcel of people's mistrust of financial advisers.

As a financial adviser yourself, I would have hoped you were better informed. People make important (and expensive) decisions based upon what you say to them.

Hi Al

You are talking about which advisers can advise on such things, I was talking about you stating advice was a legal requirement. The DWP states:

You are talking about which advisers can advise on such things, I was talking about you stating advice was a legal requirement. The DWP states:

Department for Work and Pensions said:

The following do not constitute transfers or conversions to which the advice requirement applies:

Cheers- payment of a pension commencement lump sum in respect of safeguarded benefits (that is, taking one-off tax free cash at the same time as starting to receive a pension)

- purchase of an annuity from another provider, rather than taking up a GAR offered by the member’s existing provider.

Armitage.Shanks said:

This pension is with Royal London by chance and what a PITA it is ringing them after being on hold for 30mins and now having to speak to the 'annuity department' who are likley to confirm I need advice for a 'fixed-term' annuity option or transfer out into their own Retirement Fund

Good luck!

JulianPH said:

Yes he was!

Different prisms. I am referring to the option of having to take benefits, flexibly. Armitage.Shanks said:

This pension is with Royal London by chance and what a PITA it is ringing them after being on hold for 30mins and now having to speak to the 'annuity department' who are likley to confirm I need advice for a 'fixed-term' annuity option or transfer out into their own Retirement Fund

Nowt wrong with RL - far from it - but be sure to ask them what happens to your fund charges once you go under c£28k. You may lose a rebate. Gassing Station | Finance | Top of Page | What's New | My Stuff